Growth Equity Update

June 2025 – Edition 39

- Major AI fund launches: Saudi Arabia is launching the $10bn state backed Humain Ventures to focus on AI in the US, Europe, and Asia. In France Cathay Innovation has just closed a €1bn AI fund.

- And funds launching using AI: A $250m fund raise by Quantum Light, ‘the world’s first truly systematic venture capital and growth equity firm’ started by Revolut’s founder, uses a proprietary AI system, Aleph, to ‘identify the next 10x companies.’

- Valuations firming up: Pitchbook indicates the percentage of European venture raises that were downrounds fell from 17% in Q1 2024 to 12% in Q1 2025.

- Tibi or not Tibi: The UK government is enlisting pension funds to support investment in private UK businesses and projects. We look at how France’s Tibi plan has approached the use of state influence to promote early-stage businesses.

- The UK Mansion House Accord has 17 of the largest workplace pension providers pledging 10% of their DC default funds to private assets. The accompanying Pensions Investment Review addresses key issues like value for money. It falls short of mandating the 10% commitment but allows for a reserve power.

- Rothschild & Co is hosting a London conference on 10th June – Funding the UK Innovation Economy- Delivering on the Mansion House Accord.

- IPOs outflanked by private raises: With markets stabilising, a trickle of IPOs has resumed on both sides of the Atlantic. In the US ytd 81 IPOs have raised $11.8bn; meanwhile 178 growth equity raises of $100m+ have garnered $90bn.

- Against tough comps May saw $12bn of US VC deal raises, up 5% yoy. Europe was up 12% at $3.8bn.

- Fall if you will, but rise you must – James Joyce.

Click here to download a PDF version of Growth Equity Update

The Humain League – Together in Electric Dreams

Saudi Arabia is launching a $10bn venture fund, Humain Ventures, in the summer of 2025 to focus on AI startups in the US, Europe, and Asia.

Just ahead of US President Trump’s visit to Saudi Arabia on the 13th-16th May, the Crown Prince of Saudi Arabia announced the launch of a new Saudi artificial intelligence company, Humain. It will initially be funded by the PIF as part of the Vision 2030 initiative in Saudi to diversify the country’s economy beyond energy.

The stated objective of Humain is to develop advanced data centres, AI infrastructure, associated cloud technology and the world’s most powerful Arabic large language model. It initially aims to establish 1.9 gigawatts of data centre capacity by 2030 enabling it to process 7% of global AI training and inference at that point. It then intends to push on to reach a capacity of 6.6 gigawatts by 2034. The expected cost of the project is in the order of $77bn.

The CEO of Humain, Tareq Amin, is reported to be in talks with several US tech groups and investors, including a16z, OpenAI and xAI with a view to finding a substantial equity partner for its data centre business.

A number of US companies have already announced partnerships with Humain. These include Nvidia which will supply c18,000 of its recently developed Blackwell GPUS. AMD is partnering to provide 0.5bnMW of AI computing infrastructure. Amazon has committed to establish a $5bn ‘AI zone’ in Saudi. Other deals involve Qualcomm and Supermicro.

The first phase of the plan sees the establishment of a 50MW plant utilising 18,000 Nvidia GPUs in 2026. The expansion to 500MW will require c180,000 of the GPUs. One of the attractions to establish data centres in Saudi are low energy cost with the Saudi authorities offering to discount (the already very cheap, by global standards) electricity prices.

As part of the initiative Humain is to launch a $10bn venture fund, Humain Ventures, in the summer of 2025. Its CEO, Abdullah bin Sharaf Al-Ghamdi, has a wide-ranging brief for the operation. It is to focus on AI startups in the US, Europe, and Asia. At $10bn the fund would be one of the largest dedicated AI funds globally.

Meanwhile in France in late May Cathay Innovation closed a €1bn multi-stage fund with an AI emphasis. Cathay will target startup companies ‘applying AI deeply tailored to specific sectors’ with a focus on those employing AI techniques and disciplines in the fields of digital health, fintech, consumer services, mobility and energy.

The fund was originally announced in 2022, at which point it was somewhat different, targeting Series A and Series B companies with an emphasis on the sustainable transformation of industries in AI, digital health, mobility and energy tech. In 2023 the emphasis on AI was reinforced when Cathay allocated €50-100m specifically to support back French AI businesses. Cathay will now devote the whole fund to AI and associated ventures although its status as an Article 8 fund means it must still ‘promote’ environmental and social characteristics.

Cathay expects around half of the fund to be deployed in Europe and the rest in the US and Asia and indeed that is the shape of the c€235m already invested in fourteen companies. The seven that are European include Nabla (French AI assistant for doctors), two AI powered drug discovery businesses, Aqemia (France) and Owkin (UK), Bioptimus (biotech) and Entalpic (materials discovery).

The number of companies in which Cathay's new fund will invest will likely rise to around thirty, spread across all stages of development with widely varying ticket sizes. Denis Barrier, cofounder of Cathay Innovation comments “For portfolio champions, we’re looking to invest at least €50m throughout their lifetime.… With AI it is extremely important to have a fund with a significant size that can invest in founders from the start and then follow-on without having to raise capital externally.”

