ESG insights for 2025 and beyond

2025 finds the Environmental, Social and Governance (ESG) investment landscape in transition, shaped by shifting policies, mixed fund flows, and continued technological progress. While political headwinds have created uncertainty in some markets, structural trends—ranging from regulatory tightening to clean energy momentum—signal a deepening commitment to sustainable finance.

At Rothschild & Co Wealth Management Switzerland, we recognise that differing interpretations of regulatory developments and ESG trends may coexist within the industry. This publication reflects our current perspective on the evolving ESG landscape.

What does the current investment landscape look like?

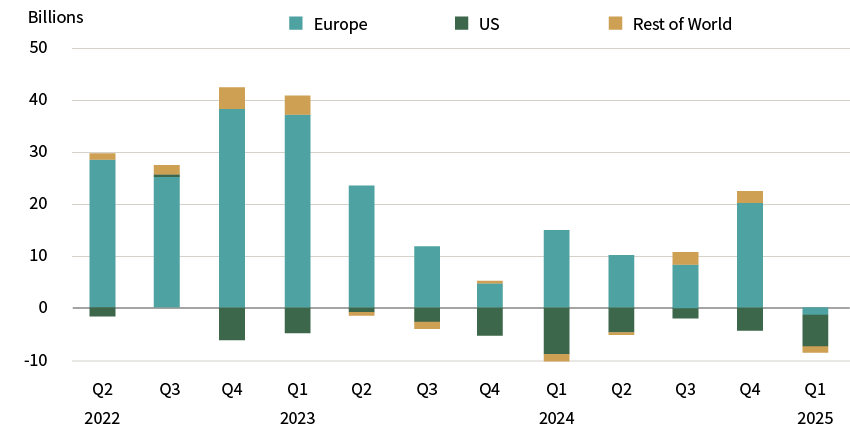

The global sustainable fund universe[1] endured its worst quarter on record in the first quarter of 2025, registering net outflows of USD 8.6 billion. This marked a sharp reversal from the USD 18.1 billion in restated inflows seen in the final quarter of 2024 (Chart 1).[2]

Despite record outflows, global ESG fund assets remained steady at USD 3.16 trillion as of March 2025. The main driver of first-quarter outflows was a wave of modest, yet notable, redemptions in Europe—marking the first time since at least 2018 that European sustainable funds saw net outflows, even as conventional funds attracted strong inflows. This reversal reflects several interlinked factors.

Geopolitical tensions, including the return of President Donald Trump, have shifted Europe’s focus away from climate goals towards economic growth, competitiveness, and defence. Trump's anti-climate stance and policy actions—such as an executive order targeting diversity and inclusion—have introduced legal uncertainties, leading US asset managers to scale back global ESG promotion. For some European investors, this retreat has raised doubts about global alignment on sustainability, further complicated by evolving EU regulations and persistent underperformance in sectors like clean energy. Together, these dynamics appear to have dampened broader market appetite for ESG strategies.

Chart 1: Annual global ESG fund flows (USD billion)

Source: Morningstar Direct. Data as of December 2024

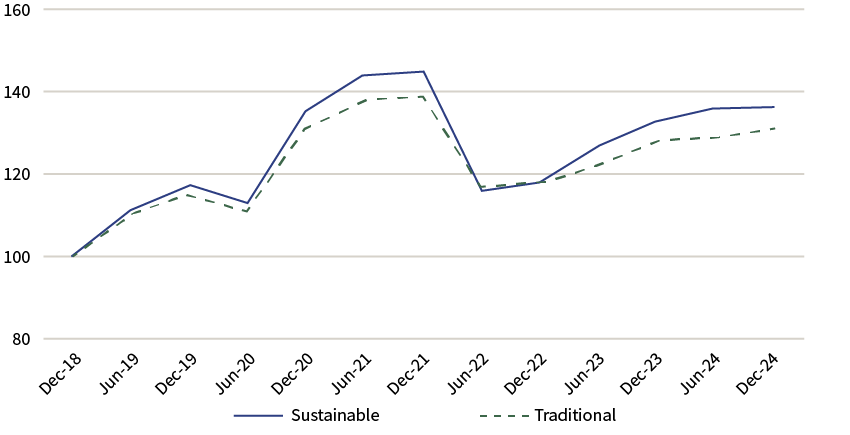

Looking at performance, however, over the longer term, sustainable funds have outperformed their traditional counterparts. An analysis of Morningstar data shows that a hypothetical investment of USD 100 in a sustainable fund in December 2018 would have grown to USD 136 by today, compared to USD 131 for a traditional fund over the same period (Chart 2).

Chart 2: Long term performance (Dec. 2018 = $100)

Source: Morgan Stanley Institute for Sustainable Investing analysis of Morningstar data as of 4 Feb 2025.

This underscores the ability of ESG-integrated investments to remain competitive over time, even amid market fluctuations.[3]

How are regulations shaping the ESG landscape?

Regulatory divergence has become a defining feature of the global ESG framework.

- In the United States, a shift in federal leadership at the beginning of 2025 has led to a rollback of various climate-related initiatives, including a pause in SEC climate disclosure rules and an exit from the Paris Agreement. ESG policies are now largely state-driven.

- In Europe, supporting the transition and fighting greenwashing remain key priorities. However, regulators are currently revisiting the CSRD framework to reduce compliance burdens, potentially leading to i) a significant cut in the scope of companies subject to the regulation and(ii) standards simplification with fixed and fewer data points to report on.On the other hand, the entry into force of the ESMA funds’ name guidelines in May 2025 raises the bar, focusing on the use of ESG or sustainability related terms in funds. It led to 262 Article 8 and Article 9 funds rebranded in Q1 2025.

