Growth Equity Update

January 2026 – Edition 46

• Buoyant growth equity markets: 2025 was a stellar year for growth equity markets.

• US fuelled by AI raises: The value of US growth equity market raises in 2025 rose by 2.1x yoy to $234bn (2024 $109.7bn). US AI raises grew 3.3x in value and accounted for 57% of the $234bn raised.

• In Europe, where the AI effect is less marked, the overall value of 2025 raises grew by 44% yoy to $49.2bn. AI was the second largest sector by funds raised with $5.3bn (2024 $2.8bn), 11% of the total. In Europe software, with 113 rounds raising $7.5bn, rose to be the largest sector by value, overtaking Climate Tech.

• Will it continue? Despite market fears over the capex requirements of the big LLM companies, the largest of these continue to raise going into 2026. xAI has just closed a $20bn round while OpenAI is reported to be negotiating a further $100bn round and Anthropic one for $10bn. Between the US and Europe we see c$158bn of raises already in gestation at the start of 2026, over half the 2025 total.

• AI infusing the VC market: Investors are embracing the impact of AI with increased investment in sectors serving AI (datacentres, semiconductors, quantum) and transformed by it (autonomous vehicles, defence, legal tech, robotics).

• Peering into 2026. We review the predictions we made for 2025 and make some more for 2026. Despite the very tough comp, we think the value of growth equity raises will rise again in 2026. We anticipate strong growth in funding for defence, crypto/blockchain and long gestation businesses like nuclear, fusion energy and quantum computing. We think realisations will improve with the M&A and IPO markets picking up.

• Public markets in 2026: The average end 2026 level of the S&P 500 forecast by 18 Wall Street firms is 7,572, a rise of just over 10%. The debate is whether rapid earnings growth and falling Fed rates can offset high valuations and AI bubble fears.

• ‘I’m going to make a prediction - it could go either way’ – Ron Atkinson

The Growth Equity Market in 2025

The US growth equity market grew 2.1x by value in 2025 to $234bn (2024 $109.7bn). The growth was fuelled by AI raises which grew 3.3x yoy and accounted for 57% of total proceeds. Europe, where the AI effect was less marked and the leading sector was software, saw the value of raises grow by 44% in 2025 to $49.2bn.

The US

Our Rothschild & Co Deals Monitor tracks US VC deals valued at $100m or more. We recorded 487 US growth equity deals of $100m or more in 2025 raising a total of $234.1bn. This compared with 309 such deals raising $109.7bn in 2024, growth of $124bn yoy in value or 113%. The summary tables for both years show the raises split by sector with the top three raises by value in each one.

A few features:

Concentration: The top ten deals in 2025 cumulatively raised $106.5bn, 45% of the annual total. The equivalent 2024 figures were $47.6bn and 43%.

AI dominates: There were 84 AI deals in 2025 raising $132.6bn, 57% of the annual total. Three deals provided just over half of this total, the $40bn Open AI raise announced in March, the $15bn raise for Anthropic in November and the $14.3bn raise for Scale AI backed by Meta in June. The dominance of AI was more marked than in 2024 when big AI raises were really just a Q4 phenomenon. In 2024 AI raises totalled $40.8bn, 37% of the annual total with the largest raise being $10bn for Databricks.

AI infusing the growth equity market: There are a number of other sectors which are proxies for AI. These are sectors where the companies are either serving AI (datacentres, quantum, semiconductors) or are applications of AI (autonomous vehicles, robotics, legal tech).

Here we see how AI is broadening its effect across VC as investors look to take advantage of the AI phenomenon more widely through associated industries. Cumulatively those six sectors raised another $13.8bn in 2025 or 6% of the total, taking the total AI percentage of the annual raise to 63%.

Thirty raises of $1bn +: There were 30 raises of $1bn or more in 2025. Of these 17 were for AI businesses including all the top eight raises. Two were for datacentre businesses powering AI and one (Cerebras Technologies) for an AI semiconductor business. The biggest non AI raises were for metaverse business Infinite Reality ($3bn from a mysterious private investor in January); $2.5bn for defence business Anduril, $2.1bn for the insurance brokerage, Acrisure; $2bn for Polymarket and $1bn for Kalshi in the blockchain driven prediction markets; $1bn for the Sam Altman-backed age defying Retro Biosciences; $1bn for Elon Musk’s X; $1bn for PsiQuantum; $1bn for the humanoid robotics business FigureAI and $1bn for grid batteries business, Base Power.

In 2024 there were 14 $1bn+ raises, eight of which were for AI businesses plus one large raise ($9.2bn) for datacentre business, Vantage Data Centres.

Software prominent: 2025 saw 72 raises for software business totalling $14bn (2024 40 raising $8.5bn). Software businesses tend to be asset light, cash generative and frequently profitable, meaning that the amounts they raise are typically smaller than those in AI. The average size of raise was $194m. The three biggest deals were $700m for Savyint, a security, compliance, identity governance and access management solution; $500m for Metropolis (a $1.6bn total raise including a $500m equity element) for its AI powered frictionless parking payment platform and $500m for Nerdio, a business that simplifies the deployment and management of Microsoft cloud technologies.

Biotech and FinTech revivals continue: AI powered drug discovery is a major theme in Biotech. It swapped second position in sector raises in 2024 (77 raises for $12.6bn) for third position in 2025 (69 raises for $12.5bn). The biggest raises were for $1bn for Retro Biosciences which, Sam Altman backed, is looking to develop drugs to extend the human lifespan by ten years; Kailera Therapeutics, which has a programme of obesity drugs, raised $600m and Maplight Therapeutics raised $373m in a Series D for its therapies for central nervous system disorders.

Fintech was the fourth largest category in 2025 with $10.3bn raised across 36 deals (2024 seventh position, $4.3bn raised, 25 deals). The key deal was the $2.1bn raise for Acrisure a financial services platform combining AI across its services in insurance, reinsurance, cybersecurity, real estate, payroll, benefits, and wealth management. The alternative investment platform iCapital raised $820m in July. In April the open banking business Plaid raised $575m in a round valuing the business at $6bn, down from $13.4bn in 2021.

The biggest movers: Three sectors – Defense, Crypto/Blockchain; Quantum

These three sectors saw the biggest relative upwards movement between 2024 and 2025:

Defense – Moving to offense: The sixth largest sector for VC raises in 2025 was Defense, up from tenth slot in 2024. Defense companies raised $7.2bn in 20 $100m+ deals (2024 three deals raised $1.8bn). The outlook for the defence sector changed in mid-February 2025 when US vice president JD Vance announced that, as far as the US was concerned, Europe must take responsibility for its own security, sparking a scramble by European countries to raise their GDP spending on defence and step up their direct support for Ukraine. Simultaneously the US has been redirecting its defence spending into new avenues to reflect the changing nature of warfare, demonstrated by the evolving nature of the conflict in the Ukraine.