Cathay Innovation’s LPs are split roughly equally between financial and strategic investors. In many cases the strategic LPs, who include Sanofi, BNP Paribas Cardif, Total Energies and Valeo, are corporates looking to access technologies developed by the portfolio companies.

Barrier comments: 'We are entering a phase in AI where future champions will be those who can work together with the ecosystem to find solutions that will reinvent industries.’

The world’s ‘first truly systematic venture capital and growth equity firm’: In an intriguing take on AI fundraising, QuantumLight, the venture capital firm started by the founder of Revolut, Nik Storonsky, recently raised $250m. What is different about QuantumLight is its investment methodology. The firm claims to be ‘the world’s first truly systematic venture capital and growth equity firm.’ The $250m Fund I, is ‘backed by a global group of top-tier LPs, including billionaire tech founders and prominent institutions.’

QuantumLight has built a proprietary AI system called Aleph whose task is ‘identifying the next 10x companies.’ The system claims to analyse the entire universe of venture-backed companies since the 1990s, identifying robust and stable success patterns. The platform tracks 0.7m VC backed companies globally and has 10 billion data points for reference. The VC claims its 17 investments to date have all been selected using this method.

Nik Storonsky observes:

"Our ambition is to build the world’s best systematic venture capital and growth equity firm and support the new generation of founders by sharing some of the operating principles that we developed at Revolut."

Disappearing down rounds?

Valuations firming up - Pitchbook figures show that in Europe the percentage of venture raises that were downrounds fell from 17% in Q1 2024 to 12% in Q1 2025.

We have been noting for some time the buoyancy of the VC market on both sides of the Atlantic. The global market for VC grew in value in 2024 for the first time since 2021. The VC funding market has surged again year to date with the US up 3x yoy to $90bn in terms of funds raised to the end of May 2025 and Europe up 17% to $17.4bn in the same period.

Although public markets are relatively flat ytd this comes off the back of two strong years of public stock market performance (the S&P 500 was up 24% in 2023 and 23% in 2024). There has been substantial enthusiasm for AI driven businesses, but this is not the whole story with the value of raises for non-AI businesses also strongly up year-on- year.

Unsurprisingly this is beginning to feed into valuations. The Pitchbook European VC Q1 2025 Valuations Report records a year-on-year falling percentage of downrounds. It has the percentage of downrounds dropping from 17% in Q1 2024 to 12% in Q1 2025.

It observes that in Q1, valuations for European startups grew across almost all but the pre-seed stages, with the most significant increases in median prices, being seen in venture growth at +30% yoy and late-stage, +14%.

Q1 2025 median pre money VC valuations advance yoy

With the percentage of flat rounds at below 5% Pitchbook observes that over 80% of startups raising money in Q1 2025 did so at a higher price, which it describes as a decade-high rate. It is likely that the enthusiasm for AI and, more recently, for defence tech, helped these trends.

Unicorn activity also picked up with five new unicorns being established in Q1. These were TravelPerk, a travel software business with a $200m raise at a $2.7bn valuation; Synthesia, an AI powered video business which raised $180m at a $2.1bn valuation; Neko Health, a body-scanning healthtech valued at $1.8bn after a $260m Series B; Tines the Irish software monitoring business which raised $125m at a $1.125bn post money value; and payments business Rapyd that raised $500m at a $4.5bn valuation.

Deal sizes also increased yoy with the more mature companies benefitting the most. Late-stage deal sizes were 37% larger than 2024’s annual figure. The median deal size in venture growth rose almost 25% from 2024.

Deal sizes also rising

How they do it in France

The UK government is enlisting pension funds to support investment in private businesses and projects in the UK. We look at how France has approached using state influence to promote early-stage businesses in the pursuit of economic growth.

In recent editions of the Growth Equity Update we have looked at the efforts being undertaken by the UK government to promote venture capital investment in the UK via the Mansion House Accord.

In this edition we look at the system used by French governments to promote VC investment. In particular we focus on the Tibi scheme, an inspiration for the UK Labour Party’s approach to promoting investment by the state and we look at the role of the key state run VC investor, Bpifrance.

“We were a start-up nation; we are going to become a nation of large technology companies. France has a vocation to be one of the nations writing the 21st century.” French Economy Minister Bruno le Maire – June 2021.

In June 2017 French President Emmanuel Macron declared that France should become a start-up nation with entrepreneurs as the new role models. He lauded the excellence of France’s schools of engineering and expressed an ambition that the French state should act as a start-up, as a platform that makes it easier to become an entrepreneur.

His announcements included a €10bn public fund managed by Bpifrance to invest in start-ups. There were changes to the French tax system in capital gains and the wealth tax to encourage entrepreneurs and investors. Notably he confirmed the introduction of the French Tech Visa, a four-year visa to attract key workers from abroad to work in France.

In September 2019 President Macron announced ahead of France Digitale Day a new target - “I’ll leave you with a goal: there should be 25 French unicorns by 2025.”

