Germany votes for growth

Something momentous has just happened in Germany: the sick man of Europe is about to get a fiscal shot to the arm. After some wrangling – not to mention an election and change of government – the Bundesrat has voted through a significant infrastructure package and, importantly, removed the constitutional debt-related constraint on defence spending.

Verboten Gestattet

The timing could scarcely have been better for the Chancellor-in-waiting, Friedrich Merz. The budgetary discord which collapsed the last ‘ampel’ coalition in November has been replaced by a new resolve to spend in the wake of President Trump’s insistence that Europe pick up more of the bill for its own defence. Talk of withdrawing the US defence umbrella gave the incoming Chancellor the political inertia to push through such reforms with the outgoing Bundestag.

To be clear, this is not window-dressing: the package is big. At the very least it will include €500bn for infrastructure – €100bn of which will be spent on decarbonisation efforts - over the next 12 years, and a further €500bn on defence. In practice, defence spending is effectively uncapped, and some estimates suggest it could be more than double that over this period.

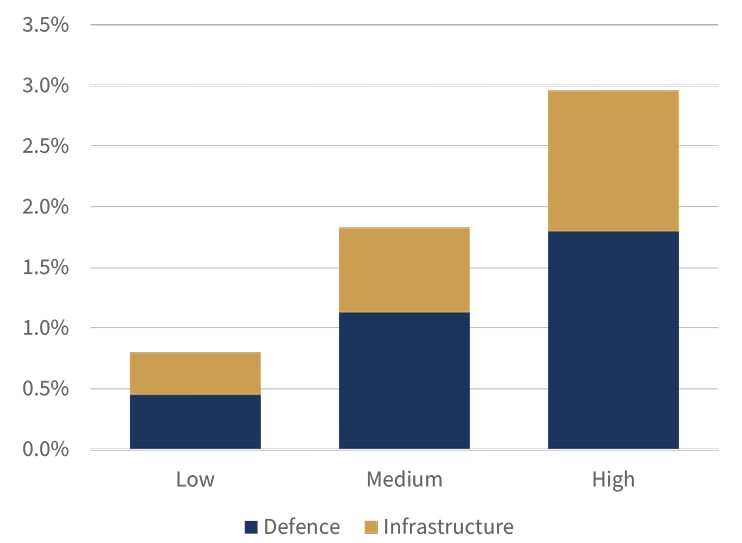

German fiscal scenarios: big spending ahead

Estimated additional expenditure each year (% GDP)*

Source: Rothschild & Co, ASR

* Scenarios assume that defence-related spending is spread out over three years; infrastructure spending is spread out over 12-years.

While this debt-funded spending is unlikely to take place until later in 2025, when it does arrive the fiscal impulse will be significant. Even the lower aggregate amount of €1tn equates to nearly a quarter of Germany’s annual economic output, or close to 2% of GDP per annum if spread evenly over the full 12-year time horizon. For an economy whose recent trend rate of growth has been negligible, the result could be a significant medium-term boost to absolute and relative performance – even without any 'multiplier' effects.

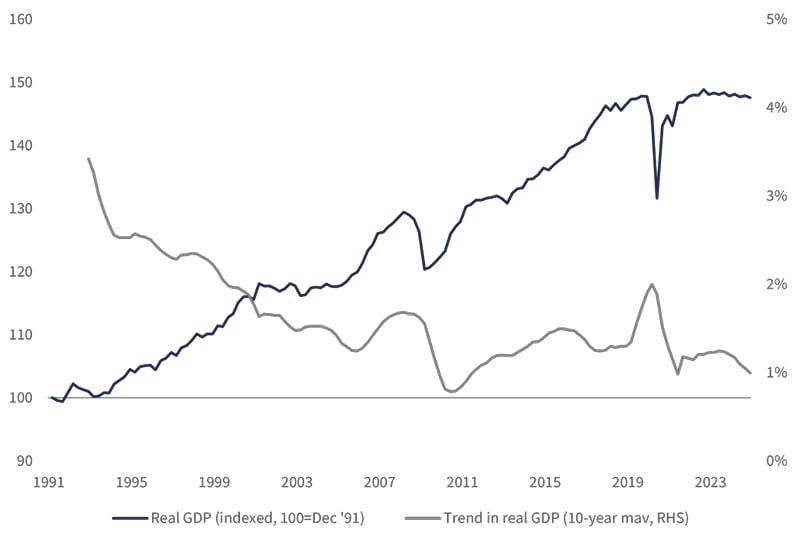

German economic output

Real GDP indexed and 10-year trend in annual GDP growth

Source: Rothschild & Co, Bloomberg. Correct to 21st March 2025.

