Growth Equity Update

January 2025 – Edition 34

- Growth equity in 2025: We wrap up 2024 and make some predictions for 2025.

- Venture capital activity grew in 2024: After two years of decline, from the peaks of 2021, global VC activity grew in 2024. Pitchbook estimates that global funding for VC firms increased, albeit by just 5%, from $349bn in 2023 to $368bn in 2024

- Ten predictions for 2025: (i) Venture capital activity to grow by value for the second year in a row (ii) Artificial Intelligence to dominate and broaden (iii) Datacentres: ‘Data is the new oil’ (iv) A revival in Fintech (v) ClimateTech- less hot (vi) Fund raising for VC firms to remain concentrated in the biggest firms (vii) Two tier market -outside AI and related funding, rounds to remain slow with more down rounds (viii) Company casualties to climb (ix) IPO environment –better again in 2025 but no bonanza (x) M&A to pick up as well.

- Public markets in 2024: Global stocks rose by 18%, US stocks (in dollar terms) delivered nearly fivefold the return of non-US stocks. The ‘Magnificent Seven’ surged almost 50% (on a market cap basis) – and accounted for around half of the global stock market’s 2024 return.

- Wall Street strategists optimistic for 2025: Looking at 20 of the leading firms’ predictions we see them anticipating a further 13% advance in the S&P500 in 2025 with the most optimistic at +20% and the most pessimistic at -6%.

- December – another bumper month for US VC raises: Our Deal Monitor recorded 29 US deals at $100m or more in December including the largest of the year, the $10bn raise for the AI led data analytics company, Databricks. European VC saw $2.9bn of venture capital raises in December (-18% yoy) but 2024 as a whole was up 7.5% at $34.2bn.

- ‘I never made predictions and never will.’ Paul Gascoigne

Click here to download a PDF version of Growth Equity Update

Peering into 2025

Some predictions for the growth equity market in 2025

"I'm not always right. Only last week I thought I was wrong, and I wasn't.’’

Jeremy Bullmore - WPP

Our thoughts on likely trends in the venture capital market in 2025.

Artificial Intelligence to dominate and widen: A two-tier market has emerged in venture capital. It’s AI, and then everything else. AI captured around a third of all new VC funding in 2024. The pace quickened with Q4 being the largest quarter by some distance for funding of big AI deals. Q4 saw raises from Databricks ($10bn), OpenAI ($6.6bn), xAI ($6bn), Anthropic ($4bn), Perplexity ($500m), Physical Intelligence ($400m), Vultr ($333m), Sandbox AQ ($300m), Liquid AI ($250m), Writer ($200m) and Tessl ($125m).

The big investments remain into the LLM providers, and the scale of funding means these companies are being funded by the larger VC counterparts – the likes of Andreessen Horowitz, Thrive Capital, the QIA Valor, Sequoia, and industry players (Microsoft, Amazon, Nvidia).

These deals, and the rapid valuation uplifts between rounds, have only stoked the appetite of investors for exposure to the potential industry transformations that the application of AI offers. We expect that the net will widen in 2025 and that a broader range of investors will seek to gain exposure to AI amongst application specific businesses.

Datacentres: ‘Data is the new oil’: Or should that be datacentres? It seems that, despite a slew of large fund raises for data centre operators in 2024 (Vantage Data Centres $9.2bn; Coreweave $1.1bn; Crusoe Energy $500m, Lightmatter $400m) there appears plenty of potential for more. Analysts at Mogan Stanley anticipate there will be 70% pa growth in GenAI related power demand 2024-27 growing from <15 terawatt hours (TWh) in 2023 to 224 TWh in 2027. By 2027 GenAI power demand could be equivalent to 75% of the total global data centre power use in 2022. In this context we see no let up for VC pursuit of new data centre operators.

A revival in Fintech: 2024 was another tough year with a 20% yoy drop in global Fintech funding estimated by Innovate Capital. A report from Silicon Valley Bank in late October observed that fundraising by Fintech oriented VC firms has dropped by over 90% since its peak in 2021. We think though that 2025 is set to see a revival in VC funding for FinTech as investors pursue sectors where the application of AI techniques is potentially transformative. And the modest numbers for primary deals in 2024 disguises substantial appetite for Fintechs in the secondary market, demonstrated by the $1bn secondary offer at Stripe and the $0.5bn at Revolut, both at substantial valuations. With a number of Fintechs poised on the block for IPO in 2025 we see appetite for the sector as likely to revive in 2025.

