Growth Equity Update

March 2025 – Edition 36

- The Mansion House Reforms and UK growth equity funding: We deep dive into the UK’s Mansion House Reforms, first announced two years ago and subsequently advanced by new Chancellor Rachel Reeves with her assertion that ‘economic growth is the number one mission of this government.’

- UK pensions are underinvested in private assets: 2021’s $300m investment by Canadian Pension Plan Investments in Octopus Energy was bigger than the total 2022 investment by UK pension funds in UK start-ups. Australian pension funds are estimated to invest 10x more in private assets than UK DC pension funds.

- The Mansion House Initiative has ten of the UK’s largest pension providers committing 5% of ‘default’ funds from DC pensions to private assets by 2030, hoping to free up £75bn of growth financing. The government has said it may sponsor ‘further interventions ... to ensure that these reforms, and the significant predicted growth in DC and LGPS fund assets over the coming years, are benefiting UK growth.’

- In its recent letter to investors Stripe observed that while the US invests around 0.7% of GDP in high growth firms, that figure is less than 0.3% in Europe.

- Save the date: Rothschild & Co is hosting a London conference on 10th June – Funding the UK innovation Economy- Delivering on the Mansion House Compact.

- Markets in 2025: ‘Trumpcession’ versus a reinflating Europe? The turnabout in relative US/European index performance continues. Ytd to 10th March the Euro STOXX 600 is +7% and the FTSE100 is + 4%. US indices are in negative territory with the S&P 500 -4%, NASDAQ -9% and the Lagnificent 7 down 15%.

- February – VC investment keeps up the pace: 2025 has started strongly for the Growth Equity market on both sides of the Atlantic. To the end of February our US Deal Monitor is at $18.7bn, up 72% yoy with Europe at $7.4bn up 20% in value yoy.

- More to come: March has started strongly with Anthropic’s $3.5bn raise at a post money valuation of $61.5bn. Another $53bn of deals are close, led by $40bn for OpenAI and $10bn for xAI.

- “Don't wait for the right opportunity: create it.” George Bernard Shaw

Click here to download a PDF version of Growth Equity Update

The Mansion House reforms and Venture Capital funding in the UK

‘Economic growth is the number one mission of this government. Low growth is not our destiny... but growth will not come without a fight.’ Rachel Reeves – UK Chancellor of the Exchequer.

UK Venture Capital – a funding problem: A common observation of UK VC backed businesses is that there is a funding gap as they progress out of the seed and Series A stages. The perception is of a dearth of UK based funding for Series B and C scale up raises and that companies must resort instead to seeking backers from overseas.

This is supported by an August 2024 report from the British Private Equity and Venture Capital Association (BVCA) which found that only 3% of pension fund investment in British private capital comes from UK pension funds. It also found that foreign investment in UK deals makes up an increasing share of deal value. In 2023 87% of £20m-50m deals and almost 95% of deal value over £50m included foreign investors.

The BVCA concluded ‘The data indicates that the increasing importance of foreign investment is due to the UK not having sufficient funds of scale to invest in deals over £20m. To fix this domestic funding gap, the UK needs to create the right framework for larger VC funds that can enable more businesses to achieve rapid growth without relying on overseas investment. An important part of the solution is to unlock greater levels of domestic institutional investment such as UK DC pension schemes, through initiatives like the British Business Bank’s Growth Fund or a UK TIBI scheme.’

The UK government cites survey data suggesting that UK pension schemes have one of the lowest proportion of funds held in domestic stocks and private assets. A March 2023 survey by New Financial concluded that:

- Over the past 25 years, UK pension funds have reduced their allocation to equities from 73% to 27% -and their allocation to UK equities from 53% to just 6% while quadrupling their allocation to bonds to 56%. UK pensions now have the highest allocation to bonds and lowest allocation to equities of any comparable pension system in the world

- Since 2000, the share of the UK stock market owned by UK pensions and insurance companies has fallen from 39% to just 4%. Only 1% of the £4.6 trillion in pensions and insurance assets is invested in unlisted UK companies.

Separately the government has noted that the investment of $300m by the Canadian Pension Plan Investments in Octopus Energy in 2021 was bigger than the total investment by UK pension funds in UK start-ups in the whole of 2022. Australian pension funds are estimated by the UK government to invest ten times more in private assets than UK DC pension funds.

