Growth Equity Update

June 2026 – Edition 51

-

Bolstering European VC: Balderton Capital’s ‘Build in Europe’ campaign looks to bolster European start-up self-confidence asserting ‘Europe's technology ecosystem is thriving. Founders are building world changing businesses in everything from AI to energy to space — right here, right now. There has never been a better time to build or join a tech startup in Europe.’

-

State-led initiatives across Europe to encourage VC led growth: We review state led funding initiatives across Europe to bolster the VC ecosystem, ranging from the European Investment Fund’s ETCI 2 initiative, the Tibi 2 programme in France, a flurry of UK initiatives including the Mansion House Accords and the Deutschlandfonds initiative in Germany.

-

The peak of VC market fundraising? YTD in 2026 three companies have raised $240bn or 68% of total US VC funding - OpenAI $132bn, Anthropic $85bn, xAI $23bn. With IPOs for all three reportedly looming, this likely marks the peak of US growth equity fundraising.

-

Around 25% of US unicorns have ‘fallen’: According to Pitchbook estimates almost half of the US’s 857 unicorns have not raised new funding in the last three years. It estimates the valuation of startups that last raised in 2021 on average to be 68% lower. Of the 857 unicorns around 220, or c25%, are estimated by Pitchbook to have fallen beneath the $1bn valuation level.

-

On the other hand, Corgi Insurance, a US full-stack insurance platform offering insurance for start-ups, announced a $160m Series B on May 7th at a $1.3bn valuation and then a $106m Series B-1 at a $2.6bn valuation on May 21 – a doubling in just three weeks…

-

Fundraising records continue to fall: In the US May VC fundraising was $69bn across 47 rounds, only the second highest month of the year after February’s $181bn but still the second largest month ever for US VC raises. Europe saw fundraising of $6.3bn, up 67% by value yoy.

-

Pipeline of c$19bn. Some big, completed raises (Anthropic $50bn, Anduril $5bn) slim the impending fundraising pipeline to c$19bn, with $10bn in the US and $9bn in Europe.

-

Public markets – Planetary alignment of Mercury, Venus, and Jupiter…Since the end of March NASDAQ is up 28% and the S&P 500 19%. Tech has contributed 80% of the returns for global markets ytd. Almost half of all global stocks have fallen. All eyes shift to the Space X IPO.

Download a PDF version of the Growth Equity Update

Built in Europe...by Balderton

Built in Europe aims to shift the conversation from potential to proof

It’s not just Jude Law on the billboards advertising Legora. This month Balderton Capital, which over 26 years has invested in c250 companies focused on early and growth stage technology businesses, launched a campaign to shore up confidence in the European start up scene. The campaign is being launched across London, Paris, Berlin, Munich and Stockholm and includes billboards and digital advertising. At its heart is a dedicated website https://www.builtineurope.com/

The campaign is ‘Built in Europe’, and it asserts that:

‘Europe's technology ecosystem is thriving. Founders are building world changing businesses in everything from AI to energy to space — right here, right now. There has never been a better time to build or join a tech startup in Europe.’

The aim is to stress that building globally significant tech businesses is not the sole preserve of the US and that Europe has the track record and capability to do the same.

The Built in Europe dedicated website incorporates a jobs marketplace with adverts from up to 1,000 startups. Balderton says the site is designed to become Europe’s largest startup talent hub with jobs advertised across AI, fintech, climate and health tech.

The website incorporates a ‘Build’ section which directs founders and early-stage businesses towards accelerators and incubators across six major European countries.

The campaign has the backing of more than 100 founders and CEOs from across Europe, among them the founders of Wayve, Mistral, ElevenLabs, Lovable, Alan, Synthesia, Revolut, Quantum Systems, The Exploration Company, Proxima Fusion, Hived, GoCardless and others.

Multiple founders are on the website extolling Europe’s advantages. As an example, Anton Osika, the co-founder of Lovable,

‘There has never been a better time to build from Europe than now. The talent is here, the capital is here, the ecosystem is here. And we have the ambition to match.’

For Balderton the aim is to shift the narrative around European tech. General Partner at Balderton, Suranga Chandratillake comments:

“For too long, the narrative around European tech has been stuck on all the things that need to change. Built In Europe aims to shift the conversation from potential to proof’

The Balderton campaign dovetails with a series of state led initiatives across Europe to encourage VC led growth with state led finance and banking. Amongst these initiatives are:

- Sovereign AI: A £500m investment fund backed by the UK state and intended to support and invest in British AI companies.

- Changes at the British Business Bank: In late 2025 the British Business Bank saw its total financial capacity increased to £25.6bn. It will be able to invest greater amounts in companies through direct investments; it will be able to lead investment rounds and make strategic investments of up to £60m in UK growth companies.

- The UK Mansion House accords: At UK government prompting, 17 of the UK’s largest DC pension funds have now pledged to invest at least 10% of their defined contribution (DC) default funds into private market assets by 2030, potentially releasing an incremental initial c$50bn of funding for private assets with at least half earmarked for the UK.

- The UK National Wealth Fund: The NWF, the UK government’s principal investor with £27.8bn of capital, will provide growth capital (£25m-£100m+) to scale businesses ‘with proven technologies, credible business plans, and strong management teams.’

- The European Investment Fund’s ETCI 2 initiative aims to create a €15bn fund of funds to unlock up to €80bn in scale-up capital across Europe.

- The EC’s €5bn Scaleup Europe Fund will invest directly into companies in strategic tech sectors looking for funding rounds of €100m+.

- The ‘Growth Fund Germany’: It is managed by KfW and is a part of the Future Fund of the German Federal Government. With a fund volume of just over €1bn it is one of the largest VC funds of funds ever launched in Europe.

- The Deutschlandfonds initiative is a €100bn fund of funds whose mission is to fill the gap in growth and innovation financing in Germany. The German government is providing €10bn in equity, with private backing to take the total to the €100bn.

- Zukunftsfonds ‘Future Fund’. In 2021 The German Federal Government introduced the Zukunftsfonds (“Future Fund”) set up with €10bn of available VC funding and aiming to support start-ups in the growth phase with high capital requirements.

- France €10bn public fund managed by Bpifrance. In June 2017 French President Emmanuel Macron declared France should become a start-up nation. As well as the new Bpifrance fund there were changes to the French capital gains and wealth taxes to encourage entrepreneurs and the introduction of the French Tech Visa, a four-year visa to attract key workers.

- Tibi 2, announced in France in 2023 saw a further €7bn in new financial commitments from 35 institutional investors focused more closely on strategic sectors deemed crucial for Europe’s technological sovereignty including AI, semiconductors, quantum computing, cybersecurity and climate tech.