The three leading raises in Defense in 2025 were from the same companies and in the same order as the three leading companies in 2024. The biggest in 2025 was the $2.5bn for Anduril Industries (2024 $1.5bn) led by Peter Thiel’s Founders Fund. Anduril offers a range of autonomous defence systems powered by Lattice, an AI-based operating system that connects autonomous sensemaking and command & control capabilities with modular and scalable hardware components. Products include the Barracuda family of military drones, the Roadrunner reusable vertical take-off and landing (VTOL) Autonomous Air Vehicle (AAV) and the Dive-LD autonomous underwater vehicle.

Saronic raised $600m in 2025 ($175m in 2024). It describes its mission as ‘redefining maritime superiority for the United States and its allies.’ Saronic develops autonomous surface vessels and will use the 2025 funds to build a new shipyard, Port Alpha, allowing it to expand its medium and large-class autonomous vessels - effectively water-borne drones.

CHAOS Industries raised $510m (2024 $145m). It is building Coherent Distributed Networks (CDN™) systems that give ‘warfighters’ time to act against borders and autonomous threats, essentially sensor technology for the military sector including the Vanquish radar to detect missiles, drones and aircraft and the Astria radar to monitor the environment for long periods.

Blockchain/Crypto: Crypto went out of style following the collapse of FTX in November 2022 and was the 28th ranked sector for US raises in 2024 with just two deals of $100m plus raising a total of $325m. The crypto friendly US administration helped spark a revival of interest in 2025. There were 12 deals raising $3bn pushing the sector into eleventh place. Indeed, if combined with the three raises in the blockchain based Prediction Markets businesses (Polymarket and Kalshi raised $3.3bn between them) the sector could be said to have raised $6.3bn, pushing it up to seventh place, just behind defense.

Leading the raises was the $800m round led by Jane Street for the crypto exchange Kraken, a globally scaled and regulated infrastructure stack that spans spot trading, derivatives, equities, tokenized assets, staking and payments. A subsequent $200m strategic investment by Citadel Securities was executed at a $20bn valuation. In October the Stripe and Paradigm backed payments-focused Layer 1 blockchain business Tempo raised $500m in a Series A led by Greenoaks and Thrive Capital. The crypto payments business Ripple raised $500m at a valuation of $40bn in November. The business has expanded from payments into custody, stablecoins, prime brokerage and corporate treasury.

Quantum: AI enables machines to learn, make decisions, and recognize patterns. Quantum computing aims to process information in distinct ways that classical computers cannot, making problem-solving faster and more accurate. Quantum can potentially speed up the training of AI models, optimise their functionality, perform better processing of large datasets, tackle complex problems in areas like drug discovery and materials science and improve natural language processing.

As interest in AI has grown, so has the engagement with quantum. There were five deals in quantum in 2025 raising $2.13bn, up from just one deal at $300m in 2024. PsiQuantum’s $1bn Series E in September led by BlackRock was one of the largest financings ever in quantum computing and valued the company at $7bn. Professor Jeremy O’Brien, PsiQuantum co-founder and CEO commented

‘Only building the real thing—million-qubit-scale, fault-tolerant machines—will unlock the promise of quantum computing.”

US Growth Equity raises in 2025 – 487 deals of $100m+ raising $234bn

Growth Equity raises in the US in 2024– 309 deals of $100m+ raising $110bn

Looking at the biggest raises overall the list was headed by Open AI with a total of $41bn raised from two deals. Anthropic raised a total of $32.5bn across three deals meaning these two companies alone accounted for 31% of US VC fundraising in 2025.

US – 2025 saw 30 raises of $1bn+

The European Venture Market in 2025

Our Rothschild & Co Deals Monitor tracks European VC deals of $20m or more. We noted 633 European deals of $20m or more in 2025 raising a total of $49.2bn. This compared with 487 such deals raising $34.2bn in 2024, a value increase of 44% yoy. The exhibit shows the year broken down by sector with the largest raises.

European Growth Equity raises in 2025 – 633 deals of $20m+ raising $49.2bn

A few features:

Smaller: The $49bn raised is just 21% of the total $234bn raised in the US. The yoy uplift was also more modest at 44% versus the 113% in the US.

Less concentrated: The leading US sector, AI, accounted for 57% of all raises in the US in 2025. In Europe the top six sectors combined reach the 57% figure.

AI is prominent, not dominant: AI was the second largest sector by funds raised in 2025 with $5.3bn (2024 $2.8bn) raised across 35 (2024 17) deals, equivalent to 11% of funds raised in the year. It supplied the biggest raise of the year, the $2bn Series C for French LLM, Mistral but only one more in the top 10, the $600m raise for AI drug design business, Isomorphic Labs.

Broader AI impacts: Looking at the proxy sectors for AI (datacentres, quantum, semiconductors, autonomous vehicles, robotics, legal tech) the influence of AI becomes more marked with these sectors adding another $6.1bn or 12% to the annual total.

Software leads the way: The Software sector rose to be the largest sector by value of raises in 2025 overtaking Climate Tech. There were 113 rounds raising $7.5bn (2024 100 deals raising $5.6bn), growth in value of 25% yoy.

The three biggest deals all came late in the year led by October’s $710m ($270m primary, $440m secondary) round for Bending Spoons at an $11bn valuation. Bending Spoons is a serial acquiror of digital businesses owning Brightcove, Evernote, komoot, Meetup, Remini, StreamYard, and WeTransfer, and with the October round helping to fund the acquisitions of Vimeo and AOL. The French CRM (customer relationship management) company Brevo raised $575m in December. Lovable, the Swedish vibe coding business raised $20m in its July Series A at a $1.8bn valuation and followed this up with a $330m raise at a $6.6bn valuation in December. The business was founded in July 2023, reported $1m in annual recurring revenue (ARR) in November 2024 and $200m of ARR in November 2025.

Climate Tech slipped into fourth place by sector value in 2025 with 68 raises bringing in $4.9bn (2024 $6.5bn across 83 raises). We have noticed since the demise of Northvolt that the ambitious funding programmes for long term projects in this field have died away. In 2023 European Climate Tech had two deals of over $1bn (H2 Green Steel, Northvolt) and another three of more than $500m (Verkor, Zenobe and Northvolt again). In 2024 there were just two deals of more than $500m (Sunfire $550m, RP Global $528m). In 2025 there were none with the largest deal in the sector being the $420m for green flexibility in Germany in January.