In July 2019 the Tibi Report was produced under the auspices of the Ministry of the Economy and Finances produced by the economist and former banker Philippe Tibi of the École Polytechnique. Its aim was to address a perceived shortage of late-stage capital for French technology companies. Stating that, in the fourth industrial revolution Europe is far behind the US and China, it called for massive investment in disruptive technologies as a key driver of French sovereignty and future prosperity. By September 2019 the French government was able to say that it had secured €5bn of committed investment into tech businesses.

In January 2020 the target was extended to €6bn of commitments to support VC funding. In its first stage, Tibi 1, 24 institutional investors pledged c€6bn to private funds targeting growth-stage companies, the aim being to develop a more robust French ecosystem to finance Series B, C, and pre-IPO rounds without relying solely on foreign capital.

The Tibi initiative has a decentralized architecture with independently managed private equity and venture capital firms certified as eligible vehicles for Tibi labelled investments. Coordination is provided by a strategic committee under the French Treasury, which reviews investor commitments and fund certifications.

A review of the Tibi initiative carried out in June 2021 (and published in August) by the Ministry of Finance announced that it had exceeded expectations. Bruno Le Maire, the Minister of the Economy, Finance and Recovery Declared in June 2021

"I propose to you a new target of €30bn invested in French technological funds. This means that we must all mobilize but also mobilize new investors. I am thinking in particular of foreign investors, through the participation of eleven new investment bank partners, fund-raising intermediaries, who are going to go and mobilize these investors all over the world. This new target will enable us to increase the number of partner investors and increase the capital committed to funds invested in France and also allow long-term investment of the best foreign funds in our country.’’

Speaking at the same conference Philippe Tibi highlighted two key routes to reach the new target of €30bn target "the very important domestic channel, employee savings and retirement savings" on the one hand, and the "international channel, all long-term investors, sovereign funds, pension funds, foreign insurance funds and family offices."

Tibi 2, announced in 2023 saw a further €7bn in new financial commitments from 35 institutional investors and was focused more closely on strategic sectors deemed crucial for Europe’s technological sovereignty including AI, semiconductors, quantum computing, cybersecurity and climate tech.

By April 2024, 92 certified funds were managing a total of €22bn in assets, with a target to attain €35-40bn in portfolio volume.

Tibi 2 has helped to accelerate the growth of French VC and growth equity funds while encouraging cross-border European investment.

Meanwhile Bpifrance is France’s public investment bank. It was formed in 2012 from the merger of three state owned financial institutions OSEO, focused on finance for SMEs; CDC Enterprises, focused on equity investments for SMEs, VC and development capital; and Fonds Strategique Investissement, France’s sovereign wealth fund. The creation of Bpifrance was designed to unify these public investment vehicles to support French businesses and especially SMEs. Bpifrance is now owned by the French state and by the Caisse des Depots et Consignations, itself a public institution, and is funded by public budget allocations and allocations of capital from CDC supplemented by some European public money, leverage and returns from investments.

Bpifrance uses two main types of financing for start-ups, non-dilutive financing and traditional equity investing. Non-dilutive financing include takes the form of grants, prizes, tax cuts, and loans at reduced rates. For its equity investments Bpifrance invests directly through its specialised funds. In 2024 Bpifrance invested c€570m directly into 147 French start-ups with 58 first time investments in companies. It also acts as an LP for French VC firms committing €1.7bn to French venture funds in 2024.

There are also sector specific initiatives. Bpifrance has said that it will devote €10bn of investment to the French AI industry by 2029. It was an early investor in the French LLM Mistral and has a €50m seed investment fund for early-stage AI business plus a €25m AI booster programme to help SMEs adopt AI techniques.

The January 2019 deeptech plan was launched with an initial funding envelope of €2.5bn and had as its target the creation of 500 new deeptech starts ups annually by 2030.

Bpifrance also has an informal role as a promoter of an entrepreneurship culture in France aligned with President Macron’s aim to present France as a ‘start up nation’.

The Mansion House Accord and mandation - Never say never

The UK Government’s Mansion House Accord has seventeen of the UK’s largest workplace pension providers pledging to invest 10% of their DC default funds in private assets. The simultaneous Pensions Investment Review supports the process by addressing issues such as value for money. The review falls short of mandating the 10% commitment but allows for a reserve power if necessary. As Chancellor Rachel Reeves says, ‘never say never.’

In its Mansion House Accord published on May 13 seventeen of the UK’s largest workplace pension providers pledged to invest 10% of their DC default funds in assets that boost the UK economy such as infrastructure, property and private equity by 2030, with at least half allocated to the UK. The government says that this should release ‘£25 billion directly into the UK economy by 2030.’

The Accord indicated that ‘progress against the commitment will be monitored’. The signing of the Accord is a voluntary expression of intent by the signatories. There remains a debate about whether the commitment might become mandatory on due course. When the Accord was signed the UK government said it would be:

‘…reinforced by measures to be announced in the upcoming final report of the Pensions Investment Review. The final report will tackle fragmentation in the UK pension system, creating pension megafunds that take advantage of scale and consolidation like Australian and Canadian funds do, to invest in productive assets like private markets and big infrastructure projects.'

