Growth Equity Update

November 2025 – Edition 44

- Next version: With a market capitalisation of $4.6trn Nvidia is the largest company in the world. It is emerging as a key player in the ecosystem for the new AI economy through industry initiatives and participation in funding rounds, upping the pace and scale of its investments in recent months. We identify 74 Nvidia funded startups.

- Envy: Nvidia’s investments range across LLMs (Open AI, xAI, Thinking Machines), datacentres (Crusoe, Lambda, Nscale), quantum (PsiQuantum, Quantinuum) autonomous vehicles (Wayve), robotics (FigureAI), Drug discovery (Genesis) through to AI applications in data, coding, video, 3D models and chatbots. It is reported to be close to several more substantial investments.

- The pace of unicorn creation has accelerated in 2025. In the first three quarters of 2025, 117 new unicorns were created, an annualised rate of 156, the highest rate since the market peak in 2021.

- Exit activity improves: YTD to end September there were 176 US IPOs raising $32.8bn, a 20% increase in deal proceeds yoy. September, with $8bn raised, was particularly strong. Meanwhile Pitchbook estimates global M&A deal value increased 26% yoy after nine months of 2025. Q3 deal value was the highest since Q4 2021.

- October’s European deal value was up 73% yoy at $6.1bn led by software and healthcare. European fundraising ytd to end October is at $41bn, up 33% yoy.

- US growth raises in October were $21.1bn, up 33% yoy. YTD US raises to end October are at $182.5bn, up 2.3x yoy and 1.6x the whole of 2024. US growth raises were again led by AI which accounts for c60% of the value of all US raises ytd.

Click here to download a PDF version of Growth Equity Update

Nvidia - Promoting the AI ecosystem

We look at the role of Nvidia in fuelling the development of AI infrastructure around the world and its increasing scale and pace of funding for AI related start ups.

With a market capitalisation of $4.6 trillion Nvidia is the biggest of the Magnificent 7, the largest company in the world and one whose capitalisation recently exceeded the GDP of Japan. The company’s rise was based on its development of the GPU in 1999, whose parallel processing ability originally found its use in video gaming but more recently has fuelled the growth of AI, being critical to the development of large language models.

As Nvidia has grown it has become a vital component of the ecosystem around AI and its applications. With its immense resources (Nvidia finished Q2 2025 with $48.3bn in net cash and quarterly cash flow from operations of c$15.4bn) it has become a substantial player in the ecosystem of investment around AI. This includes substantial backing for the US Stargate plan , for the EU’s plan to invest €20bn to establish 20 AI Factories including five ‘gigafactories’ to increase its AI infrastructure and financial investment in the leading private AI companies in the US , Europe and elsewhere.

In France, Mistral AI is building an end-to-end cloud platform powered by 18,000 Nvidia Grace Blackwell systems in the first phase, with plans to expand across multiple sites in 2026. The infrastructure will host Mistral AI’s cloud application service, which customers can use to develop and run AI applications with Mistral AI’s and other providers’ open-source models. Mistral AI and Nvidia are collaborating with Bpifrance and MGX, the UAE’s investment fund to establish Europe’s largest AI campus — to be located in the Paris region and expected to reach a capacity of 1.4 gigawatts. The campus will feature advanced Nvidia compute infrastructure to support the full AI lifecycle, from model training and inference to deployment of generative and applied AI systems. Nvidia participated in Mistral’s €2bn Series C round in September this year.

At the end of October 2025 Bloomberg reported that Nvidia will invest up to $1bn in French AI business Poolside as part of an intended $2bn round at a valuation of $12bn. Nvidia previously contributed to Poolside’s $500m Series B in October 2024. Poolside, which was founded in the US but moved its headquarters to Paris in 2023, is developing a large language model that writes software code.

In mid September 2025 NVIDIA announced an investment of £2bn in the UK ‘to catalyse the nation’s AI startup ecosystem and scale the next generation of globally transformative AI businesses. The new capital will be used to foster economic growth, develop more innovative AI technologies, create new companies and jobs, and empower the U.K. to compete in the AI market globally’ Nvidia will work in collaboration with Accel, Air Street Capital, Balderton Capital, Hoxton Ventures and Phoenix Court to accelerate the UK AI ecosystem with new capital for AI startups.

Nvidia’s CEO Jensen Huang commented,

“The United Kingdom is in a Goldilocks moment, where world-class universities, bold startups, leading researchers and cutting-edge supercomputing converge. There has never been a better time to invest in the U.K. - AI is unlocking new science and sparking entirely new industries. With new capital and advanced infrastructure, we are doubling down to empower the U.K. to lead the next wave of AI innovation.”

Saul Klein, founder of Phoenix Court observed “With nearly 800 venture-backed U.K. companies generating revenues of over $25 million, the opportunity now is to back the next wave of truly differentiated AI companies solving real-world challenges.”

As part of this process, cloud provider Nscale announced its first AI factory in the UK deploying 4,600 Nvidia Blackwell GPUs. It followed this up in September 2026 with a series of announcements around the launch of the UK-US Technology Partnership.

Nscale and Microsoft announced alongside Microsoft that it will build the UK’s largest AI supercomputer at Nscale’s AI campus in Loughton. It is intended the site will deliver 50MW of AI capacity, scalable to 90MW, and will initially house 23,000 Nvidia GB300 GPUs to be delivered in Q1 of 2027 to support Microsoft’s Azure services across the UK.