Biotech was again well represented: There were 66 deals in 2025 raising a fraction under $5bn with the largest being the $410m Series A by Verdiva Bio which is focused on developing a weekly (as opposed to daily) dosed oral GLP-1 focused obesity treatment. Next in line was the $358m raise by German cancer treatment biotech, Tubulis. The sector saw good growth with the value of deals rising by 29% versus the $3.87bn of 2024.

It was a strong year for healthcare as well with the value of raises rising by $1.65bn (+87%) yoy boosted by the $900m raise for smart rings business Oura in October valuing the business at $11bn. Oura had previously raised $200m at a $5.2bn valuation in December 2024. There was also a substantial $260m raise for Daniel Ek backed healthcare scanning centre business Neko Health as it built out its network of scanning centres.

Fintech and the return of crypto: Fintech has been staging a solid recovery since H2 2024. It is represented in the top 10 European raises of the year by the $500m round from the Israeli global payments’ platform Rapyd in March to fund its acquisition of Dutch fintech PayU from Prosus. In total 2025 saw 58 raises by Fintechs for a total of $4bn (2024 55 deals for $3.6bn).

As in the US, there has been a marked revival in blockchain/crypto deals, with 12 European deals in 2025 raising $659m led by the $136m Series C from Fnality, which is a global settlement network employing distributed ledger technology to connect wholesale markets with tokenised and decentralized markets. In 2024 there were just five deals raising a total of $195m.

The biggest movers: Four sectors – Cybersecurity, Datacentres, Defence, Quantum

Cybersecurity moved up from 15th to 7th in the sector rankings between 2024 and 2025 with the value of raises up 5.4x from $469m to $2.57bn. Of the 36 raises in the sector, 24 were from businesses based in Israel which has become the European centre of excellence for this industry. These included the three biggest raises, the $400m for the AI and data security business Cyera at a valuation of $9bn; the $359m Series G raise by Cato Networks and the $120m raise for Vega.

Datacentres are key to AI development. Datacentres are the real estate of AI in terms of availability of GPUs and land and energy access to drive them. European businesses raised $2.1bn in 2025 up from just $155m in 2024, jumping to eighth position in terms of sector value. Over three quarters of the total came from just two deals, reflecting the scale of the capex in this sector.

The UK’s Nscale described its $1.1bn October raise as the largest Series B in European history. The hyperscaler will use the proceeds to further its deployment of large-scale AI infrastructure across Europe, North America and the Middle East, enabling the rapid rollout of the company’s “AI factory” data centres for projects like Stargate UK and Stargate Norway, and the expansion of its vertically integrated AI cloud platform. The Norwegian energy and industrial group Aker led the round with $285m of funding and payment in kind. The latter consisted of a portion of its Narvik land portfolio in northern Norway. In exchange Aker will receive a 9.3% stake in Nscale whose implied valuation was c$3bn. Swedish datacentre business EcoDataCenter raised $521m in equity in March and followed this with $700m in debt financing in September. The business has teamed with Coreweave to build one of Europe's largest AI clusters in Falun, Sweden.

Quantum Computing – the next leg of AI: There has been a flurry of raises on both sides of the Atlantic for quantum computing businesses reflecting the view that quantum computing is the next key stage in the development of AI. Europe, traditionally the poor relation to the US in quantum computing funding, saw 14 deals in 2025 with five at over $100m (IQM Quantum - $320m, Multiverse Computing $215m, Quantum Machines $170m, Classiq $110m and Alice & Bob $105m). Quantum leaped from 20th to 10th in the sector rankings with a $1.2bn or 6.7x increase in yoy funding to $1.38bn.

Defence scaling up: As in the US, interest in VC funding of emerging defence business quickened as the year went on. The experience of the Ukraine war has shifted the focus of incremental defence spending from traditional military platforms (tanks, warships, planes) to new technologies like AI, robotics, autonomous solutions, quantum computing and cybersecurity.

Our Deal Monitor records twelve defence deals, led by the $690m Helsing Series D in June valuing the business at $13.8bn. Helsing designs AI applications focusing on all-domain defence spanning air, land, sea, space, and cyber using AI software to process information from defence systems and improve battlefield decisions. It also had the largest defence raise in 2024, its $487m Series C valuing the business at $5.4bn.

May 2025 saw a $176m round for the German Quantum Systems, an ‘aerial data intelligence company that provides multi-sensor data collection products to government agencies and commercial customers.' It is a dual use business with commercial as well as defence applications with government contracts in the US, the Ukraine, Germany, Spain, Australia, and Colombia. This was followed by an additional $180m round led by Balderton Capital in November, lifting the company’s valuation above €3bn. At the end of the year the Finnish satellite developer Iceye which has adapted its satellite monitoring fleet for defence use, raised $233m at a $2.8bn valuation.

The ‘missing’ sector- Online grocery: Online grocery businesses raised $1.1bn in 2024 with Getir, Rohik, Flink and Picnic all making $100m plus raises. Europe has fallen out of love with the instant grocery delivery model meaning in 2025 there was just one raise in this space, albeit a substantial one, the $495m raise by Dutch business Picnic. In an associated sector there was a clutch of ride hailing and e-mobility raises from the likes of FINN, Voi and Blacklane in 2024. There were none in 2025.

Europe’s biggest growth equity raises in 2025.

Fundraising outlook: c$158bn of potential raises

A substantial pipeline of impending raises going into 2026

Our Deal Monitor shows a substantial group of impending raises. We identify c$147bn of impending US deals and $11bn in Europe.

The key addition to the US list is the reported intended $100bn raise at OpenAI at an $830bn valuation reported in the WSJ. The intention is to close the round by the end of Q1 with sovereign wealth funds targeted as potential investors.

Autonomous vehicle company Waymo is said to be looking to raise $15bn at a valuation of $110bn with Alphabet as a key supporter. Its previous funding round was $5.6bn at a $45bn valuation in October 2024.

Anthropic, which raised a total of $32.5bn across three deals in 2025 is reportedly planning a further $10bn raise at a valuation of $375bn. GIC and Coatue Management are said to be leading the raise.

High on the US list and emphasising the return of crypto, is Tether, the stablecoin issuer, widely reported to be looking to raise between $15-$20bn for a c3% stake. Robotics business Skild is looking to raise $1bn from a combination of Softbank and NVIDIA. AI cloud computing business Fluidstack is looking to raise $700m at a $7bn valuation in a deal led by Google.

xAI which announced its $20bn raise at the start of January, moves off the US list.