ClimateTech - less hot: An unusual feature of the European VC market in the last couple of years was that, even as investors became more cautious about pre-revenue/profit/cash flow businesses in the wake of the change to the interest rate environment, there was still a surprising amount of support for ClimateTech companies which were pre-revenue and certainly pre-profit and which required heavy capital investment to build projects like battery gigafactories or networks of EV charging station stations. As the world gets warmer some of the urgency in pursuing such climate led opportunities appears to have dissipated, the outlook for electric vehicle sales has waned ( fewer incentives, lower prices for used EVs, rapid charging infrastructure issues) and the incoming Trump administration (‘Drill, baby, drill’) appears less likely to promote climate initiatives. The Chapter 11 filing by Northvolt, which had received $14-15bn of venture funding, is also a jolt to the system. We think a scaling back of ambition in ClimateTech raises may be a feature of 2025.

Venture capital activity to grow again in 2025: After two years of decline from the heady peaks of 2021 global VC activity grew in 2024 over 2023. Pitchbook estimates that global funding for VC firms increased, albeit by just 5%, from $349bn in 2023 to $368bn in 2024. We think that VC deal value will rise again in 2025 for four reasons (i) there is intense interest in artificial intelligence and associated technologies, and we think these areas will continue to attract substantial funding in 2025 (ii) the public markets have had two years of 20%+ returns. This is positive for investor mood - critical for VC investing (iii) The quality of companies is better. After three years of adapting operating practices to accommodate growth with profits /cashflow rather than all out growth, the universe of VC companies is more investable while valuation expectations are tempered – a better environment for VC investing (iv) if –as we expect – the IPO market improves in 2025- the liquidity of the whole private capital system will improve in turn.

We don’t expect a growth bonanza- the AI raises of 2024 have set a tough comp- but we do expect another year of solid growth in 2025.

Pitchbook - Global VC deal value rose in 2024 for the first time since 2021

Source: Pitchbook

Source: Pitchbook

Fund raising for VC firms to remain tough - concentration in the biggest firms: The corollary of an improved VC market may well be that fund raising for VC firms improves as well. The industry has struggled since its peak of $404bn of global fundraising in 2021, with inflows of funds dropping to $214bn in 2023 and $170bn in 2024.

Global Venture Capital funding raised – 2024 down 20% on 2023

Source: Pitchbook

Source: Pitchbook

Reports suggest that the number of venture capital funds has fallen by around a quarter since 2021 with underlying investors, in a tricky environment for venture capital returns, concentrating their firepower with larger firms.

We expect this consolidation of funding around the bigger VC firms with the strongest track records to continue. Even for such funds the scale of new fundraising may diminish. Some smaller funds may find it more difficult to raise and some casualties may become apparent here as well – whether via M&A and consolidation into bigger units or by closing funds and returning money to investors.

The top 30 funds raised 75% of all venture capital in the US in 2024

Source: Pitchbook data as of December 4, 2024

Source: Pitchbook data as of December 4, 2024

Outside AI and related, funding rounds slower, more down rounds: The AI experience is giving a false impression of the general state of VC markets. While we have seen investors crowding into AI deals with speed and with companies and founders in the ascendant in terms of valuation, the environment is very different elsewhere.

More typically the process of fund raising is much more measured than in the 2020-22 period. VCs are taking their time to do substantial due diligence. There is a greater focus on sustainable revenue growth and the path to profitability and free cash flow. There is a scepticism towards funding multiple years of capex intensive activity before revenues arise. Valuation is keenly thrashed out and investor protections are commonly sought.

In turn this shift of emphasis contributes to the number of down valuation rounds in the system. Multiples are still below the 2020-22 levels. The necessity for companies in the new funding environment to focus on cash and profits has frequently been at the expense of top line growth – which in turn has affected multiples and valuation. Many companies have held off raising in this less attractive valuation environment but in due course they will need to return to the market for new funds. The less attractive growth dynamics combined with the lower public valuations since the last raise and the lower availability of capital combined with a higher investment hurdle, means that there will be more down rounds. Pitchbook numbers at H1 2024 suggested down rounds in the US were 16% of the total, twice the 7.6% of 2021.

Company casualties still climbing: The venture capital model assumes a relatively high failure rate of companies along the way, with the effect hopefully more than offset by some good, and some spectacular, successes. The shift in the interest rate environment and the ensuing change in the ease of accessing capital is through a pivot moment and it is likely that the number of venture capital backed projects that shut down will climb in 2025 as some companies run out of financing road or the motivation to continue in straitened circumstances. The most recent S&P Global Market Intelligence data indicates that bankruptcy filings made by US companies backed by PE and VC climbed more than 15% to 110 in 2024, the highest annual total on record.