- Bpifrance is France’s public investment bank designed to support French businesses and especially SMEs.

- EU AI Champions Initiative: In February 2025 the General Catalyst led ‘EU AI Champions Initiative’ called for greater investment in AI infrastructure and less regulation. The project sees twenty institutions investing €150bn in European AI over the next five years.

- InvestAI - €50bn of incremental EU backing: At the 2025 Paris AI summit the EU announced a €50bn EU initiative, InvestAI, including a new European fund of €20bn for AI gigafactories.

- Poland has seen substantial government support for the emerging tech scene coordinated by the National Centre for Research and Development. It uses the Polish Development Fund which supports PFR Ventures, a government owned institutional Limited Partner to boost the development of the VC-funded sector.

- In Italy the state-owned Cassa Depositi e Prestiti (CDP) manages over €2bn across direct investments, fund-of-funds, and technology transfer funds to support startups from pre-seed to scale-up.

So, there is state support and now Balderton’s ‘Built in Europe’ moral support. As Build in Europe says

‘For years, the conversation has been about Europe's potential. What we could be. What we might become -once a long list of things finally change.

But that misses what's already happening. Right now, across the continent, founders have built and are building some of the most important companies in the world.

Not waiting for permission. Not looking somewhere else for the blueprint. Just building.

They're rethinking how we move, how we create, how we generate energy, how we look after our health.

They're competing globally - and winning - from Amsterdam, Paris, London, Stockholm, Warsaw, Berlin and cities in between.

Yes, there is more to do. There always is. But the gap between Europe's potential and Europe's reality is closing - faster than the headlines suggest.

It’s time to say that clearly, and loudly. To celebrate the founders doing the hard work, and to inspire the next wave to join them.’

Valuation and the private markets

Some perspectives on VC market valuations

Three illustrations of the state of venture markets right now.

Startup Insurance, Doubling in Weeks: Corgi Insurance is a ‘full-stack insurance platform built for technology companies. That means fast quotes, great pricing, and a team that understands your business.’ It operates under the slogan ‘Start Up Insurance, Quoted in Minutes.’

https://www.corgi.insure/

It’s a great idea. The company offers insurance packages for start up businesses offering protection for core categories like commercial general liability, technology errors and omissions, protections for directors and officers, and cyber. As businesses scale up through the funding rounds the insurance becomes more comprehensive. Speed and simplicity are key with Corgi offering quotes within minutes and same day cover. It can do this because its full stack approach means it encompasses the key elements like underwriting, policy management, and claims itself rather than going out to third-party insurers.

Its funding record is remarkable.

January 2026 - $108m Seed and Series A at a $630m valuation: The company emerged from stealth on January 10, 2026, announcing a combined seed and Series A round of $108m backed by, amongst others, Y Combinator, Kindred Ventures and Contrary.

Founder Nico Laqua commented "Founders shouldn't have to choose between speed, coverage quality and price. We built Corgi to deliver all three in one place, so startups can get covered quickly and focus on building. This capital helps us expand coverage and keep improving the product."

May 7, 2026 - $160m Series B at $1.3bn valuation. Just under four months later Corgi announced a TCV led Series B raising $160m with a valuation of $1.3bn. Other funds backing the deal included Kindred Ventures, Repeat VC, Alpha Square Group, and GSBackers.

Founder Nico Laqua commented “Our mission is bigger: we want to use the fresh capital to expand into more lines of insurance and build a generational company.”

May 28, 2026 - $106m Series B-1 at a $2.6bn valuation: Exactly three weeks later Corgi announced a $106m Series B-1 raise at $2.6bn, meaning its valuation had doubled intra-month. The B-1 round was only made available to existing investors. with TCV, Kindred Ventures and Prime Capital participating.

Founder Nico Laqua commented that the process was initiated by the shareholders “We weren't planning on doing it. It wasn't something that we went out and solicited. We didn't want to take too much, but I think the company is clearly worth a lot more than it was even a couple weeks ago. It's important that we have a lot of financial strength as a financial institution.”

He observed that insurance is a “highly capital-intensive industry” and that post the Series B “demand has accelerated quickly across new product lines and partnerships.”

The B-1 round was only made available to existing investors with TCV, Kindred Ventures, Prime Capital and others participating meaning that the same funds agreed to pay twice the early May valuation three weeks later.

Unanticipated revenue trajectory acceleration in three weeks to justify doubling of valuation? Corgi claimed $40m of annualised revenue in January 2026 and that it went profitable in April. It reports a trajectory of revenue growth ‘rarely seen in fintech or insurance’. Revenue growth at a rapid rate must though already have been anticipated by investors in evaluating the $1.3bn valuation in early May (a multiple of c32.5x annualised January revenue).

Reported in TechCrunch Kanyi Maqubela of Kindred Ventures observed that revenue growth justified the higher valuation in the Series B-1 round. There are though no figures cited for the step up in revenue trajectory that would imply a doubling of valuation within three weeks. The real test of the new valuation will be in the next funding round or, more substantially, the eventual exit.

Kalshi – More scrutiny but another raise

We first wrote about the rise of Kalshi and Polymarket in our December 2025 Growth Equity Update. The two prediction market gambling businesses operate on blockchain infrastructure with Polymarket historically focused on international markets and Kalshi on US markets. Their US regulatory status has evolved. Kalshi is licensed by the Commodity Futures Trading Commission (CFTC) which regulates the US derivatives markets. Polymarket has lacked the legal status to operate in the US but recently acquired a CFTC-licensed exchange, QCEX, and has relaunched.

In early March the CTFC’s Market Oversight Division launched a formal rulemaking process for what kinds of events can be included in prediction market contracts and under what conditions.

Democratic Congress members have introduced the BETS OFF act looking to ban events connected to military operations and government actions.

Some individual states have looked to restrict the prediction markets based on their activities amounting to unlicensed wagering - Massachusetts, Nevada, Arizona and Michigan are prominent in this respect. In early May though a federal judge permanently blocked Arizona from pursuing a criminal case against Kalshi on the basis that its regulation is exclusive to the Commodity Futures Trading Commission.

California has focused on insider trading issues with Governor Newsom signing an order to bar state officials from using non-public information to profit in prediction markets.

Three recent insider trading cases – involving a Google employee using private information to bet on internet search trends, a US Special Forces member betting on impending US military operations and a former US Congress Representative betting on his own actions – have come to light.