The Mansion House Reforms: The new UK government has a growth agenda and appears determined to help address this gap. In doing so it is picking up on the original Mansion House Reforms announced by the then Chancellor of the Exchequer, Jeremy Hunt, in July 2023. The key initiative was to ensure the channelling of some part of defined contribution pensions into private companies.

At its heart was an agreement signed by ten of the UK’s largest pension providers to commit 5% of their ‘default’ funds from defined contribution pensions to private companies and start-ups by 2030.

The ten DC pension schemes to sign up to the Chancellor’s ‘Mansion House Compact,’ representing around two-thirds of the UK’s DC workplace market, are Aviva, Scottish Widows, L&G, Aegon, Phoenix, Nest, Smart Pension, M&G, Aon and Mercer. At present such funds invest just c0.5% of their c$500bn of assets in unlisted UK companies.

The intention was that, if the scheme was also taken up more broadly by other pension providers, the proposed changes could induce c£50bn of additional investment in start-ups by 2030.

Mr Hunt also targeted a shift in the investment intentions of local government pension scheme allocations. The aim was to encourage such schemes to double investments in private assets to 10% from c5% presently, unlocking another c£25bn in additional investment into private companies, a total of an additional £75bn of financing for growth by 2030.

According to Mr Hunt this would enable 'our financial services sector to increase returns for pensioners, improve outcomes for investors and unlock capital for our growth businesses' and thus 'finally address the shortage of scale up capital holding back so many of our most promising companies.'

Growth – the ‘number one mission’ under Labour: The new Labour Government also has a strong growth agenda with Chancellor Rachel Reeves having declared that growth is the ‘number one mission.’

Superfunds: In her own November 2024 Mansion House address the new Chancellor built on the work of her predecessor with a ‘superfund’ scheme to pool assets from the UK defined contribution pension sector and local government pension schemes.

Two consultation programmes are underway with a report due by summer 2025. A core concept for the government is that current pension schemes may be too small to take advantage of a full range of investment opportunities. The government’s preferred size for DC schemes and Master Trusts is assets under management of £25bn-£50bn, thought to be the scale at which funds would be better able to access a wider range of investment opportunities notably in infrastructure projects and in private equity, venture capital and unlisted equities.

‘The government is clear that the future of the workplace DC market lies in fewer, bigger, better run schemes, with the scale and capability to invest in a wide range of asset classes, such as private equity and infrastructure, that can deliver better returns for savers long term and boost investment in the UK, which benefits savers and their communities.’

In addition, the assumption is that private market pension portfolios tend to invest more domestically

‘The Review is encouraged by clear evidence that where pension schemes are managing private market portfolios, they tend to operate a significantly higher domestic weighting than in more liquid asset classes. This strengthens the case that these reforms driving scale and unlocking greater alternative investments will benefit UK growth.’

The government is thus hoping to consolidate the c£800bn (by 2030) Direct Contribution workplace market. Key proposals include:

- the introduction of minimum size requirements and limits on the number of default fund arrangements for multi-employer schemes.

- permitting schemes to avoid the need for individual consent to the bulk transfer of assets in contract-based schemes.

- requiring DC scheme trustees to focus more on investment return than cost. The government consultation paper observes ‘There has been a consensus for some time that the DC market is not operating effectively. An excessive focus on keeping costs down has come at the expense of considering a broader range of metrics of scheme quality such as effective governance and net investment returns.’

Meanwhile the local government pension schemes (LGPS) hold £392bn of invested assets. Since 2015, the 86 administering authorities have come together in eight groups of their own choosing to move towards managing their investments through eight LGPS asset pools. Here the government proposes:

- requiring the LGPS funds to delegate the management of their assets to one of the eight existing asset pools.

- and obliging them to consider local growth opportunities in their investment strategies

The Government has more control over the local government schemes where it hopes that the asset pooling exercise may be completed by March 2026.

The DC scheme changes, if they happen at all, are unlikely to come into effect before 2030. There is also likely to be some time before the changes to headline investment strategy feed down into execution.

Accelerating the progress: There is of course the opportunity to move more quickly in the interim. Baroness Stowell, the Chair of the House of Lords Communications & Digital Select Committee has commented that '2030 is all very well, but we need to accelerate the process.'

