December: No ‘Santa rally’ for stocks

Investment Communications Team, Investment Strategy Team, Wealth Management

Investment Communications Team, Investment Strategy Team, Wealth Management

Summary

Global equities declined by 2.4% in December (USD terms), while global government bonds fell by 0.7% (USD, hedged terms). Key themes included:

- Broad-based weakness in stock and bond markets, after interest rate rethink;

- Sticky inflation persists and most of the major central banks signal caution ahead;

- US averts shutdown; new government in France (and soon Germany).

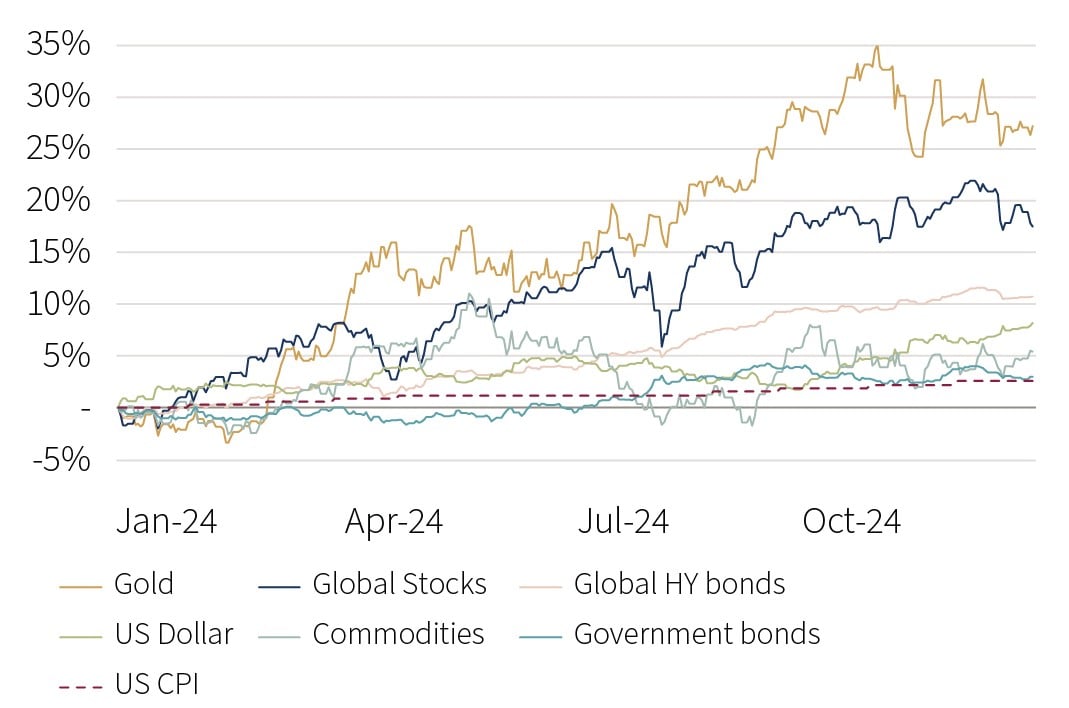

Key chart: Cross asset class returns, 2024 (USD terms, %)

Source: Rothschild & Co, Bloomberg

Chart note: Stocks indices are MSCI, fixed income indices are Bloomberg (dollar, hedged terms), and US dollar is the JP Morgan nominal broad effective exchange rate.

Market: Stocks and bonds sell off

Global stocks fell in December, with broad-based weakness across regions, as the US Federal Reserve unveiled hawkish-looking interest rate projections for the year ahead. That said, global stocks rose by 17.5% in 2024 in dollar terms – largely driven by the US – marking the second consecutive year of double-digit returns. US stock market breadth declined in December, following the Trump-related bounce in the prior month, though the tech-heavy US mega-cap names continued to outperform. In fixed income, government bonds were hurt by the evolving interest rate backdrop, with 10-year yields rising across the US and Europe. Moreover, 10-year bond returns were mixed across regions in 2024: UK gilts were down, US treasuries were modestly weaker, and German bunds were roughly flat in local terms – while peripheral European countries outperformed. In commodities, oil edged higher in December but was down slightly overall in 2024. Despite the US dollar rising to an all-time high on a nominal trade-weighted basis, gold still recorded its best year since 2010 in dollar terms. Bitcoin hit another high, briefly surpassing $100,000.

