Challenges, Perspectives, and Opportunities in Private Markets

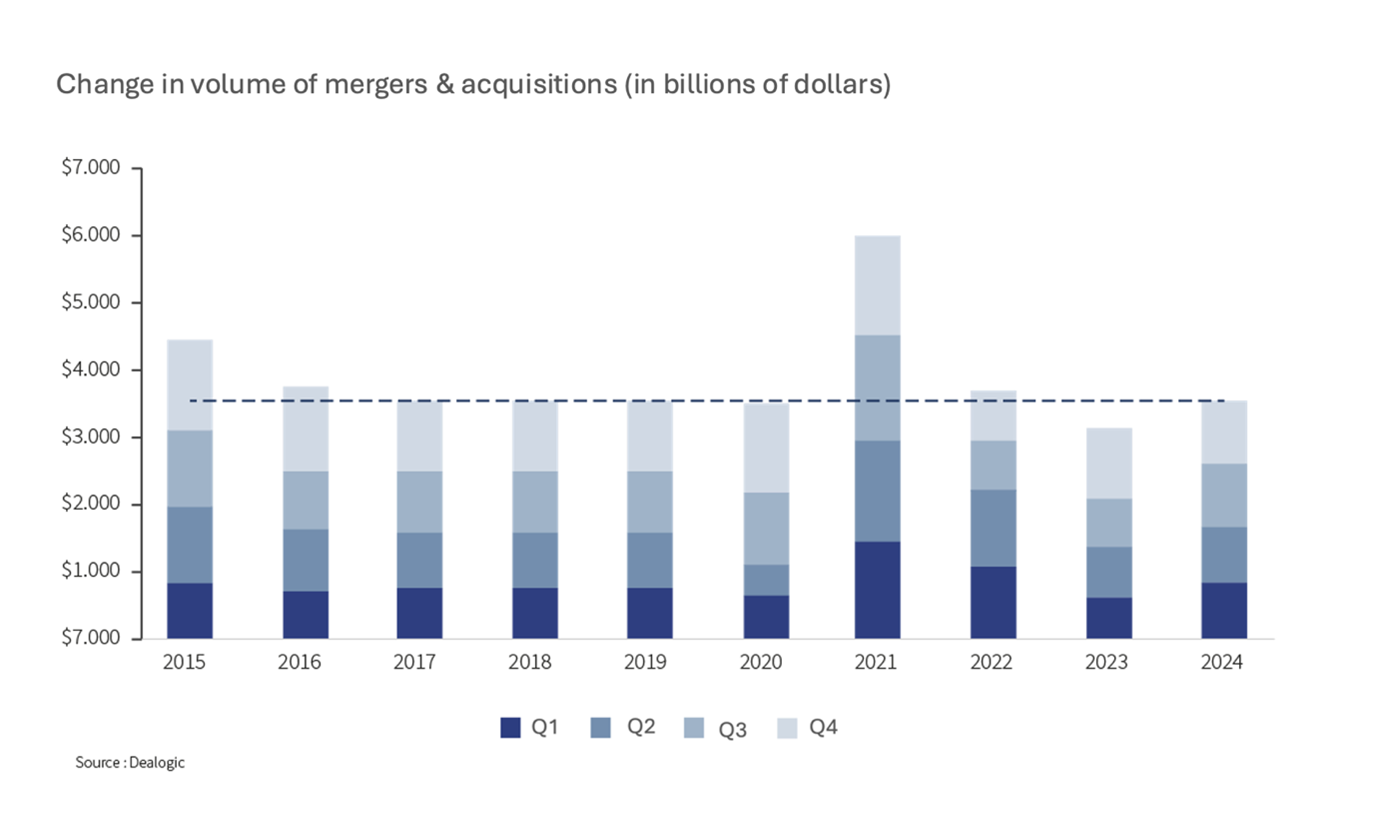

On the heels of 2023, a year marked by a low point, 2024 showed signs of a recovery for private markets, one that was easier to see in the second half, driven by improved financial conditions, falling interest rates and better political visibility. This dynamic paved the way for transactions to recover, albeit more in terms of volume than number. In this category, take-private transactions1 hit a record level in 2024.