Separately, Nscale, OpenAI and Nvidia intend to establish Stargate UK, a UK version of the US programme. The UK scheme is a planned infrastructure platform to deploy OpenAI’s technology, with a particular focus on sovereign workloads. OpenAI will explore sourcing 8,000 Nvidia GPUs in Q1 2026 potentially scaling to 31,000 Nvidia GPUs over time at a number of sites in the UK

In total Nscale may deploy up to 58,640 NVIDIA GPUs across the UK, part of the company's broader plan to deploy 300,000 Nvidia GPUs globally. On the back of this Nscale raised what it called the largest Series B in European history at $1.1bn, followed shortly by a $433m pre Series C SAFE . The round was led by Aker ASA and supported by Nvidia amongst others.

In Germany, Nvidia and its partners are building the world’s first industrial AI cloud for European manufacturers. It will be powered by Nvidia DGX B200 systems and Nvidia RTX PRO servers featuring 10,000 Nvidia Blackwell GPUs and will be used accelerate manufacturing applications including design, engineering, simulation, digital twins and robotics. Leading start up German AI companies are closely aligned with Nvidia. Black Forest Labs, which specialises in AI image generation, has a partnership with Nvidia to accelerate the development of its AI models using Nvidia's infrastructure and TensorRT framework. DeepL, the German developer of AI translation software, is among the first to commercially deploy the DGX SuperPOD which, it is said, would make it capable of translating the entire internet in 18 days, down from a previous 194 days.

In Italy NVIDIA is collaborating with Italian supercomputing organizations, academia, AI startup Domyn and other companies to support industries with local AI factories and sovereign AI infrastructure. Model builder Domynis collaborating with Nvidia on a large AI factory powered by 5,760 Nvidia Grace Blackwell GPUs. The AI data center from Domyn includes plans to use Nvidia techniques for building AI agent platforms with advanced open reasoning foundation models. Domyn’s supercomputer will support the development of large-scale AI solutions in highly regulated industries. Domyn is in the middle of a planned €1bn equity raise to help fund its AI gigafactory projects and expand its large language model offerings. It is not known whether Nvidia will participate.

On a pan European basis Nvidia has announced the expansion of NVIDIA DGX Cloud Lepton™ to connect Europe’s developers to NVIDIA’s global compute ecosystem. DGX Cloud Lepton™ is an AI platform featuring a global compute marketplace that connects developers building agentic and physical AI applications with GPUs now available from a growing network of cloud providers. This enables developers to keep their data local, supporting data governance and sovereign AI requirements. NVIDIA is working with Accel, Elaia, Partech and Sofinnova Partners to offer up to $100,000 in GPU capacity credits and support from NVIDIA experts to eligible portfolio companies. Early adopters include the UK digital medicine company Biocortex, the French AI startup Bioptimus which is developing a foundational model for biology, and the UK drug discovery company Latent Labs.

Nvidia has upped the pace and scale of its direct investments into AI related start ups in recent months. We can identify 74 startups where Nvidia has a stake, either directly or through its venture arm NVentures. Nvidia made about 17 investments in 2023, 29 in 2024 and year to date has made 28 investments. Of these 20 have come since July. Nvidia is also reported to be on the verge of a number of further substantial investments. These include an up to $1bn investment in Poolside; a reported impending $500m further investment in the UK autonomous vehicle business Wayve; and a $100m investment in the UK AI manufacturing software platform business, PhysicsX.

Nvidia has of course also been active in promoting IA infrastructure in the US. It is a key technology partner in the Stargate Project, originally announced in January 2025. The Stargate Project is a new company which intends to invest $500bn in the next four years building new AI infrastructure for OpenAI in the United States.

It is a gathering of the technology clans with some powerful financial backing. The initial equity funders are SoftBank, OpenAI, Oracle, and MGX, the Abu Dhabi based fund investing in AI initiatives. SoftBank and OpenAI are the lead partners, with SoftBank having financial responsibility and OpenAI in charge of operations. Masayoshi Son of SoftBank is the chairman. Arm, Microsoft, Nvidia, Oracle, and OpenAI are the technology partners.

The new company was announced by President Trump who dubbed it 'the largest AI infrastructure project by far in history' saying it would help keep 'the future of technology' in the US.

The companies announced an immediate $100bn of funding and revealed that its first data centre is already under construction in Abilene, Texas. It is one of an initial ten datacentres each of 0.5m square feet to be built. The revenue model and what products and services are to be offered are yet to be disclosed.

Separately in September 2025 OpenAI and Nvidia announced a strategic partnership to deploy 10 gigawatts of AI data centres with Nvidia systems, equivalent to millions of GPUs, to support Open AI’s AI infrastructure. To facilitate this deal Nvidia intends to invest up to $100bn in OpenAI progressively as each gigawatt is deployed, with the first phase targeted to come online in the second half of 2026. Nvidia had previously participated in the $6.6bn Series E funding round for OpenAI led by Thrive Capital in October 2024.

Nvidia was an early investor in AI datacentre business, CoreWeave participating in its $221m round in April 2023 and in subsequent rounds. It continues to own a stake worth around $3bn. In September 2025 Nvidia agreed a deal to purchase unsold compute capacity from CoreWeave for $6.3bn. The deal will involve Nvidia buying any residual cloud capacity not sold to other customers. The primary customers of CoreWeave are Open AI and Microsoft. This unusual deal would appear to be providing a backstop guarantee to Coreweave in case its expansion plans, which involve the purchase of hundreds of thousands of GPUs from Nvidia, should not be fulfilled.

