2024: Markets, Momentum and MAGA

2024 was a year of friendly economics and uncomfortable geopolitics. But it was the former which dominated risk appetite these past twelve months, amid favourable growth, disinflation and falling interest rates. Stocks have delivered another year of double-digit returns, in what has been an uneven ascent.

Here we outline some of the key market themes in 2024.

1. Another good year for investors – the US is still exceptional

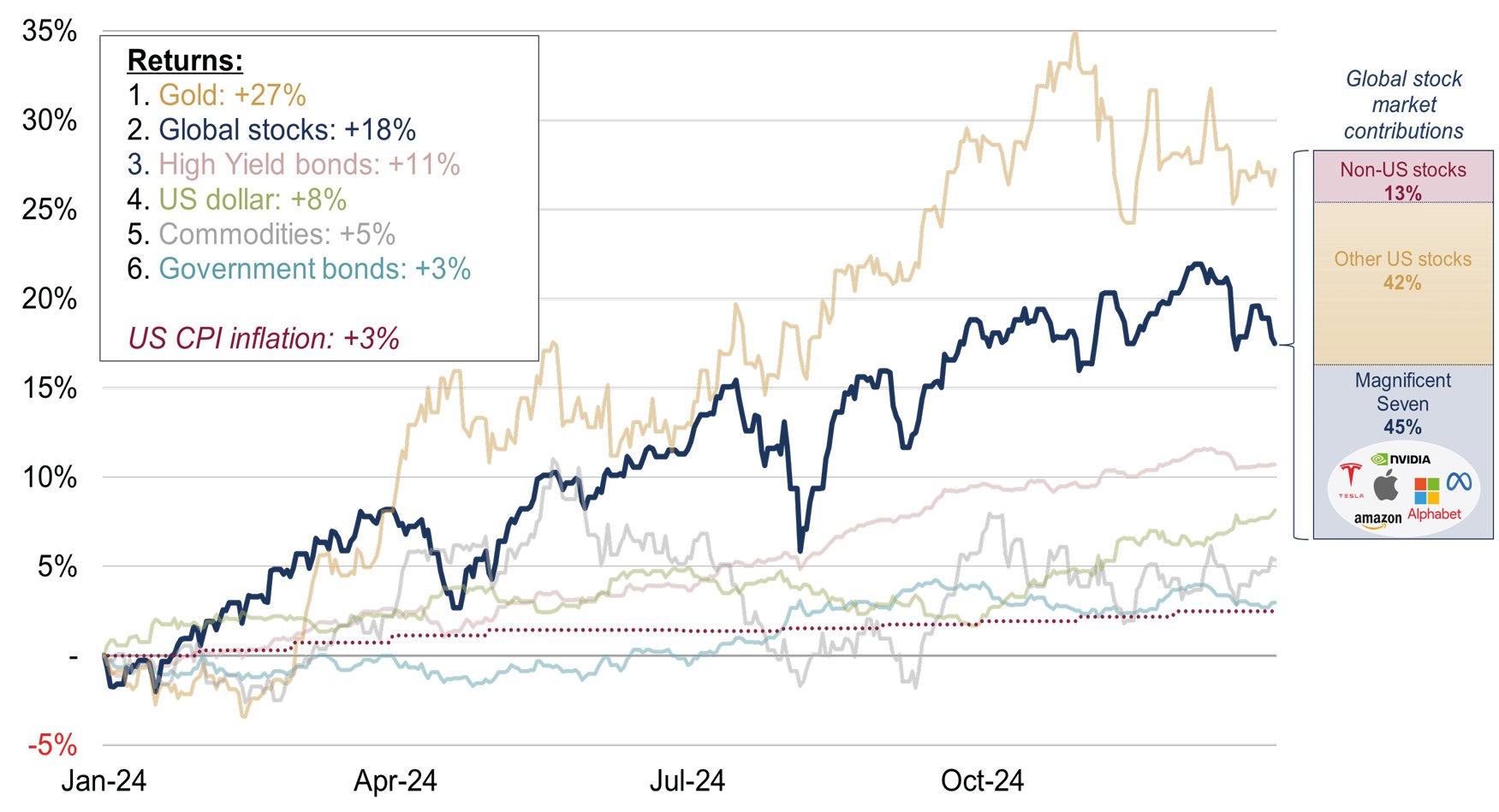

2024 was largely a rerun of 2023, with broad-based gains across most asset classes. Global stocks rose by 17.5% to fresh highs in dollar terms, though this fell short of last year’s gains. In fixed income, global government bonds delivered positive returns (in dollar, hedged terms), despite a rebound in longer-dated yields. Corporate bonds continued to perform well in absolute and relative terms, with positive returns and a further spread tightening. Commodities moved modestly higher in dollar terms, but there were major divergences within the indices: gold continued to shine, surging by more than a quarter, while oil softened despite heightened geopolitical risk.

Most striking though was the uneven rally in stocks, with US stocks delivering nearly fivefold the return of non-US stocks (in dollar terms). The US stock market has now outperformed the rest of the world in all but three of the past 15 years. Momentum-type strategies excelled, with the richly valued US ‘technology’ juggernauts firmly in the driving seat. Nvidia nearly tripled (again) and the wider ‘Magnificent Seven’1 cohort surged by close to 50% (on a market cap basis) – and accounted for around half of the global stock market’s 2024 return.

2024 cross asset returns

(USD, %)