Some are already moving to fill the gap. In February 2025 Cambridge Innovation Capital, an early-stage fund focused on science start-ups, launched the new £100m CIC Opportunity Fund. It was supported by, amongst others, British Patient Capital and Aviva Investors, contributing £20m and £15m respectively.

British Patient Capital Limited is a subsidiary of British Business Bank plc, the UK government’s economic development bank whose mission is to enable long-term investment in innovative firms. Launched in June 2018, British Patient Capital has £3bn of assets under management, investing in venture and venture growth capital to support high growth potential UK businesses in accessing long-term financing. Aviva, meanwhile, is one of the ten initial signatories of the Mansion House Compact.

Some pushbacks: The proposed changes have ignited discussion on a range of issues, notably:

- Scepticism that size is a critical factor in limiting pension fund investment in the UK.

- Concerns that pension funds should be focused on their duty to maximise members returns rather than act as promoters of a UK investment agenda.

The UK government though has determined that the use of pension fund capital is a key priority in promoting a more entrepreneurial spirit in the UK with pension managers encouraged in ‘responsible and informed risk taking’ as a ‘prerequisite for growth’.

Indeed, the government has indicated to the pensions industry that failure to back UK investment may provoke ‘further interventions ... by the government to ensure that these reforms, and the significant predicted growth in DC and LGPS fund assets over the coming years, are benefiting UK growth.’

Pensions Investment Review Interim Report

Meanwhile a number of fund managers have launched initiatives to support the agenda of the Mansion House Reforms. Many of these are building on the LTAF (Long-Term Asset Fund) ecosystem established by the FCA in November 2021 to ease investment in illiquid long-term assets like private equity, infrastructure and real estate.

Future Growth Capital: One of the first private market investment managers to be established in the UK to promote the objectives of the Mansion House Compact is Future Growth Capital set up in July 2024 by Phoenix Group and Schroders.

Phoenix is the UK’s largest long-term savings and retirement business with 12 million customers. Schroders is a global investment manager with a £74bn private market capability.

Phoenix intends to invest 5% of its relevant savings products on behalf of its policyholders, in line with its Mansion House Compact commitment. This will provide scale at inception, with fundraising thereafter led by both Schroders and Phoenix Group. The intention is that Future Growth Capital will support the objectives of the Mansion House Compact, allowing investment opportunities in private markets for pension savers. FGC aims to deploy an initial £1bn, and £10-20bn over the next 10 years into UK and global private markets.

FGC will design and manage UK and Global multi-private asset solutions for UK insurance and pension clients leveraging Schroders’ LTAF investment platform in its dedicated private markets business, Schroders Capital.

Aviva Venture and Growth Capital Fund: Aviva is one of the UK’s leading insurance, wealth and retirement businesses with 20.5m customers, including 4m pension customers, and assets under management of £407bn. In February 2025 it launched the Aviva Investors Venture & Growth Capital LTAF, its fourth LTAF fund. The fund will receive an initial c£150m commitment from Aviva, through a combination of assets and cash commitments and will to provide opportunities for its 4m members across 26,000 corporate pension schemes in Aviva’s default DC workplace pension business to support investment in private markets.

The fund will have a UK bias and invest across multiple venture and growth stages in the UK, Europe, and North America, with a focus on Fintech and Insurtech; Healthtech; Science and Technology; and Climate and Sustainability. Venture investments will be made through third-party funds and evergreen vehicles to access a wide range of external managers, co-investment opportunities and deal flow, with direct investment in later-stage opportunities helping to scale-up growth companies.

One of the initial moves by the fund has been its £15m investment with Cambridge Innovation Capital.

L&G Private Markets Access Fund: In July 2024 L&G unveiled its L&G Private Markets Access Fund, offering its 5.2m defined contribution members access to private markets.

The new fund will employ L&G’s £48bn private markets platform to offer investments in areas such as clean energy, affordable housing, university spinouts, and critical infrastructure. Up to 40% of the portfolio will be invested in the UK. L&G plans to deploy up to £1bn by the end of 2025.

L&G will make use of the LTAF regime structuring the initiative as a Fund of Funds, with an investment in the Legal & General Private Markets LTAF, sitting alongside exposure to liquid securities, as well as L&G and third-party funds. The fund will include a range of private market assets, including private equity, real estate, private credit, and infrastructure.