Polymarket raised $2bn in November 2025 at an $8bn valuation, up from $1.2bn in January. The company is reported to be currently raising between $0.4bn-$1bn at a $15bn valuation.

Kalshi raised a $185m Series C led by Paradigm in June 2025 at a $2bn valuation. In October 2025 it raised a $300m Series D led by Andreessen Horowitz valuing the business at $5bn. In November it raised $1bn at $11bn in a round led by Paradigm, Sequoia and Andreessen Horowitz. In March 2026 Kalshi raised a further $1bn in a round led by Coatue Capital at a valuation of $22bn, twice the November level. In May Kalshi raised another $200m as an extension of its Series F at the $22bn valuation. In under a year the valuation of Kalshi has risen by 11x. Kalshi’s annualized revenue based on the May figure is $1.5bn.

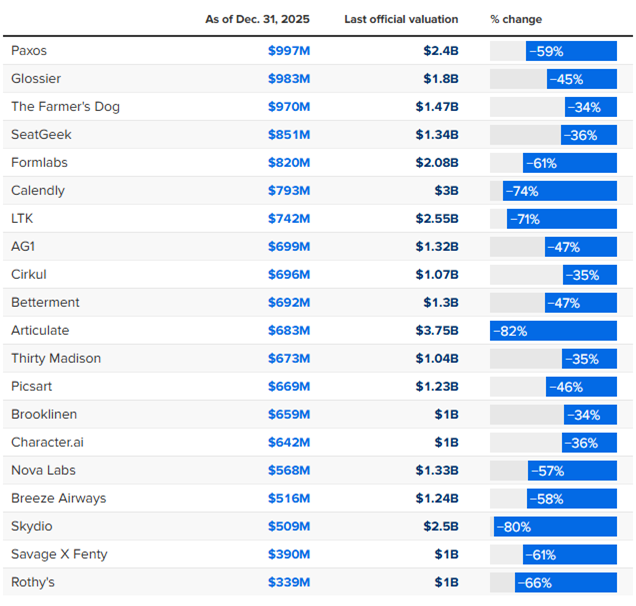

Falling Unicorns – Bubble aftermath

Valuation movements can work both ways. An interesting analysis by Pitchbook reported by CNBC analyses the condition of the 857 companies identified as US unicorns and makes a series of observations:

- almost half of the 857 companies have not raised new funding in the last three years. This means that the valuation benchmark is at best stale. It may be that the companies have flourished, become cash generative and require no extra funding. Pitchbook observes it may more likely be the result of underperformance of growth expectations against testing initial valuations – in turn a function, particularly in software, of changed market conditions post the advent of AI.

- The valuation of startups that last raised in 2021 is on average 68% lower: Perhaps not surprising. 2021 marked the then peak of the VC market with a bubble in valuations revealed by the fall away in H2 2022 and 2023 before the revival of the VC market started in H2 2024 on the back of AI. It is unsurprising that some businesses found themselves stranded on excessive valuations. Pitchbook finds a similar phenomenon for companies that last raised in 2022 with a valuation decline averaging 52% for those that have not raised since then.

- Around 25% of unicorns have ‘fallen’: Of the 857 identified unicorns, around 220 or c25% are estimated by Pitchbook to have fallen beneath the $1bn valuation level. The estimates are made based on comparisons with public company valuations and ‘soft’ factors such as growth in headcount. Reflecting the changing AI driven environment the largest sector category within the ‘fallen’ names is enterprise software with 75 SaaS firms on the list. The next largest, with just under 40 names is fintech.

The Exhibit highlights some prominent names amongst the 220 estimated fallen unicorns which contrasts Pitchbook’s latest estimate of their valuation with the last valuation mark from a funding round.

A selection of fallen unicorns identified by PitchBook.

Source: CNBC, Pitchbook

The peak of venture capital markets?

Are we hitting the peak of venture capital fundraising?

Year to date to end May 2026 has seen c$350bn of venture funding raised in the US. This is $6bn more than the total for 2024 and 2025 combined. In turn the 2025 total at $234bn was 2.1x the $110bn raised in 2024.

The phenomenon has been driven by the big AI rounds. In 2024 US AI companies raised- according to our R&Co Monitor - $41bn, 37% of the annual total. In 2025 the figure was $133bn, 57% of the annual total. In 2026 to date AI raises stand at $276bn out of $352bn raised, or 78%.

The growth in private markets has played out against the backdrop of public markets that have suffered substantial de-equitisation over time. There has been a relative dearth of IPOs since 2021, and we have seen the phenomena of private companies staying private for longer and raising unprecedentedly large amounts of capital in private rounds.

The structure of this appears to be about to change. In the matter of a few weeks Space X and Anthropic have filed S-1s in readiness for an IPO. OpenAI is widely reported to be lining up for an IPO in 2026 or 2027 (see Anthropic files for blockbuster initial public offering – FT June 1, 2026).

The shift of these businesses from private to public status would remove the biggest recipients of private funds from the field. In 2024 these three companies raised $22.6bn – 55% of that year’s AI total and 21% of all US VC funding (xAI $12bn, OpenAI $6.6bn, Anthropic $4bn).

In 2025 the same three companies raised $77.5bn, 58% of the AI total and 33% of the venture market total.

YTD in 2026 these companies have raised $240bn (OpenAI $132bn, Anthropic $85bn, xAI $23bn) or 68% of the total US market VC funding.

These companies spearhead venture fundraising, attracting a disproportionate percentage of the total funding. As and when they move into the public sphere, the total value of private funding will inevitably fall away. Their influence may not die with them as the model for backing AI start-ups and achieving an IPO exit at a very substantial valuation will encourage funds and LPs that the process can be repeated.

The issue is whether there are successor companies out there that will absorb the scale of funding taken by the big three. There are a few candidates out there, but they appear unlikely to raise at the same scale.

Project Prometheus: Jeff Bezos’ AI startup has a strong appetite for capital. The company kicked off proceedings with a $6.2bn raise in November 2025. A further $10bn followed in April 2026 in a round led by JP Morgan and Blackrock which valued the company at $38bn. Project Prometheus is training models on real-world experimental data, robotic interactions, and engineering workflows, targeting industries including aerospace, automotive, advanced manufacturing, and drug discovery.

Waymo: The autonomous vehicle company Waymo has substantial expansion plans with the intention to launch services in 2026 in Dallas, Denver, Detroit, Houston, Las Vegas, Miami, Nashville, Orlando, San Antonio, San Diego, and Washington as well as the first international services in London and Tokyo. Originally owned by Alphabet, external capital has been progressively introduced with successive raises of $2.5bn, $3.5bn and, in October 2024, a $5.6bn Series C valuing the business at $45bn. In February this year it raised a further $16bn at a $126bn post money valuation in a round led by Alphabet, Dragoneer, DST Global, and Sequoia and including significant investments from Andreessen Horowitz and Mubadala although Alphabet remains the ‘majority investor.’.