In Europe the list is headed by the expected $2bn raise for autonomous vehicles business Wayve, led by Nvidia, Microsoft and Softbank, and $2bn for the French AI coding business Poolside led by Magnetar and Nvidia. Italian AI infrastructure business, Domyn is said to be raising $1.15bn.

Additions to the list this month include a possible $2bn raise for UK datacentres business Nscale. It last raised $1.1bn in its Series B as recently as October 2025.

Yann LeCun was the key architect of Meta’s AI strategy. He has left the company to form Advanced Machine Intelligence (AMI) Labs. This AI business will develop so-called ‘world models’, sophisticated, forward thinking AI systems capable of planning complex actions. The new business, a ‘talent raise’ will be based in Paris and is looking at an initial $585m raise at a $3.5bn valuation.

US Growth Equity – c$147bn in reported upcoming raises

European Growth Equity – c$10.6bn in reported upcoming raises

Our predictions for growth equity in 2025 – how did we do?

In the January 2025 edition of the R&Co Growth Equity Update we made ten predictions for the coming year. We review here how we did. Marking our own homework, gives a score of 7.5 out of 10….

We made ten predictions. We show each in italics and our assessment of the current state of play and of our prediction beneath each one.

1. Artificial Intelligence to dominate and widen: A two-tier market has emerged in venture capital. It’s AI, and then everything else. AI captured around a third of all new VC funding in 2024. The pace quickened with Q4 being the largest quarter by some distance for funding of big AI deals. These deals, and the rapid valuation uplifts between rounds, have only stoked the appetite of investors for exposure to the potential industry transformations that the application of AI offers. We expect that the net will widen in 2025 and that a broader range of investors will seek to gain exposure to AI amongst application specific businesses.

Not bad as a prediction and less obvious than it seemed at the time. It was only in Q4 2024 that the start of the surge in growth funding for AI businesses began. In 2024 our revised numbers show that 37% of US venture funding was for AI businesses, a total of $40.8bn. In 2025 the percentage rose to 57% and the total to $133.3bn

2. Datacentres: ‘Data is the new oil’: Or should that be datacentres? It seems that, despite a slew of large fund raises for data centre operators in 2024 (Vantage Data Centres $9.2bn; Coreweave $1.1bn; Crusoe Energy $500m, Lightmatter $400m) there appears plenty of potential for more. Analysts at Mogan Stanley anticipate there will be 70% pa growth in GenAI related power demand 2024-27 growing from <15 terawatt hours (TWh) in 2023 to 224 TWh in 2027.

Here we were looking in the right ballpark, but the theme expressed itself largely away from the growth equity market. Indeed, one of the Stock Market’s biggest themes in 2025 was the burgeoning AI capex requirement faced by the hitherto capital light tech companies. The amount of capital deployed in data centre development via growth equity raises shrank in 2025 versus 2024. The 2024 total of $10.8bn was boosted by the $9.2bn raise for Vantage Data Centres late in the year. The equivalent figure in 2025 was $5.2bn with Crusoe Energy leading the way with a $1.4bn raise.

3. A revival in Fintech: 2024 was another tough year with a 20% yoy drop in global Fintech funding estimated by Innovate Capital. A report from Silicon Valley Bank in late October observed that fundraising by Fintech oriented VC firms has dropped by over 90% since its peak in 2021. We think though that 2025 is set to see a revival in VC funding for FinTech.

The revival of fintech did occur in 2025 with the 25 rounds raising $4.3bn in the US in 2024 expanding to 36 raises reaching $10.3bn in 2025, a 2.4x increase. There was substantial activity also in the secondary market for fintech, including big secondaries from Stripe and Revolut as well as some high profile fintech IPOs.

4. ClimateTech - less hot: An unusual feature of the European VC market in the last couple of years was that, even as investors became more cautious about pre-revenue/profit/cash flow businesses in the wake of the change to the interest rate environment, there was still a surprising amount of support for ClimateTech companies which were pre-revenue and certainly pre-profit and which required heavy capital investment to build projects like battery gigafactories or networks of EV charging station stations. As the world gets warmer some of the urgency in pursuing such climate led opportunities appears to have dissipated, the outlook for electric vehicle sales has waned (fewer incentives, lower prices for used EVs, rapid charging infrastructure issues) and the incoming Trump administration (‘Drill, baby, drill’) appears less likely to promote climate initiatives. The Chapter 11 filing by Northvolt, which had received $14-15bn of venture funding, is also a jolt to the system. We think a scaling back of ambition in ClimateTech raises may be a feature of 2025.

A decent prediction. In Europe raises in Climate Tech declined in value from c$6.5bn in 2024 to $4.9bn in 2025. The very substantial raises that typified 2021-23 remained absent but there was a steady stream of $100m plus deals – 16 in total in 2025- led by the $420m raised for green flexibility, the $330m for Skynrg and $172m for Aira.

In the US Climate Tech had a stronger year with the amount raised up from $5.2bn in 2024 to $9.8bn in 2025. The bigger deals though are AI and datacentre related raises in the guise of Climate Tech. Thus, two of the three biggest deals classed as Climate Tech were for fusion and nuclear energy developers, with these technologies seen as key to providing power sources for new AI datacentre demand.

Fusion energy as a solution to the world’s energy needs is a technology under intense development and Commonwealth Fusion System’s $863m raise was the largest of its kind this year. Ally Yost its Senior Vice President of Corporate Development referenced how the interest in powering AI datacentres has quickened investor interest in new energy tech like fusion power.

‘CFS offers investors the clearest path to bringing commercial fusion to the world — and an unprecedented opportunity to make a real impact as global demand for power accelerates with electrification and increased use of AI and data centres.’

Similarly, the third largest raise in Climate Tech was the $700m round for small modular nuclear reactor business X Energy. Amazon supported this raise. Its Vice President of Global Data Centres Kevin Miller was the one to explain the investment.

“This collaboration between Amazon and X-energy is a significant step toward accelerating advanced nuclear technologies that can help us bring new sources of carbon-free energy to the grid cost-effectively and safely.”