Asked post the announcement of the Accord whether the government would at any stage mandate pension funds to the 10% commitment, Chancellor Rachel Reeves said, ‘never say never’.

The Government’s final report on the Pensions Investment Review was published at the end of May. Its key commitment is to double the number of UK pension mega funds by 2030, and in doing so to unlock potentially billions of pounds of patient capital to help scale new businesses across the country.

Central to the Report is a decision to add momentum to the significant consolidation already underway amongst Defined Contribution (DC) pension schemes, driving towards a market characterised by bigger, better and less fragmented schemes. It is hoped the larger, more consolidated system will achieve scale benefits, with lower costs, an ability to invest in a wider range of assets, and higher returns for savers. It is hoped that larger DC pension schemes will be better able to invest in more productive assets, including infrastructure and fast-growing companies.

The key provisos of the review are:

Larger pension schemes: The key aim is to double the number of UK pension megafunds by 2030. The Pension Schemes Bill will require that providers and master trusts must have £25bn in AUM by 2030. There will be transition arrangements for smaller funds.

Broader investments with a new focus on private assets: The government thinks that greater scale will mean DC pension providers are better placed to invest in a fuller range of asset classes, including specialist private markets such as venture capital, infrastructure, property and private credit.

The review notes that there are benefits for savers of investing in these types of assets, not least to support diversification and that these sorts of investments can be a key source of funding for economically critical investments, pre-IPO companies, and infrastructure projects.

The government welcomes the Mansion House Accord investment commitment and has concluded it is not necessary currently to mandate investment.

The Pension Schemes Bill will though include a reserve power which would, if necessary, enable the government to set quantitative baseline targets for pension schemes to invest in a broader range of private assets. The government says it does not anticipate exercising the power unless it considers that the industry has not delivered the change on its own, following the Mansion House commitments.

The value for Money framework: The government observes that the consensus in the feedback to the consultation is that the DC pensions market is operating with an excessively narrow focus on cost which can be detrimental to saver outcomes. Specifically, it has the added effect of limiting investment into asset classes that might have higher upfront costs (like private investments), but which can deliver more net value in the long-term. Such asset classes are also important to driving economic growth. The government will legislate for a VFM Framework for the DC pensions market in the Pension Schemes Bill which will support decision making based on a wider set of metrics than just cost.

Reforming the Local Government Pension Scheme is a key part of the Pensions Investment Review. The scheme has a value of £400bn and 6.7m members The aim is again scale, to consolidate eight pools to six and direct the funds to a local investment focus to support “housing, key infrastructure and regeneration projects”. There is a March 2026 deadline for LGPS asset pooling.

The next phase of the Pensions Review will be launched “in the coming months”.

The new Mansion House Accord

17 of the UK’s largest DC pension funds have now pledged to invest at least 10% of their defined contribution (DC) default funds into private market assets by 2030, potentially unleashing an incremental initial c$50bn of funding for private assets with at least half earmarked for the UK

Rothschild & Co is hosting an event - Funding the UK Innovation Economy: Delivering on the Mansion House Accord on Tuesday 10 June 2025 in London.

Rothschild & Co is hosting this event to bring together senior level policy makers, pension fund allocators, regulators, UK venture and growth investors and UK based innovation businesses. We will discuss progress towards achieving the 10% target, the barriers which still exist, and the UK sectors with sustainable competitive advantage best placed to benefit from this new capital.

If you would like an invitation to the Funding the UK Innovation Economy event on June 10 please contact Tim Brenton or Patrick Wellington.

Grammarly raise

General Catalyst and the ‘unbundling of growth equity’.

A notable fund raise in May was the $1bn financing announced by San Francisco-based Grammarly which has developed a software-based tool to improve writing.

There is no implied valuation in this funding round. Instead, the backer, General Catalyst, is supplying $1bn in non-dilutive financing from its Customer Value Fund (CVF). General Catalyst will make $1bn of funding available and, instead of receiving equity, Grammarly will repay the capital plus a fixed, capped percentage of revenue it generates from the use of General Catalyst’s funds.

In a style similar to venture debt, GA CVF makes capital available that is secured by the company’s recurring revenue. GA CVF therefore looks for businesses with predictable revenue streams who need incremental capital to grow.

The advantage for the target company is that this sort of financing is non-dilutive, it does not create additional equity. It also avoids the company doing a priced round. In the case of Grammarly its last raise in 2021 at the peak of the market was at a valuation of $13bn, a level it would be unlikely to hit in current market conditions.

The rationale for this form of financing is outlined on the General Catalyst website where it calls it the ‘unbundling of growth equity’

‘Over the last decade, subscription and subscription-like business models have become pervasive. Business models have shifted to allow customers to grow into their lifetime value rather than commit to large upfront payments. In this model, the faster your business grows, the more cash it burns from S&M (Sales & Marketing):

The acquisition of each customer represents a cash ‘trough’ on day one, which is only paid back in months and years to come by the lifetime value of that customer; by the time the customer acquisition spend from the past is in the positive, a fast-growing company is spending multiples more on new customer acquisition, which means companies grow faster and faster – with consistent unit economics and positive metrics – all the while continually burning cash. As a result of this cash trough, founders have grown dependent on “growth” equity capital to fund their ambitious goals. But that growth comes at a price: dilution. Most founders own <20% of their companies by the time of their IPO; some founders own <5%.