- The UK’s Sustainability Disclosure Requirements (SDR) pushes for more transparency and clarity integrating both an anti-greenwashing rule and requirements for naming and marketing for asset managers.

- China has taken initial steps toward regulatory alignment, issuing voluntary ESG reporting standards in late 2024.[4] These lay the groundwork for a more comprehensive national ESG framework expected by 2030, in parallel with ongoing growth in green finance.

Across major markets, expectations around financial products disclosure and credibility are rising, and scrutiny of ESG claims is intensifying.

What are the key market trends?

Despite regulatory and political challenges, we continue to see capital flowing into the green transition across global markets. In 2024, global investment in clean energy reached an all-time high of USD 2 trillion, double the level of fossil fuel investment.[5] Renewable energy, electrification, and energy efficiency are now dominant market themes. Solar alone accounted for USD 500 billion of investment, and electric vehicle sales rose to over 17 million units, representing 20% of new car sales worldwide.[6]

Alongside this, mergers and acquisitions have become the preferred route for climate tech exits, with 95% of transactions in 2024 taking this form. Corporates are increasingly acquiring clean energy, mobility, and waste-to-energy firms to accelerate their own sustainability transitions. Notably, major energy companies are reorienting towards low-carbon infrastructure, as demonstrated by ExxonMobil’s USD 4.9 billion acquisition of Denbury Inc., which gained them access to one of the largest CO₂ pipeline networks in the US.[7]

Several of the world’s largest asset managers – including Allianz, Robeco, and Invesco – have also revised their approach. While some are moving away from using the term “ESG” in response to politicisation, their strategies remain focused on climate and social themes. For instance, one leading asset manager[8] has set a target for 75% of its holdings to be aligned with science-based emissions targets by 2030.[9] The broader industry continues to view ESG integration as a core part of long-term risk-return analysis.

What are the sustainable investing themes dominating the market over 2025?

As the ESG landscape evolves, certain structural themes are emerging or being confirmed as prominent investment themes within the sustainable investment landscape. At large, in the market:

Climate adaptation and resilience

With extreme weather events becoming more frequent, investment is growing in companies and infrastructure that enhance climate resilience. These include water management, catastrophe insurance, and sustainable agriculture.

Nature and biodiversity

In line with the Global Biodiversity Framework, portfolios are increasingly allocating capital to sectors that support ecosystem preservation and sustainable land use. Such exposure may help position investors ahead of emerging regulation such as EU biodiversity disclosures and recommendations from the Taskforce on Nature-related Financial Disclosure (TNFD).

Electrification and clean energy

Accelerating the transition to low-carbon energy remains central. Renewables, electric vehicles, and supporting grid technologies continue to benefit from strong policy and investment momentum.

Efficiency and circularity

Energy and resource efficiency offer compelling financial and environmental returns. Investments range from industrial process optimisation and building retrofits to recycling technologies, in line with frameworks like the EU Circular Economy Action Plan.

Emerging technologies

Allocations to early-stage solutions—such as green hydrogen, carbon capture and storage, and advanced battery technologies—can offer high potential but require selective, risk-aware exposure. Interest from corporates and governments continues to grow, which signals future scaling opportunities.

High-performing ESG companies

Exposure to companies with strong governance and sustainability credentials is increasingly perceived by investors with appetite for sustainable investment as providing stability, diversification, and consistent performance, even across different sectors and business models.

Green bonds and sustainable fixed income

The market for labelled bonds has deepened considerably. New regulation, including the EU Green Bond Standard, is expected to further enhance transparency and alignment with the EU taxonomy. As a result, the yield premium (or “greenium”) between labelled and conventional bonds is expected to narrow.

These themes reflect areas emphasised by global climate and biodiversity agreements, including COP28, COP15, and broader net-zero policy frameworks. They allow investors to align their portfolios with long-term sustainability trends while adapting to regulatory and market developments.

What does this mean for investors?

Private clients are increasingly seeking solutions that deliver financial performance alongside measurable sustainability outcomes. Many ESG-integrated strategies in the market are designed to meet this dual objective—capturing upside from the green transition while helping manage long-term risks such as carbon exposure, regulatory disruption, and resource scarcity.

While 2024 highlighted some of the challenges inherent in sustainable investing—particularly political backlash and uneven short-term flows—it also reaffirmed the long-term case for ESG in many parts of the market. Regulatory clarity, technological innovation, and client expectations are all converging to reinforce sustainability as a key consideration of modern portfolio construction.

Looking ahead

The ESG investment landscape is steadily evolving. As it matures, the most effective strategies will be those that combine strong foundations—such as transparency, data integrity, and alignment—with the flexibility to respond to shifting policy, market, and technological trends. While the current environment may seem uncertain, it also opens the door to new and meaningful opportunities. Investors who see sustainability as a core part of their investment philosophy should not be discouraged by today’s complexities. Instead, they are encouraged to speak with their bank or advisor to explore solutions that reflect both their values and long-term goals. ESG investing remains a relevant and forward-looking approach in a changing world.

[1] Open-end and exchange-traded funds focused on sustainability; impact; or environmental, social, and governance factors.

[2] Morningstar. (2025, May). Investors Turn Away from ESG Funds in Record Numbers in Q1 2025. (Link)

[3] Reuters. (2025, January). Sustainable funds market inflows halve as ESG falls out of favour. [Link]

[4] UN environment programme. (January 2025). China embarks on a journey of ESG disclosure: 2024 progress and focus for 2025. [Link]

[5] iea. (2025, May). Overview and key findings. [Link]

[6] iea. (2025, May). Overview and key findings. [Link]

[7] ExxonMobil. (2023 November). ExxonMobil completes acquisition of Denbury. [Link]

[8] https://www.trilliuminvest.com/.

[9] PRI.(2023 November). Net zero in practice: Insights from equity investors. [Link]

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.