Lambda is a cloud provider specialising in AI training and inference. Nvidia participated in its $480m Series D in February 2025. In September 2025 Nvidia agreed to lease 18,000 of its own GPUS from Lambda in a deal worth c$1.5bn. This makes Nvidia the biggest customer of Lambda. According to reports the GPUs will be used for in house purposes by Nvidia. Presumably, the GPUs in question were previously sold by Nvidia to Lambda.

The exhibit outlines Nvidia’s participation in other datacentre deals. In February 2025 it supported the $305m Series B by Together AI led by General Catalyst. Together AI has 200 MW of power capacity and is deploying Nvidia Blackwell GPU clusters across North America. Firmus Technologies is an Australian business which closed an A$330m round led by Ellerston Capital with participation from Nvidia. The funds will contribute to the development of Project Southgate, Firmus' flagship initiative in Tasmania, to establish Australia’s first sovereign AI factory campus, a facility with 36,000 Nvidia GPUs.

Crusoe Energy is a major datacentre provider to Open AI. It raised a $600m Series D in December 2024 in which Nvidia invested. In June 2025 it raised a $750m credit line from Brookfield Asset Management to establish data centres with Nvidia GPUs and related infrastructure. It is planned that its data centre in Abilene, Texas will host 400,000 Nvidia GPUs. In October 2025 Crusoe, describing itself as the AI factory company, raised a $1.375bn Series E at a valuation of $10bn with Nvidia again participating in the Valor and Mubadala led raise. The raise will support the development of Crusoe’s newest planned data centre, this one a 10 gigawatt facility in Wyoming.

Supporting data centres in a different way, Nvidia’s venture capital arm, NVentures, participated in the August 2025 Series B2 $865m raise by Commonwealth Fusion which is developing a fusion reactor to power the datacentres of the future.

Nvidia - Participation in Funding rounds for AI Datacentre businesses

Source: Rothschild & Co

Source: Rothschild & Co

Somewhat in the face of Open AI’s preference that its investors don’t support other LLM companies, Nvidia participated in the $6bn raise by xAI in December 2024. Unlike OpenAI, which uses cloud providers for its compute power, xAI prefers to own its own data centre capacity. Currently xAI is putting together a special purpose vehicle with the intention of raising c$20bn which will be used to fund the building of xAI’s Colossus 2 datacentre in Memphis. Press reports suggest that the structure of the deal, being put together by Valor Partners, is $7.5bn of equity and $12.5bn of debt which will be used primarily to lease Nvidia GPUs. xAI will have the option to buy the GPUs outright at the end of the lease period. Nvidia is believed to be contributing up to $2bn to the $7.5bn equity raise.

Nvidia has been a significant presence in other rounds for leading LLM companies. We have already touched on Nvidia’s support for the $2bn Mistral raise in October this year. Nvidia was an investor in the $2bn raise in June by Thinking Machines Lab, the largest seed round in Silicon Valley history which was led by a16z. Thinking Machines Lab automates the creation of custom frontier AI models.

Inflection AI raised $1.3bn in funding in a deal led by Microsoft and Nvidia in June 2023. Alongside Nvidia and Coreweave, Inflection AI is building the largest AI cluster in the world comprising 22,000 Nvidia H100 Tensor Core GPUs. Inflection AI has used this to develop its own LLM Inflection 1 which in turn enables users to interact with Pi (stands for personal intelligence), a chatbot designed to be an AI driven personal assistant with ‘emotional’ features. More recently Inflection AI has shifted to use Intel’s Gaudi 3 accelerators. In September 2025 Nvidia announced that it will invest $5bn in Intel common stock.

Cohere is a Canadian business specialising in LLMs for enterprises, notably those in regulated fields such as finance, healthcare, manufacturing and the public sector. Nvidia has supported Cohere in multiple funding rounds, most recently in the $500m Series D in August which valued the business at $6.8bn.

In early October 2025 Reflection AI raised $2bn at an $8bn valuation in a round led by Nvidia. The company develops open-source AI models. Reflection AI releases for public use the model weights which are the core parameters that drive how an AI system works while reserving datasets and other proprietary elements for itself.

Nvidia - Participation in Funding rounds for AI LLM businesses

Source: Rothschild & Co

Source: Rothschild & Co

Quantum computing is one of the key future building blocks for the development of AI. Quantum computers use the principles of quantum physics potentially to bring a new level of computational power to bear in AI by processing vast amounts of data in parallel, enabling them to address complex problems more efficiently than can be achieved with traditional computing techniques. In turn AI techniques improve the efficiency of quantum calculations and data analysis.

In March 2025 Nvidia established NVACQ, the Accelerated Quantum Computing Research Centre in Boston, alongside both education (Harvard, MIT), and commercial partners (Quantinuum, QuEra, Quantum Machines). Its intention is to integrate quantum hardware with AI supercomputers, to develop ‘accelerated quantum supercomputing’ to make quantum computing more effective.

In recent months Nvidia has been a prominent investor in the recent flurry of quantum venture deals. Nvidia’s NVentures participated in the September $1bn Series E from Australia’s PsiQuantum led by BlackRock, Temasek and Baillie Gifford which valued the company at $7bn. Alongside the raise PsiQuantum announced a collaboration with Nvidia to accelerate quantum computing development with areas of cooperation including quantum algorithms and software, GPU-QPU integration and PsiQuantum’s silicon photonics platform.

September also saw a $600m raise at Quantinuum at a valuation of $10bn led by Honeywell and supported by Quanta Computer, NVentures and QED Investors. Like at PsiQuantum there is an operational agreement with Nvidia. The company ‘will work with NVIDIA as a founding collaborator on breakthroughs at the NVIDIA Accelerated Quantum Research Center. Additionally, Quantinuum has entered strategic partnerships aimed at innovative quantum computing solutions that will expand the capabilities of classical artificial intelligence and realize next-generation technologies.’