For many companies that have found product-market fit, their primary use of capital is to fund the burn caused by S&M spend (Sales & Marketing) or CAC (Customer Acquisition Cost). This activity is largely funded using “growth” equity today, which inadvertently turns these businesses into dilution machines and provides minimal leverage on that investment.

Traditional debt and variations of it such as ARR financing, credit lines, or revenue-based financing can be a cheaper source of capital, but are not designed to fund S&M, for the simple reason that debt has to be repaid or refinanced on a fixed schedule. The payback on S&M is variable in nature, but a company’s debt repayment is typically fixed.

GC created the Customer Value strategy to solve the issue of how to fund S&M/CAC– avoiding the endless dilution and instead providing leverage on this investment. We did this by treating S&M/CAC as though it's an asset.

With this strategy, GC pre-funds a company’s S&M budget. In return, GC is entitled only to the customer value created by that spend, and GC’s entitlement is capped at a fixed amount. After GC reaches that fixed amount, the remaining lifetime value of the customers is the company’s to keep forever.

On the flipside, if the S&M spend does not pan out as expected, GC owns the downside – GC only gets paid if and when the company gets paid. The company never comes out of pocket to pay GC back.’

For those interested the link to the General Catalyst site is here: General Catalyst-The-unbundling-of-growth-equity

Markets – Europe to the fore

Much turmoil but in the end the US market is up 1% ytd with Europe’s STOXX600 up 7%.

There’s a familiar sense of chagrin for active fund managers who live the daily stresses and strains of periods of great market stress when they discover that their counterparts who have gone on holiday for a couple of months have returned to similar share prices, as if nothing had ever happened.

The chart shows the geographical performance of markets year to date to June 2. After all the tariff and geopolitical stress, global markets are up c3% year to date in local currency and c5% in dollar terms. The US has moved 1% in the first five months.

European stocks have outperformed in 2025 ytd

What is different about the chart is the inversion of the recent world order, set since the market started to recover in mid-2023. Ytd the tech lighter European markets have outperformed while the US overall has performed less well with the Magnificent Seven bringing up the rear. The other feature of the chart is the weakness of the US $ which has boosted the dollar returns of global markets ex US. President Trump’s apparent determination to have a weaker dollar is playing out.

What is more familiar is the outturn of the next chart. It shows the resumption of the ‘natural’ hierarchy of recent times, with the tech favoured indices outperforming, with the April 2 to June 2nd performance being headed by the Magnificent 7, followed by NASDAQ, then the S&P 500, with the European STOXX600 and FTSE 100 bringing up the rear.

The FTSE Venture Capital Index which measures the performance of the US venture capital industry, with a strong sector weighting towards technology, is now up 12% ytd.

Impact of tariff announcements - Performance of major indices

Source: Rothschild & Co

Source: Rothschild & Co

Private market fundraising outstrips US IPO value

The VIX volatility index, the key measure of perceived market risk which was at 21 immediately before the April 2 tariff announcements, peaked at 52 on the day before the tariff suspension on April 9, and is at 17.5 at the start of June. The IPO market typically operates best when the VIX is below 25 and, despite some postponements, a trickle of IPOs has resumed on both sides of the Atlantic.

We note thought that in the US year to date to June 4th there have been 81 IPOs raising an aggregate $11.8bn (average size $145m). In the same period there have been 178 growth equity raises of $100m or more raising $90bn (average size $505m). Even stripping out the $40bn raised for Open AI, the rest have raised $50bn at $282m.

US IPO exit value outstripped ytd by the value of Growth equity raises

Source: Rothschild & Co

Source: Rothschild & Co

The emergence of the TACO theory – that President Trump is inconstant on his tariff initiatives – has prevailed and has allowed the market to recover and for the ‘fear factor’ to retreat. There is still plenty of room for it to resuscitate with the US once again imposing tariffs on steel, finding it difficult to set a tariff accord with China and as the date of the 90-day tariff suspension deadline on July 9th is approached.

Fed interest rate cuts -lowered expectations: Prior to Liberation Day the market had been anticipating two more US interest rate cuts in 2025 in line with the official Fed dot plot. Post Liberation Day the market factored in at least three interest rate cuts in the expectation that this would be needed to stave off a faltering economy. Since then, the administration has softened the message on tariffs and a series of other factors have come into play.

In its meeting on May 6th the Fed kept interest rates unchanged at 4.25%-4.5% - it has kept rates unchanged since January. Recent informal data has been pointing to a weakening economy. The closely watched ADP data showed private hiring rising by just 37,000 in May the lowest monthly job total from the ADP count since March 2023. The Institute of Supply Management survey of the services sector fell below in May the first-time economic activity in the services sector had contracted since June 2024.

