UK stocks outperforming?

The British government has been in difficulties of late, despite its huge parliamentary majority, with the most recent issue relating to the revelations regarding the contentious (or lack of) hiring process for the former ambassador to the US.

Meanwhile, the economy may not be in dire straits, but it is definitely sluggish, and with no fiscal boost in prospect (in contrast to its continental European peers). The unemployment rate has risen by more than in other major economies over the past year or so. The UK looks highly vulnerable to the Middle East supply shock as well, given it is a big net energy importer with few domestic gas storage facilities (this is despite the presence of some large global oil companies in the UK stock market – more on this below). In its latest forecasts, the IMF downgraded the UK’s near-term GDP estimates more than the rest of the G7’s.

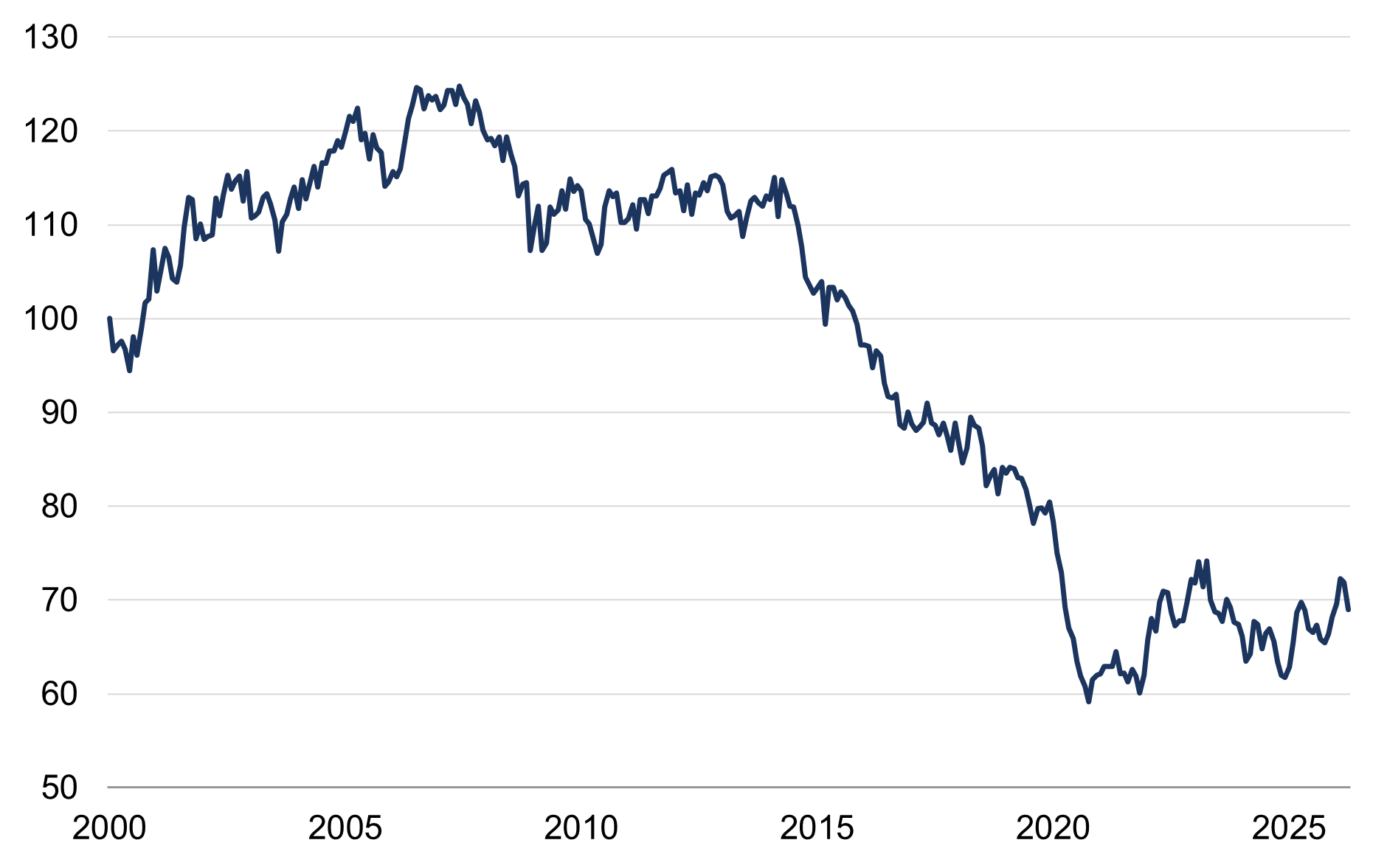

Yet, the local stock market has seemingly overlooked both politics and economics: it has outperformed both year-to-date, and in 2025. For context, the UK’s relative performance had been poor since the global financial crisis (figure 1), though to be fair most regions struggled to keep pace with the US (the bulk of the global market) over this timeframe.

