Growth Equity Update

May 2024 - Edition 26

- ‘Pandemic era winners suffer $1.5trn fall in market value’ according to the FT, citing 50 corporate winners from the pandemic era that have lost $1.5trn in value since the end of 2020.

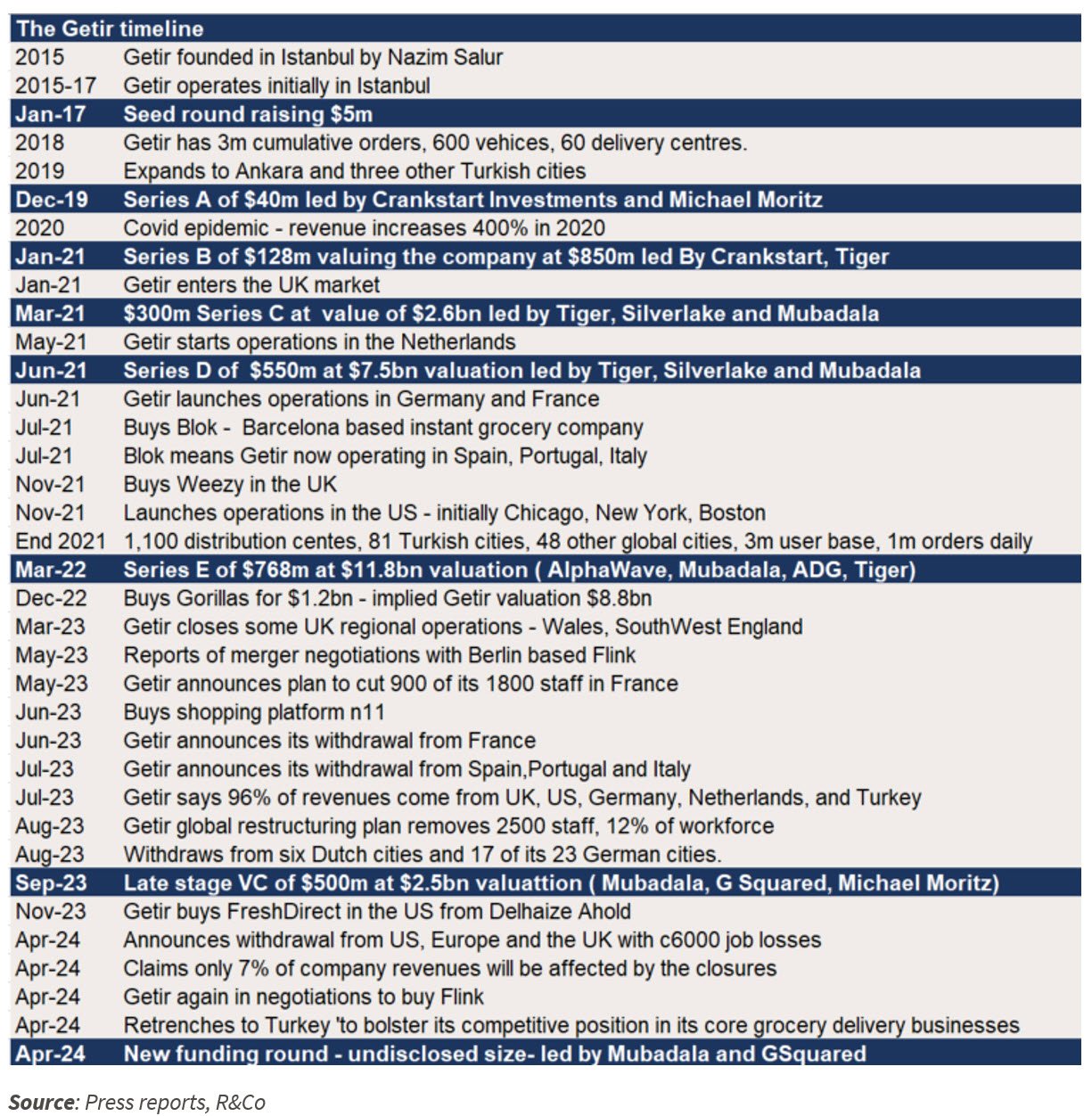

- We review the rise, rapid expansion and sudden retrenchment of Turkish ultrafast grocery delivery company, Getir. Founded in 2015 super-fast grocery delivery business Getir operated only in Turkey and with just $45m of VC funding until the end of 2019. Explosive pandemic growth combined with VC backing of $2.25bn between January 2021 and September 2023 for international expansion followed. In March 2022 Getir raised $768m at a valuation of $11.8bn. At end April 2024 Getir announced its withdrawal from the US and Europe; another funding round of undisclosed size and its re-focus on Turkey where ‘the opportunities for operational profitability and sustainable growth are stronger.'

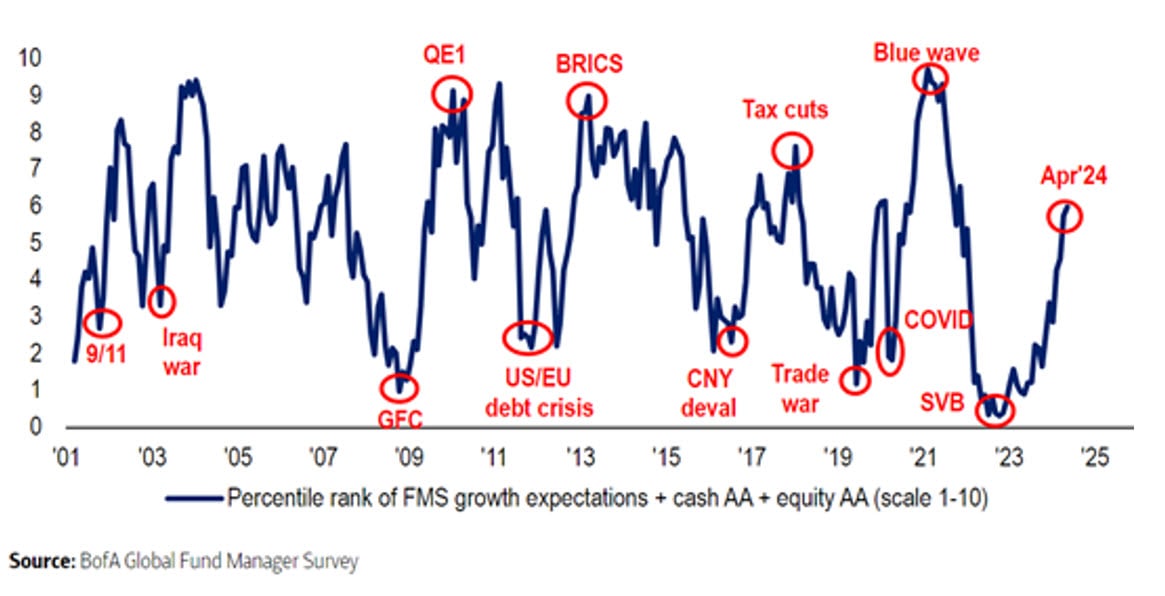

- Fund managers at their most bullish since November 2021: The most recent Bank of America global fund manager survey indicates they are at their most bullish since the last peak of the equity markets in November 2021. Most (56%) expect a soft economic landing. 11% expect a hard economic landing. 31% now expect a benign ‘no landing’ scenario.