5. Venture capital activity to grow again in 2025: After two years of decline from the heady peaks of 2021 global VC activity grew in 2024 over 2023. Pitchbook estimates that global funding for VC firms increased, albeit by just 5%, from $349bn in 2023 to $368bn in 2024. We think that VC deal value will rise again in 2025 for four reasons (i) there is intense interest in artificial intelligence and associated technologies, and we think these areas will continue to attract substantial funding in 2025 (ii) the public markets have had two years of 20%+ returns. This is positive for investor mood - critical for VC investing (iii) The quality of companies is better. After three years of adapting operating practices to accommodate growth with profits /cashflow rather than all out growth, the universe of VC companies is more investable while valuation expectations are tempered – a better environment for VC investing (iv) if –as we expect – the IPO market improves in 2025- the liquidity of the whole private capital system will improve in turn.

We got this one right, and it was a tougher prediction than it looked with the AI surge in the last three months of 2024 only just taking the 2024 total past 2023. We underestimated the extent to which 2025 would exceed 2024. At $234bn vs $109.7bn the US growth equity market grew 2.1x in 2025. In Europe, where the AI effect was less marked, growth was 44% to $49.2bn.

Europe – Value of growth equity raises up 44% in 2025

US – Value of growth equity raises up 2.1x in 2025

6. Fund raising for VC firms to remain tough - concentration in the biggest firms: The corollary of an improved VC market may well be that fund raising for VC firms improves as well. The industry has struggled since its peak of $404bn of global fundraising in 2021, with inflows of funds dropping to $214bn in 2023 and $170bn in 2024.

We were only partly right on this one. Pitchbook has revised its figures for global VC fundraising and now charts the peak year as $414bn in 2022 with $271bn in 2023 and $219bn in 2024. Far from improving in 2025 both fund count and the amount raised continued to slide sharply in 2025. The new fund count declined from 2,122 to 1,148 and fundraising from $219bn to $118.4bn, down 46%.

US fundraising, which had held steady yoy at just over $100bn in 2024, dropped to $67.6bn in 2025 (-35%). European fundraising dropped 47% to $13.4bn. Asia Pacific saw the most dramatic fall, down almost 60% at $33.2bn.

The concentration effect into larger, more established funds continues. In the US the ten largest venture funds amassed 43% of the total fundraising. This is the corollary of the AI fundraising effect. Investors are keen to get exposure to the prime private AI assets and see the largest funds as the best way to get that access. Quoted in ‘The Newcomer’ Samir Kaji, CEO of Allocate observed

“Now, the focus from LPs has been getting into these ‘white truffle’ assets… That has now increased the attention toward these mega funds, who have access to these ‘consensus’ hyper-scale AI companies.”

Global VC fundraising activity – sharp decline in 2025

7. Outside AI and related, funding rounds slower, more down rounds: The AI experience is giving a false impression of the general state of VC markets. While we have seen investors crowding into AI deals with speed and with companies and founders in the ascendant in terms of valuation, the environment is very different elsewhere.

More typically the process of fund raising is much more measured than in the 2020-22 period… In turn this shift of emphasis contributes to the number of down valuations rounds in the system. Pitchbook numbers at H1 2024 suggested down rounds in the US valuations of the total, twice the 7.6% of 2021.

Mixed report here. The AI boom led to a broader pick up in VC market conditions. If we exclude AI specific deals the US non-AI VC market grew by 47% in value in 2025 versus the total market (including AI) up 113%. In Europe overall VC fundraising was up 44% with non-AI fundraising up 33% yoy. Valuations also were on an upwards trend against a background in which the public markets were up c20%.

At the same time the number of downloads remained high. PitchBook data shows that after seven months of the year around 16% of 2025’s US venture-backed deals in 2025 were down rounds, marking a decade high. Additionally, almost every major IPO listing in Q2 came in below its peak valuation.

8. Company casualties still climbing: The venture capital model assumes a relatively high failure rate of companies along the way, with the effect hopefully more than offset by some good, and some spectacular, successes. The shift in the interest rate environment and the ensuing change in the ease of accessing capital is though a pivot moment and it is likely that the number of venture capital backed projects that shut down will climb in 2025.

Looks about right, though the data is slow to come in on this. S&P Global Market Intelligence data indicates that bankruptcy filings made by US companies backed by PE and VC rose 15% to 110 in 2024, the highest annual total on record. According to the same source 52 bankruptcies were recorded in H1 2025, unchanged from the same period in 2024. Overall US bankruptcies, including nonportfolio companies, reached 371 in the first six months of 2025, up 10.7% yoy.

US PE/VC portfolio company and total bankruptcy filings, 2010 – 2025 *

9. IPO environment – improvement in 2024, better again in 2025. Two successive years of c20% gains by the S&P 500 should have created an environment where investors are feeling more confident, a useful backdrop for a potential IPO market revival. Global IPO value of $123bn was just modestly ahead of the $122.2bn in 2023. There was though a sharp revival from a low base in the US and Europe. By late December, US IPOs had raised $41bn versus 2023’s $24bn and the $22 bn of 2022. All in all, it appears likely that the IPO market, especially in the US, should pick up again in 2025 with flow down benefits into the growth equity markets as liquidity in the system is released.

The IPO revival did occur. EY figures report that overall, 1,293 IPOs raised US$171.8bn globally, a 39% increase in proceeds across a static number of deals compared with 2024. The US IPO market saw deal count and proceeds increasing by 27% and 38% respectively compared with 2024. Across Europe, IPO activity declined with deal count down 20% to 105 IPOs vs 131 in 2024 and proceeds down 10% from 2024 to US$17.3bn.

Quarterly global IPO activity (2021 – 2025)

10. M&A picking up as well: M&A has also begun to see an upswing with successive Fed cuts to interest rates, lower inflation and still substantial levels of dry powder giving the market a more stable feel. The strength of public markets has helped in the process of closing valuation gaps. Pressure on PE funds to return capital to investors may spur activity further in 2025. The intense interest in AI is likely to boost activity.

This was accurate. In 2025, global M&A volumes reached $4.3 trillion, a 39% increase from the prior year, driven largely by megadeals in tech, healthcare, and financial services.

North America deal value rose from $1,572bn in 2024 to $2,074bn in 2025 (+32%). Appetite for AI deals was a key driver.

North America M&A deal value +32% yoy in 2025

In Europe M&A deal value was flat in the first half of 2025 but accelerated in H2 to be up 15% yoy at $746bn. Technology was the leading sector by deal count, as buyers targeted digital capabilities and assets to support AI transformation. Energy transition and infrastructure transactions were also prominent.

Europe – M&A deal value +15% yoy in 2025

We also discussed,

How will the end of 2025 look? US interest rates may be only 30bps lower than the levels of the start of the year as inflation remains stubbornly high. There may be some shocks to global trade caused by the imposition of tariffs by the US and retaliatory activity elsewhere. Global GDP growth remains relatively weak (US GDP growth is forecast by the OECD at 2.4% in 2025, down from 2.8% in 2024 with a further slowdown to 2.1% for 2026). Public investors may have made some good money on reasonably priced IPOs. Venture Capital companies will be three years into the focus on profits and growth, more and more will be turning the corner to demonstrate that profitability is there and looking for funding for renewed growth.