The buyout2 segment enjoyed stronger momentum in 2024, totalling some $520bn in transactions, i.e. +27%3 year on year.

These deals are nevertheless more complicated to finalise due to the greater selectiveness of buyers and a disconnect between buyer and seller expectations in terms of valuation.

As a result of this situation, deals tended to centre on large-scale transactions, particularly in the United States. In fact, the US market made up nearly three-fourths of the increase recorded over the year. And, although further behind, Europe could very well benefit from this momentum in 2025.

Liquidity and exits gradually make a comeback

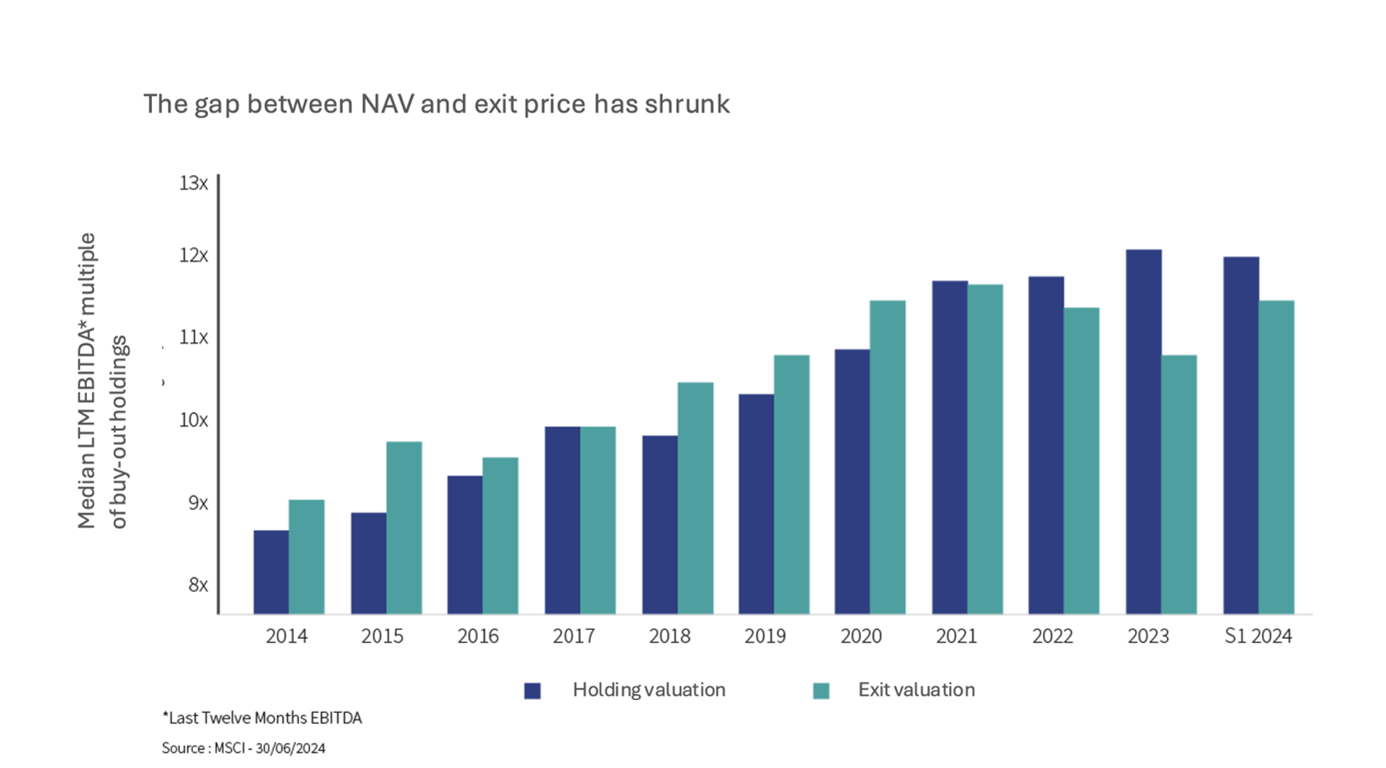

One of the biggest challenges on the market in 2023 and, to a lesser extent, 2024 was the complexity of exit strategies. Historically speaking, exit valuations have exceeded holding valuations, reflecting high demand from buyers. This trend got turned on its head in 2022 and 2023, showing just how challenging it was for funds to sell their assets.

This phenomenon sapped the momentum from both the unlisted assets market and from fund-raising efforts, with investors impatiently waiting for the payouts associated with the sales. Prices did remain resilient, however: although no massive correction was observed, the limited number of transactions nevertheless slowed the market once again.

In 2024, buyer and seller expectations began the process of converging, but this process is not yet fully complete. That said, the stabilisation in progress is conducive to getting deals done.

From an exit standpoint, 2024 saw investors bring significant pressure to bear on asset management companies. Exits were primarily carried out via strategic M&A deals (50% of transactions) and secondary LBOs (35%)4, while the IPO market remained sluggish.

