August: a short-lived panic?

Investment Communications Team, Investment Strategy Team, Wealth Management

Summary

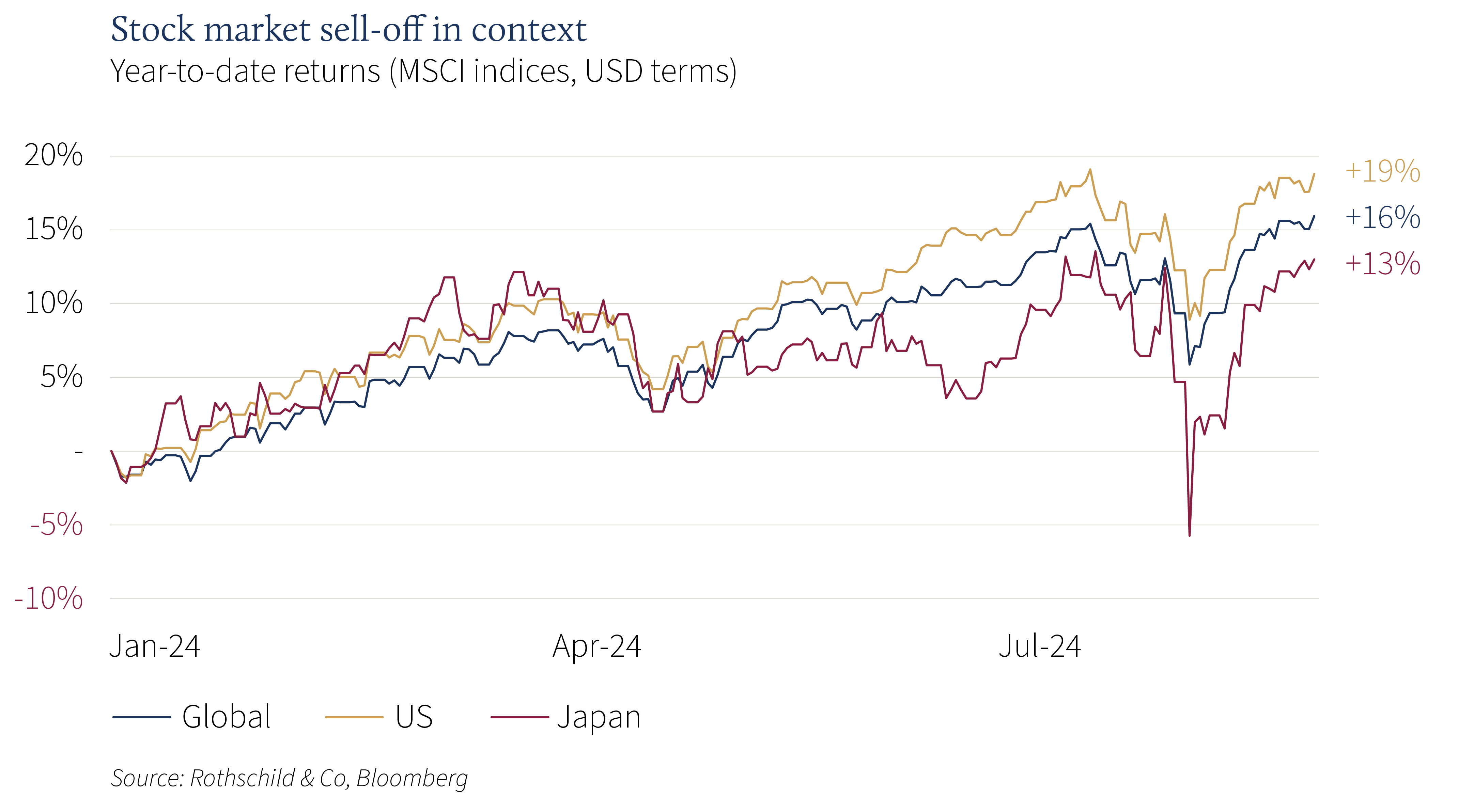

Global equities moved higher by 2.5% in August (USD terms), while global government bonds returned 1.0% (USD, hedged terms). Key themes included:

- Stocks rebound to fresh highs after a sharp sell-off at the start of the month;

- Powell signals that the Fed will begin its easing cycle in September;

- Uneasy geopolitics deteriorates further in the Middle East and Ukraine.