Few expect an interest rate cut at the next Fed meeting on June 6th. Thereafter there are four more meetings to the end of the year (July 30, September 17, October 29 and December 10). The market has not ruled out a July rate cut although it thinks a rate cut at the September meeting is more probable with then one more cut at either the October or December meeting to leave rates at 3.75%-4% by year end.

Meanwhile in Europe the ECB cut interest rates in mid-April by a further 25bps to 2.25% and again in early June to 2%. This was the fourth rate cut of 2025 so far and the eighth since June 2024. The April inflation number, published in early May was flat month on month at 2.2%. By contrast the May figure fell to 1.9%, below the ECB’s target 2% for the first time since September 2024. Core inflation, excluding energy and food, was 2.3% after 2.7% in April and 2.4% in March. Services inflation, typically sticky, was down to 3.2% from 3.9% in April and 3.5% in March. It was the lowest reading for this measure since March 2022. The ECB is forecasting an interest rate of 1.6% for 2026.

The market confidently expects a further two cuts by the end of the year.

In the UK the Bank of England cut interest rates in early May by 25bps to 4.25%. Figures published in mid-May showed the UK economy grew by a better than expected 0.7% in Q1, up from 0.1% in Q4 2024 with the March growth number at 0.2%. UK inflation though rose to 3.5% in April (subsequently revised to 3.4% due to a calculation error), higher than expectations of 3.3% and at its highest level for 15 months. In a contrast with the EU numbers, services inflation, typically sticky, rose sharply to 5.4% in April, versus expectations of 4.8% and the 4.7% of March. At the start of June, the governor of the Bank of England Andrew Bailey said in a Treasury Committee meeting that the trajectory of interest rate cuts is still downwards despite global uncertainties. The market expectation is, despite a three-way split in the Monetary Policy Committee, for two further interest rate cuts of 25bps by end 2025.

Market expectations for interest rates

Source: Rothschild & Co/ Bloomberg

Source: Rothschild & Co/ Bloomberg

Rothschild & Co strategist Kevin Gardiner summarises the current key drivers of the market in this graphic:

Source: Rothschild & Co

Source: Rothschild & Co

May – Growth equity raises up yoy versus tough comps

Another strong month. US now up 190% by value ytd; Europe up 17%

US $12bn of VC deal raises in May, up 5% yoy: The scale of the year-on-year advance in the value of US growth equity raises was not as substantial as in recent months. May saw 36 US venture capital raises of $100m or above, raising $12bn against the toughest comp ytd, the $11.4bn of April 2024.

This brings the ytd total to just short of $90bn, almost 3x the end May 2024 level. Even stripping out the largest single deal of 2025, March’s $40bn for OpenAI, the yoy total is still 61% ahead of the 2024 level.

Fintech leads the raises: The recent revival in Fintech raises continued with the $2.9bn raised in May making the sector the biggest raiser of funds, largely thanks to a $2.1bn raise by Acrisure led by Bain Capital and other investors. It valued the business, whose services have expanded to include insurance, reinsurance, cybersecurity, real estate, payroll, benefits, and wealth management solutions, at $32bn.

19% of May’s raises were for AI related businesses, compared to 40% in April. Ytd AI is just short of 60% of the value of all US raises.

The largest AI deal of the month was the $1bn in non-dilutive financing from the General Catalyst Customer Value Fund (CVF) for Grammarly, the English language writing assistant software tool. Anysphere, which developed the AI-powered coding tool Cursor, was the other big AI raise of the month with Thrive Capital leading a $900m round valuing the company at $9bn.

May’s other substantial raise was a $1bn Series B2 from climate tech business Commonwealth Fusion Systems. The unnamed lead investor was identified as a hyperscaler developer. It is known that Microsoft and Google both contributed to previous rounds. The company has targeted having two 400MW fusion reactors in operation by the first part of the 2030s. The ability to build a workable fusion power commercial energy source remains a major technical challenge.

The US – $12bn of US venture backed raises of $100m+ in May

Source: Rothschild & Co

Source: Rothschild & Co

$90bn of US VC /Growth raises ytd to end May, 3x the level of 2024

Source: Rothschild & Co

Source: Rothschild & Co

Europe - $3.8bn of VC deal value in May: The European venture capital market continued to make solid progress in May with a 12% yoy increase to $3.77bn in the value of deals recorded by our Deal Monitor. This was all the more creditable for being up against a May 2024 total which included the largest single deal of 2024, the $1.05bn raise for autonomous driving system business, Wayve. Showing the greater breadth of the market there were 13 $100m + deals in the month versus 8 in May 2024.

The largest deal in the month was a $330m raise for Dutch sustainable aviation fuel business, Skynrg, led by APG. Two of the deals were AI related. The Israeli natural language programming business A121 Labs raised $300m in a deal supported by both Google and Nvidia. Parloa is a German business which delivers agentic AI for customer experience – essentially AI powered customer chatbots. It raised $120m at a $1bn valuation in a deal led by Durable Capital, Altimeter Capital and General Catalyst.