Source: Rothschild & Co, Bloomberg, MSCI

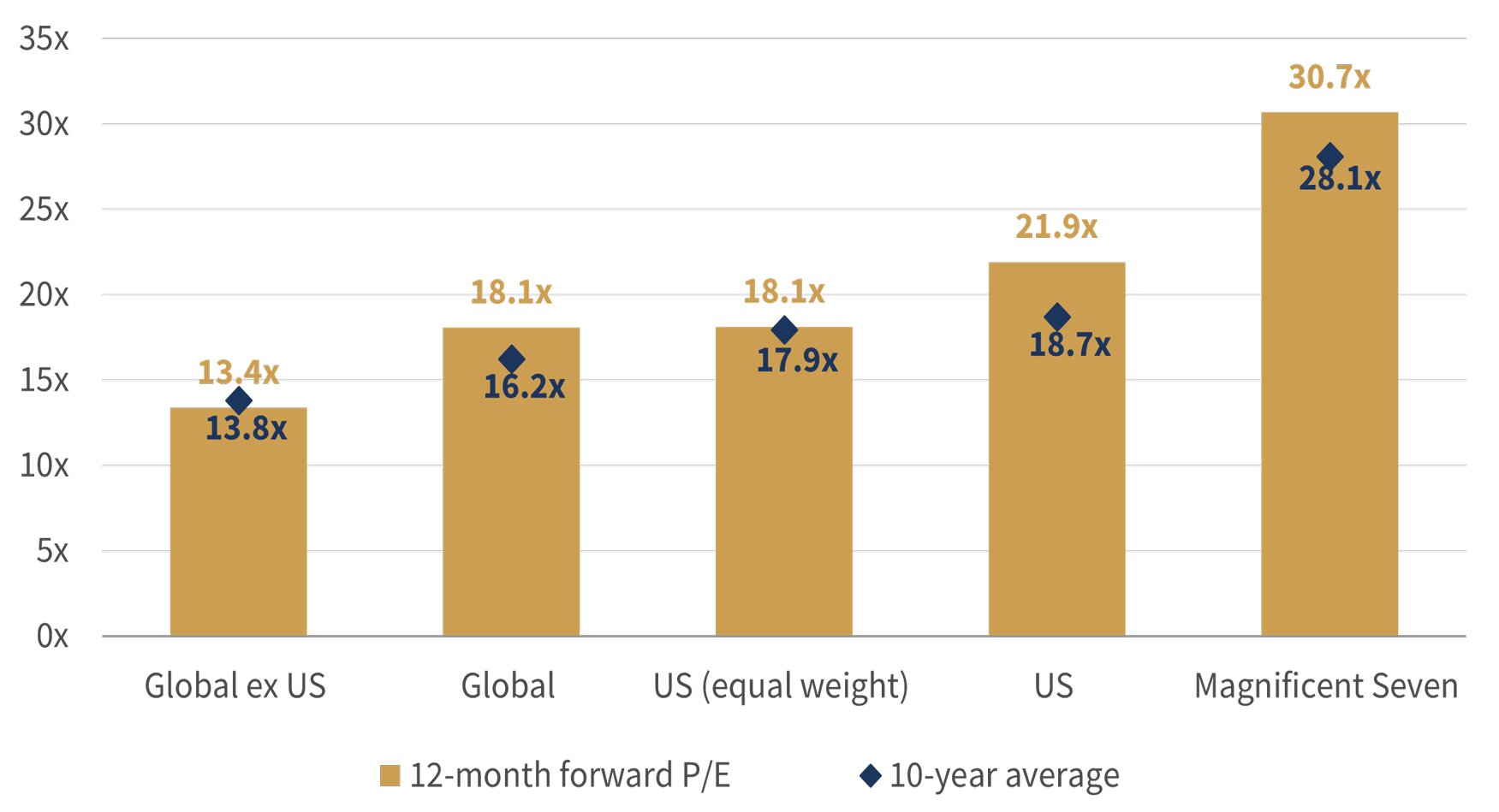

2. Narrow earnings and wide valuations

As noted, 2024 was another year of narrowness and lopsided returns, which has led to a further widening of the valuation gulf between the richly valued US market and its developed market peers. The US is usually the most expensive market – reflecting its higher profitability and growth – but that valuation spread is unusually wide today. Much of it can be ascribed to a further revaluation of the large ‘tech-like’ names this year. An equal-weighted US stock index, for example, appears closer to what we might think of as ‘fair value’.

However, there are also signs that something more fundamental has been happening, with earnings delivery coming through, following a subdued 2023. US earnings grew most briskly – as they have done over the past decade or so (again, the US mega-cap ‘Magnificent Seven’ led the way, as they did with valuations) – while the earnings cycle in the rest of the world also appeared to turn a corner (though, the longer-term trend in earnings growth remains much lower than in the US).

If analysts’ expectations are anything to go by, the narrow earnings story may be set to broaden to other sectors and beyond. Other developed regions seem poised to see their earnings expand at an above-trend pace over the next couple of years.

The US and its tech-focused stocks may perhaps not be the only game in town in 2025.

Stock market valuations

12-month forward price-earnings ratio (relative to 10-year average)