Source: S&P Global Market Intelligence

Source: S&P Global Market Intelligence

IPO environment –improvement in 2024, better again in 2025. Two successive years of c20% gains by the S&P 500 should have created an environment where investors are feeling more confident, a useful backdrop for a potential IPO market revival. Global IPO value of $123bn was just modestly ahead of the $122.2bn in 2023. There was though a sharp revival from a low base in the US and Europe. By late December, US IPOs had raised $41bn versus 2023’s $24bn and the $22 bn of 2022. (source, Dealogic)

The experience for investors of those IPOs has also been positive. Nine of the top 10 2024 IPOs are trading above their issue price. The chart from Dealogic shows the returns in the top five US IPOs, four of which are trading ahead of their issue price.

Investor returns on the 5 largest US IPOs in 2024

Source: Dealogic

Source: Dealogic

European IPOs doubled in value in 2024 to €14.7bn from the very modest €7.2bn level of 2023 (source E&Y). This though only brought the value of European IPOs back to the 2022 level and it is notable that momentum petered out after a relatively strong first half.

There is a backlog of private companies waiting to go public. Private equity firms have struggled in the last couple of years to monetise their portfolios and, despite valuation potentially remaining an issue, are likely to act swiftly if the IPO market is deemed to be open and gathering momentum. All in all, it appears likely that the IPO market, especially in the US, should pick up again in 2025 with flow down benefits into the growth equity markets as liquidity in the system is released.

European IPO activity – 2024 twice the level of 2023 but on a par with 2022.

Source: S&P Global Market Intelligence LLC

Source: S&P Global Market Intelligence LLC

M&A picking up as well: M&A has also begun to see an upswing with successive Fed cuts to interest rates, lower inflation and still substantial levels of dry powder giving the market a more stable feel. The strength of public markets has helped in the process of closing valuation gaps. Pressure on PE funds to return capital to investors may spur activity further in 2025. The intense interest in AI is likely to boost activity.

Global M&A – Deal volume and value ($bn) – 12 months rolling

Source: LSEG accessed on November 16, 2024

Source: LSEG accessed on November 16, 2024

How will the end of 2025 look? US interest rates may be only 30bps lower than the levels of the start of the year as inflation remains stubbornly high. There may be some shocks to global trade caused by the imposition of tariffs by the US and retaliatory activity elsewhere. Global GDP growth remains relatively weak (US GDP growth is forecast by the OECD at 2.4% in 2025, down from 2.8% in 2024 with a further slowdown to 2.1% for 2026). Public investors may have made some good money on reasonably priced IPOs. Venture Capital companies will be three years into the focus on profits and growth, more and more will be turning the corner to demonstrate that profitability is there and looking for funding for renewed growth

The outlook for public markets in 2025

2024 - a good year for investors

2024 saw broad-based gains across most asset classes. Global stocks rose by 18%, global government bonds delivered positive returns (in dollar, hedged terms), corporate bonds performed well in absolute and relative terms, and commodities moved modestly higher in dollar terms with gold leading the way while oil softened despite heightened geopolitical risk.

Stocks were all about the US with US stocks delivering nearly fivefold the return of non-US stocks (in dollar terms). The US stock market has now outperformed the rest of the world in all but three of the past 15 years. The ‘Magnificent Seven’ surged almost 50% (on a market cap basis) – and accounted for around half of the global stock market’s 2024 return.

Another strong year for US (and thus global) stocks

Source: Rothschild & Co, Bloomberg, MSCI, Wikimedia Commons

Source: Rothschild & Co, Bloomberg, MSCI, Wikimedia Commons

The strength of the US market led to further widening of the valuation gap between the US market and its developed market peers. The US is usually the most expensive market – reflecting its higher profitability and growth. Nevertheless, the current valuation spread is unusually wide.

Source: Rothschild & Co, Bloomberg, Datastream, I/B/E/S

Source: Rothschild & Co, Bloomberg, Datastream, I/B/E/S

Much of this can be ascribed to the substantial valuation of the ‘tech’ names. The next chart shows the disparity between the forward p/e multiple of the Magnificent Seven stocks (30.7x) and the US market as a whole (21.9x) and an equally weighted US index (reduces the impact of the Magnificent 7) at 18.1x. These compare with the global market ex the US at just 13.4x.

Interestingly the chart above shows that while earnings estimates continued to grow sharply in the US in 2024, they also are showing signs of a (more subdued) pick up in the rest of the world which, combined with lower valuations, is a positive indicator for 2025.

