Growth Equity Update

February 2026 – Edition 47

• SaaS Apocalypse: In successive weeks the launch of Google’s Project Genie AI-generation tool led to a sharp selloff in shares of video games developers, the launch of Claude Cowork’s plug ins led to a sharp selloff in software, IT services and workflow tools stocks, and the four big hyperscalers have revealed plans to spend $650bn on 2026 AI capex, up from $390bn in 2025.

• SaaS who? The potential for AI to commoditise previously high-priced technical services and execution functions, and the pressing need for the AI hyperscalers urgently to recover their substantial AI investment, have been highlighted.

• End to gentle co-existence: The Stock Market has lurched from a view of existing industries’ peaceful coexistence with AI to a starker vision of AI potentially gouging out multiple industry business models (software developers, SaaS, workflow, consultancies, data providers, legal, media, advertising agencies, games developers, publishers, classifieds, price comparison, wealth management etc) as it seeks a return on its massive capital outlays.

• Rotation, not sell down: The FTSE Venture Capital Index is down 16% ytd, reflecting its read across exposure to ‘SaaS Apocalypse’ stocks. NASDAQ is down 1% ytd. Other leading world markets are up. This is market rotation, not sell down.

• Simple conclusions for growth equity. Enthusiasm for AI raises will remain high. Fundraising in software will become tougher. Given the scale of software raises this may, like in public markets, see rotation into non-AI affected real world assets and sectors. The impact of changes in private market valuations will be seen only slowly – this is a market of occasional not daily pricing.

• Appetite still strong: We continue to expect the value of growth equity raises to exceed 2025, both in the US and Europe. January saw US raises up 3x yoy in value and Europe up 8%. February has started well. We see $151bn of impending raises in the US and nearly $10bn in Europe

Download a PDF version of the Growth Equity Update

The SaaS Apocalypse and growth equity markets

‘Whoever fights monsters should see to it that in the process he does not become a monster. And if you gaze long enough into an abyss, the abyss will gaze back into you." Friedrich Nietzsche

The last three weeks have seen the public equity markets jolted out of their comfortable cohabitation with AI into renewed fears that AI advances will threaten the business models of a wide range of established industries.

Three things happened in quick succession

• In the last week of January there was a sharp selloff of shares in videogames developers after Google revealed its Project Genie AI-generation tool. This enables users to create ‘interactive environments’ in seconds using text prompts rather than coding. Take Two Interactive, Roblox, Unity Software and CD Project shares all fell by c10% in a day. At present the Google innovation is a time and facility limited ‘environment’ rather than a game creation vehicle, but Genie 3 has launched fears that world models could disrupt how video games are produced through fully automated game creation.

• The first week of February saw a substantial fall in the share prices of software, workflow and data businesses. The catalyst this time was the launch by Anthropic of eleven open-source plugins for Claude Cowork. Cowork is a digital workflow tool that allows non-technical users, such as finance, marketing, and consulting professionals, to use plain English text prompts to connect to various enterprise applications to perform complex tasks. Cowork can edit documents, build spreadsheets and slide decks, analyse data and automate workflows The equity market view was that such developments could commoditise the creation of enterprise software, erode competitive moats, pressure seat growth (revenues linked directly to the numbers of users) and reduce pricing power. The S&P500 Software and Services index fell 4% on Thursday February 5th and is down 16% ytd. A range of data related businesses, which combine proprietary datasets and workflow tools also fell sharply – led by Gartner down 24%, RELX down 15%, Wolters Kluwer down 13% and LSE Group down 10%. Advertising agency groups WPP and Publicis were down 11% and 9% respectively

• The third factor was the revelation in the same week over the results of the four big hyperscalers, Microsoft, Meta, Alphabet (Google) and Amazon that they plan to spend $650bn on AI capex in 2026. Alphabet announced capex of $175bn-$185bn on Wednesday 4th February and Amazon a $200bn plan the following day. Meta had already announced spend of $115bn-$135bn while Microsoft is on track for c$150bn. The cumulative c$650bn figure compares with c$380bn of expenditure in 2025 with the money going predominantly into data centres, AI semiconductors and servers. This level of spend is substantially ahead of initial expectations and has, in turn, impacted the share prices of these companies as the market concerns itself about the scale of the spend.

Put this also in the context of Open AI. This is a business which for its impending round is attracting a valuation of up to $830bn – about half the market cap of Meta. Open AI’s Sam Altman has talked about $20bn of annualised revenue at the end of 2025 (Source: The Information) and has talked about reaching $100bn annualised perhaps as early as 2027 and ‘hundreds of billions’ by 2030. Assuming the latter implies c$300bn by 2030 it would give OpenAI revenues about twice those of Meta (2024 revenue c$165bn). Sam Altman has stated that ‘You should expect OpenAI to spend trillions of dollars on data centre build outs in the not-too-distant future’ and most external estimates anticipate c$1.4 trillion in data centre and compute requirements in the next few years. OpenAI expects to grow fast and needs to do so. Some of its activities may create entirely new revenue streams. Much will have to be from the revenues currently enjoyed by somebody else.