Source: Rothschild & Co, Bloomberg, MSCI

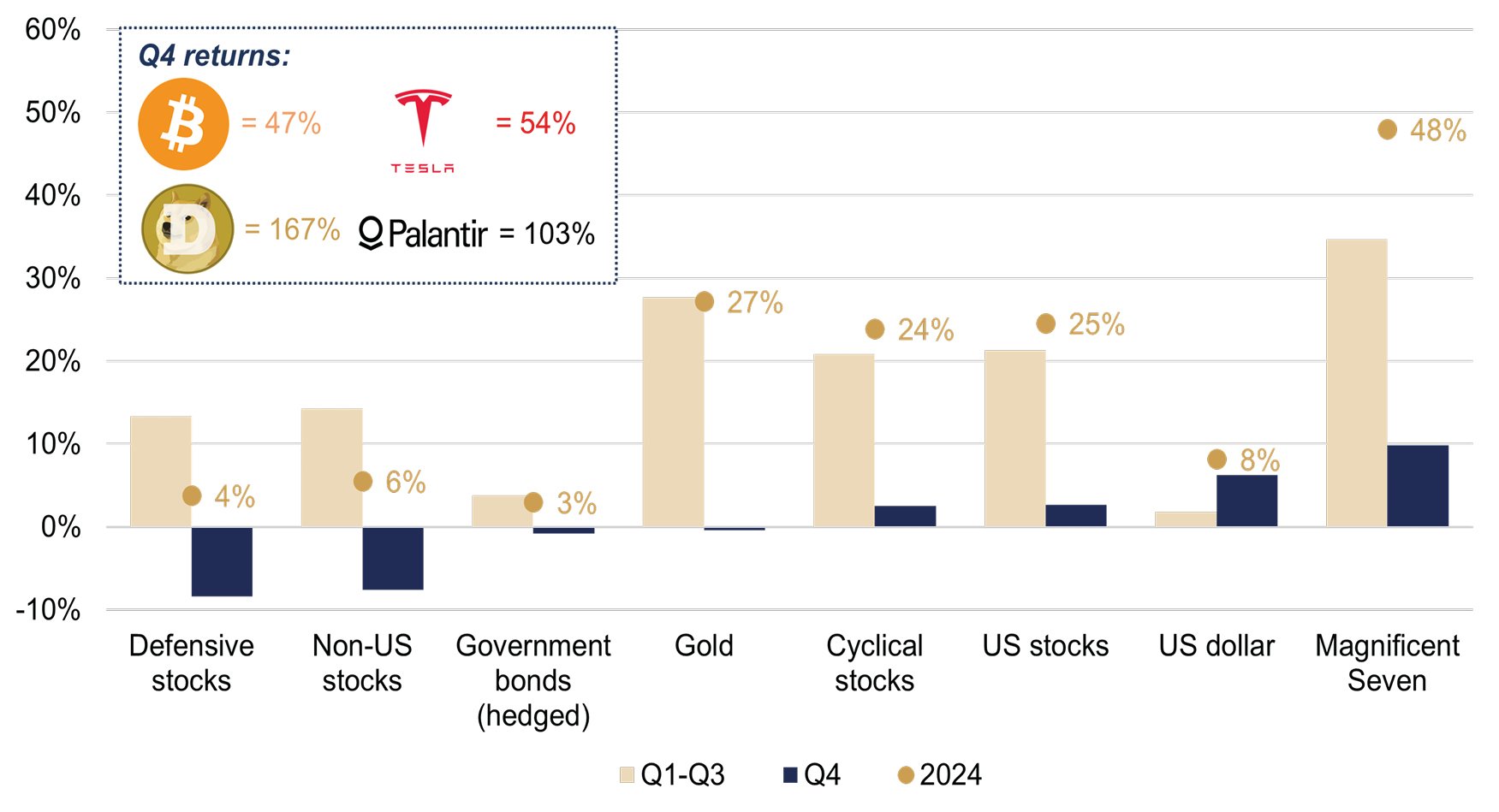

3. T.R.U.M.P.

The last twelve months has seen tremendous political change across the developed world: new leaders and faces in the UK and Japan, with potential change ahead in Germany, France and Canada. But perhaps most momentous of all is the return of Donald Trump, bolstered by a Republican sweep of Congress.

Markets initially responded vigorously to the reflationary promise of tax cuts and deregulation, boosting anything with a cyclical or US tilt – further cementing the winners’ lead. The ‘Magnificent Seven’ companies rallied a further tenth after the election, while anything with a perception of closeness to Trump (such as bitcoin and Tesla) surged even more dramatically. Meanwhile, defensive segments and emerging markets suffered, as did US treasuries given the potentially inflationary consequences of Trump’s policies.

Whether these revitalised animal spirits persist remains to be seen. There is a lot of uncertainty around the ‘MAGA’ agenda: what, when and how the policies are implemented. Arguably, there is some post-election complacency visible – not only the big surge in more speculative assets, but also in terms of near-term investor optimism. The modest bout of volatility in December was perhaps a gentle reminder that nothing should be taken for granted.