Source: Rothschild & Co, Bloomberg, MSCI

Source: Rothschild & Co, Bloomberg, MSCI

In the last Growth Equity Update we looked at the market’s enthusiastic response to the election of Donald Trump as US President, the Trump effect. We observed that the US election result had refuelled market optimism on the basis that President Trump’s administration will imply less regulation and lower taxes, despite the risk of higher tariffs. It sent certain sectors of the stock market notably higher, including banks, energy stocks, smaller companies, and some tech stocks. Crypto related stocks were also big beneficiaries of the expectation of lower regulation.

The sectoral responses to the Trump re-election are nicely captured in the next chart which shows Q4 performance. Defensive stocks, non-US stocks and government bonds underperformed post the Trump re-election. Cyclical stocks, US stocks, the dollar and the Magnificent 7 performed well. Crypto performed strongly on hopes of a friendly administration (Bitcoin up 47%, Dogecoin up 147%). Hopes of increased spending on national security and immigration control sent data analytics firm Palantir up 103%. Elon Musk’s Tesla was up 54%.

Source: Rothschild & Co, Bloomberg, MSCI

Source: Rothschild & Co, Bloomberg, MSCI

As we move into 2025 a reminder of Wall Street strategists’ forecasts for the level of the US stock market in 2025.

There’s nothing like a year of strong performance of an index to make people more bullish. Having greatly underestimated the prospects of the S&P500 at the start of 2024, the strategists have compensated with more optimistic forecasts. Looking at 20 of the leading firms’ predictions we see them anticipating a further 13% advance in the S&P500 in 2025.

The most optimistic end sees about a 20% advance to c7,000 from the year end level of 5,882. Oppenheimer heads the list with its target of 21% upside to 7,100 citing ‘the resilience in economic growth, business activity, the consumer, and job creation’. The firm looks for 10% earnings growth and for the S&P 500's 12-month forward p/e ratio to rise, reaching 25.8x forward earnings, well ahead of the five-year average of 20x. Yardeni Research, the most optimistic forecaster at the start of 2024 looks for a 19% advance in the S&P 500 to 7,000 citing ‘animal spirits’ and saying 'Trump 2.0 represents a major regime change that’s bullish for the economy and stocks.'

Thirteen of the twenty forecasts put the S&P 500 in a range of 6,500-6,700, upside of 11-14% from the start year level. RBC comments on its 6,600 forecast (12% upside) 'The story the data tells us is that another year of solid economic and earnings growth, some political tailwinds, and some additional relief on inflation (which should keep the S&P 500’s P/E elevated) can keep stocks moving higher in the year ahead.'

Morgan Stanley and Goldman Sachs are at a 2025 year-end level of 6,500 (+11%). The Goldman Sachs 6,500 forecast is ‘predicated on continued U.S. economic expansion’ and looks for 11% earnings growth with the impact of higher tariffs offset by lower corporation tax rates. Morgan Stanley looks for 13% eps growth in 2025 and appears to anticipate market leadership changes – presumably, a reference to the strength of tech stocks yielding to other sectors, as well as to uncertainty post the US presidential election.

The are few pessimists around. Morgan Stanley has a face-saving range of potential outcomes - from 4,600 at the low end to 7,400 at the high end. The low end would imply a 22% fall in the market. The only firm which actually forecasts a fall in the S&P500 in 2025 is Stifel. We characterise its 2025-year end forecast for the S&P500 as 5,500, downside of 6%. More accurately it describes its forecast as ‘mid 5,000s’. Stifel thinks momentum will carry the S&P500 higher in H1 2025 before a fall of 10-15% in the second half. It cites a possible slowing down in US GDP growth to 1.5% in H2 2025 and core personal consumption expenditure inflation still over the Fed’s target as catalysts for this second half correction.

Wall Street’s forecast for the S&P 2025-year end level – up 13%

Source: Press reports; R&Co

Source: Press reports; R&Co

So far in 2025 – and we are less than two full weeks in – the debates have centred around what might disrupt the market’s optimism with a focus on two immediate linked factors, rising bond yields and the prospect that stubborn inflation may mean that cuts to interest rates, notably in the US, are nearing their end for this cycle. The US bond market has seen 10-year benchmark yields exceed 4.7%, the highest since April 2024 with the strength of the dollar (itself a function of strong inflows into the US market post the Trump election) and the impact of potential tariffs on inflation and interest rates leading factors.

The market correctly anticipated the 25bps Fed rate cut to 4.25%-4.5% at its December 2024 meeting. The tone from the Fed though was markedly more cautious. The Fed chair Jay Powell remarked that the decision to cut rates in December was a ‘closer call’ than in previous meetings and he observed both that inflation was now going ‘sideways’ while the risk to the jobs market – the other factor in the Fed’s thinking on rate levels- was now ‘diminished.’