Some commentators have suggested the outcome might echo Germany’s experience after reunification, or even the ‘Wirtschaftswunder’ in the wake of WWII (which was partly driven by the Marshall Plan). In fact, the level of spending – relative to output – is likely to eclipse both developments. Importantly, tired infrastructure (extra spending could help loosen bottlenecks there) and some visible slack in the labour market (the unemployment rate has been drifting higher in recent years) suggest the outcome is indeed likely to be tilted more towards output – real growth – rather than inflation.

A new European consensus?

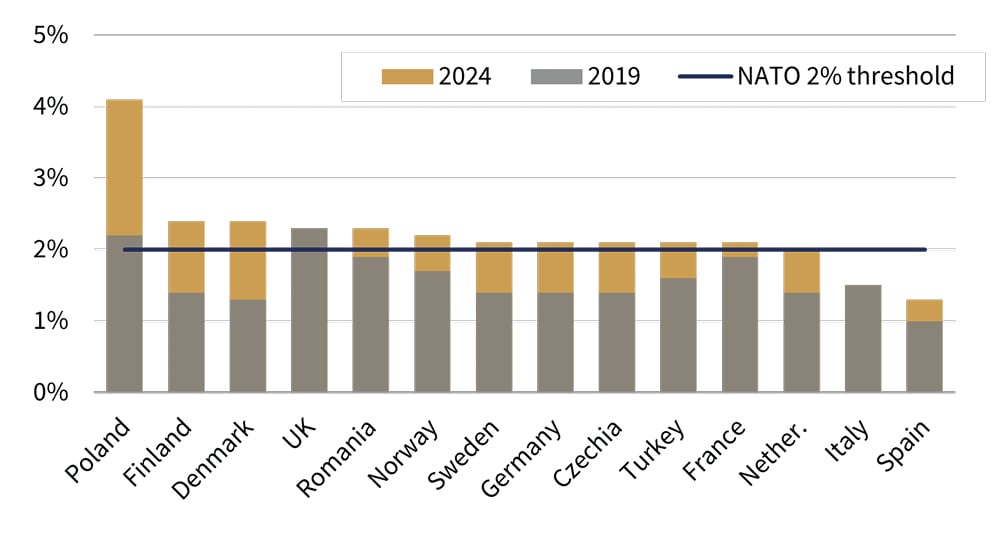

And, of course, it’s not just Germany that stands to benefit. Over the past year, there has been a tremendous amount of political upheaval (more than half of the G7 has either a new leader or government), and Europe more widely has been grappling with political indecision, populism, and that need to bolster defence spending. While budgetary constraints have hardly been abolished overnight, a new consensus is forming, particularly around defence (a topic we wrote about last April), where the UK and French governments have signalled more spending. The EU Commission’s ‘ReArm Europe/ Readiness 2030’ package includes at least €150bn of new borrowing - its long-standing inclination towards mutualised debt issuance may now face fewer misgivings from Germany. For defence spending itself, the much-touted NATO target of 2% of GDP may become a floor.

EU defence spending (% GDP, 2024 vs 2019)

Source: Rothschild & Co, Bloomberg

A European reflation story was slowly gathering momentum even before Germany unveiled its fiscal firepower. Year-to-date, European stocks (+15% in 2025, in USD terms) continue to outperform the global stock market (which is broadly flat since the start of the year), with US stocks in particular lagging in 2025 as expectations for AI slowly return to earth.

Of course, the structural problems facing Germany and Europe have not just disappeared, or even yet been fully addressed: durable growth likely requires a deep-seated change to working practices, risk-taking and product leadership, not just more government spending (even on this scale). The scale of tariffs which Europe will face – and its likely impost on US exports – is also of course still very much in the balance. But there is a certain irony in the fact that a US president pledged to Making America Great Again may so far have done more to boost prospective growth elsewhere than at home.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.