The Trump trade: winners and losers

Sorted by Q4 2024 returns (USD, %)

Source: Rothschild & Co, Bloomberg, MSCI

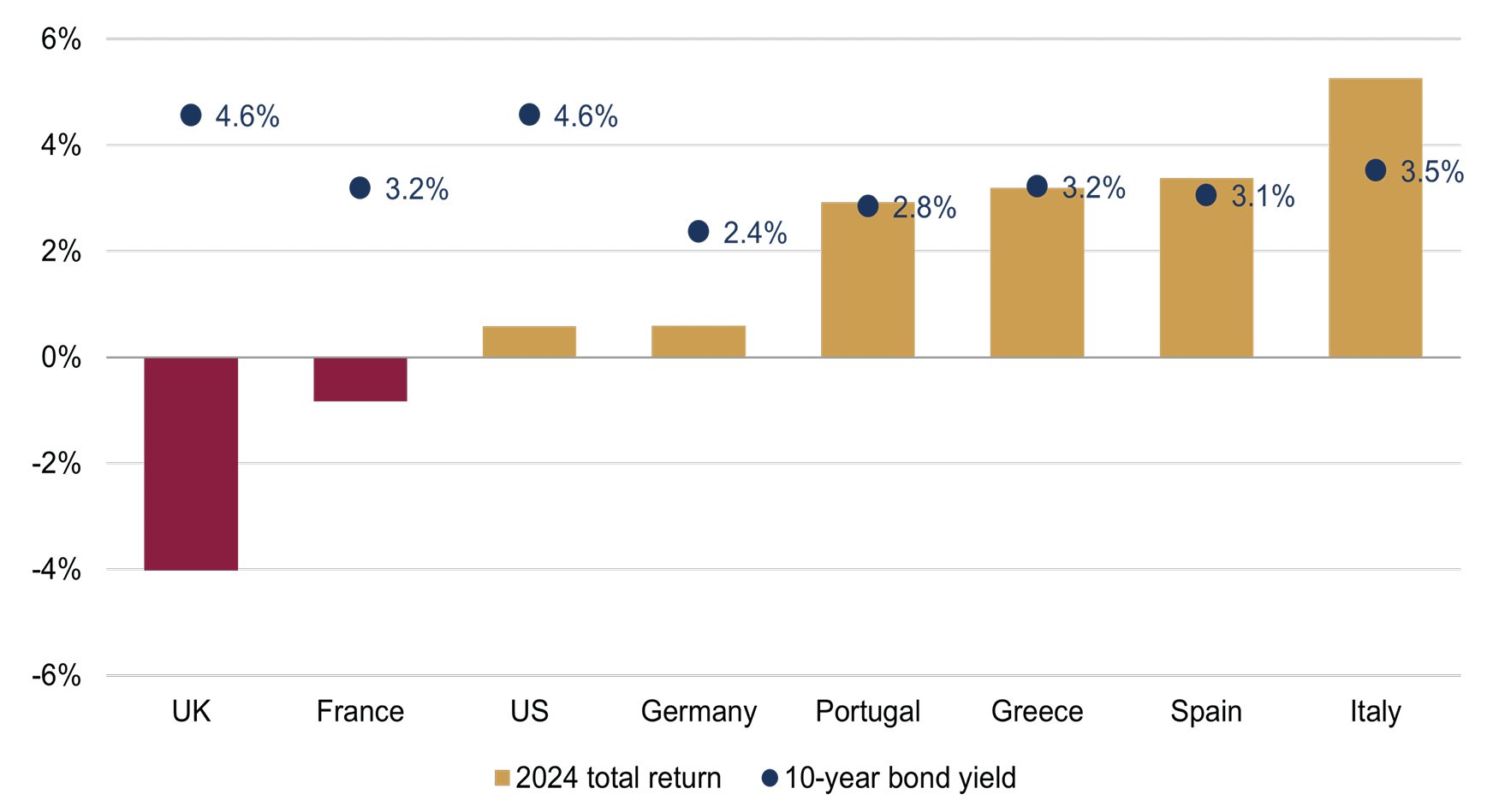

4. Bonds: have the vigilantes returned?

While stocks marched higher in 2024, bonds oscillated in response to varying growth rates, shifting politics, and, most importantly, the evolving interest rate backdrop. During the course of the year, central bank policy rates fell by 100 basis points (bps) in the US and eurozone, 50bps in the UK and 125bps in Switzerland. However, the expected level of policy rates at the end of 2025 actually rose in some of these economies, as it became clear that they were not about to collapse, and that inflation might be bottoming out. That favourable growth backdrop likely explained corporate bonds’ outperformance relative to sovereigns, with investment and speculative grade credit spreads (relative to those government bonds) narrowing to their tightest levels in over 15 years.

However, returns diverged markedly across high-quality government bonds: UK gilts were the worst performing, -4%, with 10-year yields rising by over 100bps over the course of the year; US treasury returns were slightly positive, despite the US 10-year yield rising some 70bps.

German bond returns were also modestly positive, though most notable perhaps was the outperformance of peripheral Europe – the so-called PIGS (Portugal, Italy, Greece and Spain) – where borrowing costs for many of these countries are now at levels comparable with that of traditionally more highly-rated France. This highlights the uncertain political situation facing the core of the eurozone, but it also speaks to a dramatic turnaround for these economies since the debt crisis a little over a decade ago.

Maybe PIGS can fly after all?

Government bond returns in 2024 (all-maturity, local, %) and current 10-year yield (%)