Going into the December meeting the Fed’s official dot plot looked for a cut of 25bps in December and a further fall of 100bps in rates to 3.25%-3.5% by the end of 2025. The new dot plot produced after the meeting had just 50bps of rate cuts in 2025 which would leave the year end rates at 3.75%-4%. End 2026 is projected at 3.25%-3.5%. The Fed officials revised up their forecasts for core (PCE) inflation, now seen at 2.5% in 2025, reflecting some impact from rising tariffs.

Post the meeting the markets appeared to pencil in just 30bps of rate cuts for 2025. There is no expectation of a rate cut at the Fed’s next meeting on January 31st.

This expectation of a flatter profile of projected rate cuts is shared in the UK where rates were held at 4.75% in the December 2024 meeting. The BoE noted that increases in prices and wages had ‘added to the risk of inflation persistence,’ projected to rise to 3%+ in the Spring. The BoE Governor commented ‘with the heightened uncertainty in the economy, we can’t commit to when or by how much we will cut rates in the coming year.' Most commentators appear now to expect just c50bps of interest rate cuts in 2025.

This potential flattening of the interest rate curve in the US and the UK, and the contrast with the Eurozone which has been steadily cutting, is illustrated in the chart.

Most of the interest rate easing may have already been done

Source: Rothschild & Co, Bloomberg

Source: Rothschild & Co, Bloomberg

For more on these subjects read this excellent piece from the R&Co Global Investment strategists. 2024: Markets, Momentum and MAGA | Rothschild & Co.

Rothschild & Co strategist Kevin Gardiner thinks the prospect of further significant market gains are becoming less likely in 2025. He summarises the current key drivers of the market in this graphic:

Source: Rothschild & Co

Source: Rothschild & Co

December – another bumper month for US VC raises.

Our Deal Monitor recorded 29 deals at $100m or more in the US in December as well as the largest VC raise of the year, the $10bn for the AI-led data analytics company, Databricks led by 2024’s perennial AI investor, Thrive Capital, which is understood to have invested $1bn plus. The monthly total for VC raises reached $15.9bn, just short of November’s $16.4bn and in line with the $15.9bn of October. In all this meant that Q4 in the US saw $48bn of VC raises, a remarkable total.

Databricks raised $10bn from investors in a Series J at a valuation of more than $62bn, the largest venture capital raise of the year. The deal was led by a blue-chip list of AI investors including Thrive Capital, Andreessen Horowitz, DST Global, GIC and Insight Partners. The raise is to fund employee stock activity with employees able to sell out their maturing stock options and to cover payable taxes. In addition, the company states that ‘To satisfy customer demand, Databricks intends to invest this capital towards new AI products, acquisitions, and significant expansion of its international go-to-market operations.’

Databricks runs its Data Intelligence Platform which allows companies to control their data and to put it to work with AI. Databricks has over 10,000 customers (including 60% of the Fortune 500). Annualised revenue is expected to reach $3bn by the end of January 2025 implying a forward valuation of c20x revenue. The company grew revenues 60% yoy in Q3. The company expects to be free cash flow positive on a quarterly basis for the first time in Q4 (ending 31 January 2025). Non-GAAP subscription gross margins are above 80%.

Illustrating the appetite for premium AI related deals, the Databricks CEOI Ali Ghodsi claims that the company initially targeted a raise of $3-4bn. Huge investor interest, however, meant that the size of the round and the valuation weas increased. Quoted in TechCrunch Ghodsi remarked:

“I saw this Excel sheet where they keep a tally of all the people that want to invest. It was $19 billion of interest, and I almost fell off the chair. And we hadn’t even talked to everybody. I was like, ‘Oh my God, that’s a huge amount of numbers.’ So, then we actually moved the price up.”

There has been a lot of commentary as to whether AI valuations in venture capital are in ‘bubble’ territory. Interestingly Ali Ghodsi – as a virtual AI incumbent – sees a case for this amongst some of the junior members of his industry.

“I mean, it’s peak AI bubble. It doesn’t take a genius to know that a company with five people which has no product, no innovation, no IP — just recent grads — [is not] worth hundreds of millions, sometimes billions,” You get billion-dollar valuations on these startups that have nothing — that’s a bubble.”