Economy: Inflation bottoming out?

US economic data generally remained upbeat in November: consumer spending was robust, jobs growth rebounded following weather-related disruptions, and business surveys showed a buoyant services sector. Overall, fourth-quarter GDP estimates were tracking at an above-trend pace, in what was an overall upbeat year. However, US inflation remained sticky, as the headline rate edged up to 2.7% (y/y), while core inflation was unchanged at 3.3%. European economic data remained more subdued, though service sector activity rebounded according to the business surveys (manufacturing activity remained muted). UK hard data were disappointing, as monthly GDP contracted in October and retail sales were weaker than anticipated in November. Yet, core inflation remained elevated in the eurozone at 2.7%, and rose again in the UK, to 3.5%. Elsewhere, China’s consumer spending data was underwhelming in November, though authorities revealed ‘boosting domestic consumption’ as their top priority for 2025.

Policy and politics: Cautious central banks | Political turbulence

The major central banks mostly continued to ease policy rates in December, though retained a hawkish tone. The US Federal Reserve reduced its target rate to the 4.25-4.50% region and suggested two further rate cuts in 2025 in their quarterly projections (reduced from four). In Europe, the Bank of England left its base rate unchanged at 4.75% in a split decision. Conversely, the European Central Bank appeared less concerned with inflation risk, lowering the deposit rate to 3%, while the Swiss National Bank reduced its main interest rate with a larger-than-expected cut, to 0.50%.

Geopolitics remained uneasy, particularly in Ukraine and the Middle East – in the latter, the Assad regime fell in Syria. In the political sphere, a last-minute deal was reached to avert a US government shutdown. Macron selected François Bayrou as the new French PM, following Barnier’s failed attempt to pass the budget. In Germany, Chancellor Scholz lost a confidence vote, setting the scene for a federal election in February. In other parts of the world, Canada’s Finance Minister resigned amid Trump’s tariff threats, and martial law was briefly declared in South Korea by the (now) impeached President.

Performance figures (as of 31/12/2024)

| Equity (MSCI indices $) | Month | Year |

|---|---|---|

| Global | -2.4% | 17.5% |

| US | -2.6% | 24.6% |

| Continental Europe ex. Switz. | -2.0% | 0.7% |

| UK | -2.8% | 7.5% |

| Switzerland | -4.0% | -2.0% |

| Japan | -0.3% | 8.3% |

| Pacific ex Japan | -5.7% | 4.6% |

| EM Asia | 0.2% | 12.0% |

| EM ex Asia | -1.7% | -8.2% |

| Fixed income | Yield | Month | Year |

|---|---|---|---|

| Global Govt (hdg $) | 3.18% | -0.7% | 3.0% |

| Global IG (hdg $) | 4.75% | -1.3% | 3.7% |

| Global HY (hdg $) | 7.49% | -0.2% | 10.7% |

| US 10Y ($) | 4.57% | -2.2% | -0.7% |

| German 10Y (€) | 2.36% | -1.7% | 0.1% |

| UK 10Y (£) | 4.56% | -1.8% | -3.0% |

| Switzerland 10Y (CHF) | 0.33% | -0.4% | 4.2% |

| Currencies (NEERs) | Month | Year |

|---|---|---|

| US Dollar | 1.8% | 8.2% |

| Euro | -0.2% | -0.4% |

| Pound Sterling | 0.1% | 4.2% |

| Swiss Franc | -1.2% | -1.9% |

Table note: NEERs under ‘currencies’ are the JP Morgan trade-weighted nominal effective exchange rates

| Commodities ($) | Level | Month | Year |

|---|---|---|---|

| Gold | 2,625 | -0.7% | 27.2% |

| Brent Crude oil | 75 | 2.3% | -3.1% |

| Natural gas (€) | 49 | 2.3% | 51.1% |

Source: Bloomberg, Rothschild & Co.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.