US interest rates fell further than expected in 2025, starting the year at 4.25%-4.5% and ending the year down 75bps at 3.5%-3.75%. The Fed’s December 2024 dot plot had just 50bps of rate cuts in 2025. The annual inflation rate in the US came in at 2.7% in December 2025 having ended 2024 at 2.9%. US GDP growth was at 4.3% annualised in Q3, stronger than expected and implying about 2% for the year (Q1 was down) with c2% expected for 2026. The performance of 2025’s IPOs was reasonable (the average premium to IPO price at the end of the year was c20%). Enthusiasm for VC companies, especially in AI remained high.

And so, what about 2026?

One of the lessons of 2025 is to make fewer predictions and so the first thing is to focus on some of the key issues:

1. Will the value of Growth Equity deals rise again in 2026?

The US: This is a tough one as 2025 was a remarkable year of growth in the US market, up by $125bn yoy to $234bn with ten of the twelve months showing yoy growth. One of those that didn’t was December. There are three inter-related indicators here.

Appetite is there from AI businesses: Six US raises, all of AI businesses, raised $93.5bn, 40% of the US total in 2025 (Open AI $40bn, Anthropic $15bn and $13bn, Scale AI $14.3bn, Project Prometheus $6.2bn, xAI $5bn).

For the outturn in 2026 to exceed 2025 it will depend on a clutch of similar big raises. Already xAI has announced a $20bn raise at the start of 2026. OpenAI is reported by the WSJ to be seeking a raise of as much as $100bn. Tether is said to be looking at a $18.5bn raise and Waymo at $15bn. On that basis the 2026 US fund raising total has the potential to exceed that of 2025.

Will these be Growth Equity deals or IPOs? The FT reported at the very start of this year that OpenAI, Anthropic and SpaceX ‘are working on listings expected to raise tens of billions of dollars in proceeds.’ It’s arguably semantics but IPOs would shift them from the growth equity to the public bracket. OpenAI is said to be looking at valuations of $750bn, SpaceX at $800bn and Anthropic at c$300bn. Databricks – which raised $4bn in 2025 may also translate to the public markets with a c$135bn valuation targeted.

Is there an AI bubble? Clearly these businesses are not conventionally valued. Open AI’s Sam Altman has talked about $20bn of annualised revenue towards the end of 2025 (Source: The Information) and has talked about reaching $100bn annualised perhaps as early as 2027 and ‘hundreds of billions’ by 2030. Assuming that implies c$300bn by 2025 it would make OpenAI about twice the size of Meta (2024 revenue c$165bn). Sam Altman has stated that ‘You should expect OpenAI to spend trillions of dollars on data center build outs in the not-too-distant future’ and most external estimates anticipate c$1.4 trillion in data center and compute requirements in the next few years.

This heavy capex load, although perhaps shared with partners, is a key concern for markets, flying in the face of the typically capex light model that has supported the growth of the major tech stocks. If OpenAI can reach a valuation of $850bn in its next round, that is 42.5x end 2025 ARR, perhaps c8.5x start 2027 ARR and 2.6x 2030 ARR. By comparison Meta trades at c8.5x 2026 EV/revenue. The growth rates of Open AI are much higher; the profitability is obviously much lower.

And the applications of AI and the associated industries, autonomous vehicles, AI drug discovery, robotics, legal tech, software coding, cybersecurity, defense etc are still in the foothills of development.

So, our answer for the US market is yes – a further increase in the total sums raised in growth equity in 2026 – but it will be close.

Europe: An easier answer here. AI was less of a factor in market growth in 2025 - with AI only the second largest category of raises at $5.27bn, behind Software at $7.5bn. Nor has the European market grown as dramatically – its low was $31.8bn in 2022 – the 2025 level was just 55% higher at $49.2bn and just 23% higher than 2022’s $39.7bn. Looking at the shape of the year, growth was modest in H1 2025 – just 23% while in H2 it was 66%. We think the momentum- helped by lower valuations as investor interest spills out of the US – will see the total of raises grow again in 2026.

2. The sectors to look out for

Of course, we expect AI to dominate again. Looking beyond the LLMs there are three areas to highlight:

Defense: An obvious one perhaps but it was only the sixth largest VC raise category in the US in 2025 with $7.2bn raised and the ninth biggest in Europe with c$1.7bn raised. The trends are all in its favour – heightened political tension around Ukraine, Venezuela, Greenland and the other flashpoints of the world, the JD Vance Munich speech which pushes the onus for European defence onto the shoulders of European countries and has them scrambling to raise the percentage of GDP committed to defence to 5% while new technologies and methods of conducting warfare are offering an opportunity to young, VC backed tech led companies to take a disproportionate share of this new spending from the traditional platform led defence contractors. VC investment in defence companies is accelerating, and the trend appears likely to keep gathering pace as the world adapts to the new reality of heightened geopolitical tension and the realisation that regions, like Europe, will need to shoulder more of the burden and cost of their own defence rather than relying on the US.

Crypto and Blockchain: Crypto went out of style following the collapse of FTX in November 2022, the charges against Binance and its founder which led to convictions in November 2023 plus a supporting cast of bankruptcies and mishaps at the likes of Three Arrows Capital, Genesis Global, BlockFi, Voyager Digital, Celsius Network, Bittrex, and ComputeNorth.

The industry has recovered its poise post these vicissitudes under the umbrella of a more crypto friendly US administration and one of the features of 2025 was the accelerating pace of growth equity deals for crypto businesses. In Q4 there were five US deals in crypto and blockchain raising $2.1bn. Leading these was the $800m raise led by Jane Street for the crypto exchange Kraken executed at a $20bn valuation. A substantial Series A raise for Layer 1 blockchain business Tempo was led by Greenoaks and Thrive Capital, valued the business at $5bn and was supported by the financial infrastructure and payment processing business Stripe and the crypto investment firm Paradigm. The two big prediction market players Polymarket and Kalshi raised $3.3bn between them in Q4 2025. These are blockchain marketplaces. Polymarket, for instance, runs on Polygon blockchain technology using the USDC cryptocurrency. Every trade is matched peer-to-peer through smart contracts.