Databricks: The data intelligence platform raised $10bn in a Series J in December 2024 at a valuation of $62bn, the largest raise of that year. It had a modest $1bn internal Series K in September 2025 followed by a more substantial December 2025 Series L for $4bn at a $134bn valuation. In February 2026 the company raised another $5bn in equity and $2bn in debt backed by JPMorgan Chase, Goldman Sachs, Morgan Stanley, the Qatar Investment Authority, and Microsoft.

Annualised revenue was $5.4bn in the January quarter up 65% yoy, implying a c25x sales multiple. The company now claims to be FCF positive, and the CEO has talked about an IPO “when the time is right.”

Scale AI’s $14bn raise in June 2025 introduced Meta as a 49% shareholder implying that the data labelling business may not necessarily pursue private markets for further large raises.

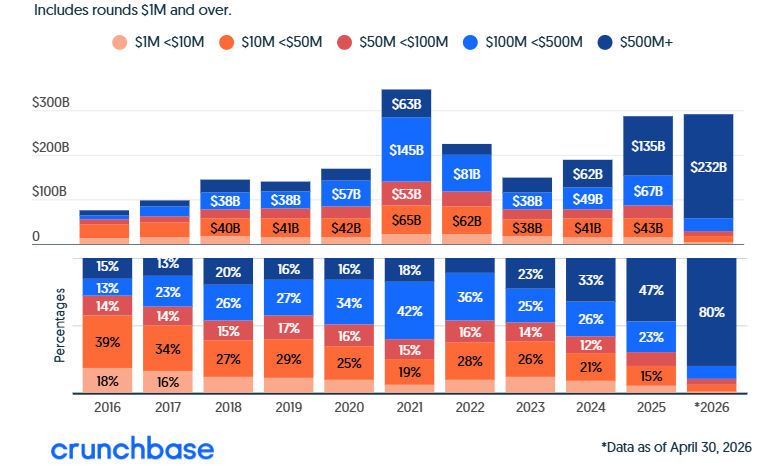

A couple of interesting charts from Crunchbase to show how the US VC market might look shorn of SpaceX (xAI), OpenAI and Anthropic.

The first chart illustrates how the last couple of years have seen the US VC market disproportionately boosted in scale by deals of more than $500m. In Crunchbase’s calculation such deals took 33% of the value in 2024, 47% of the value in 2025 and 80% of the ytd 2026 value. Back at the market peak in 2021 such deals were just 18% of the total.

US Venture Deals by size range and percentage 2016-April 2026

Source: Crunchbase

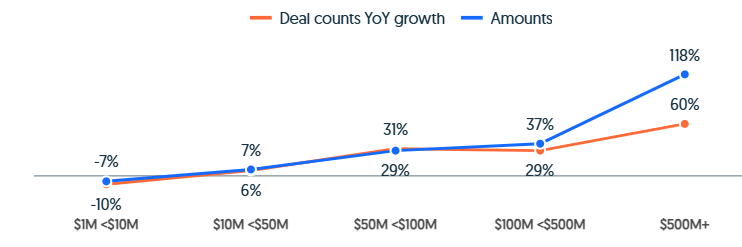

The second chart looks at the yoy growth in 2025 by size of deal and number. It shows that deal amounts and numbers were relatively static yoy at the >$50m level; grew yoy by roughly a third in the mid-range (up to $500m), while the big growth, 118% in amounts and 60% in deal counts, was in the $500m plus deals.

Projecting forward: A 2027 chart ex the ‘big three’ might see the growth in the $500m plus range reversing while the mid and smaller size deals would maintain a similar trajectory. This would imply a declining total deal value relative to 2025 and 2026.

US 2025 yoy VC funding growth by deal size and count

Source: Crunchbase - https://news.crunchbase.com/venture/data-capital-concentrating-faster-startups-100m-ai/

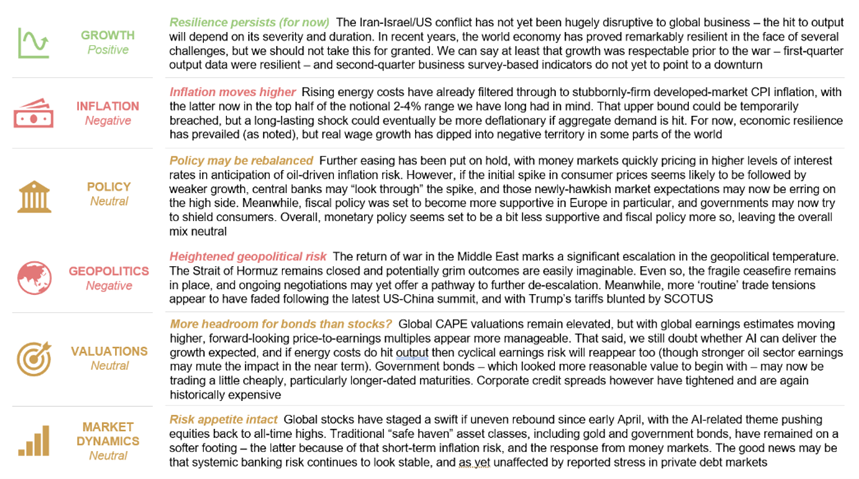

Public markets - Earnings, jobs and interest rates

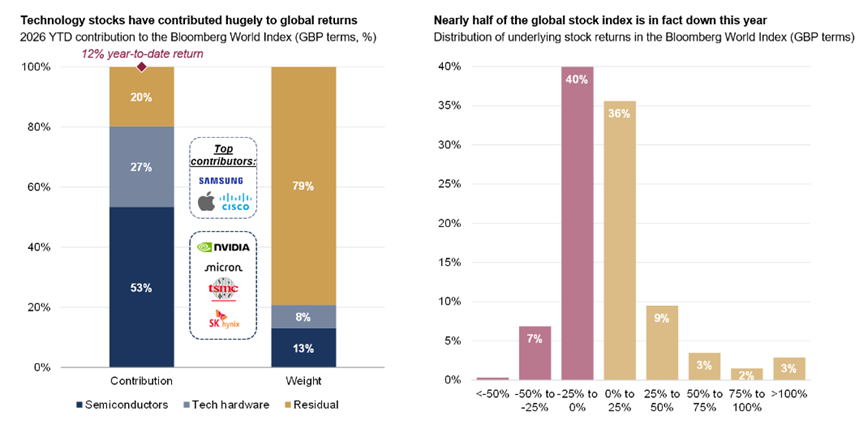

The market rally since the end of March continues. President Trump’s recent declaration on peace negotiations with Iran that they are ‘very boring. I really don’t care. I couldn’t care less’ appears to reflect an insouciance shared by public markets. Since the end of March, NASDAQ is up 28% and the S&P 500 by 19%. In May the two markets were up 9% and 5% respectively.