What then has driven this recent revival in UK stock market outperformance? And will it continue?

Figure 1: UK relative returns

Relative to MSCI ACWI (ratio; rebased to 100)

Source: Rothschild & Co, Bloomberg, MSCI

The answer to the first question is the same thing which drove its earlier underperformance: namely, the UK stock market’s composition.

Stock indices do not always reflect their domestic economy. The most widely-watched UK indices derive most (roughly three-quarters) of their earnings from overseas. Moreover, the sectoral mix is unusual in several ways. The largest companies listed in the UK indices include global oil, gas, mining and pharmaceutical companies, while a bank primarily focused on Asia has a weighting of almost a tenth in the ‘main’ indices. Meanwhile the indices’ technology sectors are very small.

The UK stock index is thus usually perceived to be a global, ‘value’-style play, with relatively high weightings in the energy, financials, materials and staples sectors. It has some ‘growth’-style exposure due to its large weighting in healthcare, but, as noted, it conversely has little technology (the UK’s homegrown semiconductor darling, Arm Holdings, used to be a FTSE 100 company until it was acquired by Softbank in 2016, who then chose to re-list it several years later across the Atlantic in 2023).

This means that the performance of the UK economy – or government – may matter less than global trends. And the lack of technology in particular has held the UK market back in a decade characterised by global investors’ affection for the sector. Last year’s UK stock market outperformance was mostly due to its large financials sector, which contributed close to half of the index’s 26% local return at a time when financials were outperforming globally. This year, its energy and materials sectors have accounted for most of its 7% local return.

That said, smaller-cap UK indices such as the FTSE 250 are more domestically tilted, and sensitive to local growth and policy. Other assets altogether, such as bonds and real estate, are more domestically focused again. The exchange rate, too, is of course also more affected by local events.

The answer to the second question then will depend on whether the UK’s sector mix remains in vogue globally – or not. There are parallels with 2022, when the UK stock market also outperformed. Russia’s invasion of Ukraine and the UK’s high weighting in the energy and materials sectors contributed significantly. (We might also suggest that domestic political instability then turned out to have only a fleeting effect on bond markets and the pound…).

However, 2022’s outperformance did not last, as energy prices fell back and technology’s appeal reignited. The outcome of today’s conflict is unknowable, but the real price of oil so far looks unremarkable on a long-term view: year-to-date UK energy sector returns have been half those in 2022. Indeed, the wider UK stock market has in fact underperformed since the start of the Middle East hostilities, as the so-called “beta bounce” in April has seen technology stocks – and other cyclical sectors – notching big rebounds. There is still little sign of underlying AI-related momentum stalling and, again, the UK stock indices lack technology exposure.

Earnings growth, profitability and valuations will all reflect, to varying extents, the UK’s geographic and sector mix. UK earnings performance has been unremarkable, for example. Oil and mining seem poised to do better, but they may not be valued highly by global investors, and UK forward earnings overall were still declining in relative terms as of the end of March (as technology sector earnings boosted the global aggregate).

Overall, we carry no strong ‘top-down’ tactical torch per se for the UK stock market. It may continue to outperform if there is a prolonged energy shock given its unique sector composition. However, if the world gradually returns to the status quo, then there may be greater opportunity in more cyclical segments of the global stock market.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.

-

The next UK Prime Minister

Strategy Blog

Following Keir Starmer’s resignation, Andy Burnham has emerged as Labour’s likely successor. Despite political uncertainty, markets remain calm, with economic and geopolitical trends outweighing domestic politics. Significant policy change appears unlikely.

-

SpaceX: Infinity and beyond?

Strategy Blog

Markets are preparing for a wave of megacap IPOs led by SpaceX, amid strong AI-driven optimism. While liquidity should absorb issuance comfortably, questions remain around valuations, passive investing, concentration risk and index influence.