Aegon Universal Balanced Collection Fund: In July 2024 Aegon included private market assets as part of its DC default offering. The £12bn Universal Balanced Collection fund will introduce private market investment and enhanced ESG integration. Aegon will partner with three fund managers.

BlackRock will manage a diversified alternative private markets strategy, including private equity, private debt, real estate and infrastructure. Aegon Asset Management will manage a new multi asset credit mandate which includes global high yield, asset backed securities and emerging market debt strategies from H2 2024, and JP Morgan Asset Management will manage a strategy, offering exposure to private equity, infrastructure and forestry. Aegon expects much of this investment to be in unlisted equities aligning with its Mansion House Compact aim to invest at least 5% of its default fund assets in unlisted equities by 2030.

Torsten Bell was appointed as pensions minister in January 2025. He has sought to assuage pension trustee fears that the government’s initiative to promote pension investment in the UK and in private assets rather than investing in overseas markets is potentially at odds with maximising the financial returns for UK pensioners.

Quoted in the FT Elaine MacGregor, legal director at Pinsent Masons, has commented that ‘any reforms proposed by the government which could be seen as either diluting fiduciary duty or mandating investment decisions at the expense of returns will likely be strongly resisted by pension funds’.

Speaking at an investor conference in early March Torsten Bell he noted there is ‘talk about the tensions between the interests of the economy as a whole and those of pension savers. Those tensions can exist in some cases, but they are often overdone…A better economy underpinned by higher investment... is in everyone’s interests’ stating that the UK 'cannot continue being the lowest investor in the G7.’

‘Active, engaged owners are what this economy needs more of... scale doesn’t make that inevitable, but it makes it significantly more likely … The largest source of UK domestic capital matters in terms of its returns to savers but it also provides the financial plumbing for our economy and our capitalism. I think we’ve forgotten that in previous decades too often, but we are not forgetting it today.’

Mansion House – Dissenting voices

There is not universal acceptance that the government’s proposed reforms are the best solution for the promotion of economic growth and returns for investors

An interesting report by VenCap, an investment management and advisory firm focused on investing in venture capital funds, makes the case that the UK is not short of VC investment but has not managed to maximise returns in the asset class.

The report is here.

It agrees that venture is an asset class that can produce higher returns for pension investments. Using Cambridge Associates VC index and Benchmark statistics, it cites a 16.5% annualised return for the global VC industry compared to 9.1% for the S&P500.

It argues however that the UK is not as effective in its VC industry as the US. It makes three assertions:

- That there is no shortage of investment capital for the best companies in the UK and that the issue is instead that the UK lags significantly behind the US when it comes to scaling and exiting these businesses.

- That UK venture capital funds have historically underperformed their US counterparts in delivering realised returns to investors.

- That venture capital is a 'power law' asset class. Returns are driven by just a handful of companies each year. The vast majority of these companies are located outside of the UK making it hard for venture firms focused on the UK to achieve the highest returns.

Clearly the latter two assertions are connected. VenCap then observes that the dispersion of returns within venture capital is much wider than in other asset classes meaning that investors need to be in the top-quartile VC funds to generate the outperformance offered by venture capital.

Looking at these assertions:

No shortage of UK growth capital? The government’s aim is to release growth capital out of the pension industry to fund venture capital. The Pitchbook data presented in the exhibit below suggests that UK VC backed companies may not lack capital.

It shows that UK VC companies are behind only the US and China in terms of the amounts raised in VC investment and that, as a percentage of GDP, the UK is at the top of the rankings in VC investment.

Venture capital investment as a percentage of GDP

The next exhibit, also derived from Pitchbook, looks at the distribution of VC money between the various growth phases in the UK and US. Overall, the weightings are very similar with 63%/62% of US/UK investment aimed at the later stages.

The distribution of growth capital by stage – UK and US compared

UK companies have thus been successful in attracting VC investment and its distribution between the growth stages is similar to that in the US.

A key difference is the sheer scale of the US means that the absolute pools of investment monies are much larger in the US. The European investment Fund made this point in a report in September 2023. It noted that:

- there are at least 7x more large-size (>€600m) VC funds in the US than in Europe.

- the average VC-backed company in the US receives five times more backing than its European peers.