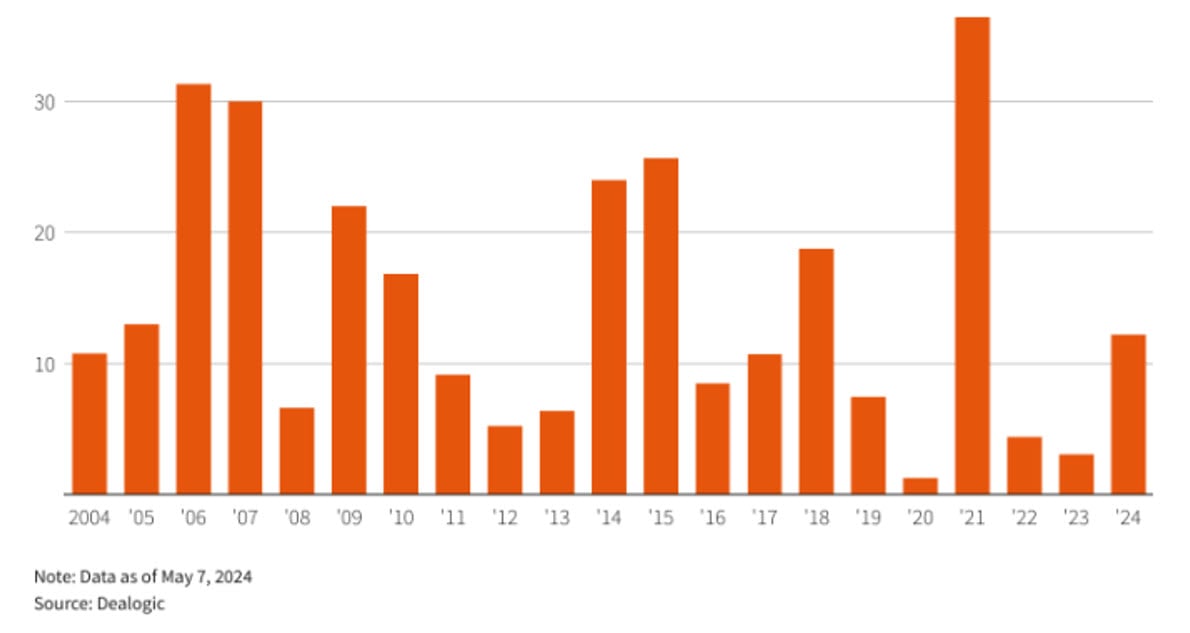

- IPO window open. Ytd to mid-May European IPO proceeds are at c$12bn, four times the level at this stage in 2023 and the fourth highest level in the last ten years. YTD in 2024 there have been thirteen US IPOs raising more than $400m with aggregate proceeds of $10.5bn. All but one saw a rising share price on day one. To mid-May the average weighted gain on these stocks is 23%.

- European VC raises up 40% yoy: Our monitor shows the value of European VC raises at c$11.4bn ytd , up 40% yoy. The leading sectors are Climate Tech (26 deals, value of $2.9bn), Artificial Intelligence (18/$1.7bn), Software (33 deals/ $1.66bn) and Fintech (23/ $1.48bn).

Click here to download a PDF version of Growth Equity Update

Getir – It all happened so fast….

We review the rise, rapid expansion and sudden retrenchment of Turkish ultrafast grocery delivery company, Getir. In December 2019 it was a Turkey only business that had raised $45m. The $2.25bn then raised between January 2021 and September 2023 went into a rash of international start-ups, acquisitions and restructuring. At end April 2024 Getir withdrew from its international territories and will once more be a Turkey only business.

Getir is the pioneer of ultrafast grocery delivery. The tech company, based in Istanbul, has revolutionized last-mile delivery with its 'groceries in minutes' delivery proposition, offering approximately 2,000 everyday items to its customers. Source: Getir US website

Getir’s purple and yellow branded bikes and motor scooters promising ‘groceries in minutes’ have become a familiar sight across Europe and parts of the US. The company was founded in Turkey in 2015 and, fuelled by venture capital funding, opened operations in the UK, the Netherlands, Germany, France, Spain, Italy, Portugal and the US. Its consumer promise was one of ultimate convenience - all your everyday grocery essentials, delivered in minutes whenever you need it – no need to book a slot and no substitutions – the real time inventory means what you order is what you get. All done on an app.

The company was founded in Turkey in 2015 by Nazim Salur who had previously run a taxi app, BiTaksi. When that business faced regulatory obstacles he reasoned that if a taxi could be delivered to a customer within three minutes then groceries could be delivered within ten.

We deliver cabs in 3 minutes anywhere in the city, why not do the same with groceries in 10 minutes?”

The super-fast business model means Getir employs its delivery people in each city and sets up its network of dark stores, owned or franchised, close to, or in, city centres. The customers download the Getir app – monthly app downloads peaked at 4m at the end of 2021 - and are offered a choice of 1500-2000 items, with the range being curated by Getir. Getir has two main revenue streams. It purchases its products from wholesalers and then marks up the prices, typically charging 5-15% more than typical local grocery store prices. There is a delivery charge paid by the customers and a minimum delivery amount. The delivery charge - $1.95 in the US- was frequently waived as part of promotion activity. Tips are retained by drivers.

After a couple of years of establishing itself in the Istanbul market, the idea began to take off and Getir expanded rapidly, both across Turkey and then, fuelled by venture capital funding, extending its operations to the UK, the Netherlands, Germany, France, Spain, Italy, Portugal and the US. In doing so Getir raised around $2.3bn in financing. Even as the Covid related e-commerce surge wore off, and the interest rate environment deteriorated, it completed its largest raise, a $768m Series E in March 2022 valuing the business at $11.8bn. As market conditions demonstrably deteriorated, and the company continued to be EBITDA negative in all its operating territories, it still raised a further $500m from VC investors in March 2023.