Source: Rothschild & Co, Bloomberg

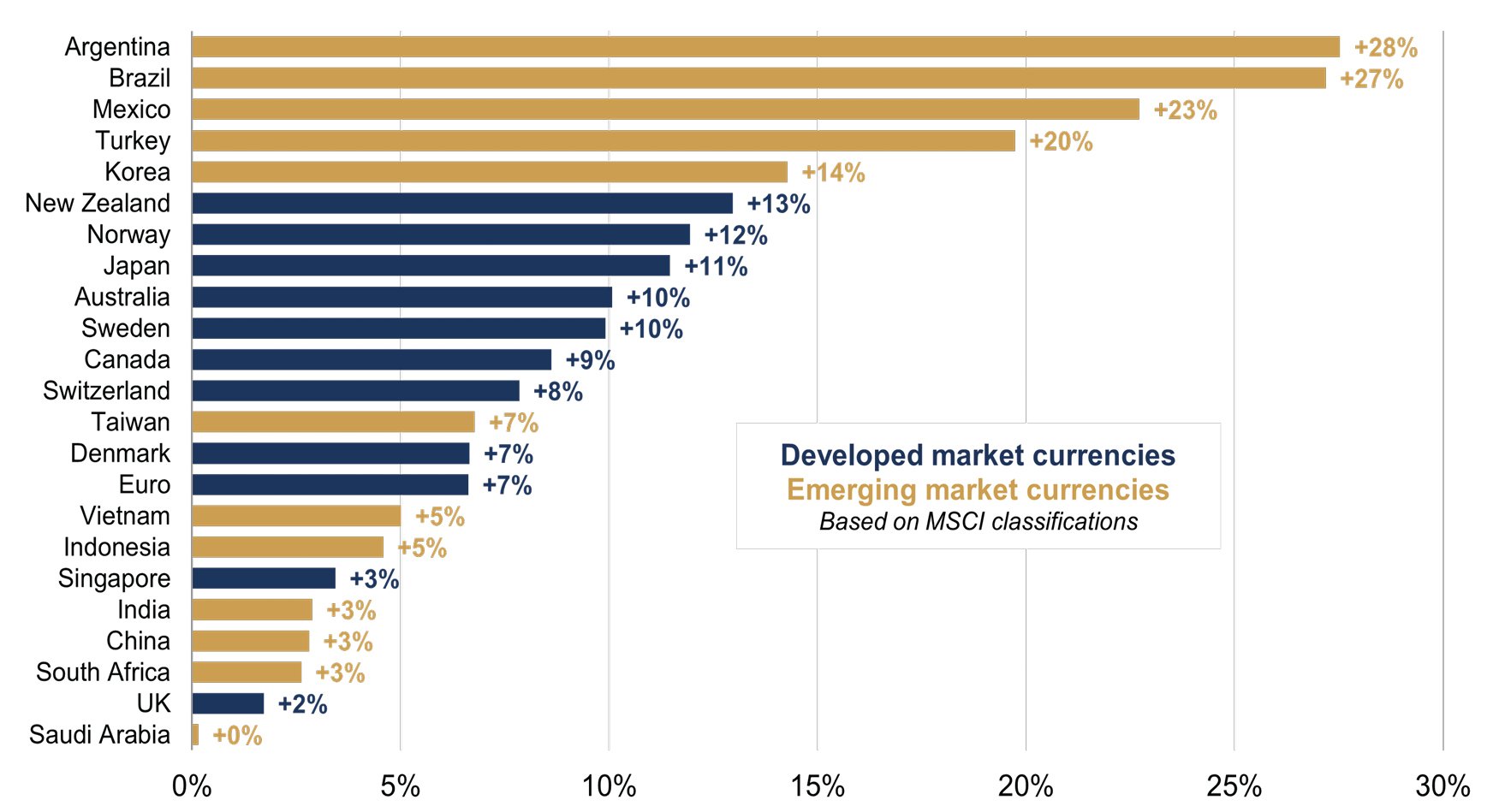

5. US dollar: from strength to strength

The US dollar had significant momentum in the final few months of 2024, appreciating the most in any calendar year since 2015, and now at a record high on a nominal trade-weighted basis (that is, comparing its value with a range of other currencies). It has indeed been a broad story: the dollar has appreciated against every G20 currency over the past year. The stronger greenback might have partly reflected better relative US growth and ‘carry’ (higher US interest rates may persist relative to elsewhere) – not to mention the return of MAGA. Arguably, with the dollar having outperformed most currencies most of the time in recent years, for many investors America has never not been ‘Great’…

The consequences for unhedged stock (and bond) investors have not gone unnoticed – the translation effect of a stronger dollar has amplified US stock market outperformance in common currency terms, dampening returns from other regions. For example, the Japanese stock market returned 21% last year for local investors – but for those located in the US, returns were closer to 8%. Conversely, UK stock returns were similar in both local and dollar terms, as the pound sterling was one of the more resilient currencies against the greenback.

Latin American currencies were particularly weak in 2024 – as they so often are – illustrating why we view these markets as prohibitively risky for private investor portfolios: there is more than enough volatility elsewhere, without adding this sort of risk.

US dollar appreciation relative to other nations' currencies

2024 (%)