- large US private equity and venture capital players have been building teams in Europe to look for regional opportunities, with the intention to fill the scale-up gap on the European market. As an example, US pension funds hold a €4.7bn stake in German startups, whereas German retirees have an exposure of just €94m.

In its 2024 State of European Tech Report 2 Atomico also highlighted the funding gap between the US and Europe. It states:

‘The funding gap between Europe and the US is bigger than people think. While the share of companies founded in 2015 that go on to raise at least a $1m round is similar between the US and Europe (22% versus 18%), the gap widens by the time companies reach $5m. The proportion of US companies able to raise rounds of $15m or more is twice that of Europe, 8.3% versus 4.1%. Atomico surmises that while Europe has raised $300bn in tech growth-stage rounds since 2015, the amount would have been double if European companies had had the same access to capital as their international peers.’

Share of tech startups founded in 2025 that raise minimum sized round

UK venture capital funds have historically underperformed their US counterparts in delivering realised returns to investors. Venn Capital asserts that the area of relative underperformance is mainly in achieving successful exits. The next exhibit indicates that the US and China’s percentage of exit value exceeds that of their invested capital whereas the UK (in common with European countries) lags with an exit rate just over 60% of the invested capital rate. The UK does worse when considering big exits - $1bn plus – with the exit rate percentage falling to 2.8%.

VC Exit rates as a % of invested capital

These figures are naturally reflected in the ability to deliver realised gains back to investors.

Realised VC gains – The US and UK compared

Returns are driven by just a handful of companies each year giving the UK a problem as the vast majority of these companies are located outside of the UK. The argument then focuses on the nature of returns in VC investment where the bulk by volume of companies in which VC invests produce minimal or negative returns (82% of a sample of 9,000 produced <1x to 1-3x).

A very small proportion producing the bulk of returns (4.6% produce 10x+) with just 1% being the ‘fund returners’ – super successes which return the value of the entire fund.

Pitchbook calculates that over the last ten years, the top 1% of VC-backed exits (around 33 companies a year) have generated circa 50% of the total exit value created by the VC industry globally.

Since 2014, the median value of a top 1% exit has been $4.3bn, while the average value is $8.3bn. Pitchbook data indicates that six UK VC backed companies have exited at a value over $4.3bn in the last twenty years and only two (Wise, Deliveroo) have exceeded $8.3bn. Ther implication is that UK VC returns to investors will always lag unless there is a greater flow of these super successful companies.

Meanwhile what about pension funds in the UK trying to capture VC performance? The assertion is that the outsized performance of VC is captured not across the industry but only in the very top funds – VC cannot be indexed.

The vast majority of VC-backed companies lose money for their investors and most VC funds fail to produce acceptable risk-adjusted returns. So, UK pension funds would need to access the funds invested in the top 1% of exits and, at the moment, these are mainly coming from companies outside of the UK and likely to be owned by global rather than UK VC firms.

There is some comfort in the latter point from a report produced in mid-2024 by Invest Europe using data from the US based Cambridge Associates. The report suggested that European VC returns are better than US returns over a 10 and 15 years horizon with the US outperforming on a 20 year basis.

IRR of European and North American VC funds

The distribution of IRRs though emphasises the relative paucity of opportunity to invest in the best performing VC funds. Of the 223 European funds raised between 1986-2023 that were surveyed, 162 remain active. Of these just 14 (8.6%) had an IRR of more than 30%. Just one had an IRR of 100% plus.

Stripe- another liquidity round

Stripe has confirmed it has signed agreements with investors to provide liquidity to current and former employees through a tender offer at a $91.5bn valuation.

Fintech Stripe has a habit of conducting private rounds to provide liquidity for its employees and shareholders.

In March 2023 Stripe Inc raised $6.5bn in a funding round to address the Restricted Stock units (RSUs - share incentives) which the company had for some years built into the compensation packages of key employees.

Stripe cofounder and president, John Collinson commented:

‘The funds raised will be used to provide liquidity to current and former employees and address employee withholding tax obligations related to equity awards, resulting in the retirement of Stripe shares that will offset the issuance of new shares to Series I investors. Stripe does not need this capital to run its business.’

Some $3.5bn of the $6.5bn was to be used to cover the tax obligations arising from the RSUs with the rest being used to buy shares from employees who wished to sell.