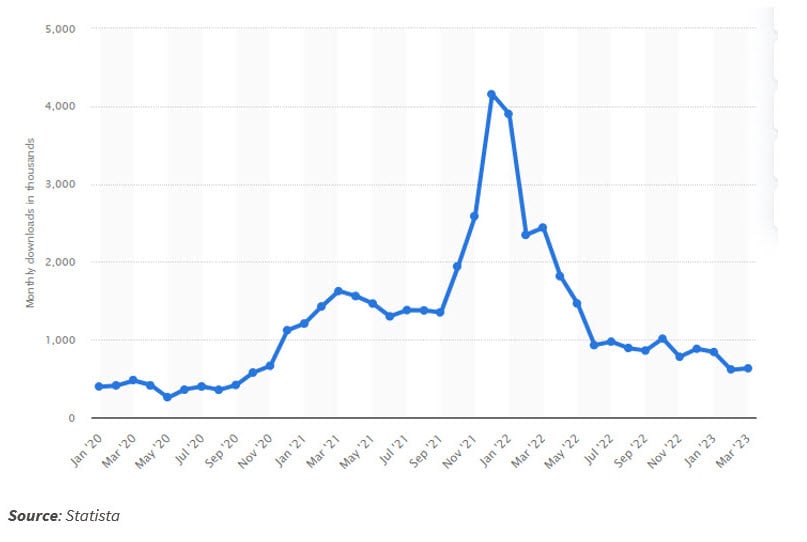

Monthly number of Getir app downloads worldwide from January 2020 to March 2023

The timeline exhibit outlines the rapid expansion of Getir.

nitial funding rounds were small, starting with a $5m seed round in January 2017. By the end of 2018 Getir had serviced 3m cumulative orders and had 600 vehicles and 650 delivery centres. In 2019 it expanded outside Istanbul to Ankara and three other Turkish cities. In December 2019 its early success was marked with a $40m Series A valuing the company post money at $350m.

Getir - the timeline

The key period for Getir though came with the outbreak of Covid 19 in 2020. The concept of fast grocery took off in the lockdown environment, paralleling a surge in eCommerce generally. At the time this was regarded as the speeding up of an inevitable trend rather than as a lockdown induced bubble. As the chart shows, Getir was averaging about 0.5m app downloads a month as the pandemic started in early 2020. By the end of 2020 monthly app downloads were running at over one million a month. By the renewed lockdowns at the end of 2021 the figure was up to 4m a month. In 2020 Getir’s revenue increased four-fold.

2021 was the key year of expansion for Getir. It was fuelled by three funding rounds in six months, raising just under $1bn. In January 2021 Getir raised $128m at a valuation of $850m. Just two months later in March, Getir raised $300m at a valuation of $2.6bn in a deal led Tiger Global, Silver Lake and Mubadala. A further three months later, in June 2021, there was a $550m Series D with Getir tripling its valuation to $7.5bn post money. The deal was led by Tiger Global and Sequoia, and Mubadala and Disrupt AD, both parts of Abu Dhabi’s sovereign wealth funds, participated.

On the back of this funding Getir began to spread geographically through a combination of new organic market penetration reinforced by acquisition. It started with entry into the UK market in January 2021 focusing initially on London and then bulking up with the Weezy acquisition in November.

In May the same year it started in the Netherlands, initially in Amsterdam. In June 2021 Getir launched in Berlin and Paris in quick succession. The Spanish business was reinforced by the acquisition of the Barcelona based instant grocery service, Blok, in July 2021. Blok brought with it nineteen Getir dark stores in Madrid and Barcelona. The acquisition also had operations in Italy and Portugal which now established Getir in these countries.

In November 2021 Getir announced its arrival in the US, launching operations initially in Chicago, New York and Boston. Getir CEO and founder Nazim Salur commented ‘Just like every basketball player dreams of playing in the NBA, a startup dreams of playing in the US. We want to succeed in the U.S.'

At the end of 2021 Getir was established in 81 cities in Turkey and 48 other cities worldwide in the US, the UK, France, Germany, the Netherlands, Spain, Portugal and Italy. The company had some operational difficulties, notably around zoning laws restricting the development of dark stores in some cities. The more obvious issues that would emerge though were the difficulties Getir was having in making its business model turn a profit, the waning interest in superfast grocery delivery - app downloads were down from four million a month in December 2021 to one million by mid 2022 as Covid lockdowns ended and living conditions normalised. The third factor was the change in the inflation and interest rate environment post the Russian invasion of Ukraine in late February 2022.

The peak valuation of Getir was reached in March 2022. On the back of its rapid 2021 expansion Getir raised $768m in new funds at a valuation of $11.8bn in a deal led by Alphawave, Mubadala, ADG and Tiger. Altogether 16 investors joined the round. By this point Getir had raised almost $1.8bn in venture funding, the bulk of it since the start of 2021.

The unravelling of the Getir growth procession was rapid at this point. Surrounded by other challenged rapid grocery delivery companies and with publicly funded businesses like Delivery Hero, DoorDash and Deliveroo also operating in the space, consolidation appeared inevitable and Getir appeared determined to lead it.

In December 2022 Getir acquired its counterpart German business Gorillas in a deal valuing the combined group at $10bn. That deal valued Gorillas at an ostensible c$1.2bn ( which compared with the previous valuation of Gorillas at $3bn in September 2021). Gorillas itself had raised a total of $1.3bn in venture funding. The shareholders of Gorillas ( Delivery Hero, Coatue, Tencent, DST) received c$40m in cash and a c12% stake in the enlarged Getir entity. The combined group was valued at $10bn, implying $8.8bn for Getir, a reduction of $3bn or 25% from the March 2022 round just nine months earlier.

In March 2023 signs appeared of further pressures on the business model with Getir closing some UK regional operations (in Wales and South West England) and trimming its presence in London and Birmingham. Such moves might reasonably, though, have been attributed to good housekeeping post the merger with Gorillas.

In May 2023 Getir was again said to be in talks to take over a counterpart business, another German operator, the Berlin fast grocery delivery service Flink, a company supported by the German supermarket chain, Rewe, US food delivery group DoorDash and Mubadala, which was also invested in Getir. The talks were eventually unsuccessful with Flink instead raising a further €150m from its existing shareholders.

In May 2023 Getir cut half of its 1,800 staff in France and followed this up in June 2023 with the announcement that it was to withdraw altogether from France, exactly two years after it first entered the territory. Getir said the decision was occasioned by a French regulatory ruling in March 2023 that "dark stores" were to be treated as warehouses rather than businesses and thus be subject to local authority regulation. This would potentially leave them subject to sudden closure under PLU ( plan local d’urbanisme) regulations. Counterpart quick commerce company Flink had previously announced that it would close its 19 Parisian dark stores on the back of this regulation.

In July 2023 Getir was, according to press reports, facing a ‘cash crisis’ – reported to be burning as much as $100m of cash per month- and announced its withdrawal from Spain, Italy and Portugal, essentially abandoning the territories acquired with the Blok acquisition of July 2021. In a statement the company said

'Getir, the ultrafast grocery delivery pioneer, announced that it intends to withdraw in an orderly manner from Spain, Italy, and Portugal. At the same time, Getir is finalizing a funding round and will continue to operate in the UK, the US, Germany, the Netherlands, and Turkey, which generate 96% of the company’s revenues. Getir’s withdrawal from these three markets will allow it to focus its financial resources on existing markets where the opportunities for operational profitability and sustainable growth are stronger.'

This was the first time that Getir admitted to a need to conserve its financial resources in the face of a tougher consumer environment and rising interest rates and the need to take steps to advance the point of break-even.

The challenges faced in the build out of an ultra-fast grocery delivery model are illustrated by the 2021 Getir accounts published on the website of the Dutch Chamber of Commerce. These showed 2021 revenue of $466m (vs $182m in 2021, +156%). The operating loss was $589m, equivalent to 1.26x revenue and was up from $38m a year previously. Cost of goods sold was at $357m, giving a gross margin of just 23%. The operating cost items in 2021 included logistics and delivery expenses of $261m, personnel expenses of $158m and marketing expenses of $169m.