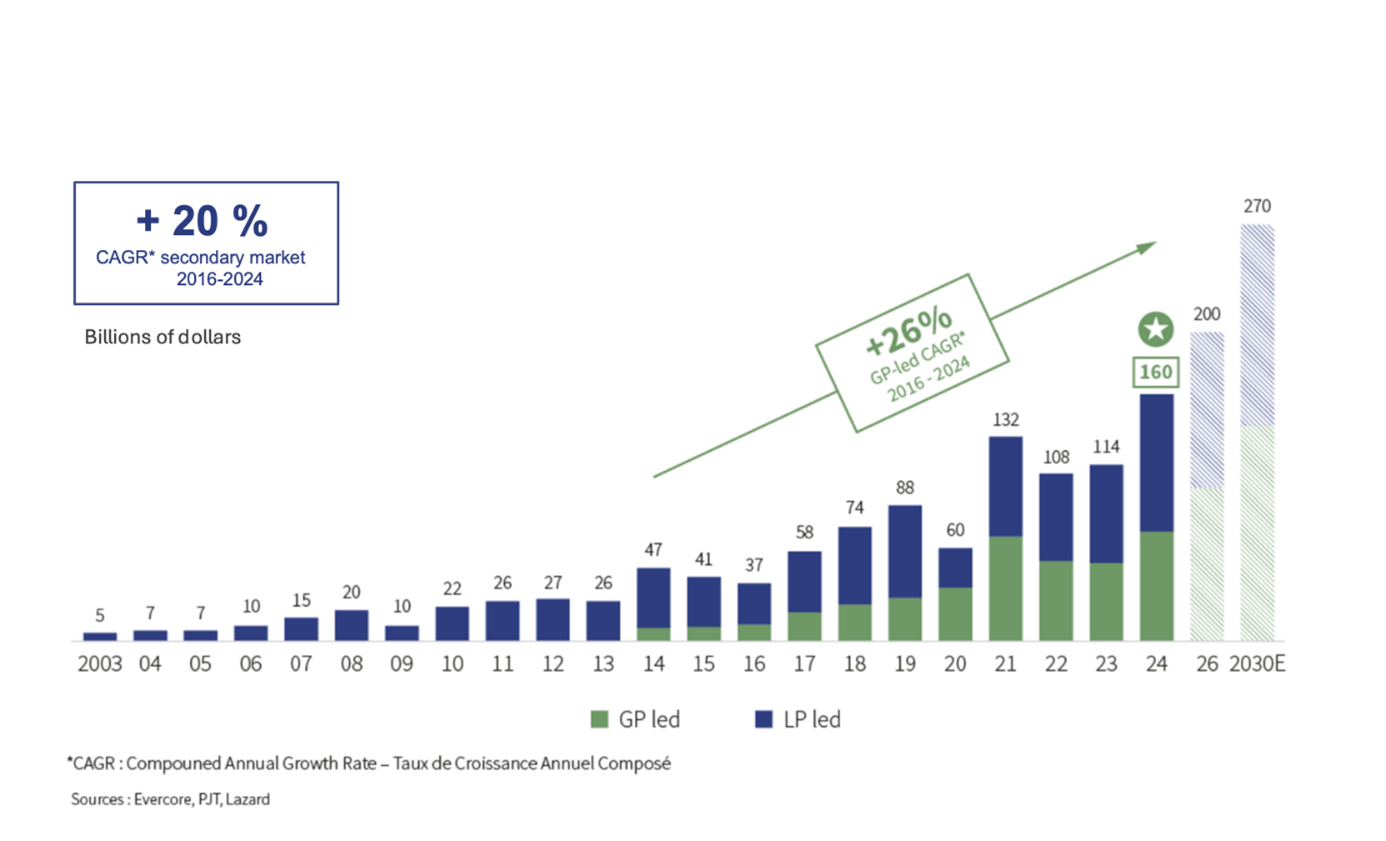

Ongoing expansion for the secondary market

The secondary market continued to expand in 2024, playing a central role in providing the liquidity so essential to GPs working to raise money for successor funds.

Bear in mind that the secondary market is structured around two types of transactions: LP-led (initiated by investors selling some or all of their portfolio) and GP-led (initiated by asset management companies to sell one or more assets). Interest in the market has been plentiful, with substantial amounts of capital raised, as evidenced by the $30bn hard cap recently reached by Ardian. This dynamic offers liquidity opportunities to primary investors and an additional exit option to asset managers, all while furthering value creation in the target companies. This is especially true when it comes to continuation funds, which are designed to simultaneously offer a liquidity window to existing LPs, while allowing the initial GP to maintain control of the assets.

We can also point to the collateral effect of the development of evergreen funds. This is because, in order to build their portfolio, evergreen funds use secondary transactions (particularly LP-led), sometimes with lower projected returns compared to institutional investors, thus putting upward pressure on prices. This influx of capital also works to support the valuations of secondary transactions and to reduce the discount.

Lastly, this type of transaction gives participants the benefit of leverage specific to the deal through the use of financial engineering, often involving deferred payments.

Consequently, during the selling process, today’s secondary market offers an additional and alternative exit option versus strategic or financial exits.