Source: Rothschild & Co, Bloomberg

Looking ahead: 2025 and beyond

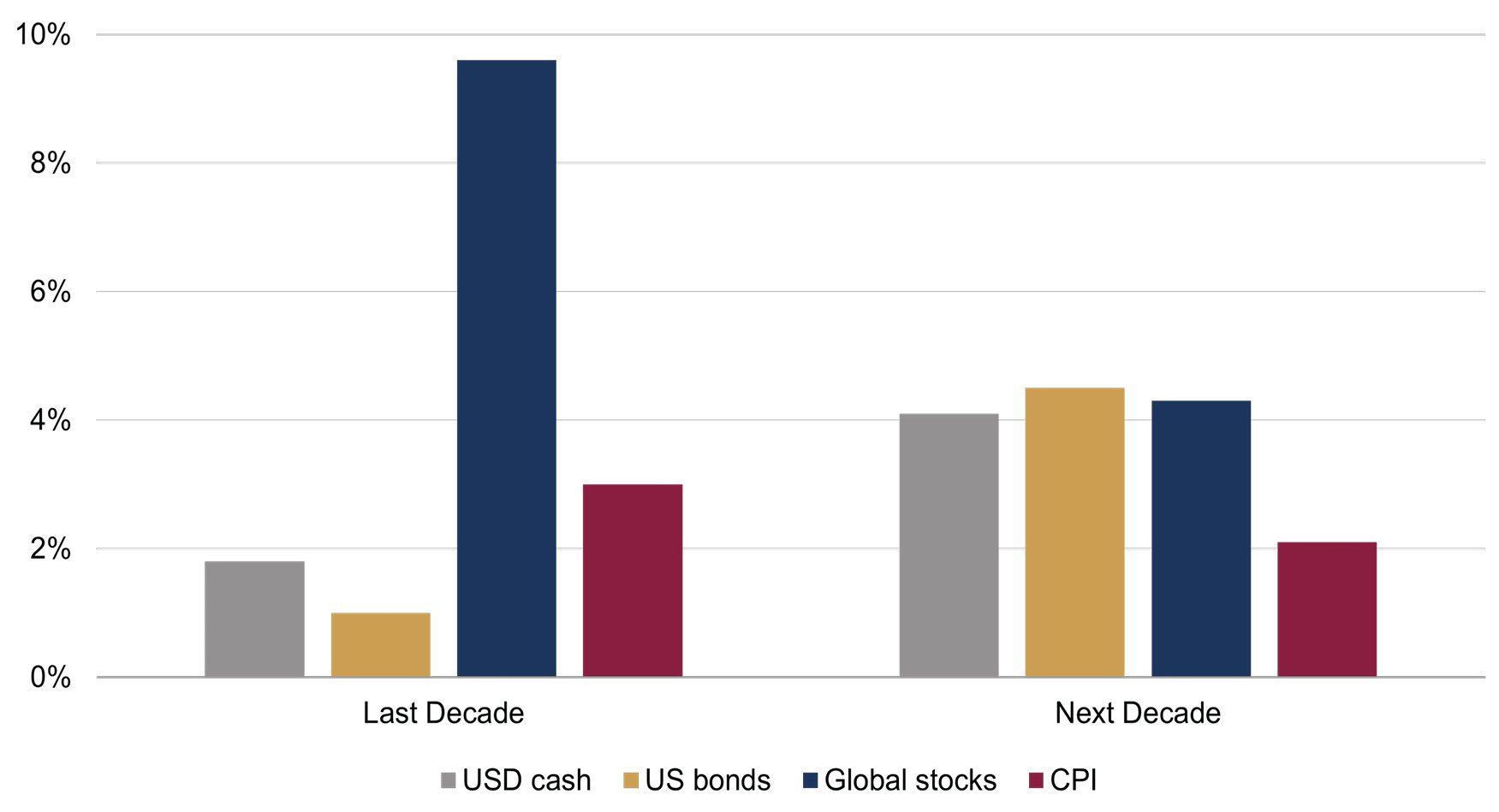

Without doubt this has been a favourable couple of years for stock investors, and a more challenging period for bond holders. However, stocks have now used-up considerable valuation headroom, and while valuations are not a good short-term market timing tool, there is a lot of ‘good news’ now in the price. With so much policy and political uncertainty, and inflation having bottomed out, we see the need for some near-term tactical caution.

None of this changes our constructive view on the business cycle, nor does it change our generally positive long-term outlook on growth and stocks. But as we see things, the plausible long-term returns we might expect from the major asset classes are closer together than they have been for many years – particularly with bond yields recently at levels that we might have considered ‘fair value’ historically (at least in the US and UK). While we should never try to optimise portfolios based solely on ‘top down’ prospective long-term returns, one thing is clear: the last decade was entirely about stocks – the future might look a little different. That said, we do still see likely returns on stocks and bonds outpacing prospective inflation – though doubtless not in each and every year…

Cross asset returns over the last 10-years vs prospective top down returns over the next 10-years

Annualised returns (USD, %)

Source: Rothschild & Co, Bloomberg, IMF, authors’ calculations

Note: Forecasts are not a reliable indicator of future performance. Data correct to 31st December 2024.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Citations

[1] The ‘Magnificent Seven’ are Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.