Taken together these factors illustrate on the one hand the potential capability of AI to commoditise technical services and execution functions that have previously been highly priced, and on the other illustrate the pressing need for the AI driven businesses urgently to recover their substantial AI related investment.

An example of the first. This exhibit is from the Klarna Q3 2025 results presentation. The footnote reads ‘Estimated by McKinsey and Claude. Claude was significantly cheaper.’

It’s a simple illustration. The market had been travelling along with an AI and existing industries gentle co-existence narrative. Analysts and strategists were outlining baskets of relative AI winners and losers, companies were talking about how AI would infuse their businesses, allow efficiencies, some of which would be shared with customers and some of which would drop through to the bottom line. The story was humans with AI will replace humans without AI.

The narrative has now lurched to a much starker vision of the future. In this blasted heath version of AI disruption, the gentle coexistence is replaced by an AI industry which attempts to gouge out the functionality and value added of traditional business models, laying waste to the industries and companies that previously occupied these roles.

‘They're coming to get you, Barbara’: And this is not to be confined to software and services businesses in the direct path of the AI revolution using vibe coding to replace traditional programming skills. AI in this vision is coming for all the client industries in workflow, services, execution and analysis where a proprietary moat does not exist. It implies that AI is coming for a broad range of industries beyond software developers, IT services, and workflow tools. As the market has digested the potential implications, share prices in consultancies, data providers, legal services, media, publishers, advertising agencies, classifieds, price comparison, wealth management and other professional and business services have declined.

The sell off has spawned a wave of dramatic headlines - ‘Selloff wipes out nearly $1 trillion from software and services stocks’ (Reuters); ‘$300 billion Evaporated: The SaaS-Pocalypse has begun’ (Forbes); ‘AI fears pummel software stocks’ (CNBC).

The broader market remains relatively unruffled. The S&P500 is up 1% ytd and is up since the day of the Anthropic announcements. Markets outside the US are robust with the FTSE 100 and the STOXX 600 up 5% ytd. Even the tech heavy NASDAQ, home to perceived AI winners and losers, is down just 1% ytd.

Rotation, not sell off: So, this is not a market sell off. It is a rotation away from software, IT and professional services stocks. Other sectors are outperforming. The dust will settle on which sectors will outperform but there are a few visible trends going on in markets.

Banks, Tanks and basics: The rotation has been into industries deemed unaffected by AI and driven by other positive fundamentals. Bank stocks continue to perform strongly on both sides of the Atlantic. Defence stocks, driven by heightened geopolitical tensions and by the impulse for Europe to rearm in the face of the Ukraine war and the JD Vance March 2025 Munich speech unravelling the US protective defence commitment, have soared after years of relative neglect. The same impulse that Europe must form its own future more independent of the capabilities of the US and China has also been prevalent. It was a key theme in the Mark Carney ‘rupture’ speech and has convinced manty fund managers that industrial and basic industries will be rebuilt in Europe – and in the US – and that this means a focus on heavy ‘real world assets’ – manufacturing companies and potential beneficiaries of a potential bigger industrial capex cycle.

Risk and uncertainty: “Uncertainty must be taken in a sense radically distinct from the familiar notion of Risk, from which it has never been properly separated.... It will appear that a measurable uncertainty, or "risk" proper.... is so far different from an unmeasurable one that it is not in effect an uncertainty at all.”

Frank Knight, of the ‘Chicago School’ of economics argued that risk is observable and measurable. While risk may be undesirable, the probability and potential impact of an event can be defined and its outcomes assessed and measured through having adequate knowledge via the observation of past events.

Uncertainty, by contrast, is where possible outcomes are not known to us and we do not have the knowledge or experience to assign probabilities for possible outcomes and impacts. There is no ability to determine the appropriate response based on rational calculations.

Fund managers can cope with risk; they can’t deal with uncertainty.

Risk can be assessed, quantified and a measured approach can be taken balancing risk and valuation, calculating ‘what’s implied by the price’ and assessing outcomes and relative desirability.

Uncertainty, of the type created by the onrush of potentially far-reaching AI developments, makes these assessments virtually impossible and investment in affected sectors a shot in the dark. And in turn this is why, despite a flurry of sell side commentary arguing that perhaps the status quo is not so upset, the shares in the sectors most impacted are not recovering their steep falls. Rather than shoot in the dark fund managers prefer to go to those real-world sectors where the impact of AI is remote.

It feels like this is where we are now with the impact of AI innovation. The vast sums being thrown at the industry, scaling up at an unanticipated pace, the lack of guidance about where the returns on this investment are to be made ( OpenAI gives few clues where its $100s of billions of revenue are to come from) combined with a flurry of threatening ( for established industries) product announcements and a lack of knowledge and experience of the AI industry as to what will come next and when (albeit an expectation that innovations will be rapid and dramatic) means that asset managers are cautious.

What does this mean for growth equity markets? There is a point to writing about this in the context of growth equity. A few, simple, conclusions can be drawn.