As is now usual, all the leading deals of the month have a strong artificial intelligence connection. December’s second largest deal was the $693m Series D for semiconductor designer Tenstorrent at a valuation of $2bn. Tenstorrent describes itself as ‘a next-generation computing company that builds computers for AI.’ These are built using its Tensix cores. In addition to selling hardware, the company licenses AI and RISC-V intellectual property to customers that want to own and customize their silicon. Tenstorrent says it will use funding to build out open-source AI software stacks, hire developers, expand its global development, and design centres, and build systems and clouds for AI developers. The deal was led by Samsung Securities and AFW Partners and included XTX Markets, Corner Capital, Protagonist, MESH, Export Development Canada, Healthcare of Ontario Pension Plan, LG Technology Ventures, Hyundai Motor Group, FMR, Innovation Engine, Baillie Gifford, and Bezos Expeditions. The deal saw strong demand and was over-subscribed.

The data centre company Crusoe is an AI infrastructure provider. It closed a $600m Series D in December led by Founders Fund, with other investors including Fidelity, Long Journey Ventures, Mubadala, NVIDIA, Ribbit Capital, and Valor Equity Partners. Crusoe provides large-scale clean energy, AI-optimized data centres, and Crusoe Cloud, a cloud platform tailored for AI and machine learning workloads.

AI Search engine Perplexity closed its latest $500m round just before Christmas with its valuation reaching $9bn. The raise was led by Institutional Venture Partners and supported by Nvidia, New Enterprise Associates, B Capital, and T Rowe Price. Perplexity announced ARR of $35m in August, implying a forward revenue multiple of c250x.

In April 2024 Perplexity raised a $250m Series C valuing the business at $2.5bn. The round was led by NEA and IVP. This followed a $74m Series B completed in early January 2024 and supported by Nvidia, Jeff Bezos and others which came in at a valuation of c$520m.

Perplexity describes itself as ‘the world's first fully functional conversational answer engine.’ The business looks to compete with Google, with users typing in questions and receiving conversational style answers, with much of the information derived from web scraping. This has led to accusations by publishers that Perplexity has plagiarised their material which in turn led Perplexity to announce in July a ‘Publishers Program’ that offers publishers a double-digit share of Perplexity’s (as yet modest) revenues.

In all December saw 11 deals of $200m+ in the US. Of the other seven deals three were AI related and four were fintechs, a notable resurgence for the sector where primary activity was very subdued in 2024.

The other AI related businesses were Vultr, a cloud infrastructure business which raised $333m at a valuation of $3.5bn with AMD and LuminArx Capital Management leading. Vultr will use this new equity financing to support its accelerated global expansion in AI infrastructure and cloud computing. Sandbox AQ raised $300m at a $5.4bn valuation. The company is developing Large Quantitative Models (LQMs- ‘the next wave of AI’) and AI-driven technologies across healthcare, materials science, navigation, and cybersecurity. Liquid AI is building a new type of LLM - ‘Liquid Foundation Models (LFMs) – a new generation of generative AI models that achieve state-of-the-art performance at every scale, while maintaining a smaller memory footprint and more efficient inference.’ The company raised a $250m Series A at a $2.3bn valuation from AMD.

The four fintech raises were a $350m raise for Splitero from the Blue Owl Managed Funds which took the form of funding for Splitero’s programme of Home Equity Investments which enable homeowners to partially monetise in cash the future value of their home. One, which is majority owned by Walmart, provides financial services such as instalment loans, debit cards, and payments services to Walmart customers and employees. Walmart and Ribbit Capital led a $300m raise for the company. The consumer fintech banking platform Current raised $200m from Andreessen Horowitz, Wellington Management, and Avenir. It is focused on providing mobile access to financial services. Zest AI is a credit underwriting solutions provider using AI to improve the accuracy of its credit scoring for US banks and credit unions. It raised $200m from Index Partners and Battery Ventures to ‘take aim at high impact M&A opportunities.’

The US – $15.9bn of US venture backed raises of $100m+ in December

Source: Rothschild & Co, Crunchbase

Source: Rothschild & Co, Crunchbase

Europe: There was a flurry of year end activity in European VC resulting in $2.9bn of venture capital raises in the month with nine deals of $100m+. The total was 18% down on the $3.5bn raised in December 2023.

Overall Europe had a strong start to the year with the value of VC raises up 36% yoy at $17.7bn by the end of H1. Q3 was down 28% yoy and Q4, helped by a strong October, was up 11% yoy. Overall though the value of raises in H2 fell by 12% yoy. This left the year up 7.5% at $34.2bn, a decent result but less than might have been anticipated after the strong start.

What was missing in H2 2024 versus H2 2023 were big raises in Climate Tech. In H2 2023 there were five deals of $750m and above in Europe, all in Climate Tech and cumulatively amounting to $5.4bn. In H2 2024 there were no deals above $750m.