Dojo is a payment provider focused on SMEs in the UK. The familiar Dojo card machines’ secret weapon is that settlement to the SME takes place next day -a key attraction for small businesses. The company raised a $190m funding round with Vitruvian Partners. The Dutch fintech Finom is also aimed at SMES. The challenger bank raised $105m in growth capital from General Catalyst.

There has been an increased focus on European defence sovereignty and self sufficiency in recent months and this has started to percolate through the venture capital market in recent raises for the likes of drone manufacturer Tekever and battlefield operating software business, KELA Technologies. May saw the biggest defence related raise of the year with the $176m round for Germany’s Quantum Systems led by Balderton Capital, Hensoldt and Airbus. Quantum Systems describes itself as an ‘aerial data intelligence company that provides multi-sensor data collection products to government agencies and commercial customers’. It is a dual use business with commercial as well as defence applications. It has government contracts in the US, the Ukraine, Germany, Spain, Australia and Colombia with its CEO Florian Siebel stating that ‘The need for sovereign, aerial intelligence has never been more pressing.’ The business had revenue of c€115m in 2024 and cites 100% yoy revenue growth.

Three biotechs had raises of more than $100m in the month continuing the strong revival in growth raises seen in this sector. Dutch Azafaros raised $145m in a deal led by Jeito Capital and Forbion Growth to address rare lysosomal storage disorders. The UK’s CellCentric raised $20m in a Series C led by RA Capital Management and Forbion for its new cancer treatment, Inobrodib. Swiss business glycoEra raised $130m in a round led by Novo Holdings for protein degraders for autoimmune diseases.

We classify Xoople as a data business. It describes itself as an Earth Intelligence business. Its purpose is to produce a stream of Earth data which, when processed using AI and combined with geospatial reasoning and enterprise intelligence, can recognise useful patterns, detect change and provide predictive insights about the planet. Its $126m raise was led by CDTI, a public entity that is part of the Spanish Ministry of Economy and Competitiveness and AXIS, a VC manager owned by Instituto de Crédito Oficial (ICO). It also received support from the Spanish Space Agency.

Three eclectic deals to round out May’s $100m raises. The Italian industrial automation group MECH-I-TRONIC produces automated assembly lines and plastic processing machinery. It raised $115m from Three Hills, Azimut Libera Impresa, and HAT. Quantum raises rarely seem to come in at under $100m Israel’s Classiq is a quantum software development platform and raised $110m from Entrée Capital, Norwest, NightDragon and Hamilton Lane.

Fancy watching an obscure European art house film with subtitles? Your ability to do so will have been enhanced via the $100m of incremental funding provided for the streaming business MUBI by Sequoia.

After five months of the year the total value of raises for European growth stage businesses is at $17.4bn, 17% ahead of 2024 at the same stage and and 69% ahead of 2023. It’s a more broadly based market by sector than the US. Notably, whereas AI businesses have accounted for 59% of all raises to date in the US (or 25% excluding the $40bn OpenAI deal), the figure for Europe is just 10% of the value of all raises ytd.

The top five sectors in Europe have accounted for 64% of the funds raised ytd with software leading with 16%, followed by Fintech at 14%, Biotech at 13% and Climate Tech at 11% with AI in fifth place.

Ytd software remains the biggest sector both by volume and value with 52 raises for a total of $2.8bn led by $260m for the medical technology business AMBOSS, $200m for the travel software platform TravelPerk and $175m for the decision intelligence business, Quantexa.

Fintech has sustained the revival seen initially 2024 and is in second place by both volume and value with 36 rounds raising $2.4bn, the biggest being the $500m raised for Israeli international payments platform, Rapyd followed by the $190m raised for card payments business Dojo.

Biotech has seen 29 deals raising a total of $2.25bn. Verdiva Bio announced a $411m, co-led by Forbion and General Atlantic in one of Europe’s largest ever Series A rounds.

Climate Tech deals are at $1.9bn after five months with the biggest raises being $420m for green flexibility, a German developer of large-scale battery storage systems led by Partners Group. May saw a$330m raise for sustainable aviation fuel business, Skynrg.

The $1.8bn of AI deals are led by $600m for Isomorphic Labs which uses artificial intelligence for drug discovery, the $300m for natural language programming business A121 Labs, and $180m for AI video communications platform Synthesia.

Europe - $17.4bn raised to end May 2025 – 17% ahead of 2024, 69% ahead of 2023

Source: Rothschild & Co

Source: Rothschild & Co

Europe - $3.8bn of raises in May 2025

Source: Rothschild & Co

Source: Rothschild & Co

Fundraising outlook: Investors continue to look for any signs that the tariff turmoil or even some of the provisions of the ‘big, beautiful bill’ like the section 899 surtaxes on corporates in certain jurisdictions deemed to have unfair tax policies, has had any effect on the flow of deals in growth equity.

As we have said before the immediate recent experience is likely a poor forward indicator due to the length of time it takes to put venture and growth equity raises together. Announced deals better reflect conditions prevailing three to four months prior.