The power of AI: As we know AI and related raises dominated the growth equity market in 2025, furnishing 57% of the value of raises in the US. The top eight raises by value in the US were for AI businesses. The trend has continued into 2026 with already a $30bn raise for xAI, a $16bn raise for AV business Waymo, a $1.4bn raise for Skild AI in robotics and $1bn for AI infrastructure business, Cerebras. With the market viewing AI LLMs as the businesses of the future the wave of interest in these and AI innovation businesses will remain very strong.

The price/valuation impact in private markets is delayed: Public markets display a visible, daily traded price level in quoted assets. Liquidity and size issues can mean that the quoted price on the screen does not fully reflect perceived valuation, but a share price acts as a daily real-time barometer of the market’s view.

Such is not the case in private markets. Here price formation accompanies fund raising rounds. These are occasional and irregular. Where a company’s valuation stands in between rounds can only be dimly perceived, with views being formed in relation to the company’s perceived progress since the last round, valuations amongst comparator public companies, valuations achieved by comparator companies in other private rounds or by the price levels in very thinly traded and occasional secondary markets.

The experience of 2022 and its aftermath is instructive. The public markets fell back rapidly at the start of the year on the impact of the Ukraine war, rising inflation and the upwards turn of interest rates. The global growth equity market peaked in fund raising terms and valuations in 2021, but momentum carried it forward strongly in H1 2022, partly due to the time lag between the start and end of rounds, even as public valuations for equivalent businesses were falling. The chart illustrates the relative strength of Q1 and Q2 2022 fundraising for growth equity companies even as growth managers like Matt Turck of Firstmark were sending out alarm signals.

“Right now, the start-ups that are in the trickiest situation are growth-stage start-ups with unicorn-type valuations, a high burn rate, good but not great metrics, and 12 months of cash. You're going to see a lot of layoffs there, because companies need to urgently cut their burn if they don't want to run out of cash.” (Matt Turck, Firstmark, quoted in WIRED – June 2022)

Global Growth Equity deal activity by quarter- H1 2022 remained strong

Are we are seeing a similar phenomenon now? In the last few days Databricks has raised $7bn ($5bn equity, $2bn debt) at a valuation of $134bn. Its platform is designed to help users ingest, analyse and build AI applications using complex data from different sources. Its closest public comparator is Snowflake, a $60bn market cap business who shares are down 18% since the start of February and 35% since its recent peak at the end of October.

RELX, the £40bn market cap professional data supplier with a growth business in AI and machine learning derived tools in the Legal, Science and Risk markets has seen its shares drop by 22% since the start of February and by 51% in the last year despite improving growth rates in revenue and EBITA.

The debate in this company has been fear that its growth potential in workflow tools would be cut away by new AI based companies offering similar tools, notably Harvey AI. Indeed, Harvey AI is both competitor and partner having struck a deal with RELX which allows its customers to interface seamlessly to RELX to access, as RELX customers, its proprietary data lake of legal information.

Harvey is thus a legal workflow tools business making the jobs of legal professionals more efficient with its products streamlining workflows in areas including contract analysis, due diligence, compliance, and litigation. This is one of the areas addressed by Anthropic and Claude Cowork’s new plug-ins. Its legal plug-in allows users to review documents, flag risks and track compliance.

Yet Harvey is reported in the press to be raising $200m at an $11bn valuation just months after raising $160m at an $8bn valuation. The underlying equity story for Harvey may be as strong as that for RELX - that its knowledge of workflows, the usefulness of its tools and the critical accuracy required by legal users means that in the real world its functionality may not be impinged on by generalist AI tools. Nevertheless, the contrasting fates of the public company RELX, down 50% with a loss in market capitalisation of $49bn in a year and that of Harvey – a valuation gain of $6bn (+120%) since its $5bn valuation at its June 2025 Series E – is stark.

The impact on growth equity raises in software: The next exhibits show the sectors in which growth equity was raised in 2025. They indicate that Software was the second largest value category in US growth equity raises in 2025 with $14bn raised over 72 deals. In Europe Software was the largest category with $7.5bn raised over 113 deals.

The across-the-board enthusiasm for software deals is likely to be re-examined in the aftermath of the public market sell off. Software and SaaS raises will be scrutinised even more fiercely under the lens of their potential vulnerability to AI led disruption.

The same factor is already being seen in the private equity market, which is also a big investor in software companies. The prices of publicly quoted private equity businesses have been under pressure, with the relative scale of the falls approximating to their perceived exposure to software assets. While the underlying current performance of software companies may remain strong, the uncertainty will feed into valuation and potentially investor appetite. Quoted in the FT John Zito, Co-President of Apollo Asset Management, cites the uncertainty factor as predominating:

“This is not just ‘nothing to see here’. This is a logical repricing of terminal value, of forward growth, of heightened uncertainty.

US Growth Equity in 2025 – Software the second largest sector by value of raises

European Growth Equity in 2025 – Software the largest sector by value of raises

Growth equity sector rotation: An interesting feature of the market’s sudden adoption of the scale of the potential disruptive effect of AI on software, services, IT and related industries is the potential broadening of the growth equity market.