In August 2023 Getir announced further retrenchment with a global restructuring plan which included 2,500 job cuts across five countries, equivalent to 12% of its staff. As part of this efficiency drive Getir reduced its presence in some of its remaining territories. In August 2023 it withdrew from six Dutch cities (Leiden, Breda, Delft, Eindhoven, Tilburg, and Groningen) and cut five of its 20 dark stores in Amsterdam. In Germany in the same month Getir withdrew operations in 17 of the 23 cities in which it operated.

Getir announced it would continue to operate in Turkey, the UK, Germany, the Netherlands and the United States representing 96% of its revenues and said the restructuring would 'significantly increase operational efficiency'.

On the back of this restructuring a further funding round was announced. In September 2023, still reported to be EBITDA negative both as a group and in each of its individual countries of operation, Getir raised $500m of fresh funds at a $2.5bn post money valuation in a deal led by Mubadala, GSquared and Michael Moritz. Although the valuation was greatly reduced, down almost 80% from the March 2022 deal eighteen months before, this was still a substantial raise. The rationale of the Getir investors appears to have been that, as funding conditions deteriorated in the fast grocery sector and the ranks of the competition thinned out, the prospects of Getir surviving as market leader on the back of fresh backing must be enhanced.

The fundraise was followed by another bout of consolidation. In November 2023 Getir announced the acquisition of FreshDirect in the US from Delhaize Ahold. The New York based FreshDirect was originally established in 1999 and attracted $517m in venture funding before being bought by Delhaize and Centerbridge for $300m in November 2020.

According to its 2023 Report & Accounts Delhaize recognized an impairment loss of €153m on FreshDirect in Q3 2023 based on fair value less costs to sell. On November 8, 2023, Ahold Delhaize announced it had entered into an agreement to sell its FreshDirect business to Getir. The transaction closed on December 6, 2023. Its accounts say.

Upon the divestment, Ahold Delhaize recorded a pre-tax loss of €250 million as a result on sale, offset by a net tax benefit of €75 million, which were included within General and administrative expenses and Income taxes in the consolidated income statement, respectively. Divestment of business, net of cash divested was a negative €144 million.

The implication of this is that it appears that Getir paid nothing for FreshDirect and in fact was paid around €138m (note 28 of the accounts) to take it on.

The announcement at the time said:

'The acquisition will lead to significant synergies between Getir and FreshDirect and emphasizes Getir’s strategic ambitions to grow in the United States. FreshDirect will leverage Getir’s technology and operational footprint to offer faster services to its loyal customer base, which will also benefit from easy access to Getir’s quick convenience service. FreshDirect will enable Getir to further increase the quality and breadth of its product range, especially regarding fresh products.'

The story though moved rapidly on. In April 2024, just five months after the FreshDirect acquisition, Getir announced that it was withdrawing from its US, European and UK operations. The business will instead just operate in Turkey, where it sees ‘the biggest potential for long-term sustainable growth’. Getir indicated that Fresh Direct ‘will continue its operations’ but has not explained how. In total 6,000 jobs will go with the closures in the US and Europe.

There is to be a new funding round to be led by existing investors Mubadala and G Squared. It is intended that this should ‘bolster its competitive position in its core food and grocery delivery businesses in Turkey.’

Getir’s claim now is that only 7% of its revenues come from the UK, Germany, the Netherlands and the US. The implication is that 93% come from Turkey.

This is of course reminiscent of its claim in August 2023, after it shut France, Spain, Portugal and Italy, that these territories represented only 4% of revenues and that the then remainder (Turkey, the UK, Germany, the Netherlands and the United States) represented 96%.

TechCrunch reports that in 2023 the gross market value of transactions at Getir was approximately $3.3bn of which around a third, $1bn, was derived from the US, Europe and the UK. Elsewhere we have seen 2023 revenue (not GMV) estimates of $800m for Getir, which would suggest a take rate of 24%.

These figures might suggest that there is as much as $2.3bn of GMV and perhaps $300m-$350m of revenue still to play for in the Turkish market. This may be optimistic but might explain the apparent willingness of the existing shareholders to keep funding the business. It appears Getir is still lossmaking at an EBITDA level in Turkey as a whole although the founder has indicated it is profitable in some cities. The company is reported to be looking to sell its online shopping platform n1, Fresh Direct and its stake in its original BiTaksi business.

Getir has essentially moved full circle. In December 2019 it was a Turkey only business and had raised $45m in total. The $2.25bn raised between January 2021 and September 2023 seems largely to have gone into the rash of international start-ups, acquisitions and restructuring. At the end of the $2.25bn Getir has withdrawn from all those territories and returned to Turkey, where seemingly it is not break even and is still absorbing cash. In the meantime Tottenham Hotspur have found a replacement shirt sponsor and a lot of people in Europe and the US have enjoyed highly subsidised fast grocery delivery.

We’re democratising laziness…It’s like having a butler for a dollar or two.’’

Markets move on

Robust earnings take over from interest rate hopes

Public markets are keeping up their overall momentum and roughly retaining their hierarchy although it is notable that the gap between US markets, where early interest rate cut hopes have faded, and European markets, where they have been maintained, has narrowed. YTD to the 14th May the Magnificent Seven tech stocks are up 20%, the NASDAQ composite index is up 11%, the tech heavy NASDAQ 100 is up 10% as is the S&P 500. The STOXX 600 Europe is up 9% as is the usually lagging FTSE 100. Even the neglected small-mid caps in the FTSE 250 have started to perform, up 5.5% ytd.

The Thomson Reuters Venture Capital Index, which seeks to monitor the real time performance of the venture capital industry and whose performance is partly driven by the moves in public markets, and particularly tech heavy indices like NASDAQ, is 9% off its 2024 top, up 10% ytd, having closed 2023 up 56%.

The chart from the Bank of America global fund manager survey indicates that fund managers are at their most bullish since the last peak of the equity markets in November 2021. Most (56%) expect a soft economic landing. 11% expect a hard economic landing. 31% now expect a benign ‘no landing’ scenario.

Global Fund Manager sentiment most bullish since November 2021 -Percentile rank of fund manager growth expectations, cash level and equity allocations

Optimism about early US interest rate cuts has faded. As a reminder the US Fed surprised the market in December 2023 when it switching the narrative from the need to keep interest rates high until the job of taming inflation was done, to a stance that said there was a risk to the economy of holding on to high rates for too long. As expressed by Fed chair Jay Powell the approach shifted to:

'We’re aware of the risk that we would hang on too long….. and we’re very focused on not making that mistake.'

Observing the Fed would be ready to cut interest rates before inflation reaches its target of 2% he commented 'you’d want to be reducing restriction on the economy well before [then] so you don’t overshoot'.

At that stage the Fed produced its ‘dot plot’ anticipating 75bps of interest rate cuts in 2024 with an expectation that the year would close with rates to at 4.5%-4.75%, and 2025 another 100bps lower at 3.5% to 3.75%.

