Trump and the dollar

The incoming US President has often said that he would like a weaker dollar. In his view, that will help ‘Make America Great Again’. It is possible, however, for a country’s exchange rate to be a result of its fortunes, not a cause of them, and that is how we see today’s strong dollar. With its relatively strong growth, reserve currency status, outperforming stock market and technological leadership, the US is already viewed pretty positively by investors. If the dollar is to fall significantly, they may need to be convinced, paradoxically, that America isn’t great.

Of course, what Trump has in mind in this context is one specific element of economic performance only, namely America’s trade deficit and associated loss of manufacturing market share, and the plausible possibility that this has something to do with the US’s ‘competitiveness’. Get the over-valued dollar to fall, and the trade deficit will go away.

The piece below addresses i) the main issues around Trump’s thinking on trade deficits and competitiveness; ii) the drivers of exchange rate fluctuations and the stronger dollar; and iii) the feasibility of devaluing the greenback.

The US is still competitive

To start with, it is not at all clear that the US’s trade deficit is a reflection of its competitiveness. Other things equal, if the US consumer spends more freely than those elsewhere, America will be likely to import more than it exports: the sheer scale of US household spending makes the US consumer customer number one for Global Inc. And many of the products exported to the US may differ from those available from home, leading much of US consumer demand to be sourced by imports, irrespective of their cheapness. If a consumption-driven slump were to occur, then the US trade deficit might narrow, but that would hardly be indicative of economic success.

Meanwhile, despite this trade deficit, the US is home to more innovative and profitable big companies than any other country. If US Inc is uncompetitive, nobody seems to have told Amazon, Apple or Microsoft.

Relative prices are not just driven by exchange rates anyway: productivity matters. The tendency for workers to gradually move up the learning curve and innovate over time, has helped to produce more with less. For example, Taiwan’s monopoly in producing the world’s most advanced semiconductors was not built overnight – and there is no guarantee either that the construction of semiconductor fabrication plants elsewhere will be able to match the price (and quality) of its chips. The fact that the Taiwanese currency has been relatively resilient against the dollar over the past decade may have partly been due to its semiconductor-related success.

(Less positively, relative inflation rates can matter too, but the US is not alone in having experienced an inflation surge of late).

Exchange rates: a lot of moving parts

When Trump labels other nations as ‘currency manipulators’, he is probably overlooking the complex mechanisms behind exchange rate fluctuations.

In a perfectly competitive, textbook world, exchange rates adjust based on the ratio of respective consumer price levels, the so-called ‘law of one price’. But inflation expectations, costs of carry (relative interest rates), local politics, capital market risks – and in the dollar’s case, its reserve status – also play an important role. Exchange rates can as a result diverge from purchasing power parity, or ‘fair value’, for long periods of time, just as the ‘expensive’ dollar has done over the past decade.

Some of these factors are reflected for example in Stephen Jen’s idea of the ‘dollar smile’ (previously noted here). It suggests that the dollar can rally during times of global crises due to its safe-haven, reserve currency status. But it can also strengthen when the US economy is performing relatively better, as investors flock to US assets and interest rates, leaving other currencies to do better only when the US is in the mediocre middle ground.