The nature of the venture model is that it induces clustering. The growth manager identifies an investment theme – the rise of AI is a classic one – and commits capital across a number of investments in that theme. The nature of venture is that the bulk of returns are made from a small fraction of the investments and so clustering around a strong theme to raise the chances of hitting the ‘fund returner’ business is logical. Thus, AI in 2025 captured 57% of US deal value. Software was second with 6%.

Not just money but attention is captured in the same way. It is common for early-stage companies outside the ‘hot sectors’ to say that they are struggling to gain an audience or attention for their proposition. Venture and growth investors are focused on a narrow range of industries or verticals in those industries to capture the companies that will provide the bulk of future returns. Thus, in vogue sectors like AI and software have the effect of sucking the oxygen of attention away from other sectors.

There is room for rebalance here. The possibility – and for some the opportunity – is that investor attention may broaden. Just as the public market investors are paying renewed attention to ‘banks, tanks and basics’ so we may see a broadening tend in private markets and a greater attention to non-AI impacted sectors.

Growth Equity – Reflecting on the 2025 trends

Picking out some of the leading growth equity trends

Pitchbook/ NVCA has published its definitive 2025 Venture Monitor looking at trends in the US venture capital ecosystem in 2025. We covered much of this territory in our own review of 2025 in the January Growth Equity Update. Pitchbook though makes for interesting reading and has some compelling charts. Picking out a few of these:

2025: A strong year of fundraising: As we have observed frequently, 2025 was a very strong year for US VC fundraising. The Pitchbook data indicates a value of $339bn of US VC raises across 16,700 deals. Since 2015 this figure has only been beaten by the $358bn of the top-of-the -market year in 2021.

US VC Deal value – 2025 behind only 2021 in the last decade

VC fund raising though depressed: At the same time, as we have regularly observed, the level of fund raising by VC firms has been very depressed. The funds raised have been concentrated into fewer, larger firms. The next chart illustrates this trend.

US VC fundraising peaked in 2022 with $223bn being raised across 1,777 funds. The next three years combined have seen just $273bn being raised. 2025 saw only $66.1bn being raised, the weakest year of fundraising since the $49.8bn of 2017. It was just 65% of the total raised in 2024.

US VC fundraising remains depressed

M&A and IPO trends offer hope of better liquidity: The reasons for this low level of fund raising are well rehearsed. In recent years a depressed exit market in both M&A and IPOs has reduced liquidity for LPs. There are some signs of this improving in 2026 with IPO activity picking up. M&A exits improved in 2025. Overall, 2025 was a better year for exits, the fourth best in the last decade. Although still well below the levels of 2019-21 this does offer some encouragement for 2026.

2025 - US VC exit activity improved from a low base

Squaring the circle: Meanwhile how to square the circle of substantial deployment of venture capital money in 2025 with the relative trickle of new money coming into VC funds?

The answer lies in the concentration of VC funding in a few large rounds and in the type of investor seen participating in those rounds. The process is that VC raises, and particularly the largest VC raises, have been dominated by AI companies.

In turn those AI businesses have had the support of some of the biggest professional VC investment firms – the likes of a16z, Softbank, Sequoia, Founders Fund and Lightspeed, as well as a breed of successful dedicated AI investors that have emerged such Thrive Capital and Khosla Ventures. This partly explains the concentration of LP funds into the largest venture firms. Everybody wants to play the AI wave; the most attractive AI raises are dominated by a few big firms; and so, the LP money flows disproportionately to those firms.

The other factor is the presence of major corporates, both directly and via their VC arms. We have tracked the rise of NVIDIA for instance as a major player across a range of AI related industries investing both directly and through its venture arm NVentures. It seems almost omni present in recent tech raises and is playing a substantial role in propping up the entire VC ecosystem. Similarly, other members of the Magnificent Seven, for whom AI is now the touchstone of their future success, have become major players in the biggest VC rounds, providing an atypical source of funds for the VC market.

Let’s illustrate this with a couple of charts. Our Rothschild & Co Deals Monitor tracks US VC deals valued at $100m or more. We recorded 487 US growth equity deals of $100m or more in 2025 raising a total of $234.1bn. AI dominated with 84 AI deals raising $132.6bn, 57% of the annual total. The top ten deals in 2025 cumulatively raised $106.5bn, 45% of the annual total. Of these eight were for AI businesses.

US Top 10 deals by value in 2025 – top eight were for AI businesses

The presence of major corporates is marked.

• Microsoft was a major investor in the $40bn raise for Open AI in March and is believed to have a 27% stake in the business. It is also an investor in Anthropic, committing $10bn to its $15bn round in October 2025. It was an early investor in the French LLM Mistral.

• NVIDIA invested $5bn in Anthropic in the same October 2025 round. In its strategic partnership with Open AI announced on September 2025, Open AI committed to deploy at least 10 gigawatts of AI data centres with NVIDIA systems representing millions of GPUs. In return NVIDIA expressed an intent to invest $100bn in OpenAI as the new NVIDIA systems are deployed. This means that, with Open AI engaged on a fresh $100bn raise right now, NVIDIA has indicated that it may invest as much as $20bn in OpenAI ‘s current $100bn round.