May was a lopsided month. A big rally in tech stocks produced the bulk of the S&P returns with all the top 10 S&P 500 performers being tech stocks. Within tech, software has rallied but the star performer has been semiconductors. Only Healthcare and Consumer Discretionary in the other sectors were in positive territory – all the rest fell.

Indeed, this has been the story year to date. Tech has contributed 80% of the returns for global markets ytd. Almost half of all stocks have fallen.

Source: Rothschild & Co, Bloomberg, MSCI - “Semiconductors” and “Tech hardware” are sectors within the Bloomberg World Index

Geographically, after a stronger start, European markets have lagged. Both the FTSE 100 and the STOXX 600 barely moved in May. Since the market rally started at the end of March the FTSE 100 is up just 2% while the STOXX 600 is up 7%. Both are up c4% ytd.

The FTSE Venture Capital Index has rallied 23% since the end of March but is still down 6% ytd largely reflecting the sell- off in the software sectors caused by AI fears.

The oil price has continued to drift off. WTI crude has retreated from its peak levels of c$113 per barrel, has been below $100 since mid-May and is presently hovering at c$93.5 albeit still substantially above the c$60 per barrel it traded at through the first quarter of 2026.

There is almost inevitably a price to pay for the Iran War in higher inflation. The full effects are yet to be felt. US headline inflation, which was 2.4% in February, jumped to 3.3% in March and then 3.8% in April. May’s figure is expected to come out at 4.1%. One year ahead inflation expectations in the US are running at c3.6%- 4%, well ahead of the Fed’s 2% target.

The US jobs market is doing surprisingly well. This, and other signs of a robust US economy, lean against the prospect of rate cuts and instead in favour of them rising. The unknown factor is the likely response of Trump’s new head of the Fed, Kevin Warsh who is being recast as more of a hawk on interest rates than his appointment by President Trump might suggest.

Warsh may certainly make the analysts work harder. The indications are that he does not favour the Fed signalling forward the likely direction of interest rates. Commentators, deprived of the Fed’s forward guidance language and with the removal of the dot plot publication on the expected direction of rates, will be scrambling to form a consensus on likely future rate decisions. Kevin Warsh is quoted as saying

“Unlike many of my colleagues past and present, I don’t believe in forward guidance. I don’t believe that I should be previewing for you what a future decision might be.’’

This process could start with the next Fed meeting on June 17. The market remains clear that rates will be unchanged at 3.5%-3.75% at that meeting with FedWatch giving just a 4% chance of a rate cut.

The prospect of the next move being a rate increase has strengthened. By the December 9th meeting FedWatch now has a 51% chance of a rate rise, a 47% chance that rates will be unchanged and just a 2% chance of a fall. Last month the outlook for that meeting was a 20% chance of a rise, 74% for unchanged rates and a 6% chance of a fall.

US market strength remains bolstered by strong earnings expectations. A good Q1 results season was driven by technology stocks and the AI infrastructure boom benefitting semiconductor companies, tech hardware, industrials and utilities companies. Some estimates put beneficiaries of AI infrastructure as accounting for half of likely total S&P 500 earnings growth in 2026 and 2027.

Earnings growth forecasts have been revised up post Q1 with updated expectations looking for 2026 earnings growth of c23%-25% with 2027 growth seen around 15%. The latest to revise up its year end S&P 500 target is Goldman Sachs which now looks a year-end 2026 target of 8000, up from 7600.

2026 earnings growth expectations of c23%-25% are well above the start of the year forecasts of c13-15% pa. It means that, despite the advance in markets since the start of the year, commentators can argue that valuations are still justified. The S&P 500 currently trades at c21x forward earnings. This is high by historic standards, ranking in the 88th percentile relative to the past 40 years. The typical scenario seen by analysts for this year is that the multiple does not expand but remains steady, while the market is borne along by earnings growth.

Into the mix comes the SpaceX IPO. The company is looking to raise an initial $75bn, potentially rising to $86bn, at a valuation of $1.78 trillion, at a multiple of over 90x annual revenues. It will be the largest IPO in history, dwarfing the previous holder of that title, the $25.6bn 2019 Saudi Aramco IPO.

Retail demand for SpaceX is expected to be strong with up to 25% of shares being reserved for such investors. As for the institutional market we observed in our last Growth Equity Update the impact of two key interlinked changes to the NASDAQ listing rules introduced in May - no minimum free float and fast index inclusion – which are likely supportive for the prospects of major tech related IPOs in 2026/27.

The changes mean that new ‘mega’ IPOs are fast tracked into index inclusion even if less than 10% of stock is sold. In the case of SpaceX about 5% is being sold. Even with this slim free float the company will be ‘overweighted’ by a factor of 3x, meaning an index weighting of 15%.

This creates a natural ‘shortage’ of stock for passive investors who are c40% of funds under management. By their nature they do not take part in price formation, buying shares only after they have entered the relevant index.

Critically the active investors will not have to wait long for the passive buying pressure to emerge. After just 15 trading days the passive funds will need to come in and buy stock.

This potentially creates an incentive for active funds to bid aggressively in the IPO for stock with the knowledge that a subsequent spike in the share price will be met by ‘forced’ passive buying of a stock in natural short supply just 15 days later.

It will be interesting to see the effect of the SpaceX IPO on broader markets. After a dearth of major IPOs in recent years there should be sufficient capital to absorb the issue although there may be some reallocation of portfolios to accommodate it.

European markets, more exposed to oil shock effect from the Iran conflict and with less weighting towards the AI effects that are driving the US market, have reverted to underperforming the US market.

Rising inflation remains a concern. Euro area inflation which was 1.9% in February reached 3.2% in May driven by higher energy and services prices. Energy costs rose 10.9%. Core inflation, which excludes food and energy prices, rose by 0.3 percentage points to 2.5%.

European interest rates are still at 2% but the expectation is that rates will now likely rise for the first time in almost three years. The market is pencilling in a 95% chance that interest rates will rise by 25bps at the June meeting with one further 25bps rise anticipated by the year end.