Nevertheless, we observe that April and May raises have remained healthy on both sides of the Atlantic and the roster of raises reportedly in preparation - drawn from press reports - appears robust as well. Despite a number of deals having come through in the last month (Neuralink for instance raised $650m rather than the $500m rumoured) our monitor of impending raises continues to hover at around the $30bn mark. Recent additions and amendments are:

Elon Musk’s xAI is reported to be raising $20bn at a valuation of $120bn. Prior to this though the AI LLM business is said to be looking to carry out a $300m secondary at a $113bn valuation. The last valuation mark (albeit an obscure one) for xAI was the $80bn it was valued at in the takeover of X (for $33bn) in March this year.

Also in AI, Cohere a Canadian LLM business focused on enterprises, is looking to raise $500m at a valuation of $6.5bn. Its ARR is at c$100m.

Israeli cybersecurity business Cyera is said to be raising c$500m at a valuation of c$6bn. It last raised with a Series D of $300m at a $3bn valuation in November 2024.

Canadian clinic management software platform Jane Software is conducting a c$500m secondary round led by private equity firm TCV which will value the company at c$1.8bn.

Electric delivery van start up Indigo Technologies is looking to raise a c$300m Series C.

Growth Equity – c$30bn in reported upcoming raises

Source: Rothschild & Co; press reports

Source: Rothschild & Co; press reports

Our views on the state of the venture capital markets

The combination of global inflation, rising interest rates, and increased geopolitical risk substantially impacted the venture capital market in 2022 and 2023. 2024 saw some adaptation to the ‘new normal’. The refocusing of venture backed companies to achieve a better balance of growth, profitability and cash flow and the delivery of interest rate cuts has led to increased optimism and enthusiasm for growth equity in 2025. Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment led to a sharp impact on valuations in private markets. The scale of the fall in the FTSE Venture Capital Index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023 and slow recovery in 2024.

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, semiconductors) supporting the development of AI.

- Outside the AI space the VC market is regaining confidence with a revival of interest in fintech, biotech and software being notable. Certain investors remain very active in the space with substantial funds to deploy. There remains substantial dry powder in the VC industry

- The speed of the investment process has slowed since 2021-22. The level of diligence on new deals has stepped up.

- 2023 and 2024 saw more downrounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these.

- Recent initiatives by the US to impose tariffs on its trading partners is likely to impact US and global economic growth and to negatively affect the fund-raising environment for venture backed companies.

- It seems likely that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses.

- Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and on DCF and comparative based multiples.

Read the previous editions:

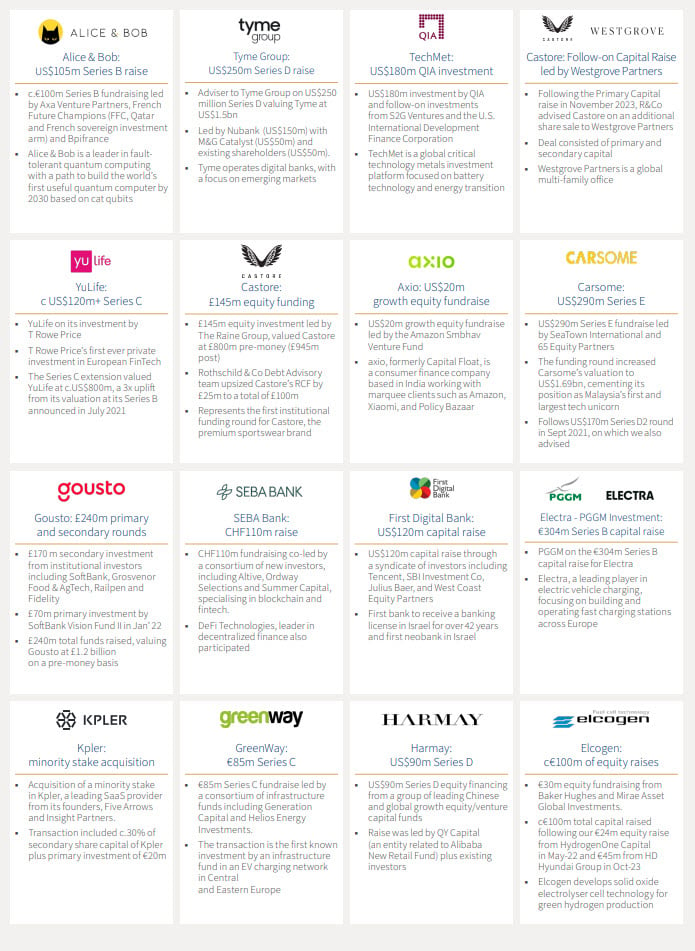

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Chris Hawley

Global Head of Private Capital

chris.hawley@rothschildandco.com

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Advisory

patrick.wellington@rothschildandco.com

+44 20 7280 5088

+44 7542 477 291

Thomas Chung

Head of Private Capital, North America

thomas.chung@rothschildandco.com

+1 212 403 5559

+1 917 594 7208

Mark Connelly

Head of North American Equity Markets Solutions

mark.connelly@rothschildandco.com

+1 212 403 5500

+1 917 297 5131

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.