• Meta was the sole investor in the $14.3bn round raised by Scale AI In June 2025, with the deal designed to secure high quality training for LLM models and giving Meta 49% of the company.

• Google made a $1bn investment in Anthropic in June this year, following its $2bn investment in October 2023 and its investment in the initial $450m round in May 2023. It has also led rounds in Sandbox AQ and A121 Labs.

• Amazon has led three rounds for Anthropic – in September 2023 and March and November 2024.

The UK National Wealth Fund – Unlocking the UK’s Future

The UK National Wealth Fund, the UK government’s principal investor and policy bank with £27.8bn of capital, has just launched its new five-year strategic plan to 2030/31. It is subtitled, ‘mobilising finance, unlocking growth’. The NWF, which is funded by taxes and borrowing and is one of several government-backed investment funds alongside the British Bank and Innovate UK, focuses on the government’s economic growth and clean energy missions. Its approach is threefold

• Unlocking growth opportunities on the pathway to clean energy

• Accelerating place-based investment across all four nations of the UK

• Strengthening sovereign and strategic capabilities.

The National Wealth Fund’s mission is to invest in capital-intensive infrastructure, supply chains and businesses across the UK, to drive more than £100bn of finance to promote long-term economic growth.

Thus far it has deployed £8.4bn investing in over 70 companies, projects and local authorities across the UK, bringing in over £17bn of private finance. With HM Treasury pursuing its growth goal, the pace of investment from the NWF has accelerated and it has shown a higher risk appetite. It is now making more equity investments ‘targeted where they can have a catalytic impact.’ It is also becoming active across a broader range of sectors, including frontier and foundational industries, to support the UK’s Industrial Strategy.

It has selected 25 sectors – from innovative technologies to strategic infrastructure – where it will be active, and which it feels have the potential to drive forward the UK’s long-term economic growth and energy transition. Within these, the NWF has identified ten sectors where it expects to have the most substantive ‘catalytic’ opportunities to support sectors. These are:

• Ports & supply chains

• Carbon capture, usage and storage

• Hydrogen

• Battery manufacturing & the electric vehicle supply chain

• Steel

• Power grid

• Energy storage

• Nuclear

• Transport infrastructure

• Place-based regeneration

In these sectors, the National Wealth Fund will aim to commit £5.8bn collectively over this strategy period.

There are a further 15 sectors in which the NWF will pursue investment opportunities which target high growth, innovative projects and businesses and accelerate the delivery of core infrastructure. These are:

• Artificial Intelligence

• Semiconductors

• Quantum technologies

• Defence

• Advanced materials

• Life sciences

• Critical minerals

• Aerospace supply chain

• Sustainable aviation fuels

• Water

• Offshore wind

• Retrofit

• Solar

• Heat networks

• Electric vehicle charging

With its investments the NWF looks at the potential to unlock further significant finance over time, co-investing with the private sector to crowd in finance throughout the lifecycle of individual investments. Its private investments typically exceed £100m and must be a minimum of £25m.

The NWF will provide growth capital to scale up businesses ‘with proven technologies, credible business plans, and strong management teams.’ Its focus is on later funding rounds. It will take minority positions in companies, wants to invest alongside institutional investors and typically does not want to be the largest shareholder.

The NWF declares that it is not an investor in third party investment funds. This marks a shift of approach. Previously, when the fund was known as the UK Infrastructure Bank, it did make such investments.

Having already deployed £8.4bn and with total funds of £27.8bn the NWF says that it aims to deploy all its funds by 2030/2, implying an investment rate of c£4-5bn pa. The NWF’s strategic plan can be found here.

national-wealth-fund-five-year-strategic-plan.pdf

Public markets - Rotation

To the 12th of February, the FTSE 100 and the STOXX 600 are up 5%, the S&P 500 is up 1% and the tech heavy NASDAQ is down 1%. The FTSE Venture Capital Index, which replicates the performance of the US venture capital industry using liquid, publicly listed assets are down 16% ytd, reflecting the read across exposure of this index to ‘SaaS Apocalypse’ impacted stocks.

The most recent BoA Global Fund manager survey published in mid-January indicates a still very upbeat attitude amongst global fund managers. Notably there has been a surge in optimism on the macro-economic outlook around growth and profits.

• A net 38% respondents expect a stronger economy, the highest reading on this measure since July 2021.

• Expectations for a ‘boom’ are the highest since September 2021 at 34%, and its corollary, expectations for a recession, at 9% are the lowest since January 2022.

• The base case expectation for the global economy is now neither a soft landing nor a hard landing but rather ‘no landing’ at 49% of respondents.

• A net 44% of respondents expect global profits to improve in the next 12 months, also the highest since July 2021.

• In line with this global investor sentiment is at its most optimistic level since July 2021.

• The greatest risks are seen as a geopolitical conflict (28%) and ‘AI bubble’ at 27%.