The $6.5bn raise valued Stripe at $50bn, 47% below its peak valuation of $95bn in March 2021.

In March 2024, Stripe again facilitated the sale of shares by employees establishing a tender offer with Goldman Sachs Growth Equity and Sequoia and funds from Stripe’s own resources. The tender offer was for c$1bn of stock at a price valuing Stripe at $65bn, 30% higher than the 2023 level.

Stripe has repeated the manoeuvre in March 2025. The company has signed agreements with investors to provide liquidity to current and former Stripe employees through a tender offer at $91.5bn, just 4% below its peak valuation of $95bn in 2021. Alongside investors, Stripe will also repurchase shares. John Collinson observed:

'We very much care about providing good liquidity for employees and existing shareholders.’

In interviews he stated that the company has been profitable for two years and should continue to be so for the foreseeable future. John Collinson has repeated that Stripe has no plans for an IPO.

‘We’ve stayed private longer than most tech companies, and that’s been a positive. We can plough profits back into R&D. But we’re not dogmatic… We decide what’s best for the business on an ongoing basis.'

At this stage last year, he observed:

'With the IPO, we’re not in a rush. Businesses which are profitable have many, many more options than businesses which are dependent on outside capital.'

Meanwhile Stripe has issued its annual letter in which it updates on its business and opines about the state of the tech industry. In the 2025 letter Stripe’s founders observe:

- Businesses on Stripe generated $1.4 trillion in total payment volume in 2024, up 38% from the prior year, and reaching a scale equivalent to around 1.3% of global GDP.

- Stripe states: ‘We’re seeing an AI boom on Stripe. We are partnered with a large number of companies with rapidly growing businesses including OpenAI, Anthropic, Suno, Perplexity, Midjourney, Cognition, ElevenLabs, Mistral, Cohere, LangChain, Pinecone, Sierra, Decagon, Invideo and others. Our 2024 data show these startups are building businesses at record pace.’

AI companies building revenues faster than SAAS

- 'Much as SaaS started horizontal and then went vertical (first Salesforce and then Toast), we’re seeing a similar dynamic playing out in AI: we started with ChatGPT, but are now seeing a proliferation of industry specific tools. Some people have called these startups “LLM wrappers”; those people are missing the point. The O ring model in economics shows that in a process with interdependent tasks, the overall output or productivity is limited by the least effective component, not just in terms of cost but in the success of the entire system. In a similar vein, we see these new industry specific AI tools as ensuring that individual industries can properly realize the economic impact of LLMs, and that the contextual, data, and workflow integration will prove enduringly valuable.’

Stripe – with its perspective on business formation – also has some comments on the VC funding scene in Europe.

- 45% of European founders say that the European business climate is getting worse (compared with only 15% of US founders). Even more strikingly, founders in Europe are twice as likely to see North America as an opportunity for growth than Europe itself. Furthermore, 66% of European founders say that European technology-related policy changes over the past four years have been unhelpful. (13% say they’ve helped.)

- First, the evidence suggests that Europe needs a broader, deeper, and more diverse array of financing solutions. In the US, almost 80% of corporate lending is now from non-bank sources, compared to just 32% in the EU. This raises the cost of capital for European firms, which in turn lowers investment rates.

- The European VC landscape is similarly behind: while the US invests around 0.7% of GDP in high-growth firms, that figure is less than 0.3% in Europe. Some of this difference stems from more conservative sources of wealth: large US pension funds, for example, have spotted the attractive returns of the venture sector, thus helping finance its growth, but large pools of European capital have generally shied away.

Public markets – inversion at the start of 2025

So far in 2025: In our last Growth Equity Update we noted the eventful start to the year in public markets. At the time, we were referring to the impact of US tariff announcements and the emergence onto the tech scene of DeepSeek as a potential AI disruptor. It turns out that these were just ripples compared to the waves affecting the markets in the last four weeks.

- The US has imposed, and then almost immediately suspended, tariffs on Canada and Japan.

- The US has suspended arms shipments to Ukraine and has expressed its lack of interest in being a backstop for Ukrainian security guarantees.

- In turn this has led to a major pivot in Europe with the EU Commission presenting a new €800bn plan to increased defence spending.