The top three of those H2 2023 Climate Tech deals were typified by major projects involving substantial upfront capital expenditure to build plant with meaningful revenues only flowing once they were up and running. Thus, H2Green Steel – now renamed Stegra –raised $1.65bn in September 2023 to build a green steel plant in Boden, Sweden with production targeted for 2026. Verkor, a designer of high performance, low carbon batteries raised €2bn in financing in September 2023 (€850m Series C funding, €600m of debt from the European Investment Bank and French subsidies of c€650m) for its planned gigafactory in Dunkirk planned to be operational in 2025. Northvolt raised $1.3bn as it pursued its battery gigafactory roll out with six planned including the main project at Ett in Sweden. Without these three deals totalling almost $4bn of equity, VC capital raised in H2 2024 would have comfortably exceeded the revised H2 2023 total. Northvolt filed for Chapter 11 bankruptcy protection in the US in November 2024 and its difficulties may have affected the environment for fundraising for this type of project in H2 2024.

H2 2023 - Five Climate Tech deals of $750m +

Source: Rothschild & Co

Source: Rothschild & Co

Coming back to December 2024’s raises the largest were:

Hostaway is a Finnish Traveltech business which helps managers of short-term rental properties to automate and improve their property management. Its platform has a range of tools and services such as dynamic pricing, smart locks, and insurance. Hostaway raised $365m in a round led by General Atlantic and PSG Equity at a valuation of $925m post money.

Finland also saw December’s second largest raise. Oura, a wearables business, produces a ‘smart ring’ which tracks sleep and other aspects of health (cardiovascular, fertility, calorie intake etc). The latest ring, the Oura 4, is priced at $349/£349 and has a monthly subscription of $5.99/£5.99 to access key tracking features. FMR and Dexcom led a $200m Series D valuing the company at $5.2bn. Oura has sold more than 2.5 million rings. Dexcom, which is a leader in glucose biosensing is believed to have invested more than $75m and the two companies will partner on cross selling.

German ClimateTech company 1Komma5 has developed a marketplace to help homeowners buy and install carbon neutral energy systems such as solar, charging stations and heat pumps. It has already installed over 300,000 decentralized, controllable energy systems. The company’s Heartbeat AI system connects private customers with the energy market and controls electricity generation and sales buying electricity in the spot market when prices are lowest and selling excess electricity back to the grid when prices are highest. Its €150m ($165m) raise, described as a ‘pre-IPO’ round, was led by CalSTRS and G2 Venture Partners, and supported by 2150, Norrsken, Hamilton Lane, b2venture, Eurazeo, and eCAPITAL. With the funds it plans to accelerate its growth and roll out Heartbeat AI across Europe and Australia.

Nscale’s $155m December raise was one of the largest European Series A rounds in 2024. Based in the UK Nscale is an AI hyperscaler with its data centres sites supporting hyperscalers and LLM platforms. The deal was led by Sandton Capital Partners, supported by Kestrel, Blue Sky Capital Managers, and Florence Capital. The company will use the build out its data centre capacity across Europe and North America from 300MW to 1.3GW, with 120MW planned for 2025.

The leading group of raises was rounded out by two biotechs. Noema Pharma, a Swiss company targeting debilitating central nervous system disorders, raised $147m in a Series B led by EQT Partners. UK based Ottimo Pharma raised $140m in a Series A led by OrbiMed, Avoro Capital and Samsara BioCapital. Its bifunctional medicines extend the lives of people living with cancer.

Europe - $2.9bn of raises in December

Source: Rothschild & Co

Source: Rothschild & Co

Our views on the state of the venture capital markets

The combination of global inflation, rising interest rates, and increased geopolitical risk substantially impacted the venture capital market in 2022 and 2023. 2024 saw some adaptation to the ‘new normal’. The refocusing of venture backed companies to achieve a better balance of growth, profitability and cash flow and the delivery of interest rate cuts have led to increased optimism and enthusiasm for growth equity.

Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment has had a sharp impact on valuations in private markets. The scale of the fall in the Refinitiv VC index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023 and slow recovery in 2024.

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models, the applications of AI and industries (data centres, semiconductors) supporting the development of AI.

- Best-in-class companies, addressing critical requirements, continue to attract support. There are still hotspots for investment most notably in Artificial Intelligence, and related industries such as datacentres. Certain investors remain very active in the space with substantial funds to deploy.

- The speed of the investment process has slowed. The level of diligence on new deals has stepped up

- 2023 and 2024 saw more downrounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these.

- There is substantial dry powder in the VC industry. This though appears to be prioritised to support existing rather than new investments

- It seems that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses.