QuEra Computing raised a $230m Series B in February plus an undisclosed investment from NVentures in September 2025 and ‘QuEra will continue to collaborate with NVIDIA on go-to-market initiatives aimed at high-performance-computing centres worldwide, integrating QuEra’s neutral-atom systems with NVIDIA accelerated computing infrastructure and software stack.’

In April 2025 Nvidia SandboxAQ, which is a developer of large quantum models LQMs for enterprises in fields like life sciences, financial services, navigation and cybersecurity raised $450m in a Series E round in which Nvidia participated alongside Google, valuing the company at $5.75bn.

Nvidia - Participation in Funding rounds for Quantum Computing businesses

Source: Rothschild & Co

Source: Rothschild & Co

Nvidia has shown a distinct appetite to help fund development and the ecosystem in a number of other industry areas. Surveying these briefly:

Nvidia has been working with the UK autonomous vehicle business Wayve since 2018. AI is a critical functionality for AV companies and Wayve has progressively introduced Wayve GAIA, a generative world model for autonomy and Wayve PRISM, a 4D scene reconstruction model enabling photorealistic representations of dynamic scenes which in turn play a key role in the decision-making capabilities of the Wayve AI Driver. Nvidia’s background as a developer of graphic chips has a clear crossover here. Nvidia participated in Wayve’s May 2024 $1.05bn round. In September 2025 Nvidia announced that is considering a $500m investment in Wayve as part of a round which may eventually reach $2bn.

In August this year the US AV business Nuro got backing from Nvidia and Uber amongst others in its $203m round which valued the company at $6bn.

nvidia - Participation in Funding rounds for Autonomous Vehicle businesses

Source: Rothschild & Co

Source: Rothschild & Co

The related industry of Robotics has also seen a high level of participation by Nvidia. It appears to be an area of focus for NVentures with six of its portfolio companies being in this field. There has also been direct investment from Nvidia. Notably it participated in the $1.0bn Series C raise by FigureAI in September 2025 which valued the company at $39bn. The deal was led by Parkway Venture Capital and Brookfield with a number of industrial backers, including a substantial investment from Nvidia. Figure AI is developing humanoid robots and says the funding will be used to expand production at its BotQ high-volume manufacturing facility and to expand real-world deployments, enabling robots to assist with household and commercial workforce tasks. It will also scale its AI platform Helix with its core models for perception, reasoning, and control, and launch advanced data collection.

Nvidia - Participation in Funding rounds for Robotics businesses

Source: Rothschild & Co

Source: Rothschild & Co

Another major focus area for NVentures is drug discovery, with a steady string of deals over the last three years. In January 2025 Nvidia announced a series of partnerships with IQVIA, Illumina, Mayo Clinic and the Arc Institute to use Nvidia AI to infuse the healthcare and life sciences industries with AI techniques to accelerate drug discovery and enhance genomic research. The largest raise in which Nvidia has been involved is the $300m Series C for Genesis Therapeutics in November 2024. Nvidia was involved in its $200m Series B in 2023 and NVentures raised its stake in November 2024. Gensis intends to apply Nvidia capability to make computation in neural networks used for drug discovery more efficient.

The most recent raise in this industry came with Nvidia’s participation in the NEA led $80m Series B from the UK biotech Charm Therapeutics in September this year. Charm Therapeutics is seeking to develop precision oncology treatments through its proprietary AI-driven drug discovery platform.

Nvidia - Participation in Funding rounds for drug discovery businesses

Source: Rothschild & Co

Source: Rothschild & Co

For completeness we show where else Nvidia is invested in the balance of its venture and growth portfolio.

Notable in this group are Scale AI which delivers high quality training data for AI applications like autonomous vehicles, mapping and robotics. Nvidia participated in its $1bn round which valued the company at $14bn in May 2024. Other data businesses in which Nvidia is invested include Weka and Minds DB.

In April 2025 Nvidia invested alongside FMR in the $308m round by AI generative video business Runway. This is an example of Nvidia supporting AI projects which expand beyond text and image tools into video. In a similar vein there are a number of investments in 3D model businesses such as Luma Labs which creates AI generated videos from text prompts or images. Most recently Synthesia, an investment in October 2025 is a UK business generating AI video for corporate use.

Nvidia - Participation in funding rounds for Data, AI video generation, 3d models and other businesses

Source: Rothschild & Co

Source: Rothschild & Co

Private Market conditions - Positive signs

Some indicators of the state of private markets.

Public markets are clearly running high with the three-year bull market since October 2022 having seen the FTSE 100 rise by 43%, the S&P500 by c90% and NASDAQ by c120%.

In the same period the FTSE Venture Capital Index is up by almost 150%.

Unicorn creation

Some recent indicators of the flush of enthusiasm in the venture markets. The first one is from Crunchbase and shows the pace of new unicorn creation globally on a monthly basis since the start of 2021. It shows the accelerating pace of unicorn creation in 2025.

The exhibit below illustrates the heavy level of unicorn (companies valued at $1bn or more) creation at the peak of the market in 2021 and its immediate aftermath in 2022.

Unicorn creation was subdued in 2023 and 2024 with respectively 102 and 112 having been created in those years.

In the first three quarters of 2025 117 new unicorns were created at an annualised rate of 156 new unicorns. 79 of these have been created in the five months since May. September’s total of 26 is the highest monthly number since June 2022.

