Stocks pause for breath

Investment Communications Team, Investment Strategy Team, Wealth Management

Summary

Global equities fell by 2.2% in October (USD terms), while global government bond returns declined by 1.2% (USD, hedged terms). Key themes included:

- Stock markets retreat as government bond yields surge;

- Economic resilience persists, with inflation modestly above target in most regions;

- Geopolitical risk intensifies in the Middle East, Ukraine and Taiwan.

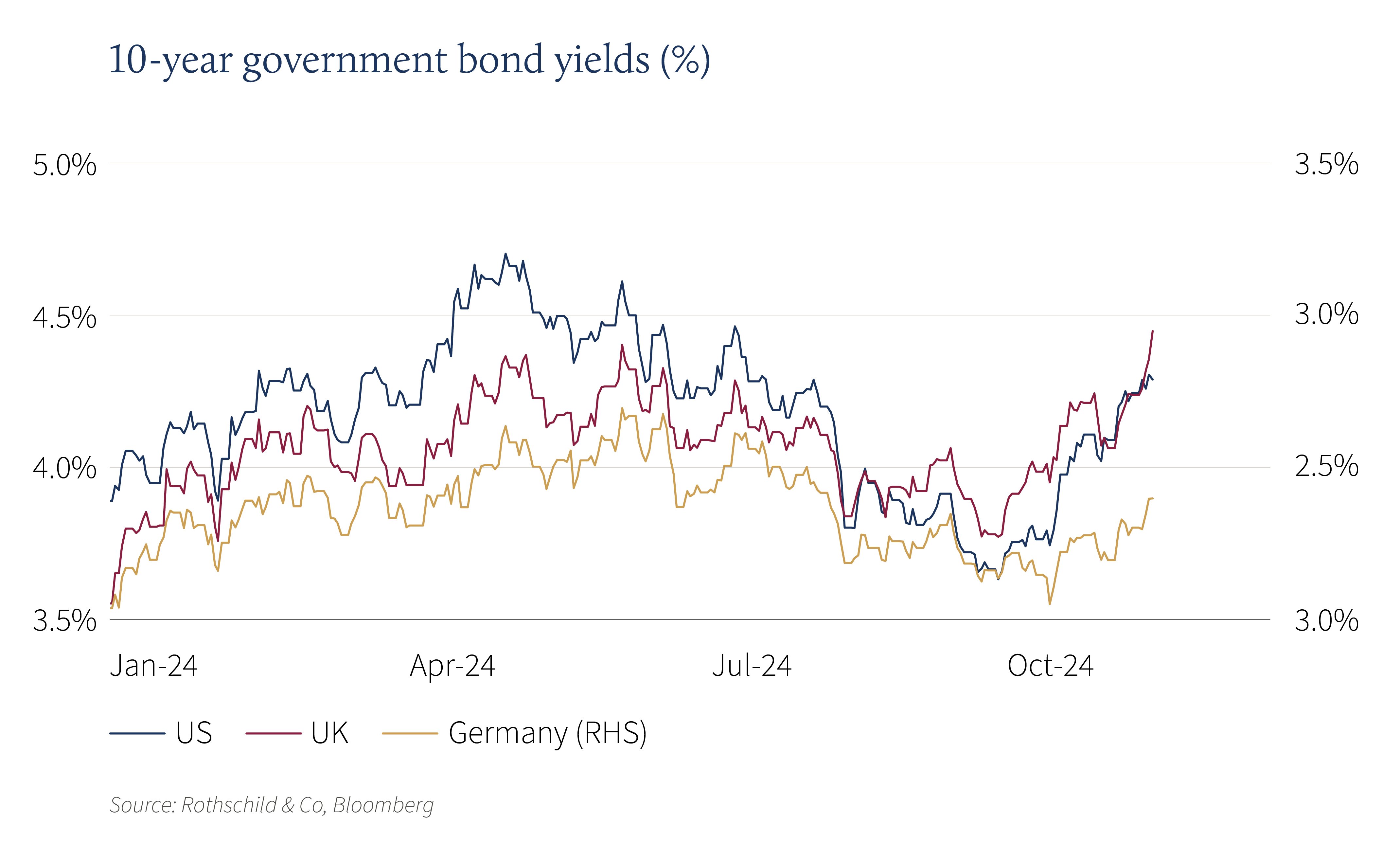

Markets: Broad-based weakness

Stock and bond volatility picked up in October, despite global stocks briefly notching a new high mid-month. US stock market momentum faded, but weakness was most visible outside North America – partly exacerbated by the impact of the strong dollar (on a common currency basis). Japan was the only major region to report positive gains in local currency terms, coincidentally as stimulus-driven momentum in China faded. In fixed income, government bond yields surged across the US and Europe. Notably, the 10-year UK gilt yield rose to a 12-month high of 4.5%, after the new government unveiled net fiscal loosening in their first budget. In commodities, Brent Crude oil remained at the lower end of recent trading ranges, despite heightened geopolitical risk. Meanwhile, gold continued to hit fresh highs in US dollar terms. Finally, third-quarter earnings growth was tracking at close to 10% (y/y) for the S&P 500 companies, according to Bloomberg (after more than 60% of stocks had reported their results).