UK inflation was 3.3% in March up from 3% in February but fell back to 2.8% in April beating analyst expectations of a 3% rise. The slowdown comes because of the implementation of a new energy price cap, offsetting pressures from rising energy prices. That cap though runs out in July with Ofgem having already announced a 13% increase in the cap from July. Nevertheless, although inflation is forecast by the market to c3.7% by the end of the year, this is lower than previous expectations of a rise to 4%. Inflation is then expected to fall back to c2.5% in 2027.

The OECD meanwhile has edged up its UK GDP growth forecast for 2026 to 0.9% from 0.7% previously while lowering 2027 growth from 1.3% to 1.1%.

The governor of the Bank of England has softened his tone on the potential for higher interest rates. He observed at the end of April that ‘higher inflation is unavoidable’ as a result of the conflict in the Middle East. In late May though he indicated that higher inflation caused by the Iran energy shock is potentially tolerable if it is a temporary effect saying

“Given the context of softness in the real economy and uncertainty around the scale and duration of the shock, tolerating temporarily above-target inflation to provide some support for the real economy is an appropriate way to approach the trade-off [between inflation and activity]… that tolerance would weaken if signs of second-round effects begin to emerge.”

The expectation remains that the Bank of England is likely to raise interest rates by the end of the year, but the consensus expectation has now moved to just one 25bps rise, taking the rate to 4%, rather than two.

Our Rothschild & Co strategists Kevin Gardiner and Anthony Abrahamian’s views on the current market outlook are summarised in the Exhibit.

Source: Rothschild & Co

Fundraising outlook: c$19bn of impending raises

Pipeline is c$10bn in impending US deals and c$9bn in Europe

Two things have conspired to reduce our impending deals total from $82bn at the end of April to c$19bn by the start of June. The first factor is the announcement of Anthropic’s incremental $50bn raise ($65bn in total with the $15bn from Google/Amazon announced last month). The second is a spring clean of some of the older impending deals on our list, some of which may yet go ahead and others of which appear to have fallen by the wayside.

As well as Anthropic, Anduril falls out of the impending list having completed a $5bn raise. The AI semiconductor business Cerebras eschewed a further private raise and went instead for an IPO with the $5.5bn proceeds exceeding the value of the rumoured $3bn private raise. Our spring clean meanwhile has removed for now the putative Tether raise, cited most recently at $5bn.

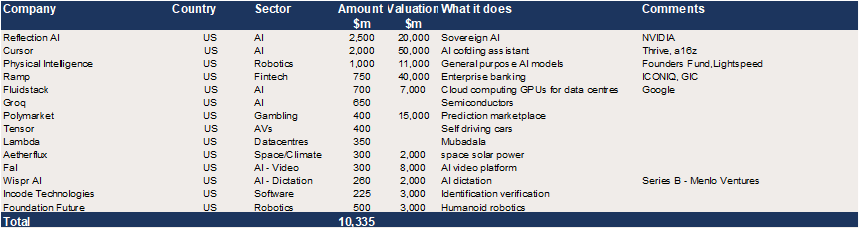

Leading the revised list is Reflection AI which provides tools to create personalized AI that can chat and interact like a person. The NVIDIA backed business is looking to raise $2.5bn at a $20bn valuation.

Coming on to the list is the AI coding assistant business Cursor AI which is said to be looking to raise $2bn at a c$50bn valuation with the round led by a16z and Thrive Capital. The company last raised $2.3bn at a $27bn pre money valuation in November 2025 which in turn followed a $900m raise at $9bn pre money in June 2025.

Also arriving on the list are the fintech Ramp, reportedly seeking a $750m raise at a $40bn valuation having raised $300m at a $32bn post money valuation in November last year, and the AI semiconductor business Groq which is reportedly raising $650m from existing investors including Disruptive and Infinitium. WisprAI is in talks with Menlo Ventures to raise $260m at a $2bn valuation for its voice dictation platform, up from its last mark of $700m in November 2025.

US Growth Equity - c$10bn in reported upcoming raises

Source: Rothschild & Co; press reports

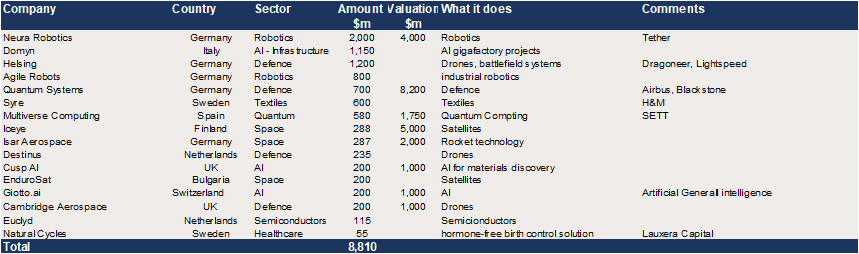

In Europe the total of identified impending raises roses from $7.8bn to $8.8bn.

This is despite us removing the potential $2bn raise for the French AI coding business Poolside which was to have been led by Magnetar and NVIDIA. Press reports suggest the raise has been suspended after a partnership with CoreWeave for a 2GW data centre in Texas fell through.

The completion of its $240m round in May means that semiconductor business Fractile also comes off the list.

Heading the list are Germany’s Neura Robotics, whose humanoid robot has consumer and industrial applications, and which is looking to raise $2bn at a $4bn valuation and Italian LLM and AI infrastructure business, Domyn, said to be raising $1.15bn in an upcoming Series B.

Entering the list are two European defence businesses led by Helsing, reportedly looking for a $1.2bn raise in a deal led by Lightspeed and Dragoneer. Germany’s Quantum Systems, which is a developer of drones for defence and security operations is raising $700m at an $8.2bn valuation in a round said to be led by Airbus and Blackstone.

Multiverse Computing, a Spanish quantum business looking to raise $580m at a $1.75bn valuation supported by SETT, is another newcomer to the list. The Bulgarian satellite business EnduroSat is looking to raise $200m some six months after it raised $104m.