Long gestation businesses: Quantum, Fusion, Nuclear: Less a sector and more an investment style. These are businesses reliant on the growth of AI but not tied to it – the picks and shovels of the AI industry. We exclude data centres themselves as too closely tied to the short-term development of the AI phenomenon. Nuclear and fusion are about supplying the long-term energy needs of AI and transforming the means of delivery to allow its growth. Quantum computing techniques are the next frontier for the processing of AI and the shift to AGI. In each case venture is fulfilling its true function – to provide early-stage capital to high risk but potentially transformative businesses.

3. Realisations – will they improve in 2026?

Fundraising trends for VC firms were at a low ebb in 2025. There was the beginning of an upturn in the IPO market and a more noticeable upturn in M&A. Nevertheless, the flow of capital around the system remains stunted with the depressed levels of VC fundraising and its increased concentration in big funds reflective of the limited scale of realisations.

One of the key trends has been the ‘private for longer’ syndrome amongst big private companies reflective of a depressed IPO market, the easier availability of substantial amounts of long term private capital in some industries ( Anthropic raised $13bn in September 2025, $15bn in November 2025 and is currently raising another $10bn), the perception that value will grow rapidly and should not be crystallised too early combined with the growth of the secondary market to allow some necessary liquidity for staff and shareholders.

2026 then will be an interesting test of the strength of the public markets. There are certainly plenty of candidates. The CrunchBase Unicorn Board Growth chart below shows that at the end of 2025 it counted 1,640 unicorns which have collectively raised $1,160bn and which are collectively valued at $6,980bn. The key test will be whether the likes of Open AI, Space X and Anthropic move to IPO and the percentage of the equity that is made available to public markets or whether these companies decide that a ‘private for longer’ approach can be sustained.

Crunchbase Unicorn Board Growth – Counts, Funding and Valuation by year end

Public markets - The outlook for 2026

2025 saw the third year of roughly 20% growth in equity markets. The FTSE 100 led the way, up 22%. NASDAQ in local currency terms was up 18% and the S&P 500 up 16%. The STOXX 600 in Europe rose 17%. The FTSE Venture Capital Index was up 13%.

After three years of very positive returns the debate is whether this trend can survive into another year. We discussed this in our last Growth Equity Update. As a recap:

We start with the 2026-year end S&P500 forecasts from strategies at the major Wall Street firms.

The exhibit shows the 2026-year end S&P500 forecasts set by 18 Wall Street firms at the start of December.

• The average of the forecasts is for an end 2026 S&P 500 level of 7,572 versus 6845 at end 2024, a rise of 10.6% on the year

• The range is 7,100 to 8,000, a rise of 4% to 17%. None forecasts the market going down.

At the top end Deutsche Bank sees elevated valuations offset by an anticipated acceleration in earnings growth.

‘In 2026, we see robust earnings growth and equity valuations remaining elevated. We expect a pickup in earnings growth in 2026 to 14% (from 10% in 2025), taking S&P 500 EPS to $320. Corporate cost-cutting and the labour market remain risks, but for administration policies we expect checks and balances in the run-up to the mid-term elections. At 25x, the S&P 500 trailing multiple is well above the historical average (15.3x) but easily explained by favourable drivers: higher payout ratios, higher perceived trend earnings growth, fewer large drawdowns in earnings, and inflation below its long-run average.’

At the more pessimistic end of expectations Bank of America sees the momentum in the market running out in 2026. Like others it looks for strong earnings growth, with 14% anticipated. Unlike others BoA sees the buying power in the market fading, arguing that the buybacks that have supported the market are levelling out with the big tech companies instead investing in AI infrastructure. It sees the combination of less money returned in buybacks, higher AI capex and the Fed pursuing quantitative tightening as unhelpful for the market.

Much of the relative caution is around the valuation of AI stocks with BoA’s chief strategist observing a ‘buying the dream’ phenomenon with companies building out power infrastructure and AI data centres commanding peak multiples with little evidence for near-term monetization.

‘We’re paying a high multiple for growth stocks, but we don’t exactly know how this all plays out over the next few years…. The valuation reset is the big story for next year. Historically, if you look at years of really strong earnings growth, you haven’t necessarily seen the strongest market gains.”

The level of the S&P 500 at end 2026- Wall Street forecasts

The most recent BoA Global Fund manager survey was published in mid-November. Asked on their expectations for the S&P 500 at the end of 2026 just 1% of respondents expected it to be at 8,000-8,500; 13% were at 7,500-8,000; 43% expected 7,000-7,500; 20% 6,500-7,000 (2025 end year level was c6,845); a surprisingly large 14% anticipate 6,000-6,500; with 9% at 5,500-6,000 or less.

Asked on the most likely outcome for the global economy in 2026, 53% expect a soft landing, 37% expect no landing and just 6% expect a hard landing.

- Global growth expectations are improving. Fund manager expectations for global economic growth turned from negative (net -8%) to positive (+3%) for the first time in 2025.

- The most bearish potential developments were cited as the combination of inflation and Fed rate hikes (43%) and a stalling of AI capex acceleration at 26%.

- Ranking likely relative 2026 market performance, 37% of investors cited Emerging Markets, ahead of NASDAQ at 13%, Euro Stoxx at 10%, the S&P 500 at 6% and the FTSE 100 at 3%.

Our Rothschild & Co strategists Kevin Gardiner and Anthony Abrahamian note that valuations are high versus history, particularly in the US but that 2026 earnings growth, anticipated at 14% is also poised to be strong.

Valuations are dear but earnings growth is intact – and may broaden.

Their views on the current market outlook are summarised in the Exhibit.

Looking into the 2026 timeline some key indicators to look out for:

US Interest rates: Following the 25bps cut at the Fed meeting on December 10 the Fed rate is at 3.5%-3.75%. The next Fed meeting is on January 28th, 2026, with an 88% expectation that rates will remain unchanged at that meeting. The current most favoured anticipated rate at the end of 2026 (the last meeting of the year is 9 December 2026) is 3%-3.25%, suggesting the market’s core expectation is 50bps of rate cuts in 2026.

New Fed Chair: The term of the current Fed chair, ‘stubborn’ Jay Powell runs out on May 15, 2026, although he can choose to remain as a Fed governor until the end of January 2028. President Trump in December 2025 made it clear that a ‘litmus test’ in his choice of new Fed chair will be their willingness to cut Fed rates. He will announce his nominee early in 2026. The market likes the combination of economic growth and lower rates. The potential kickback is higher inflation – the US is already above target at c3%.

US earnings season: With the market relying on mid-teens earnings growth in 2026 the early indicator of the US full year results season will be key. Based on historic reporting patterns Apple, Microsoft, Meta and Tesla are likely to report in the week starting January 26th with Alphabet and Amazon the following week and NVIDIA (which has a January year-end) in late February.