- The new German chancellor Friedrich Mertz has announced a plan to reform the German debt brake by lifting the cap for annual net borrowing from 0.35% to 1.4% of GDP, creating €220bn of additional spending headroom by 2030. Additionally, a special €500bn fund for infrastructure projects outside regular budgetary spending has been proposed. This caused the biggest rise in German bond yields for the 35 years since reunification.

- In turn, this has stimulated hopes of European economic revival.

- In the middle of this the ECB cut interest rates again by a further 25bps to 2.5%, the sixth cut since June 2024. It indicated though that ‘monetary policy is becoming meaningfully less restrictive,’ a signal that the pace of interest rate cuts may now slow.

- Currencies have whipsawed around with the overall trend being the dollar weakening against major currencies and a strengthening in the Euro and sterling.

The impact of tariffs and the disruptive effect of their on/off nature appears likely to push inflation up in the US (President Trump acknowledged they might ‘cause a little disturbance’) reducing the prospect of further interest rate cuts. The official line from the Fed is that tariffs have not yet had an impact and are not factored into the current thinking with Fed Chairman Jay Powell saying that on policy decisions the Fed will ‘patiently watch and understand and see how it plays out’.

The Atlanta Fed’s GDPNow model has though predicted that US GDP in Q1 will contract by 2.8%, a shift from earlier forecasts of +2.3% giving rise to fears of ‘Trumpcession’. Questioned on the possibility of recession in early March President Trump commented that:

‘I hate to predict things like that. There is a period of transition, because what we’re doing is very big. We’re bringing wealth back to America. That’s a big thing, and there are always periods, it takes a little time.'

Meanwhile geopolitical risks have risen. Few can be comforted by the statement from China’s foreign ministry spokesperson Lin Jian that: If the US has other intentions and insists on a tariff war, trade war or any other war, China will fight to the end.

In the midst of this President Trump’s support for the crypto industry by declaring a strategic reserve for bitcoin, Ethereum, XRP, Solana and Cardano, the sale of two major Panama Canal ports from Hong Kong to American ownership and the US president’s repetition of the US determination to acquire Greenland ‘one way or the other’ and to revisit the 1908 boundary treaty between Canada and the US in the context of describing Canada as the ‘51st state’ have barely had a look in.

We repeat this excellent summary from Rothschild & Co strategists Kevin Gardiner and Anthony Abrahamian highlighting the potential impacts of some of the Trump administration’s initiatives:

Trumponomics - An overview of the headline policies

What is the result of all this activity? In mid-February we observed the turnabout in the performance of indices with the US lagging and Europe leading the way since the start of the year and the relative underperformance of the Magnificent 7, now dubbed by some the Lagnificent 7.

The trends have continued. YTD to the 10th of February the European STOXX 600 was up 6.6% with the UK’s FTSE100 up 5.7%. The S&P 500 was up 2.7% with the NASDAQ lagging at a rise of 1.3%. The Magnificent Seven index was up just 1%.

Now YTD to 10th March the STOXX 600 is up 7% and the FTSE100 up 4%. The US indices have entered negative territory with the S&P 500 down 4%, NASDAQ down 9% and the Lagnificents down 15%.

The FTSE Venture Capital Index which measures the performance of the US venture capital industry, with a strong sector weighting towards technology, was up 10% ytd at 22,477 in early February, just 6% off its highs of August 2021. It is now down 9% ytd.

Rothschild & Co strategist Kevin Gardiner thinks the prospect of further significant market gains are becoming less likely in 2025. He summarises the current key drivers of the market in this graphic:

February - US and European VC raises keep up the pace.

2025 has started strongly for the venture capital/Growth Equity market on both sides of the Atlantic. To the end of February our Deal Monitor recorded 68 deals at $100m or more in the US and Canada raising a total of $18.7bn, up 72% yoy.

In Europe our Deal Monitor recorded $4.9bn of raises in Europe in January and another $2.5bn in February which means that the European market is up 20% in value yoy and is 95% up on the first two months of 2023.

In February US raises were $7.4bn (+6% yoy) and were widely dispersed by sector. The most prominent sector was AI with four companies raising a total of $1.4bn led by the $480m raised for the AI cloud platform business, Lambda. Nuclear reactor and fuel design engineering company X-Energy had the largest single raise at $700m. Four software businesses raised a total of $470m led by the $150m for video monetization platform, Uscreen.