European Growth Equity - c$8.8bn in reported upcoming raises

Source: Rothschild & Co; press reports

Fundraising - Records continue to fall

Another $69bn raised in the US in May and $6.3bn in Europe

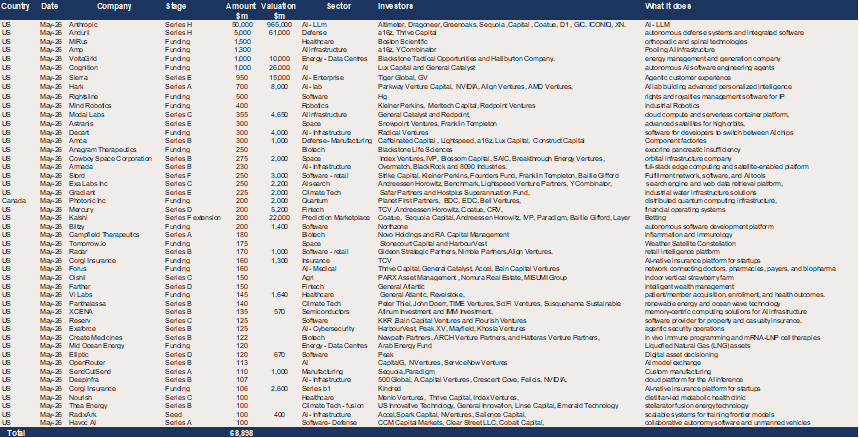

And on the fundraising carousel goes. In the US May produced total VC fundraising of $69bn across 47 rounds. Incredibly this is only the second highest total of the year after the $181bn raised in February. It was the second largest month ever though for US VC raises beating the $50.7bn of March 2025. All three of these months were characterised by substantial raises for LLM businesses. March 2025 had what now looks like a relatively modest $40bn raise for Open AI at a $300bn valuation. February 2026 had a $110bn raise for the same company at a $730bn valuation (topped up in March 2026 by a further $12bn at a $850bn valuation). May saw Anthropic announce a $65bn raise at a $965bn valuation. This includes the $15bn ($10bn Google, $5bn Amazon) already announced in April - so we record it as a $50bn new raise in our Monitor. The round was supported by a star line up of funds including Altimeter, Dragoneer, Greenoaks, Sequoia, Capital, D1, GIC, ICONIQ and XN.

US funding to end May 2026 at $350bn exceeds the sum of 2024 and 2025 fundraising by $6bn. The Anthropic fundraising dwarfed what was otherwise a notable raise, a $5bn round by defense tech Anduril. Overall, the $68.9bn May total was 6.6x the $10.5bn raised in May 2025. It brings the ytd US total fundraising to $350bn, 5x more than was raised by end May 2025. Indeed, the c$350bn raised ytd is $6bn more than the total raised in the sum of 2024 ($110bn) and 2025 ($234bn). There are seven months still to go in the year.

Albeit on a different scale Europe enjoyed another strong month in May with total fundraising of $6.3bn across 60 deals. It was a 67% yoy advance versus the $3.8bn of May 2025. Year to date fundraising in Europe is 74% ahead of 2025 at $30.2bn (vs $17.4bn).

US & Canada - 67 raises of $100m and above in May for a total of $68.9bn

Source: Rothschild & Co

Last month we wrote about the remarkable sequence for US VC fundraising which in the eight months since September had seen only one month, December, fall short of $20bn of monthly fundraising with an average monthly total of $47bn. May more than kept up the sequence with $70bn raised, meaning the last nine months average is a whisker short of $50bn.

As ever these days AI dominated the total with $55.7bn of the $69.9bn raised, 80% of the total - the same percentage as in April.

Heading the list is the new raise by Anthropic, typically reported in the press as a $65bn raise at a pre- money valuation of $900bn. In our May Monitor we record this as a $50bn new raise as we incorporated the deals struck by Anthropic with Google and Amazon as an element of our April total when those deals were first announced. Thus, the total $65bn deal breaks into three parts:

Google- $10bn: In April Google agreed to invest up to $40bn in Anthropic, with $10bn up front and $30bn contingent on performance. We reflected the $10bn in our April number and are yet to reflect the $30bn. Anthropic struck a deal with Google in early May in which it committed to spend $200m with Google Cloud over the next five years.

Amazon -$5bn: In April Amazon agreed to invest $5bn up front in Anthropic with a potential $20bn to follow over time. We reflected the $5bn in our April Monitor and are yet to reflect the $20bn. Anthropic in turn committed to spend $100bn on 5GW of computing resource from Amazon on which to train its AI models, including Trainium, Graviton and the upcoming Trainium 3 chips.

Further $50bn: Anthropic in May confirmed it had raised a further $50bn at a valuation of $900bn, neatly exceeding the $850bn valuation of OpenAI in its March funding round. The round was led by Altimeter Capital, Dragoneer, Greenoaks and Sequoia Capital. The valuation is up from $350bn in the $30bn Series G raised in March this year in the round supported by Coatue, Dragoneer, Founders Fund, GIC and Iconiq.

Anthropic is claiming run rate revenues in May (i.e. May’s revenues annualised) of $47bn and in turn claims that this has risen by five times since the start of the year – implying run rate revenues in December were sub $10bn. The valuation is implied at 19x run rate sales.

This may be the last private raise by Anthropic. On June 1st the company announced that it had submitted a draft registration statement on Form S-1 to the U.S. SEC for a proposed IPO. ‘This gives us the option to go public after the SEC completes its review. The proposed initial public offering will depend on market conditions and other factors.’

There were three more c$1bn AI related raises in May. Amp aims to buy up spare capacity in AI infrastructure to pool it and make it available to start ups, universities and other organisations otherwise starved or priced out of AI infrastructure. It raised $1.3bn in a round led by a16z and Y Combinator. Cognition carried out its long-awaited round, a $1bn raise led by Lux Capital and General Catalyst at a valuation of $26bn. Devin, the company’s autonomous software engineer, has led the company to a c$492m annualised revenue run rate (so 53x run rate sales). Sierra raised $950m at a $15.8bn valuation led by Tiger Global and GV. The business sells customer service agents and has a ‘paid-by-action’ model. Run rate revenue are $150m (10.5x sales run rate) up from $100m in November 2025.

Outside AI the second largest sector was Defense with $5.2bn raised, albeit in just two funding rounds. Anduril raised a $5bn Series H at a $61bn valuation led by a16z and Thrive Capital. Anduril has emerged as the leading VC backed new defense business with a new approach to defense production.

‘Across offense and defense alike, producibility and software-defined evolution are foundational requirements. Systems must be designed from the outset to be manufactured in quantity, fielded rapidly, and upgraded continuously in theatre. Hardware cannot be frozen at deployment. Software cannot be locked into multi-decade refresh cycles. Production capacity, upgrade velocity, and supply-chain resilience are core elements of system design, not downstream considerations.

This is the unifying logic of our portfolio. Platforms extend reach and mass. Sensors and software create targeting advantage. Defensive and counter-targeting systems preserve survivability. Lattice binds them together. All of it is designed for speed, scale, and adaptation.’