At that point public markets raced ahead with derivatives markets in January anticipating up to seven interest rate cuts in 2024 (which would have totalled 175bps) with the first to take place in April-May. This always appeared optimistic and since then the stubbornness of core US inflation has meant that interest rate hopes have faded to the extent that markets even began during April to countenance rates rising further before they fell. In this respect Jay Powell’s comments in mid-April indicating the Fed was still thinking of the next move in interest rates as being down rather than up were taken positively.

'We’ll need greater confidence that inflation is moving sustainably toward two percent before it would be appropriate to ease policy. The recent data have clearly not given us greater confidence, and instead indicate that it’s likely to take longer than expected to achieve that confidence.'

There was further relief with the April inflation number, announced in mid-May. US inflation fell from 3.5% in March to 3.4% in April and was the first inflation number since the start of the year to come in lower than expectations.

At present surveys of economists held by Reuters show two thirds (70 of 108 polled) anticipating the first 25bps US rate cut in September with 60% of economists expecting two rate cuts in 2024. Post the April inflation number derivatives markets began more solidly to anticipate two 2024 rate cuts.

US interest rates were held at 5.25%-5.5%, a 23 year high at the Fed May meeting at the start of the month with the Fed saying that it needs to see inflation move closer to 2% and the labour market cool down before considering rate cuts.

The debate about ‘the new normal’ for interest rate continues – the concept that the period of very low interest rates enjoyed up to the start of 2022 was an aberrational condition unlikely to return. The same Reuters survey (albeit with a smaller sample of 29) saw the median expectation of economists looking at a level of 3-3.25% as the ‘neutral’ Fed rate – one that neither overstimulates nor restricts the US economy.

Markets though have remained pretty firm with the strength of the US economy and a robust results season keeping up the momentum. The US Q1 reporting season, now effectively complete, surprised on the upside. Typically the trend is for US equity analysts to forecast too optimistically at the start of the year and to spend the subsequent results seasons downgrading expectations. By the end of April the YTD cut is habitually around 5%. 2024’s Q1 has seen average earnings beat in the order of 8-9% and full year earnings forecasts have held up to near start of the year levels, a pleasant surprise for markets.

An interesting feature is the potential or divergence between the Fed and its European and UK counterparts in terms of the timing of rate cuts. It now appears that European rate cuts are likely to precede those in the US.

The Eurozone April inflation figure was 2.4%, the same as in March with core inflation ( ex-energy and food) at 2.7% versus 2.9% in March, 3.1% in February and 3.3% in January. The minutes of the April ECB meeting indicate that the policymakers are content with the progress towards the 2% inflation rate target and that they, like the Fed in December, are concerned not to keep interest rates high for too long lest that stance damages economic growth prospects. The ECB minutes commented:

'The risk of undershooting the inflation target and eventually having to pay too high a price in terms of declining activity was now seen as being at least as high as the risk of acting too early and overshooting the target over the medium term.'

Market expectations are that Eurozone inflation hovers around the 2.4% level for the rest of 2024 before dropping to the 2% target during 2025. In mid-May the EC agreed with the markets with an update of its official forecasts showing that Eurozone inflation was now expected to fall to 2.5% in 2024 ( previous forecast 2.7%) and to 2% in 2025 (previously 2.2%).

The ECB seems content that if the inflation trend is confirmed in May then its first interest rate cut will come in June with the market penciling in two further interest rate cuts by the end of the year which would take rates down from 4% to 3.25%.

It is notable that two European central banks have already cut rates. In March the Swiss National Bank reduced its headline interest rate from 1.75% to 1.5%. It stood alone amongst Western economies in this cycle until joined by the Swedish Riksbank in early May. The Riksbank cut interest rates by 25bps to 3.75% and indicated that it expects to cut the rate twice more by the end of 2024. Inflation stands at around 2% in Sweden down from a peak of 10% in 2022 and the jobs market data is weak.

A slightly different picture prevails in the UK where February’s unexpectedly good inflation figure of 3.4% (after 4% in January) was followed by a modestly disappointing 3.2% in April – forecasters had expected 3.1%. Core inflation, ex food and energy, fell to 4.2% ( versus expectations of 4.1%) from 4.5% in February and 5.1% in January. Services inflation reduced from 6.1% to 6%, again above forecasts. This was enough to have market commentators pushing back expectations of the first UK interest rate cut from June to September. Subsequent data in mid-May on wage growth – unchanged at 6% - reinforced the idea that the UK may need to delay interest rate cuts.

The Bank of England’s February Monetary Policy Report notes that inflation is expected to fall to the target 2% during Q2 2024, largely due to falls in energy prices yoy, before climbing back to c2.75% by the end of 2024 and averaging c2.3% in the following two years.

As in the US the European Q1 earnings season has proved pretty satisfactory. Market commentators chart earnings beats at a net c15% of companies. Aggregate market cap weighted earnings were c6% ahead of consensus. Earnings revisions on balance have moved higher, again unusual for this stage of the year and indicating an unwarranted level of start of the year pessimism on earnings trends.

Pace of exits – IPOs and M&A picks up

In Europe Q1 2024 saw thirteen IPOs raise €4.8bn - the highest quarterly IPO proceeds since Q1 2021. Aftermarket performance has been decent with four of the top five IPOs ending Q1 in positive territory.

A series of substantial IPOs in April and May means that ytd to the 7th May European IPO value is at c$12bn, around four times the level seen at this stage in 2023. At this stage this is the fourth highest level of proceeds from the European IPO market in the last ten years.

European IPO value : 2004 YTD – 2024 YTD ($bn)

In the US 2023 saw just nine IPOs that raised more than $400m, each with the total amount raised by the group at $14.1bn.

Year to date in 2024 there have been thirteen such US IPOs, raising more than $10.5bn.

Of the thirteen issues 2024 ytd all but one saw a rising share price on day one. The weighted average day one gain of these 14 IPOs ytd was 23%. The median gain was 12.5%.

To the 14th May twelve of the thirteen IPOs remain in positive territory with the average weighted gain on the stocks being 23%. Of the 13 stocks, eight are above the close of day one price, four are flat and just one is lower implying that the aftermarket post day one has remained firm.

The IPO window is open. There is a steady flow rather than a flood of IPOs and sponsors still need to be cautious in terms of the readiness of their asset and the price expectation. Nevertheless the IPO market is building up an attractive record that suggests it is worth the while of investors to participate. Meanwhile there is little chance of a shortage of supply with, according to Pitchbook data the backlog of venture-capital-backed firms waiting for an opportunity to go public at around 220 companies.

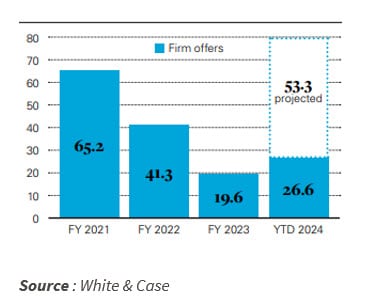

M&A markets also appear to be picking up. A notable feature is the UK market which has stood out for depressed valuations. A snapshot of UK public M&A market activity January- April 2024 indicates £26.6bn aggregate deal value with nine £1bn plus transactions. There has been a 54% average bid premium on cash bids. The £26.6bn figure is five times higher than in the same period in 2023 and the UK is on course (according to data from White & Case) for the highest annual value of M&A activity since 2018.