Five healthcare companies were represented in September’s 26 new unicorns - Strive Health $1.8bn, Ultragreen.ai $1.3bn, Lola Sciences $1.2bn, Enveda Biosciences and Thyme Care (both $1bn).

Four were AI businesses, Baesten Infrastructure $2.2bn, Invisible Technologies (AI data) $2bn, Distyl AI, (AI consultant) at $1.8bn and You.com at $1.5bn. There were two AI datacentres (Nscale $3.1bn) and Firmus Technologies in Australia at $1.2bn plus two AI cloud businesses in Modular at $1.6bn and Modal Labs ($1.1bn). LegalTech, a prominent AI application was represented by Filevine ($3bn) and Eve ($1bn)

Three were fintechs, Tide (services to SMEs, $1.5bn), Lead (banking-as- a-service, $1.5bn) and neobank Kapital ($1.4bn) plus two crypto businesses, Zerohash and RedotPay (both $1bn)

The rest came from a scattering of industries including semiconductor business Rebellions ($1.4bn), software company PostHog ($1.4bn), smartphone maker Nothing ($1.3bn), IQM quantum computers ($1bn), Periodic Labs in materials science ($1bn) and aerospace business Apex ($1bn).

By geography 17 of the 26 September unicorns are based in the US (nine of them in California), four in Europe (Nscale, Nothing and Tide in the UK and IQM Quantum in Finland) with one each in Mexico, South Korea, Singapore, Hong Kong and Australia.

Global new unicorn count by month

Source: Crunchbase

Source: Crunchbase

For interest, the next chart shows the breakdown of the total Crunchbase Unicorns Board (there are 1627 of them) by industry. Software predominates.

Crunchbase Unicorn Board - Top industries by unicorn counts

Source: Crunchbase

Source: Crunchbase

Exits - IPOs

Recent months have seen the US IPO market pick up, albeit modestly and with momentum checked in the last month by the US government shutdown. Q3 2025 was the most active quarter for US IPOs since 2021 with 23 deals of $100m or more, including five IPOs raising more than $1bn.

YTD to the end of September there were 176 IPOs raising $32.8bn, a 20% increase over the $27.4bn raised at the 9m stage in 2024 and in line with the $33bn full year total for 2024. September, which saw $8bn raised, was particularly strong.

US IPO market year to date

Source: EY Analysis, Dealogic

Source: EY Analysis, Dealogic

Exits – M&A

The M&A market has also seen strong signs of resurgence. Global M&A deal value is estimated by Pitchbook to have increased 26% yoy after nine months of 2025. As the exhibit indicates Q3 2025 deal value was the highest since Q4 2021.

YTD to end September global M&A deal value is estimated by Pitchbook at $3.4tn. This is just behind the full year 2024 total of $3.6tn and puts the annualised 2025 total at c$4.5tn. This is c$1tn more than the totals in each of 2022, 2023 and 2024, and would be not far off the record total of $4.85trn in 2021.

YTD the value of global M&A deals is estimated at $3.4 trillion

Source: Pitchbook

Source: Pitchbook

Valuations

Always a tricky subject to encapsulate. The recent Fenwick Venture Beacon Q3 Report does a good job (See Fenwick Q3-2025-Venture-Beacon-Market-Trends) . Its key conclusions are

Early stage raises (Seed, Series A and B) are seeing valuation increases. The percentage of down rounds in this category has reduced from 18% in H2 2024 to 13% in H2 2025 to date. Pre-money valuations are up quarter on preceding quarter in Q3 by between 2-29%.

There is a pivot point at Series C as companies shift from growth to scale up stage. Here Fenwick reports a declining trend in valuations through 2025, and a sharp 40% quarter on quarter decline in Q3 . Down rounds are running at 28% of the total through H2 2025.

Later stage Series D rounds are seeing valuation increases- up 42% QoQ in Q3.

Fenwick observes that AI companies enjoy a significant valuation premium over non-AI peers across nearly all sectors, with 2.5x higher revenue multiples (20x vs 8x).

Public market resilience

Markets remain resilient, seemingly in the face of anything thrown at them. The longest US government shutdown on record seemed to have minimal impact on markets while it was happening, but its cessation then sparked a further market rally. The raising and then lowering of tensions on US-China tariffs appears to have emerged as a net positive for markets. The threatened 100% tariffs on China have gone and some tariffs have been lowered, US soy beans will now flow into China while rare earths will make the return journey – for the next year at least. Meanwhile much financial newsprint is being devoted to the possibility of an AI bubble, yet the Magnificent Seven index is just 3.5% off its high towards the end of October and remains up 11% over the last three months.

In a seeming microcosm of the debates over the big tech stocks and AI valuations, Softbank sold its entire $5.8bn stake in Nvidia on November 11 with the intention of funding its recent $30bn commitment to OpenAI. The SoftBank share price initially fell by 10% on the news then rallied to close down just 3%. Nvidia shares fell just 2.5%.

To November 13 NASDAQ is now up 21% ytd, the S&P 500 up 20%, the FTSE100 up 19%, and the STOXX600 is up 14%.

We noted in our last Growth Equity Update that fund managers were in a bullish mood with the Bank of America global fund manager survey carried out in October observing that investor sentiment is at its most positive levels since February 2025, that the market expects either a soft economic landing (54%) or no landing at all (33%) with fears of a hard landing (8%) and global recession at their lowest level since February 2022. The number one upside risk factor for global growth is seen as the prospect of monetary easing.