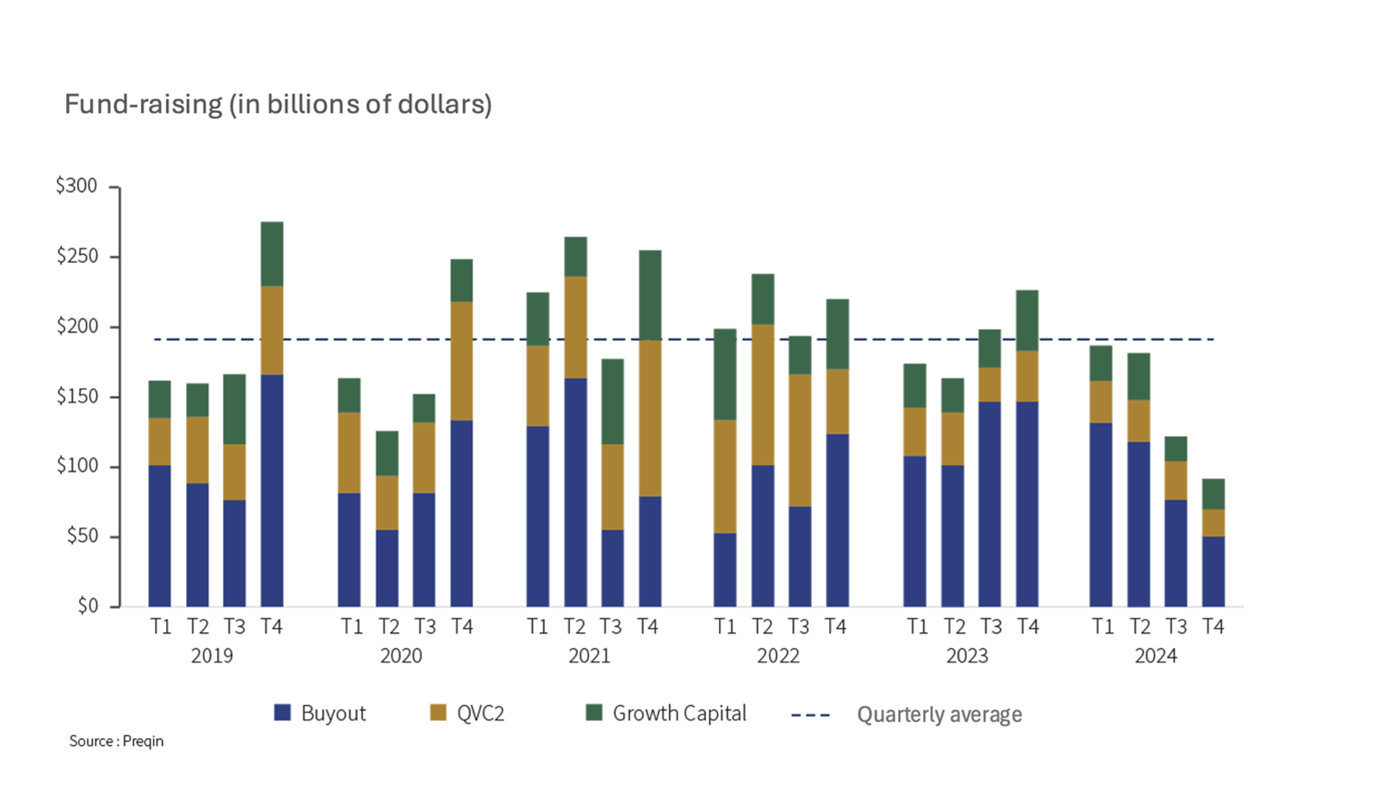

Concentration and extension of fund-raising periods

Despite a more favourable environment, fund raising campaigns have yet to recapture the robustness they enjoyed prior to 2023.

One notable factor is the concentration of capital raised: just five asset managers were responsible for capturing 60% of funds raised5 in Europe.

This phenomenon can be attributed first to the consolidation and concentration of sector players and second to the need for investors to seek out experienced teams, capable of weathering market cycles and effectively deploying capital. As a result, the number of funds achieving their target has fallen 40% compared to 20216.

Time spent raising capital has also been on the rise, putting additional pressure on asset management companies to generate payouts in a bid to raise new funds.

2025 will thus be a decisive year for gauging their capacity to redeploy capital and keep up the pace in fund-raising.

4 themes for 2025:

Investing in private markets is a long-term game: in order to capture outperformance in these asset classes, investors implicitly accept the lower liquidity of the underlying instruments. When putting together a global, diversified asset allocation, the portion invested in unlisted assets must therefore be calibrated with respect to both the investor’s liquidity needs and capacity to mobilise capital over an extended period. The goal is thus not to identify tactical adjustments, but rather to focus on lasting trends that promote value creation. In a market where selection is key, certain themes and geographic areas therefore stand out for their resilience and their prospects for long-term growth.

US market to remain central

The unlisted assets market is still largely dominated by the US, which accounted for more than half of all total capital invested in Private Equity in the first quarter of 20246; a figure that only confirmed a long-established trend.