First time in three years investor base case is ‘no landing’ for the global economy

The survey was carried out between January 9th and 15th meaning that it predated the AI fear induced turmoil in software and related shares. Nevertheless, it is interesting to see that signs of sectoral rotation were already emerging. The survey shows investors increasing allocation to banks, healthcare, and insurance and reducing allocation to energy, utilities and technology. Interestingly, and reflecting a potential broadening of the market, investor optimism that large capital will outperform small caps has been neutralised and was at its lowest level since January 2025.

It is notable within all this that expectations about potential US interest rate cuts have faded. The appointment of Kevin Warsh as the new chair of the Fed has been viewed as the installation of a credible operator who is serious about controlling inflation. He is seen less as a likely zealot of interest rate cuts and more as a candidate who will limit the Fed’s remit and reduce quantitative easing and the size of the Fed’s balance sheet.

For the moment the Fed remains in the hands of the ancient regime of Chair Jay Powell, and hopes of immediate interest rate cuts are relatively low given the combination of signs of buoyancy in US economic growth (GDP growth was +4.3% in Q3 2025), inflation well above target at 2.7% in December, and an unexpectedly strong January jobs report which saw a net addition of 130,000 jobs and a drop in the unemployment rate from 4.4% to 4.3%.

When holding interest rates flat at its January 28th meeting Jay Powell observed that the US jobs market was showing ‘evidence of stabilisation’ and the market’s view is that the buoyancy of the economy and the relative strength of the jobs market combined with inflation stubbornly above the 2% target is likely to mean that the Fed will not make further rate cuts under the current chairmanship. His term runs out on May 15, 2026. President Trump in December 2025 meanwhile made it clear that a ‘litmus test’ in his choice of the new Fed chair would be their willingness to cut Fed rates.

The current Fed rate is at 3.5%-3.75%. The next Fed meetings are on March 18th (Fed Watch has an 89% chance of no rate change) and 29 April (79% no rate change). The June 17 meeting – the first under the new Fed chair- sees the expectation of unchanged rates fall to 40% with a 60% chance of a rate cut (49% of 25bps, 11% of 50bps).

The current most favoured anticipated rate at the end of 2026 (the last meeting of the year is 9 December 2026) is unchanged at 3%-3.25%, suggesting the market’s core expectation is 50bps of rate cuts in 2026. The market likes the combination of economic growth and lower rates.

UK interest rates: The last BoE meeting of 2025 on 18 December cut rates by 25bps to 3.75%. The first of 2026 on February 5th held rates steady, but it was a close-run thing with the Monetary Policy Committee in a 5-4 vote to hold rates. The MPC was relatively more optimistic around inflation. The December reading was at 3.4% but the MPC anticipates it falling back to 2.1% in Q2, faster than it had expected in its November report. The Bank of England also lowered its GDP growth forecasts. UK GDP growth was 0.1% in Q4 2025 meaning it reached 1.3% for 2025. The BoE has reduced its 2026 GDP forecast to 0.9%.

After its decision to hold rates flat at the February meeting the Governor of the Bank of England, Andrew Bailey commented,

‘Overall, the risks from inflation persistence appear to have continued to reduce. I therefore see scope for some further easing of policy. This does not mean that I expect to cut Bank Rate at any particular meeting. I will go into the coming meetings asking whether a cut is justified.’

This has sparked expectations of a 25bps rate cut at the March meeting. The market expectation is for interest rates to come down by 50-75bps to 3.0%-3.25% by the end of 2026.

European interest rates: As expected the ECB held rates steady at its February 12 meeting. The message coming out of the ECB in the last few months has been one of interest rates, now at 2%, having reached an equilibrium after a period of sharp rate cutting. ECB president Christine Lagarde observed after the October meeting that EU monetary policy is ‘in a good place’ and that the outlook for inflation is ‘broadly unchanged’. Actually, the January print for inflation, at 1.7% was lower than expected – consensus was at 2%. The ECB commented that its

“… updated assessment reconfirms that inflation should stabilise at its 2% target in the medium term. The economy remains resilient in a challenging global environment. Low unemployment, solid private sector balance sheets, the gradual rollout of public spending on defence and infrastructure and the supportive effects of the past interest rate cuts are underpinning growth.”

The market consensus looks for interest rates to remain unchanged through 2026.

Our Rothschild & Co strategists Kevin Gardiner and Anthony Abrahamian note that stock valuations are high versus history, particularly in the US but that 2026 earnings growth, anticipated at 14% is also poised to be strong.

Valuations are dear but earnings growth has been healthy, so far

Their views on the current market outlook are summarised in the Exhibit.

Fundraising outlook: c$160bn of potential raises

The pipeline keeps replenishing

Our Deal Monitor at the start of the year indicated $159bn of impending raises. Despite substantial activity in January the total has held steady at $160bn as we move through February. Of this we identify c$151bn of impending US deals and c$10bn in Europe.

The key component of the US list remains the intended $100bn raise at OpenAI at an $830bn valuation. The intention is to close the round by the end of Q1 with NVIDIA, Microsoft, Amazon and sovereign wealth funds targeted as potential investors.