Markets: A brief re-emergence of volatility

Stock volatility surged at the start of the month as thin summer trading coincided with US growth fears, the retreat of ‘big tech’ and the technical unwind of Japan’s carry trade. The VIX Index – a measure of S&P 500 implied volatility – almost tripled intraday, before swiftly returning to more ‘normal’ levels. Most damage was evident in Japan, where a big surge in the yen prompted a 12% daily decline in the MSCI Japan Index (local terms). However, global stocks quickly retraced their losses, back to all-time highs, though there was a more ‘defensive’ sector rotation in August. Safe havens rallied, with shorter-dated government bonds rallying most visibly (and the 2s10s US treasury curve briefly uninverted). Gold also rose further, subsequently hitting fresh highs in US dollar terms, as the major currencies – including EUR, GBP, CHF and JPY – continued to strengthen against the greenback. Oil remained rangebound, despite the tense situation in the Middle East.

Economy: Signs of a US slowdown?

US economic data were more mixed over the past month. Retail sales pointed to ongoing consumer momentum in July, but cracks started to show in the labour market data. The unemployment rate unexpectedly rose to 4.3% – its highest reading in nearly three years – and the pace of job gains decelerated. Even so, the timely business surveys signalled expansion in August, and real-time US GDP estimates pointed to another quarter of economic growth. Meanwhile, inflation continued to cool: the headline rate edged lower to 2.9% (y/y), as did the core rate, to 3.2%. In Europe, the UK was the fastest growing G7 economy in the first half of the year, with activity also looking healthy at the start of the third quarter. Euro area data were patchy: business surveys signalled overall expansion, but manufacturing output remained subdued. Eurozone headline inflation fell to 2.2% in August, while UK headline inflation conversely moved up to that same rate in July, with energy price arithmetic (base effects) affecting both series. Swiss inflation remained unchanged – and muted – in July.

Policy and politics: The Powell pivot; Uneasy geopolitics

With growth concerns and market volatility in focus, money markets quickly discounted a more dovish trajectory for US interest rate cuts this year (currently close to 100 basis points of easing, even after stocks rebounded). At the annual Jackson Hole summit, Powell stated that ‘the time has come for policy to adjust’, a clear signal that the Federal Reserve is set to begin its easing cycle in September. Policymakers from the other major central banks also hinted that interest rates would continue to move lower, with the exception being the Bank of Japan.

The geopolitical backdrop remained tense. Conflict in the Middle East escalated further, despite ongoing ceasefire talks, and Ukraine’s forces advanced into Russia’s Kursk region. On a more positive note, there was further US-China dialogue, as the US National Security Advisor met with Xi Jinping in Beijing. In politics, Kamala Harris confirmed Tim Walz as her Vice President nominee at the Democratic National Convention. Voter-friendly policies aimed at working families were revealed, while the latest polling showed a slim lead over Trump. Elsewhere, Japan’s PM Kishida stepped down amid low popularity, Macron failed to form a new government in France, and the far-right AfD won its first state election in eastern Germany.

Performance figures (as of 30/08/2024 in local currency)

| Equity (MSCI indices $) | Month | Year |

|---|---|---|

| Global | 2.5% | 16.0% |

| US | 2.4% | 18.8% |

| Continental Europe ex. Switz. | 4.0% | 11.5% |

| UK | 3.3% | 15.1% |

| Switzerland | 4.8% | 11.7% |

| Japan | 0.5% | 13.0% |

| Pacific ex Japan | 4.7% | 7.2% |

| EM Asia | 1.6% | 12.5% |

| EM ex Asia | 1.6% | -1.1% |

| Fixed income | Yield | Month | Year |

|---|---|---|---|

| Global Govt (hdg $) | 2.98% | 1.0% | 2.7% |

| Global IG (hdg $) | 4.55% | 1.2% | 3.7% |

| Global HY (hdg $) | 7.71% | 1.8% | 7.6% |

| US 10Y ($) | 3.90% | 1.4% | 2.7% |

| German 10Y (€) | 2.30% | 0.4% | -0.1% |

| UK 10Y (£) | 4.01% | 0.3% | -0.4% |

| Switzerland 10Y (CHF) | 0.48% | 0.0% | 2.3% |

| Currencies (NEERs) | Month | Year |

|---|---|---|

| US Dollar | -1.2% | 2.8% |

| Euro | 0.5% | 1.3% |

| Pound Sterling | 0.5% | 4.1% |

| Swiss Franc | 1.8% | -0.6% |

Table note: NEERs under ‘currencies’ are the JP Morgan trade-weighted nominal effective exchange rates

| Commodities ($) | Level | Month | Year |

|---|---|---|---|

| Gold | 2,503 | 2.3% | 21.3% |

| Brent Crude oil | 79 | -2.4% | 2.3% |

| Natural gas (€) | 40 | 11.0% | 23.1% |

Source: Bloomberg, Rothschild & Co.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.