UK interest rates: The last BoE meeting of 2025 on 18 December cut rates by 25bps to 3.75%. With the Office for Budget Responsibility looking for inflation to average 2.5% in 2026 the market expectation is for interest rates to come down by 50-75bps to 3.0%-3.25% by year end.

European interest rates: The message coming out of the ECB in the last few months has been one of interest rates, now at 2%, having reached an equilibrium after a period of sharp rate cutting. At its end October meeting the ECB again held interest rates steady at 2%. ECB president Christine Lagarde observed after the October meeting that EU monetary policy is ‘in a good place’ and that the outlook for inflation is ‘broadly unchanged’. The market consensus looks for interest rates to remain unchanged through 2026.

December’s growth raises

December’s European deal value was $4.4bn up 55% yoy. The US at $14.4bn was down 9% yoy.

December continued the strong recent run of months in European growth equity raises. The Rothschild & Co Deal Monitor recorded $4.4bn of growth equity and VC deals of $20m and above across 49 raises.

Europe – 49 deals raised $4.4bn in December

After a very strong period in September- November when $84.8bn was raised in just three months, up 2.3x yoy, US raises in December were down 9% yoy at a still very respectable $14.4bn. It was only the second down month of the year- the other was $10.5bn in May.

USA (and Canada) – 47 raises of $100m + in December for a total of $14.4bn

Our views on the state of the venture capital markets

October 12, 2022, marked the low point for the S&P500 on the back of global inflation, rising interest rates, and increased geopolitical risk. It also ended the buoyant market conditions for the venture capital market that saw its activity and valuations peak in late 2021.

October 12, 2025, marked the third anniversary of the bull market that has seen the S&P500 rise by almost 90% and NASDAQ by 120%.

In that period the FTSE Venture Capital Index was up by almost 170% and since June 2025 has been back above its previous 2021 peaks.

This revival of the growth equity market has been led by the US and by a surge of interest in artificial intelligence model providers and for companies using AI to transform a range of underlying industries.

At the same time the venture industry has re-adopted strong underlying approaches to investment with companies in most sectors striving to achieve a better balance of growth, profitability and cash flow. The underlying quality of the cohort of VC backed companies has improved.

Our summary of the outlook

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, quantum, semiconductors, new energy sources like nuclear and fusion) supporting the development of AI.

- The influence of AI is percolating through many other industries such as drug discovery, defence, robotics, legal tech, autonomous vehicles, cybersecurity and software fuelling a broader advance in the growth equity market.

- Overall, the VC market is regaining confidence with the strength of interest in Software being notable and fintech, blockchain/crypto and biotech reviving strongly.

- There is a burgeoning interest in defence industries from investors with both the tense geopolitical political environment, the advances in AI applications and the experience of the combat in Ukraine contributing to investor focus. By contrast, ClimateTech, while still a substantial sector has become less prominent both as a result of some high-profile failures and being less favoured politically in the US under the current administration.

- Fund raising for venture capital firms remains subdued. Fund raising is concentrating into larger, established firms. US VC fundraising in 2025 was concentrated in larger firms and at near decade lows.

- The speed of the investment process has slowed down since 2021-22. The level of diligence on deals has stepped up. This is true even in the ‘hot’ parts of the market like AI. Outside these areas it is marked – processes take time, downside protection is sought.

- Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on the combination of growth and profitability (or a rapid path to it) and on free cash flow.

Read the previous editions: May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024, January 2025, February 2025, March 2025, April 2025, May 2025, June 2025, July 2025, August 2025, September 2025, October 2025, November 2025, December 2025

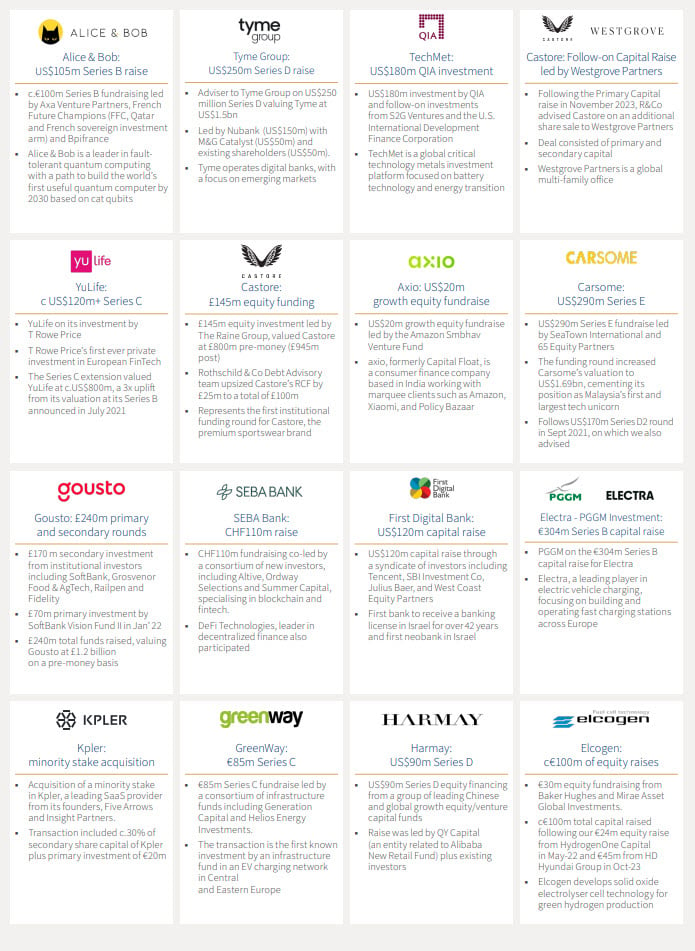

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Mark Connelly

Co-Head of Global Market Solutions

+1 212 403 5500

+1 917 297 5131

Chris Hawley

Global Head of Strategic and Private Investors.

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Capital Markets Europe

+44 20 7280 5088

+44 7542 477 291

Antoine de Guillenchmidt

Co-Head of Equity Capital Markets Europe

+44 20 7280 5377

+44 7907 712 978

Pete Nicklin

Co-Head of Equity Capital Markets Europe

+44 20 7280 1668

+44 7912 395 294

Laura Klaassen

Head of Private Distribution

+44 7926 905 488

Thomas Chung

Head of Private Capital, North America

+1 212 403 5559

+1 917 594 7208

Tim Brenton

Director of Private Distribution

+44 20 7280 1351

+44 7788 395 556