Economy: Healthy growth-inflation mix persists

US third-quarter activity expanded by 0.7% (q/q) – marking the tenth consecutive quarter of economic growth – underpinned by the US consumer. US labour market developments were mixed: jobless claims fell anew and the unemployment rate held steady, though the pace of job gains slowed dramatically amid weather-related disruption. Meanwhile, inflation continued to moderate: the US Federal Reserve’s inflation target, the core PCE deflator, slowed to an annualised rate of 2.2% in Q3. In Europe, euro area GDP expanded by 0.4% in the third quarter, its strongest reading in two years. UK activity momentum also continued, after monthly GDP expanded in August and retail sales remained firm in September. Eurozone inflation data were stronger-than-expected in October, though headline inflation was still subdued, at 2%. UK inflation was conversely on the softer side (in September) and Swiss inflation remained muted. Elsewhere, China’s third-quarter GDP was tracking just below the government’s 5% growth target. There was only a modest rebound in the October business survey data after authorities’ initial stimulus measures.

Policy and politics: Less easing ahead? | Conflict intensifies

Amid the resilient growth backdrop, money market rate cut expectations moderated in October, with only one further (0.25 percentage point) rate cut fully priced-in for the Federal Reserve and Bank of England this year. Meanwhile, the European Central Bank reduced its deposit rate again to 3.25%, with markets expecting another cut in 2024. On fiscal policy, Labour’s first budget revealed higher taxes and spending for the UK, with a net increase in borrowing relative to previous policies. Conversely, on the other side of the channel, France PM Barnier’s proposals focused on spending cuts and tax increases for corporations and the wealthy.

Geopolitical uncertainty increased, notably in the Middle East following direct exchanges between Iran and Israel (although, the former’s energy infrastructure was not targeted). China continued its intimidation of Taiwan, holding military drills around the island, while North Korea reportedly sent troops to fight with Russia. The outcome of the US presidential election loomed large, though the very tight opinion polls and betting odds tilted modestly in Trump’s favour. Finally, In Japan, the incumbent Liberal Democratic Party’s decision to call an early election backfired, as the coalition lost its majority.

Performance figures (as of 31/10/2024)

| Equity (MSCI indices $) | Month | Year |

|---|---|---|

| Global | -2.2% | 16.0% |

| US | -0.8% | 20.4% |

| Continental Europe ex. Switz. | -6.1% | 5.5% |

| UK | -5.5% | 9.1% |

| Switzerland | -5.5% | 4.4% |

| Japan | -3.9% | 8.0% |

| Pacific ex Japan | -6.3% | 7.8% |

| EM Asia | -4.6% | 16.0% |

| EM ex Asia | -3.9% | -3.6% |

| Fixed income | Yield | Month | Year |

|---|---|---|---|

| Global Govt (hdg $) | 3.14% | -1.2% | 2.5% |

| Global IG (hdg $) | 4.67% | -1.6% | 3.6% |

| Global HY (hdg $) | 7.47% | -0.1% | 9.5% |

| US 10Y ($) | 4.29% | -3.3% | 0.6% |

| German 10Y (€) | 2.39% | -2.0% | -0.7% |

| UK 10Y (£) | 4.44% | -2.8% | -2.9% |

| Switzerland 10Y (CHF) | 0.41% | 0.1% | 3.0% |

| Currencies (NEERs) | Month | Year |

|---|---|---|

| US Dollar | 2.8% | 4.7% |

| Euro | -0.1% | 1.3% |

| Pound Sterling | -1.4% | 3.9% |

| Swiss Franc | 0.0% | -0.7% |

Table note: NEERs under ‘currencies’ are the JP Morgan trade-weighted nominal effective exchange rates

| Commodities ($) | Level | Month | Year |

|---|---|---|---|

| Gold | 2,744 | 4.2% | 33.0% |

| Brent Crude oil | 73 | 1.9% | -5.0% |

| Natural gas (€) | 41 | 4.0% | 25.5% |

Source: Bloomberg, Rothschild & Co.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.