- Valuation priorities have shifted with investors having moved away from an emphasis on revenue growth and revenue multiple emphasis. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and an emphasis on DCF and comparative based multiples.

Read the previous editions:

May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024

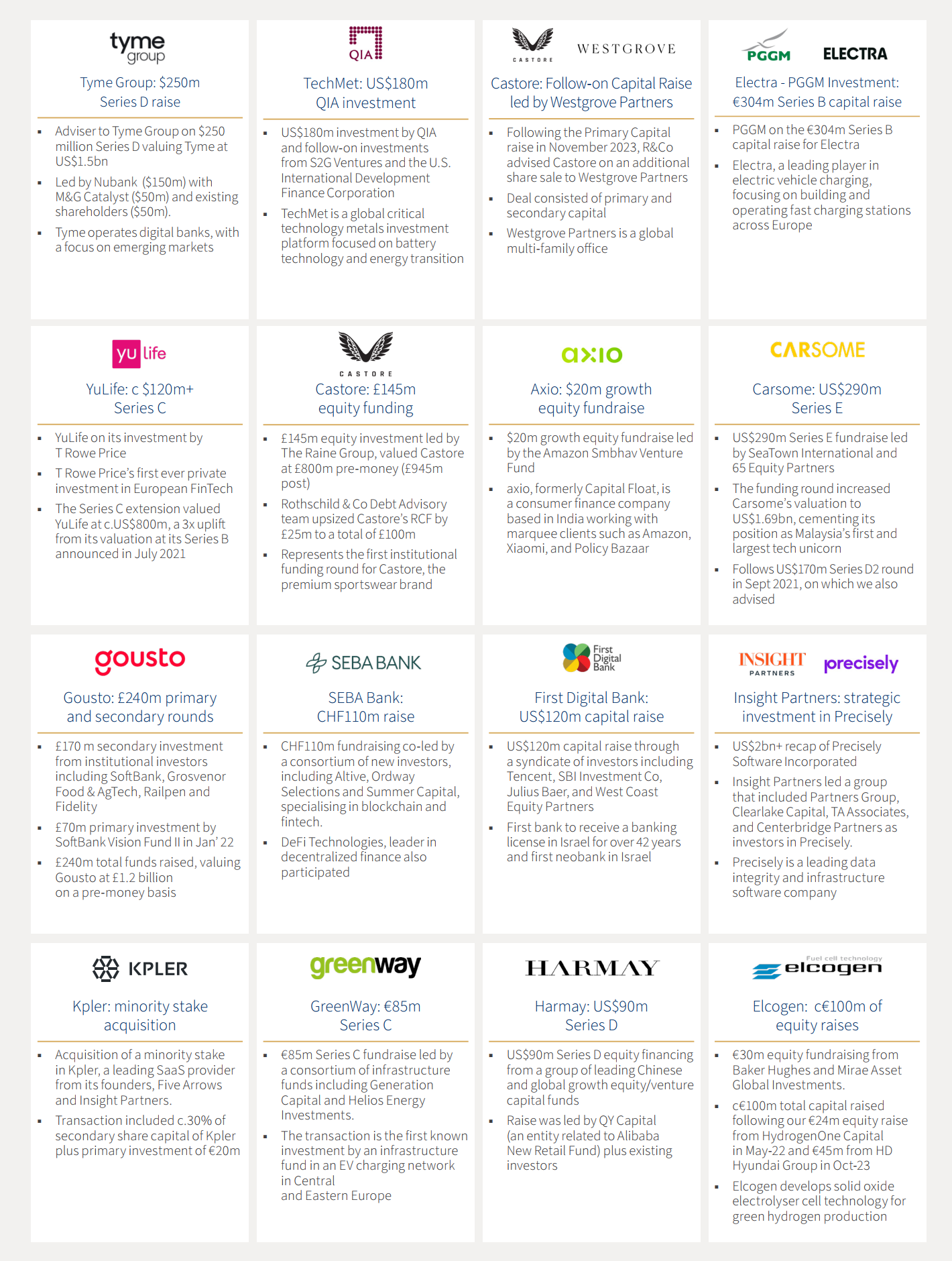

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised

For more information, or advice, contact our Growth Equity team:

Chris Hawley

Global Head of Private Capital

chris.hawley@rothschildandco.com

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Advisory

patrick.wellington@rothschildandco.com

+44 20 7280 5088

+44 7542 477 291

Mark Connelly

Head of North American Equity Markets Solutions

mark.connelly@rothschildandco.com

+1 212 403 5500

+1 917 297 5131

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.