There were three Healthcare raises for a total of $1.75bn led by the $1.5bn raised by MiRus, an orthopaedic and spinal technologies expert led by Boston Scientific. There was a pick-up in software raises in the month coinciding with the 30% rally in the S&P Software and Services index since the start of April. There were seven rounds which in total raised just short of $1.5bn. The largest of these was $500m of funding by Hg for Rightsline, a business handling rights and royalties management software for intellectual property.

We have been following the emergence of the prediction market places Kalshi and Polymarket since their flurry of raises in 2025. Kalshi raised another $200m in May in a deal led by Coatue Management which valued it at $22bn. This was its third raise in a year. Counterpart Polymarket is said to be considering a further $400m raise at a valuation of $15bn.

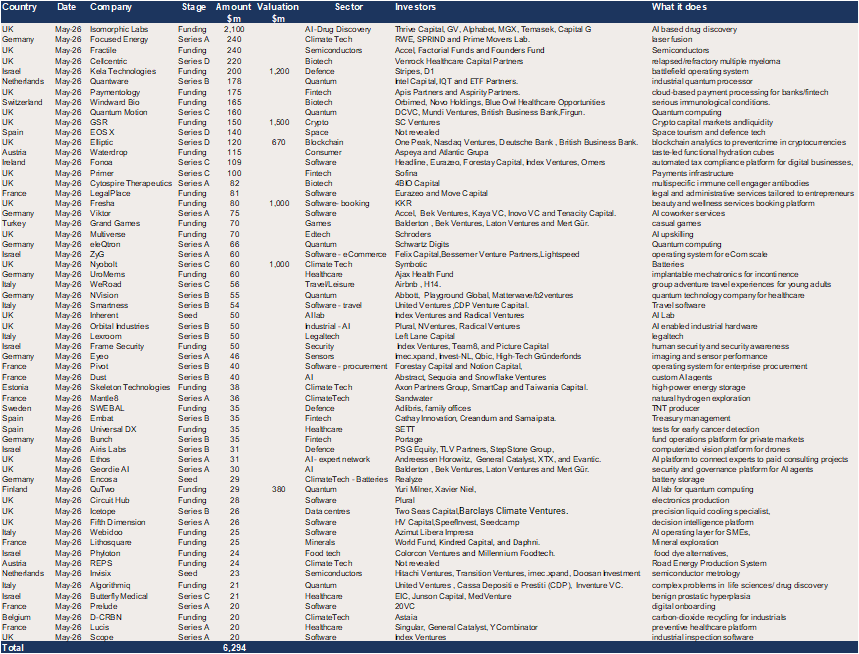

In Europe there were 15 deals of $100m or more in May. The largest of these was the $2.1bn for the AI powered drug discovery business, Isomorphic Labs. The deal was led by a who’s who of AI raise backers including Thrive Capital, GV, Alphabet, MGX, Temasek and Capital G. The UK Sovereign AI Fund also participated. Isomorphic Labs comments that ‘The new capital will be used for the continued development and deployment of Isomorphic Labs’ AI drug design engine (IsoDDE), accelerating and expanding its pipeline of therapeutic programs towards the clinic.’

In total AI deals raised $2.25bn in the month, 36% of the total, another illustration of the greater diversity of European fundraising than in the US.

The second largest European category in May was Software with twelve deals raising $618m of which the largest was the $109m raise for Irish business Fonoa, an automated tax compliance platform for digital businesses. The Series C funding round was led by Headline.

It was a strong month for Quantum raises with six rounds raising a total of $509m. The largest of these was the $178m raise by QuantWare of the Netherlands. It produces quantum processing units encompassing VIO-40K™, a quantum processor architecture for 10,000 qubits, 100x larger than today’s state of the art. QuantWare has shipped to more than 50 customers becoming the world’s largest commercial QPU supplier by volume. Its customers span quantum computing companies, national technology institutes, and major global tech companies. The round was led by Intel Capital, IQT and ETF Partners with existing investors including FORWARD.one and Invest-NL Deep Tech Fund, InnovationQuarter Capital, Ground State Ventures, and Graduate Ventures.

The UK’s Quantum Motion meanwhile raised $160m in a round led by DCVC, Mundi Ventures, the British Business Bank and Firgun. Quantum Motion describes itself as the leading company in silicon transistor-based quantum computing. The theory behind Quantum Motion is that the multi -megawatt power demands of quantum computing are unsustainable. Quantum Motion’s silicon transistor-based approach instead enables delivering utility-scale systems with 100-fold reduction in cost and space requirements, and 1,000-fold reduction in energy consumption compared to alternatives.

Three big raises (Cellcentric $220m, Windward Bio $165m and Cytosphire Therapeutics $82m) saw Biotech raises a total $467m. This was just ahead of the $447m raised in seven deals for Climate Tech. The largest of these was the $240m Series A led by RWE, SPRIND and Prime Movers Lab for laser fusion business Focused Energy in a deal advised by Rothschild & Co.

Europe – 60 $20m+ deals raised $6.3bn in May

Source: Rothschild & Co

Our views on the state of the venture capital markets

This revival of the growth equity market has been led by the US and by a surge of interest in artificial intelligence model providers and for companies using AI to transform a range of underlying industries.

At the same time the venture industry has re-adopted strong underlying approaches to investment with companies in most sectors striving to achieve a better balance of growth, profitability and cash flow. The underlying quality of the cohort of VC backed companies has improved.

Our summary of the outlook

▪ There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, quantum, semiconductors, new energy sources like nuclear and fusion) supporting the development of AI.

▪The influence of AI is percolating through many other industries such as drug discovery, defence, robotics, legal tech, autonomous vehicles, and cybersecurity fuelling a broader advance in the growth equity market.

▪ Overall, the VC market is regaining confidence with the strength of interest with fintech, blockchain/crypto and biotech reviving strongly.

▪ There is a burgeoning interest in defence industries from investors with both the tense geopolitical political environment, the advances in AI applications and the experience of the combat in Ukraine contributing to investor focus. By contrast, ClimateTech, while still a substantial sector has become less prominent both as a result of some high-profile failures and being less favoured politically in the US under the current administration.

▪ Fund raising for venture capital firms remains subdued. Fund raising is concentrating into larger, established firms. US VC fundraising in 2025 was concentrated in larger firms and at near decade lows.

▪ The speed of the investment process has slowed down since 2021-22. The level of diligence on deals has stepped up. This is true even in the ‘hot’ parts of the market like AI. Outside these areas it is marked – processes take time, downside protection is sought.

▪ Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on the combination of growth and profitability (or a rapid path to it) and on free cash flow.