Autonomous vehicle company Waymo has just announced a raise of $16bn at a post money valuation of $126bn led by Alphabet with support from Dragoneer, DST Global, Sequoia, Andreessen Horowitz and Mubadala Capital. Its previous funding round was $5.6bn at a $45bn valuation in October 2024.

Anthropic, which raised a total of $32.5bn across three deals in 2025 is reportedly planning a further $20-25bn raise at a valuation of $350bn. GIC and Coatue Management are said to be leading the raise.

While the size of the putative Anthropic raise has increased, that for Tether, the stablecoin issuer, has decreased. Reports suggest that its hopes of raising $15-$20bn at a $500bn valuation have been tempered. The company is now reported to be seeking a $5bn raise at a similar valuation.

Robotics business SkildAI which has raised $1.4bn from Softbank and NVIDIA moves off the US list.

US Growth Equity – c$151bn in reported upcoming raises

In Europe the list is headed by the expected $2bn raise for autonomous vehicles business Wayve, led by NVIDIA, Microsoft and Softbank, and $2bn for the French AI coding business Poolside led by Magnetar and NVIDIA. Italian AI infrastructure business, Domyn, is said to be raising $1.15bn.

Advanced Machine Intelligence (AMI) Labs led by Yann LeCun, who was the key architect of Meta’s AI strategy, is looking to develop ‘world models’, sophisticated, forward thinking AI systems capable of planning complex actions. This intended ‘talent raise’ will be based in Paris and is looking at an initial $585m raise at a $3.5bn valuation.

After recent raises Kraken, Parloa, Pennylane and Harmattan move off the list.

European Growth Equity – c$9.7bn in reported upcoming raiseS

January’s growth raises

US off to a flyer, Europe beats tough comp

January saw US growth equity raises off to a very strong start. Fuelled by the long awaited $20bn raise for xAI our Rothschild & Co Deal Monitor recorded $34.3bn in raises of $100m or more in the month. This was 3x the level of raises recorded in January 2025 and 9x the value of raises in January 2024.

It will come as no surprise to learn that AI related raises led the way. These accounted for €23.8bn, 69% of the total. After xAi the biggest raises were from autonomous vehicles software business, Waabi of Canada which raised $750m in a Series C led by Khosla Ventures. AI semiconductor business Etched raised $500m in a round led by Stripes. Humans&, an AI frontier lab focused on human centred AI systems raised a $480m seed round led by SV Angel, NVIDIA, Jeff Bezos and Google Ventures. As a sidenote NVIDIA was again very heavily represented in the largest AI and related raises in January 2026, including a presence in each of the top three deals.

AI related deals continue to be prominent. Notably $1.5bn was raised in Robotics led by the $1.4bn Series C for SkildAI led by Softbank and NVentures. Skild is developing an ‘omni bodied’ brain to operate any robot for any task.

Biotech continued to be well represented with eleven rounds raising a total of $2.1bn led by the $305m Series F of cancer drugs specialist, Parabalis Medicines. The recent trend of seeing VC money diverted to defense companies continued with $886m raised across four companies. The largest raise here was the $450m for the defense materials business, Atlantic Alumina, an alumina foundry with the raise led by the US DoD.

US and Canada – 62 deals raised $34.4bn in JANUARY

In Europe 51 deals raised a total of $5.3bn in January, nudging past the $4.9bn raised from 65 deals in January 2025, which was the third biggest value month in 2025. The biggest deal was the $1bn raised for Octopus Energy spin out Kraken which was valued at $8.65bn. Kraken, the ‘modern operating system for utilities’ supplies energy software to utility companies. The round was led by D1 Capital, Fidelity International and Teachers Ventures.

The Kraken raise meant that software was the biggest sector by value in January with $1.67bn raised. Other notable raises here were $300m for the Dutch travel and hospitality software business, Mews and $205m for the French accounting software business, Pennylane.

AI raises at $649m edged out Biotech ($639m) for second spot. Parloa, the German agentic AI business led the way with a $350m Series D led by General Catalyst and EQT Ventures. In the UK Synthesia, the SaaS platform for AI content generation, raised $200m in a round led by Google Ventures. AI related raises totalled a further $295m across semiconductors, quantum, robotics and legal tech. The largest of these raises was $100m for the German modular manufacturing robotics business, Robco.

As in the US defence raises maintained their recent pace with three deals raising $463m. Autonomous defence systems business Roark raised $210m in a Series B. French strike and surveillance drones’ business Harmattan raised $200m in a round led by Dassault Aviation which valued the business at $1.4bn.

Europe – 51 raises of $20m + in January for a total of $5.3bn

Our views on the state of the venture capital markets

October 12, 2022, marked the low point for the S&P500 on the back of global inflation, rising interest rates, and increased geopolitical risk. It also ended the buoyant market conditions for the venture capital market that saw its activity and valuations peak in late 2021.

October 12, 2025, marked the third anniversary of the bull market that has seen the S&P500 rise by almost 90% and NASDAQ by 120%.