The greatest risks to this optimistic picture are seen as an ‘AI equity bubble’ (33%) and a second wave of inflation (27%), albeit the percentage of investors who think global stocks are overvalued remains high (60%). Emerging Markets, are the most preferred region, followed by Europe and then the US, albeit the US is closing the gap.

Investor hopes of a soft landing with good economic growth, lowering interest rates and inflation under control were maintained with the much-anticipated Fed rate cut at the October 29 meeting seeing the benchmark rate cut by 25bps to 3.75%-4%. The CME Fed Watch index had a c99% expectation that Fed rates would be cut going into the October 29 meeting and a 98% certainty of another 25bps cut to 3.5-3.75% at the December 10 meeting.

The confidence of a rate cut at the final Fed meeting of the year has faded in the aftermath of the October 29 cut. Fed chairman Jay Powell said, as is his wont, that ‘ a further reduction of the policy rate at the December meeting is not a foregone conclusion’ and to reiterate that he wasn’t just saying it observed,

“I always say that it’s a fact that we don’t make decisions in advance. But I’m saying something in addition here: that it’s not to be seen as a foregone conclusion — in fact far from it.”

The Fed ‘s dot plot , published after the September meeting, indicated that of the 19 FOMC members (only twelve of whom have a vote), seven anticipated a rate of 4-4.5% at the 2025 year end; two were at 3.75%-4%, nine in the 3.5%-3.75% bracket and one at 2.75%-3%. It suggests a penchant for a further rate cut in December.

The Fed charman points out that the Government shutdown means that the Fed is making decisions in a fog, without a lot of data, and that ‘ What do you do if you’re driving in the fog? You slow down’. Equally the lack of data may mean that proponents of a further cut may see no incremental inflation/ jobs data to change their view while the influence of Jay Powell may fade as his term end, due in March 2026 approaches. In the absence of the official data, ADP’s private payroll data suggests that US private private-sector employers shed an average of 11,250 jobs per week in the four weeks ending October 25, and that the “labor market struggled to produce jobs consistently during the second half of the month’. Official October data may never be published.

The September inflation number, which was published, came in at 3% in line with expectations, up from 2.9% in August and 2.7% in July. It was the highest figure since January. Annual core inflation slowed to 3% from 3.1%.

Back to CME Fedwatch. The net effect is that expectations around a rate cut at the December meeting are much closer with market watchers at 53/47 in favour of a cut to 3.5%-3.75%. The view on rates after the 28 January 2026 meeting are 73/27 that the rate will be at 3.5%-3.75% or below versus the current rate. At end 2026 the most favoured rate expectation is 300-325bps, effectively a 75bps rate cut from current levels.

UK – A trifecta of indicators pointing to rate cuts:

Inflation better than expected: UK inflation was again at 3.8% in October, the same figure as reported in each of July and August. The figure was though better than expected with the Bank of England having warned inflation would peak at 4% in September. The data was published on October 22.

Jobs worse than expected: The jobs data, announced on November 11, was weak with the UK unemployment rate rising to a worse than expected 5% in the three months to September, with the estimated number of UK payrolled employees falling by 32,000 between August and September.

GDP growth worse than expected: On November 13, the latest ONS data showed UK GDP declining by 0.1% in September, worse than the zero outturn expected by the market. Pre Budget nerves (the budget is on November 26) and the Jaguar LandRover cybersecurity linked shutdown were put forward as specific reasons against the in any case tepid background.

The combination of better-than-expected inflation and worse than expected jobs and GDP growth has the market anticipating a rate cut with a c80% certainty in December. Previously the market was not expcting to see another cut until as late as March 2026.

At the November 6 meeting the BoE had decided to hold interest rates steady at 4%. It was a close call with a 5-4 split between holding steady or cutting by 25bps.

Bank of England governor Andrew Bailey indicated that he wanted to see more data before determining on future cuts (unlike his US counterpart he has that luxury) but the expected topping out of inflation seems key with the BoE saying future rate cuts

“…will … depend on the evolution of the outlook for inflation. If progress on disinflation continues, Bank Rate is likely to continue on a gradual downward path.”

The next BoE meeting is on 18 December.

In Europe the consistent message coming out of the ECB in the last few months has been that interest rates have reached an equilibrium after a period of sharp rate cutting. At its end October meeting the ECB again held interest rates steady at 2%. ECB president Christine Lagarde observed that EU monetary policy is ‘in a good place’ and that the outlook for inflation is ‘broadly unchanged’.

EU inflation was 2.1% in August and 2.2% in September. The ECB has a 2026 annual inflation forecast of 1.7%. Eurozone GDP growth grew 0.2% in Q3, better than expected. The ECB expects 2025 GDP growth of 1.2% and 2026 growth of 1% .

The ECB’s Vice president Luis de Guindos said in a mid November speech that interest rates are at the appropriate level barring changes in the economic situation. The market consensus now looks for interest rates to remain unchanged to the end of the year with a growing market view emerging that they will remain unchanged through 2026.

Market-implied policy rates for the US, UK, Eurozone and Switzerland

Source: R&Co, Bloomberg, Wikimedia Commons

Source: R&Co, Bloomberg, Wikimedia Commons

Rothschild & Co strategist Kevin Gardiner summarises the current key drivers of the market in this graphic

Source: Rothschild &Co

Source: Rothschild &Co

October's growth raises

Again strong. October’s European deal value at $6.1bn was up 73% yoy. The US at $21.1bn was up 33% yoy.

October was another substantial month in European growth equity raises with the Rothschild & Co Deal Monitor recording $6.1bn of growth equity and VC deals of $20m and above across 64 raises.