A key element of the US market lies in its granularity. If we look at companies generating revenue of more than $100m, we see that the mid-market7 comprises roughly 15,000 private companies versus just 2,500 listed companies. Such disparity and diversity call for a local approach, making it crucial to work with local teams.

Finally, the market is extremely dense in terms of investment funds, making selectiveness all the more strategic. Given the multitude of teams out there, it is all the more complicated to identify good teams with good access and to do your due diligence.

This granularity, though greater than in Europe, means it is critical to adopt a diversified approach when investing in the mid-market.

Healthcare

The healthcare sector is undergoing significant expansion, particularly in the US, which makes up 60% of the global market8. The sector’s solid fundamentals, namely the ageing of the global population, the growing impact of chronic illnesses, and technological advances, make it highly resilient indeed. Nor is it limited to research and biotech, which tend to experience long investment cycles and strong volatility.

A detailed analysis of the industry highlights various investment ideas that can be addressed through public or private markets. The diversity of sub-sectors, ranging from advisory services and data analysis to healthcare technologies (medtech) to health and diagnostic tools, calls for hyper-specialisation.

Investing in this sector requires extensive expertise and a specialised approach, with the top-performing funds combining financial, medical and entrepreneurial talents. In our own unlisted asset allocations, we rely on resilient models, drawing on robust growth and strong revenue visibility while steering clear of extreme risks (R&D, regulation, de-reimbursement).

Infrastructures

The infrastructures sector is fuelled by strong structural trends like the energy transition, digitisation and growing need for public transport and infrastructures. The funding requirements and resilience of these types of assets make them a strategic market for long-term investors.

We still hold both our interest and conviction for infrastructures and plan to continue exposing our portfolios to this key diversifying asset class. Infrastructures provide effective protection against inflation, thanks to the indexing mechanisms built into many assets, and offer stable, predictable revenue streams, often backed by long-term contracts or favourable regulatory frameworks, which help reduce the overall volatility of the portfolio.

Private debt

Lastly, private debt has become a go-to additional strategy for traditional bond portfolios, offering an attractive alternative to investors searching for yield. The main segment of the private debt market, i.e. direct lending9, delivers significantly higher rates of return than other credit categories, with less volatility primarily stemming from the illiquidity premium associated with these investments. In the US, private debt is a financing solution largely adopted by corporations, giving investors the benefit of substantial spreads10 and recurring coupons. Furthermore, the quality of the financed companies remains high, with leverage levels under control and a noteworthy stability both in terms of credit spreads and the strength of the companies themselves. All in all, private debt complements Private Equity strategies and liquid portfolios quite well.

2025: a year awaiting a rebound

2025 promises to be a pivotal year for Private Equity and unlisted assets. With valuations stabilising, liquidity making a comeback and investors proving more selective, it is shaping up to be a year full of opportunities. Europe has the potential to catch up at least somewhat with the United States, particularly if capital flows and exit momentum improve.

A rigorous and selective approach will prove essential in navigating these developments. Being able to identify the best portfolio management teams, to stay the course in an increasingly consolidated market, and to take positions in buoyant investment themes will be decisive factors in creating value over the long term in an ever-more-competitive environment.

[1] A take-private is when a company listed on the stock exchange is delisted to make it a private company.

[2] Capital invested in Buyout or Capital Transmission strategies serves to acquire an unlisted company using leverage. The buyers take out a loan in addition to their capital investment in order to purchase the target company.

[3] Source: Dealogic

[4] Source: Dealogic 2024

[5] Source: Preqin

[6] Source: Statista Research Department – June 2024

[7] Mid-market firms are intermediate-sized companies.

[8] Source: BMI Research - 2024

[9] Direct loans are not affiliated with the banking sector.

[10] A spread is the difference between the yields of a bond versus an equivalent-maturity loan considered “risk-free”.

Contact us

The Rothschild Martin Maurel teams are at your disposal to provide you with the best possible advice on these subjects.

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.