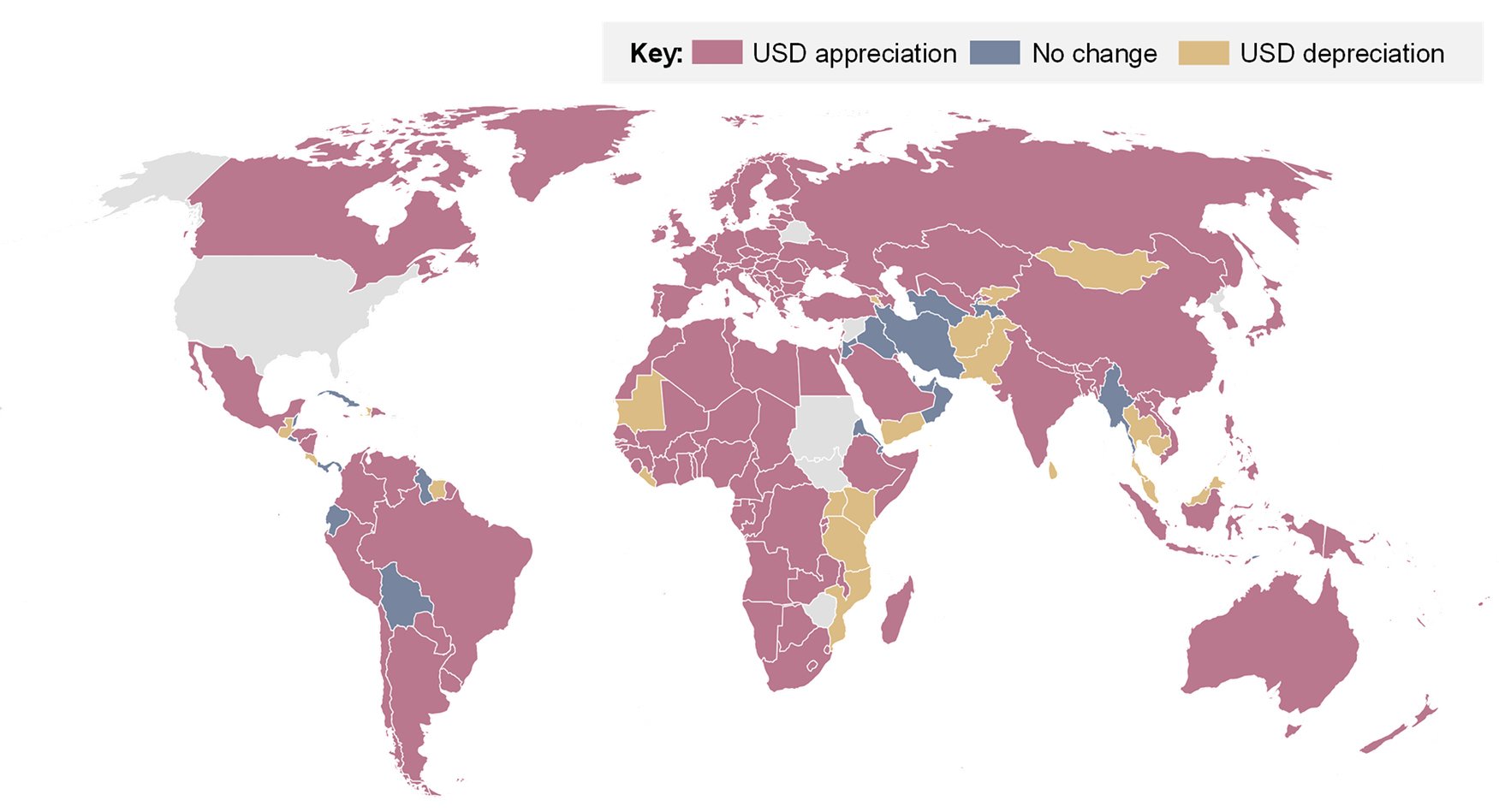

Last year’s broad-based dollar strength (figure 1) does seem to have reflected the US’s relatively strong growth and a backdrop of global instability – much of it followed the Republicans’ clean-sweep election victory in November, as Mr. Market saw Trump’s policies as likely to have a reflationary, pro-growth tilt.

Figure 1: US dollar spot returns (2024,%)

Source: Rothschild & Co, Bloomberg, Bing, Australian Bureau of Statistics, GeoNames, Microsoft, Navinfo, Open Places, OpenStreetMap, Overture Maps Foundation, TomTom, Zenrin

Note: Data unavailable for Belarus, North Korea, South Sudan, Sudan, Syria and Zimbabwe.

A Plaza Mar-a-Lago accord?

Sadly, the 47th US President is unlikely to read the above, and so may continue to focus on the trade deficit, and to blame it – and his idea of poor US competitiveness – on the stronger dollar. How feasible is it for him to get the dollar down?

The most controversial option would be for him to lean on the Federal Reserve to cut interest rates, interfering with its independence. But this extreme scenario would be counterproductive: the impact it would have on capital markets, and the US government’s borrowing costs, would be big.

Another option might involve the Treasury using its Exchange Stabilization Fund to buy foreign currencies, but it would have to purchase huge quantities, given the sheer size of today’s currency markets (daily global turnover is reportedly in the trillions of dollars). History has not been kind to governments which have indeed decided to manipulate their currencies – in either direction.

Taking the above a step further, the US could try to conduct more coordinated action, similar to the famous Plaza Accord of 1985. Back then, the dollar had also experienced a sharp appreciation in the years leading up to it – amid Volcker’s tighter monetary policy stance and Reagan’s expansionary fiscal policies – which prompted the G5 cohort to bring down the value of the greenback (until the Louvre Accord in 1987).