That figure was 73% higher than the amount raised in October 2024 ($3.5bn) and 4.7x the amount raised in October 2023. It was the third highest month by value in the last four years after September 2025 ($7.1bn) and September 2023 ($6.8bn).

The year to date European fundraising to end October is at $41bn, up 33% yoy.

October was characterised by:

A lot of deals. In total there were 64 deals of $20m and above in October. The average monthly deals in 2024 were 41 and ytd in 2025 are 55.

There were more big deals. In total there were 156 deals of $100m plus in October, the joint highest (with January 2025) in the last three years. Two of the deals exceeded $500m, Oura at $900m and Bending Spoons at $710m.

It wasn’t about AI: The European Growth equity market is putting in good deal value numbers but it is not all about AI. September was, somewhat unusually, led by AI with the big Mistral raise but October reverted to type with a narrowly defined $369m raised in AI across three deals – or if we include LegalTech (Legora at $150m) and Autonomous Vehicles (Avride in the Netherlands at $375m), a widely defined total of five deals raising $894m. Even this larger figure was beaten by software (16 deals including the $710m Bending Spoons) at $1.34bn; by Healthcare at $1.06bn including the $900m for Oura and by Biotech with ten deals raising $1bn, including $395m for the German oncology specialist Tubulis.

By contrast Climate Tech, five deals for $635m and fintech, four deals for $199m, were relatively subdued.

Europe - 64 deals raised $6.1bn in october

Source: Rothschild & Co

Source: Rothschild & Co

Four of October’s deals enter the top 10 European deals by value year to date.

Europe - the top 10 VC raises YTD

Source: Rothschild & Co

Source: Rothschild & Co

The US had a very strong October with 60 deals of $100m or more raising $21.2bn. This compares with 45 deals raising $15.9bn in October 2024, a rise of 33% yoy in deal value.

The key points about October’s US raises are:

Even stronger than it looks. In September, the value of US raises was 6.4x the level of September 2024. October 2025’s $21.2bn was just 33% ahead of October 2024. What this disguises is that the US growth equity market only started its AI fuelled boom in October 2024. Prior to that the average monthly value of $100m raises in the first nine months of 2024 was $6.9bn. Between October and December 2024 the monthly totals averaged $16.1bn with October at $15.9bn. So, October 2024 was a tough comp and October 2025 comfortably beat it.

Just more deals: As in Europe one of the keys to the yoy growth in the market is just the sheer number of deals. The average deal value in October 2024 (in our monitor of $100m plus deals) was $354m. In October 2025 the average deal size was almost identical at $353m. The key is that 2025 saw a third more deals , 60 rather than 45. It suggests that what started as an AI LLM boom in Q4 2024 (the big deals were $6.6bn for OpenAI in October 2024, $6bn and $4bn for xAI and Anthropic in November 2024 and $10bn for Databricks in December 2024) has widened. The biggest deal in October 2025 was $2bn, a level reached for Reflection AI (the open-source superintelligence AI model) and the prediction market platform, Polymarket. The key is there were a further four $1bn plus deals versus none in October 2024.

AI leads again: In the first nine months of 2025 60% of the total money raised in the US growth equity market was for AI businesses. The pattern of AI prominence was repeated, but not as prominently, in October with $7.9bn of raises representing 37% of the total. The difference was the absence of a single large LLM style deal. Biotech was the second largest category at $2.8bn (13% of total), followed by Fintech ($1.5bn, 7%) and a weaker month for software raises at $1.1bn (5%).

USA - 60 raises of $100m + in October for a total of $21.2bn

Source: Rothschild & Co

Source: Rothschild & Co

YTD US raises to end October are at $182.5bn, 2.3x the amount raised in growth equity in the first ten months of 2024 and 1.6x the amount raised in the whole of 2024.

The scale of the dominance of AI deals, particularly amongst larger deals, is demonstrated in the next Exhibit. There have been 23 $1bn plus growth equity raises in the US ytd. Six of these deals were in October. In total the 23 deals raised $102.9bn. Of these 14 deals were for AI businesses and they raised $88.3bn, 86% of the total.

US - top 23 Raises ($1bn+) in first 10m of 2025 - dominated by AI

Source: Rothschild & Co

Source: Rothschild & Co

Fundraising outlook: $40bn of potential raises

A continuing strong pipeline of impending raises.

Our Deal Monitor of impending raises continues to look healthy. We identify c$30bn of impending US deals and $10.6bn in Europe.

At the top of the US list and emphasising the return of crypto, Tether, the stablecoin issuer, is widely reported to be looking to raise between $15-$20bn for a c3% stake. The deal could ultimately value Tether at around $500bn. Meanwhile the crypto exchange Kraken is reportedly looking to raise c $500m in a deal that would value it at $15-20bn.

Otherwise, the list is AI heavy. xAI is pursuing a $20bn raise, this one for $7.5bn of equity plus c$12.5bn of debt. AI video generation business Luma has a planned $1.1bn raise at a valuation of $3.2bn. Data centres business Crusoe Energy is said to be raising $1bn at a $10bn putative valuation. AI video generation business Runway is said to be raising $500m in a deal led by General Atlantic.

In Europe the previously rumoured raise of $1bn and then $2bn for Revolut has turned into a rumoured $3bn raise at a valuation of $75bn. A secondary round forms part of the total. Revolut’s revenues are believed to be on track for $5.9bn in 2025. Notable additions to the list are the expected $2bn raise for autonomous vehicles business Wayve, led by Nvidia, Microsoft and Softbank and $2bn for the French AI coding business Poolside led by Magnetar and Nvidia plus $1.15bn for Italian AI infrastructure business, Domyn.