UK Public M&A aggregate value (£bn)

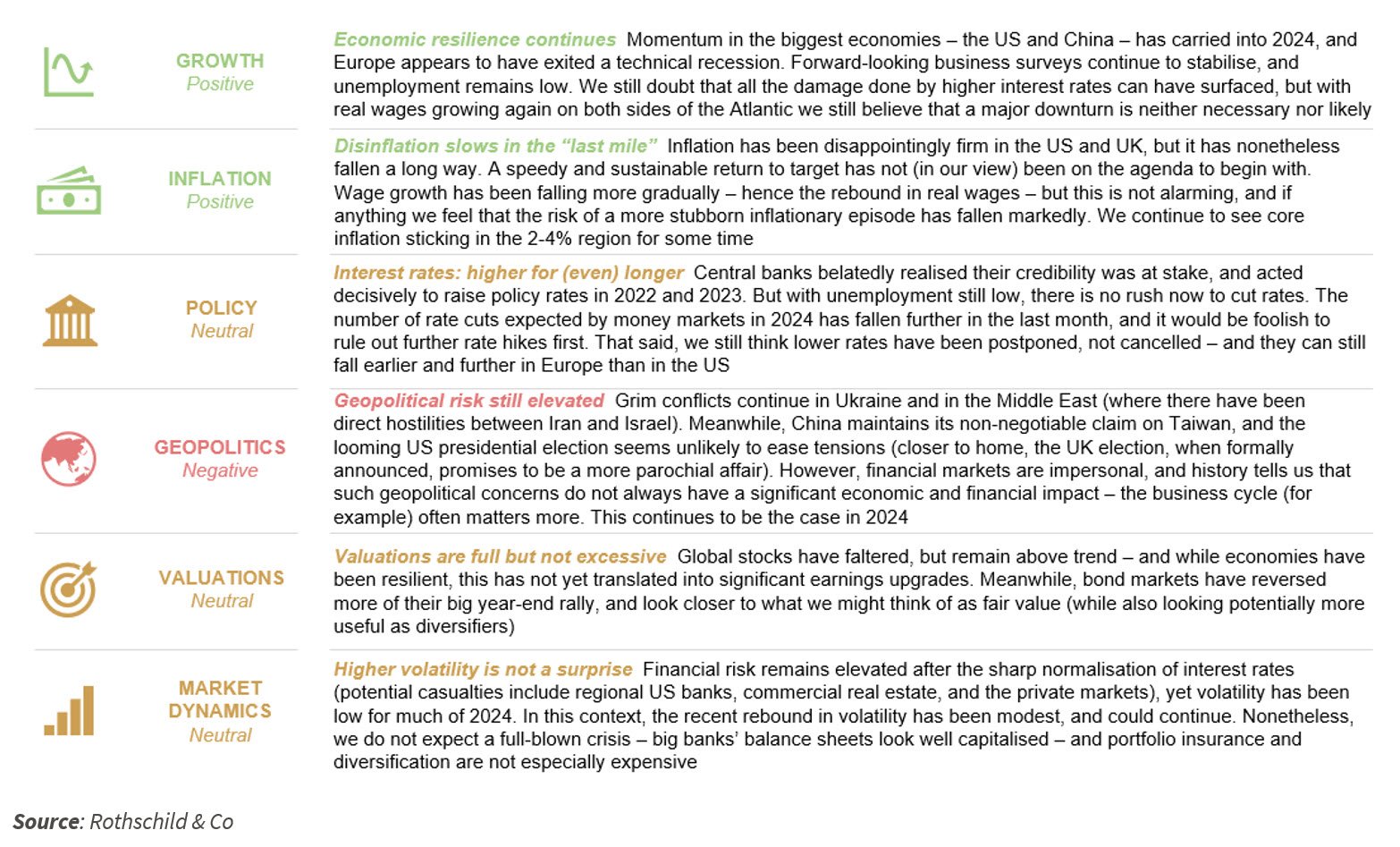

Rothschild & Co strategist Kevin Gardiner summarises the current key drivers of the market in this graphic:

The favourable mix of growth and disinflation continues:

Venture Capital deal activity

A positive start to the year in Europe

Our monitor of European venture capital raises continues to show ytd 2024 activity levels running well above the same period in 2023. On our reckoning, January European raises were more than double the levels of January 2023, February was flat yoy, March up c27% yoy with April up c11%. YTD this implies that European raises at c$11.4bn are 40% higher than in the first four months of 2023. The May total to date is $1.4bn, also running ahead of its counterpart month.

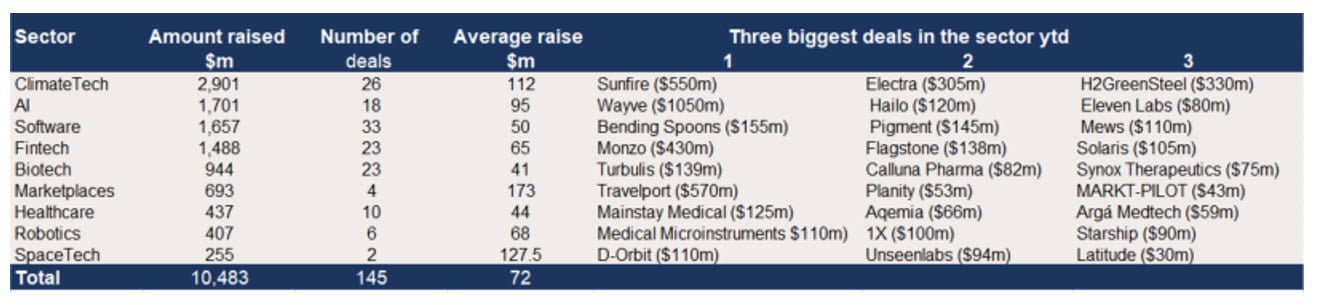

Of that $12.8bn total ytd, $10.5bn or 84% is spread between eight sectors. The top four are:

Climate Tech, as in 2023, leads the way with 26 deals with a total value of $2.9bn. Looking at the three biggest deals - German electrolyzer manufacturer, Sunfire, raised a total of $550m. French EV charging business Electra, where R&Co advised the lead investor PGGM, raised $335m. H2 Green Steel raised a further $330m in equity and $3.9bn in additional debt.

Artificial Intelligence deals climb to second place with 18 deals raising $1.7bn. The total is boosted by the $1.05bn Series C from AI led UK autonomous vehicle software company Wayve led by SoftBank and including Nvidia and Microsoft. It’s one of the largest AI raises globally to date. Israeli producer of Edge AI processors, Hailo, raised $120m in a Series C+ led by family offices and Delek Motors. The $80m deal in January for AI voice generating platform AI Labs valued the company at $1.1bn. The round was led by a16z.