In that period the FTSE Venture Capital Index was up by almost 170% and since June 2025 has been back above its previous 2021 peaks.

This revival of the growth equity market has been led by the US and by a surge of interest in artificial intelligence model providers and for companies using AI to transform a range of underlying industries.

Ast the same time the venture industry has re-adopted strong underlying approaches to investment with companies in most sectors striving to achieve a better balance of growth, profitability and cash flow. The underlying quality of the cohort of VC backed companies has improved.

Our summary of the outlook

• There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, quantum, semiconductors, new energy sources like nuclear and fusion) supporting the development of AI.

• The influence of AI is percolating through many other industries such as drug discovery, defence, robotics, legal tech, autonomous vehicles, and cybersecurity fuelling a broader advance in the growth equity market.

• Overall, the VC market is regaining confidence with the strength of interest with fintech, blockchain/crypto and biotech reviving strongly.

• There is a burgeoning interest in defence industries from investors with both the tense geopolitical political environment, the advances in AI applications and the experience of the combat in Ukraine contributing to investor focus. By contrast, Climate Tech, while still a substantial sector has become less prominent both as a result of some high-profile failures and being less favoured politically in the US under the current administration.

• Fund raising for venture capital firms remains subdued. Fund raising is concentrating into larger, established firms. US VC fundraising in 2025 was concentrated in larger firms and at near decade lows.

• The speed of the investment process has slowed down since 2021-22. The level of diligence on deals has stepped up. This is true even in the ‘hot’ parts of the market like AI. Outside these areas it is marked – processes take time, downside protection is sought.

• Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on the combination of growth and profitability (or a rapid path to it) and on free cash flow.

Read the previous editions: May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024, January 2025, February 2025, March 2025, April 2025, May 2025, June 2025, July 2025, August 2025, September 2025, October 2025, November 2025, December 2025, January 2026

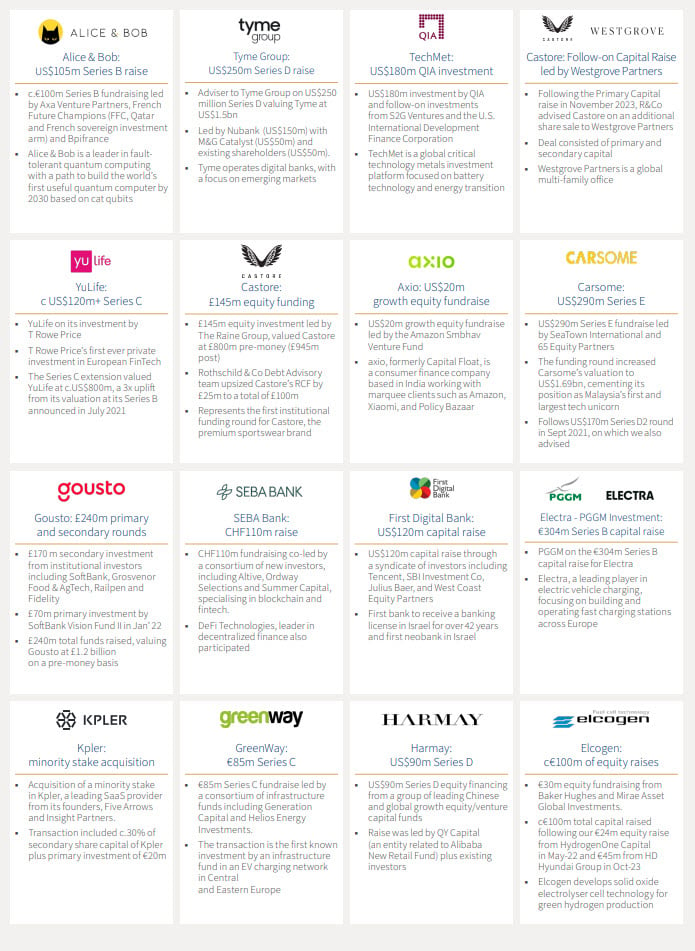

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Mark Connelly

Co-Head of Global Market Solutions

+1 212 403 5500

+1 917 297 5131

Chris Hawley

Global Head of Strategic and Private Investors.

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Capital Markets Europe

+44 20 7280 5088

+44 7542 477 291

Antoine de Guillenchmidt

Co-Head of Equity Capital Markets Europe

+44 20 7280 5377

+44 7907 712 978

Pete Nicklin

Co-Head of Equity Capital Markets Europe

+44 20 7280 1668

+44 7912 395 294

Laura Klaassen

Head of Private Distribution

+44 7926 905 488

Thomas Chung

Head of Private Capital, North America

+1 212 403 5559

+1 917 594 7208

Tim Brenton

Director of Private Distribution

+44 20 7280 1351

+44 7788 395 556

This document is being provided to the addressed recipients for information only and on a strictly confidential basis. Save as specifically agreed in writing by Rothschild & Co Equity Markets Solutions Limited (“Rothschild & Co”) this document must not be disclosed, copied, reproduced, distributed or passed, in whole or in part, to any other party.

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.