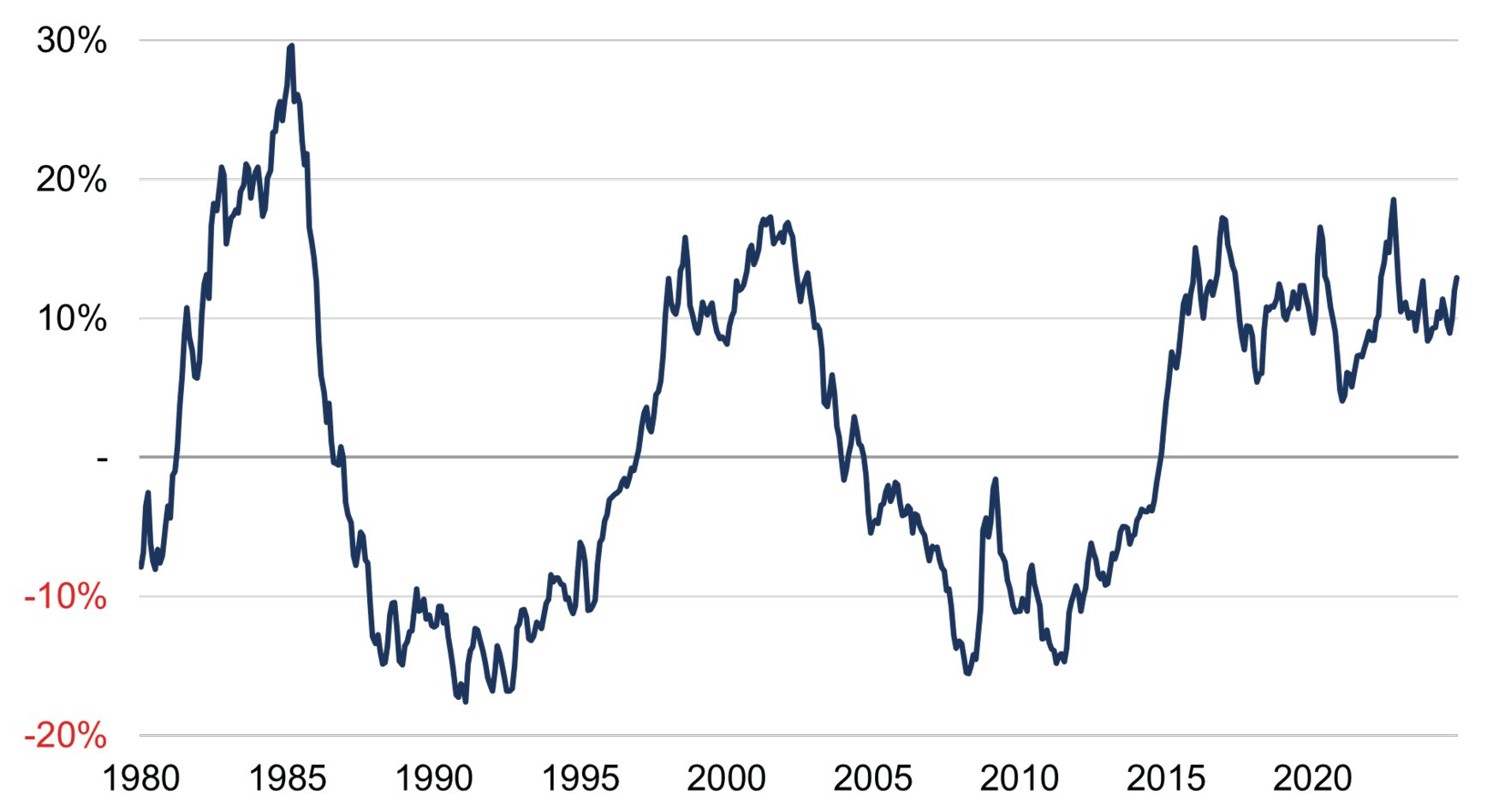

If something similar were attempted now, Trump would likely want the major economies and what it deems to be today’s ‘manipulators’ (China) involved. But it may not be in their interest. China, for instance, is trying to revive its sluggish growth (that is, when judged by its own high standards), and so raising local interest rates would not be a welcome development. And the dollar simply doesn’t look that expensive – in contrast to the mid-1980s – when looking at its real (or inflation-adjusted) trade-weighted exchange rate relative to its trend (figure 2).

Figure 2: US real effective exchange rate (relative to 10-year trend,%)

Source: Rothschild & Co, Bloomberg, OECD

Conclusion

And so, Trump may simply have to wait until other nations start to perform better for the greenback to soften significantly, or stop thinking about a weak dollar being needed to ‘MAGA’. While we can’t rule out any dollar devaluation attempts, this might just be another example of where it is better to take him ‘seriously, but not literally’.

This does not mean that Trump is wrong to talk of an uneven playing field in global trade: as we have noted many times, China, not the US, is the most protected ‘big’ economy. But this unfair competition is best addressed directly: if China’s markets are closed, even a bargain basement dollar will not get US Inc better access. Such a direct address does not have to involve tariffs…

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.