Software has the highest volume of deals ytd at 33 with $1.66bn raised. Bending Spoons, the Italian owner of the MeetUp and Evernote apps, raised $155m in a deal valuing it at $2.55bn. It was led by Durable Capital Partners. French business planning software start up, Pigment, raised $145m in a deal led by ICONIQ Growth. Dutch hospitality software business Mews raised $110m in a deal led by Kinnevik.

Fintech has staged something of a rally in 2024 ytd with 23 deals at an aggregate value of $1488m. By far the biggest deal, and the third largest in Europe ytd, was from UK neobank Monzo which raised $430m, supported by the venture arms of Alphabet, CapitalG and Google Ventures, as well as by HongShan Capital. The round valued Monzo pre-money at £3.6bn ($4.6bn). The UK cash deposit platform Flagstone raised $138m in a deal led by Estancia Capital Partners. The German embedded finance platform Solaris raised $105m from in an SBI Group led deal.

Biotech is the last of the big five sectors with 23 deals raising $944m. Average deal size in this sector is typically relatively small at $41m. The largest deal was the $139m raised for cancer therapies group Turbulis by EQT Life Sciences and Nexttech Investment.

European VC raises by sector YTD – ClimateTech leads the way

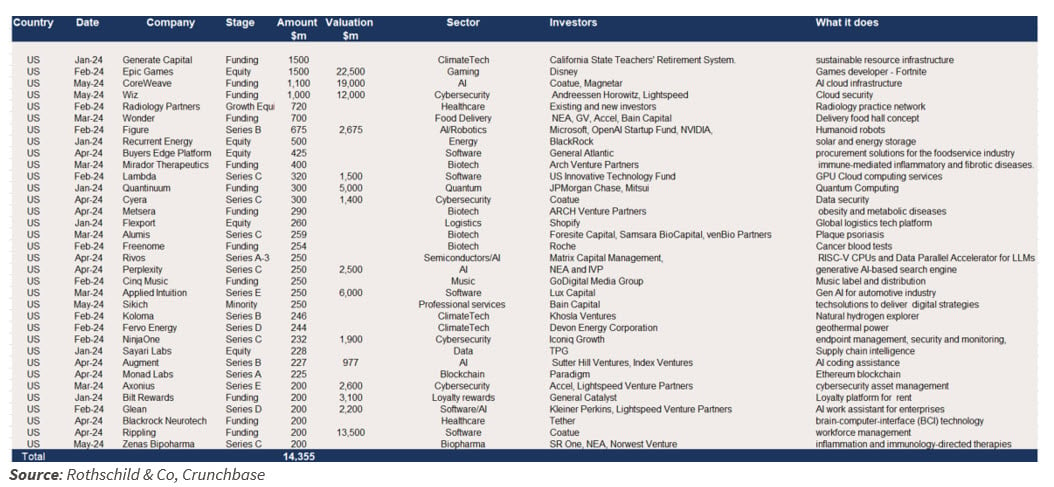

Meanwhile in the US there have been 34 deals with a value of over $200m ytd and four deals with a value of over $1bn. In total just these deals have raised in excess of $14.3bn.

Biggest US VC raises ytd ($200m and above)

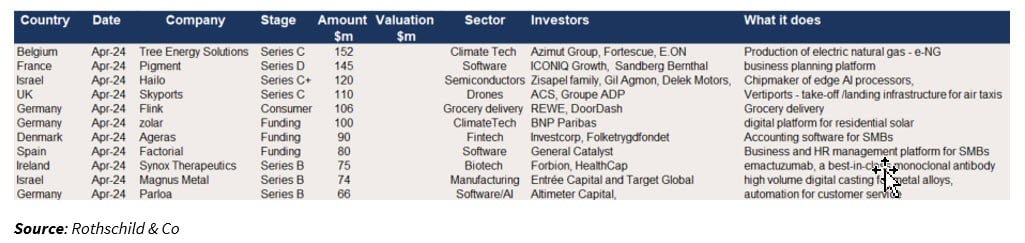

April raises in European VC

The largest European raise in April was the $152m Series C for the Belgian climate tech business Tree Energy Solutions ‘We put solar panels and wind turbines in the world’s sunniest and windiest places and use this renewable energy to generate green hydrogen. We then combine that hydrogen with recycled CO₂ to create e-NG (electric natural gas), a hydrogen based drop-in fuel.’ It was led by Azimut Group, Fortescue and EON.

Pigment raised $145m and Hailo raised $120m.

UK based Skyports – which supplies take-off and landing infrastructure for air taxis and drones, raised a $110m Series C led by ACS and Groupe ADP.

Flink, the German instant grocery delivery business received $106m of funding from existing shareholders including REWE and DoorDash. Bloomberg reported that Flink has been in merger talks with other grocery delivery businesses, including Getir, in recent months. Elsewhere in Germany the solar energy business zolar raised $100m of funding led by BNP Paribas.

Danish accounting software business, Ageras, whose product is aimed at SMBs, raised $90m in a deal led by Investcorp. Factorial, a business and HR management platform for SMBs raised $80m in a deal led by General Catalyst.

Synox Therapeutics of Ireland raised $75m in a Series B and Magnus Metals, an Israeli metals casting business, raised $74m.

Top 10 European Venture capital raises of April 2024

And valuations?

Valuations in the private market are a topic of intense interest. For most of the past two years the market has seen a disconnect between investors conscious of the demands of the higher investment returns required by the new higher rates environment and founders still in thrall to the heady valuation environment of 2020-22. In our last Growth Equity Update we noted that some leading VC investors are beginning to see value in the market.

Speaking at a conference at the start of April Anton Levy, Chairman of the Global Technology Group of General Atlantic observed, in reference to enterprise software and e-commerce that 'For the first time in a little while, prices…are fair. It’s a great environment to put new capital to work.'

At the same time Ibrahim Ajami, Head of Venture at Mubadala Capital noted ‘We are moving to offense.’

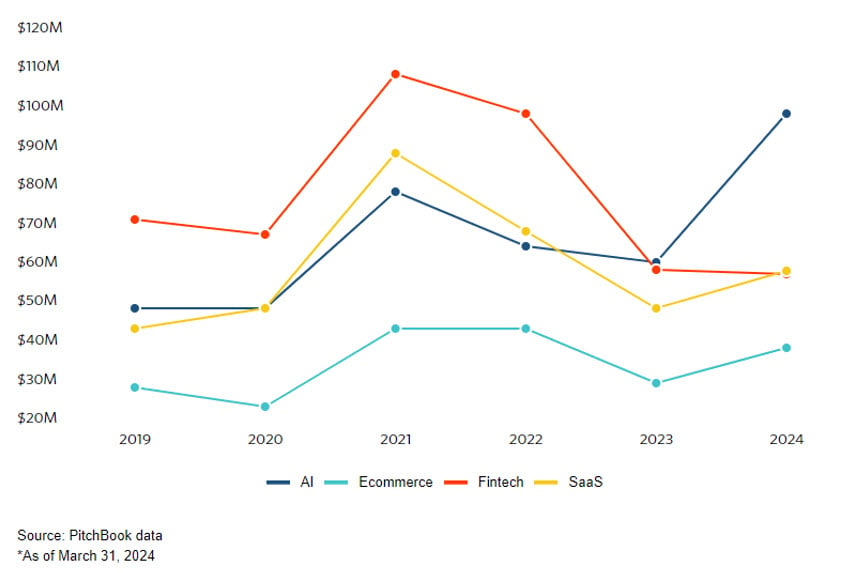

Pitchbook has just produced its Q1 2024 US VC Valuations Report. The chart shows the trend in median late stage pre-money valuations by vertical. As a valuation indicator it can directionally illustrate what investors are willing to pay for businesses over time. As one would expect valuations (as measured by median size of funding round) typically peaked in 2021 at the top of the venture market, having climbed sharply in the prior two years.