In a more traditional industry Swedish textile impact business Syre (decarbonising and dewasting the industry through textile-to-textile recycling) is raising $600m. The business is supported by H&M and Vargas and has a new deal with Nike.

US Growth Equity - c$30bn in reported upcoming raises

Source: Rothschild & Co; press reports

Source: Rothschild & Co; press reports

european growth equity - c$10.6bn in reported upcoming raises

Source: Rothschild & Co; press reports

Source: Rothschild & Co; press reports

Our views on the state of the venture capital markets

October 12, 2022 marked the low point for the S&P500 on the back of global inflation, rising interest rates, and increased geopolitical risk. It also ended the buoyant market conditions for the venture capital market that saw its activity and valuations peak in late 2021.

October 12, 2025 marked the third anniversary of the bull market that has seen the S&P500 rise by almost 90% and NASDAQ by 120%.

In that period the FTSE Venture Capital Index was up by almost 170% and since June 2025 has been back above its previous 2021 peaks.

This revival of the growth equity market has been led by the US and by a surge of interest in artificial intelligence model providers and for companies using AI to transform a range of underlying industries.

Ast the same time the venture industry has re-adopted strong underlying approaches to investment with companies in most sectors striving to achieve a better balance of growth, profitability and cash flow. The underlying quality of the cohort of VC backed companies has improved.

Our summary of the outlook

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, semiconductors) supporting the development of AI.

- Outside the AI space the VC market is regaining confidence with the strength of interest in Software being notable and fintech and biotech reviving strongly.

- There is a burgeoning interest in defence industries from investors with both the tense geopolitical political environment, the advances in AI applications and the experience of the combat in Ukraine contributing to investor focus. By contrast, ClimateTech, while still a substantial sector has become less prominent both as a result of some high profile failures and being less favoured politically in the US under the current administration.

- Fund raising for venture capital firms remains subdued. Fund raising is concentrating into larger, established firms. Overall US VC fundraising was on a rate at H21 2025 to be at near decade lows.

- The speed of the investment process has slowed down since 2021-22. The level of diligence on deals has stepped up. This is true even in the ‘hot’ parts of the market like AI. Outside these areas it is marked – processes take time, downside protection is sought.

- Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on the combination of growth and profitability (or a rapid path to it) and on free cash flow.

Read the previous editions: May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024, January 2025, February 2025, March 2025, April 2025, May 2025, June 2025, July 2025, August 2025, September 2025, October 2025

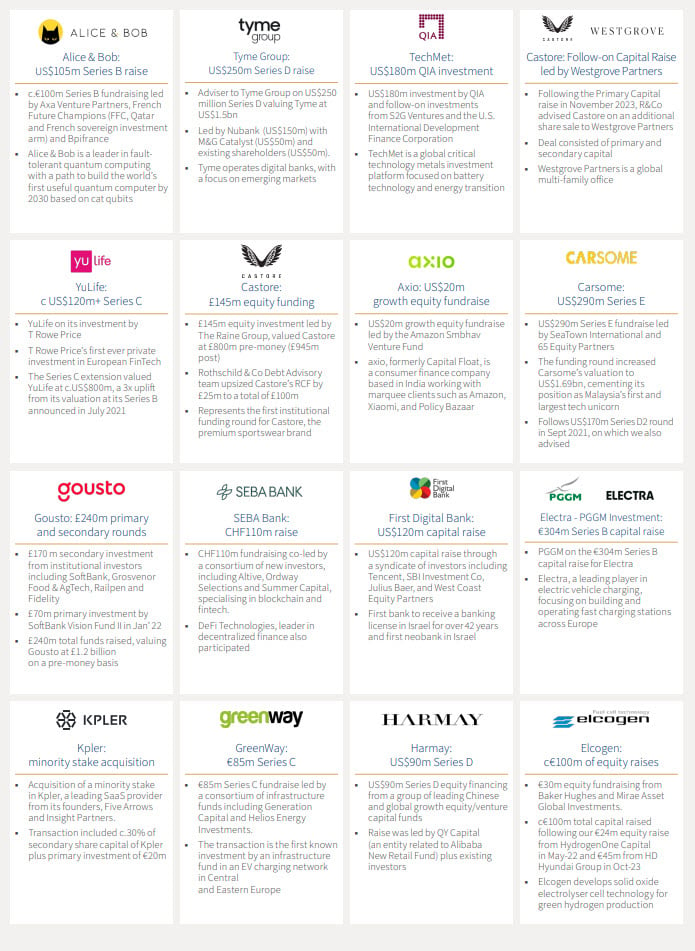

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Co-Head of Global Market Solutions

+1 212 403 5500

+1 917 297 5131

Global Head of Strategic and Private Investors.

+44 20 7280 5826

+44 7753 426 961

Vice Chairman of Equity Capital Markets Europe

+44 20 7280 5088

+44 7542 477 291

Co-Head of Equity Capital Markets Europe

+44 20 7280 5377

+44 7907 712 978

Co-Head of Equity Capital Markets Europe

+44 20 7280 1668

+44 7912 395 294

Head of Private Distribution

+44 7926 905 488

Head of Private Capital, North America

+1 212 403 5559

+1 917 594 7208

Director of Private Distribution

+44 20 7280 1351

+44 7788 395 556

This document is being provided to the addressed recipients for information only and on a strictly confidential basis. Save as specifically agreed in writing by Rothschild & Co Equity Markets Solutions Limited (“Rothschild & Co”) this document must not be disclosed, copied, reproduced, distributed or passed, in whole or in part, to any other party.

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.