Looking at the four featured sectors the median size of the funding rounds in SaaS and eCommerce have now climbed off their 2023 lows, more noticeably for SaaS than eCommerce. Of the four sectors FinTech remains the one where the median size of rounds continues to fall. This sector saw the sharpest fall in 2023 and 2024 appears to see a degree of levelling out.

The stand out sector in context is Artificial Intelligence. It is no surprise given the scale of some of the announced deals, the substantial valuations attributed to early stage businesses and the continued competition amongst VC investors to gain exposure to the sector, that the median deal size has risen sharply in 2024 over 2023 and is now at its highest level to date. Median pre-money valuations for early-stage AI startups jumped 51% from $47 million in 2023 to $71 million in Q1 2024, compared to a 29% increase across all verticals, according to PitchBook.

Global median late stage pre–money valuations by vertical

Meanwhile a16z has a report ‘16 Changes to the Way Enterprises Are Building and Buying Generative AI’ which illustrates why venture capital is so positive on the space. The a16z authors observe:

'Over the past couple months, we’ve spoken with dozens of Fortune 500 and top enterprise leaders, and surveyed 70 more, to understand how they’re using, buying, and budgeting for generative AI. We were shocked by how significantly the resourcing and attitudes toward genAI had changed over the last 6 months. Though these leaders still have some reservations about deploying generative AI, they’re also nearly tripling their budgets, expanding the number of use cases that are deployed on smaller open-source models, and transitioning more workloads from early experimentation into production.'

a16z sees budgets for generative AI ‘skyrocketing’. In 2023 it identified the average spend of the companies it surveyed across foundation model APIs, self-hosting, and fine-tuning models at $7m. It anticipates this rising typically by 2-5x in 2024 with budgets for AI spending shifting from the ‘innovation’ category to more permanent spending categories.

The appetite for gen AI inspired growth and the anxiety of VCs to hop onto the moving train is clear. As ever the focus on a single category may mean that attention and valuation is sucked awy from other categories.

Our views on the state of the venture capital markets

2022 saw sharp falls in the public markets on the back of a combination of global inflation, rising interest rates, and increased geopolitical risk. In 2023 there was a substantial rally on NASDAQ, led by the major tech stocks, a rally more palely reflected in other markets. The Refinitiv Venture Capital Index, which seeks to monitor the real time performance of the venture capital industry, fell 55% in 2022. In 2023 it was up 56%. YTD in 2024 it is up 10% meaning the total fall since the peak at end November 2021 is 32%.

Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment has had a sharp impact on valuations in private markets. The scale of the fall in the Refinitiv VC index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023.

- There is substantial dry powder in the VC industry. This though appears to be prioritised to support existing rather than new investments.

- Best-in-class companies, addressing critical rather than nice-to-have requirements, continue to attract support. There are still hotspots for investment most notably in Artificial Intelligence and Climate Tech. Certain investors remain very active in the space with substantial funds to deploy.

- The speed of the investment process has slowed considerably. The level of diligence on new deals has stepped up.

- For much of 2023 big late-stage deals were few and far between with the strongest part of the market in terms of appetite being in Seed and Series A where there is less immediate pressure on valuation. The last few months though have seen a notable pick-up in large later stage deals, particularly in Climate Tech and AI.

- 2023 saw more downrounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these

▪ It seems likely that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses. - Valuation priorities have shifted with investors having moved away from an emphasis on revenue growth and revenue multiple emphasis. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and an emphasis on DCF and comparative based multiples.

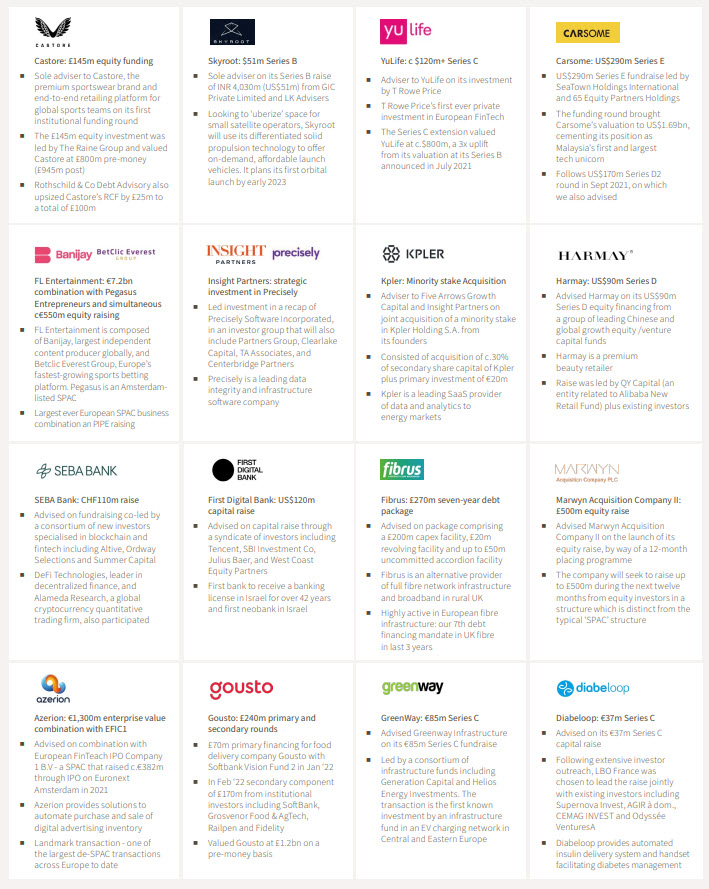

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised

For more information, or advice, contact our Growth Equity team:

Chris Hawley

Global Head of Private Capital

chris.hawley@rothschildandco.com

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Advisory

patrick.wellington@rothschildandco.com

+44 20 7280 5088

+44 7542 477 291

Mark Connelly

Head of North American Equity Market Solutions

mark.connelly@rothschildandco.com

+1 212 403 5500

+1 917 297 5131

Stéphanie Arnaud

Managing Director – France

stephanie.arnaud@rothschildandco.com

+33 1 40 74 72 93

+33 6 45 01 72 96

Read the previous editions: May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023 , December 2023 , January 2024, February 2024, March 2024

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.