In Europe our Deal Monitor recorded $2.5bn of raises in February, up 33% yoy. The top sectors were Software ($0.54bn), Fintech ($0.4bn) and Artificial Intelligence ($0.27bn). YTD there have been 23 deals of more than $100m in Europe. This compares with 19 in the same period in 2024 and 8 in January/February 2024.

The US – $7.4bn of US venture backed raises of $100m+ in February

Europe - $2.5bn of raises in February 2025

And more to come: A notable feature of the VC/Growth Equity environment in recent months has been the momentum behind early-stage investment in AI businesses. Despite the brief disruption to the narrative caused by DeepSeek, the apparent enthusiasm to support LLM businesses with fresh funds remains substantial.

Already in March AI LLM company Anthropic has raised $3.5bn at a $61.5bn post-money valuation. The round was led by Lightspeed Venture Partners, with participation from Bessemer Venture Partners, Cisco Investments, D1 Capital Partners, FMR, General Catalyst, Jane Street, Menlo Ventures and Salesforce Ventures, among other new and existing investors. This more than doubled the $30bn valuation established in its $4bn raise in November 2024 and was more than treble the $18bn valuation at its $750m raise in January 2024. It had already raised $1bn of further funding from Google this year.

Anthropic says that with this investment, it will advance its development of next-generation AI systems, expand its compute capacity, deepen its research in mechanistic interpretability and alignment, and accelerate its international expansion.

The next Exhibit indicates that there is a potential $53bn of raises in the offing in US growth equity.

Leading these, widespread press reports suggest that SoftBank is close to making a $40bn primary investment in Open AI at a $260bn pre money valuation. The intention is that the money would be paid out over the next 12-24 months. SoftBank is reportedly looking to borrow $16bn from banks to fund the initial investment. Open AI’s previous round raised $6.6bn in October 2024 at a valuation of $157bn.

Rounding out this series of LLM raises, Elon Musk’s xAI is reported to be seeking a further $10bn from investors in a round that would value the company at $75bn. Existing investors Sequoia, Andreessen Horowitz, and Valor Equity Partners are said to be considering participating. xAI’s previous raise of $6bn at a valuation of $50bn was closed on December 24, 2024. Prior to that it raised $6bn in May 2024 at a valuation of $18bn.

Figure AI is an AI led robotics company producing humanoid general purpose robots. Reuters reports that it is looking to raise $1.5bn at a valuation of $39.5bn ($38bn pre money). This valuation would be 15x the $2.6bn achieved in its $675m Series B raise in February 2024.

Thinking Machine Labs is the company founded by the former CTO of Open AI, Mira Murati. She left OpenAI in September 2024 and has been joined in her new company by about twenty other former members of staff at OpenAI. The nature of Thinking Machine Labs intended product is unclear. As yet the company indicates only that it intends to develop ‘more flexible, adaptable, and personalized AI systems.’ The company is reported to be looking to raise $1bn at a $9bn valuation- it is understood not to previously have raised.

Popular YouTuber Jimmy Donaldson - known as Mr Beast to his 368 million followers - is understood to be establishing a holding company to control his various businesses which include consumer brands as well as his video production company. Press reports suggest a raise of $200m at a potential valuation of $5bn.

Forge Nano a Boulder, Colorado based materials science business involved in battery technologies is believed to be raising money in a round valuing the business at $900m. It is currently backed by GMVentures and VW.

Anysphere is an applied research lab working on automating AI coding. It’s the developer of the code editor Cursor. The company is in talks to raise funding at a $10bn valuation with perennial AI investor Thrive Capital said to be leading the round. Anysphere last raised $100m funding in late December 2024 at a $2.5bn valuation.

Flock Safety is a manufacturer and operator of security hardware and software, particularly used for automated licence plate recognition. It is reported to be raising $250m in a round led by Andreesen Horowitz at a valuation of c$7.5bn. It last raised in 2024 at a valuation of $4.8bn.

US Growth Equity – $53bn reported upcoming raises

Our views on the state of the venture capital markets

The combination of global inflation, rising interest rates, and increased geopolitical risk substantially impacted the venture capital market in 2022 and 2023. 2024 saw some adaptation to the ‘new normal’. The refocusing of venture backed companies to achieve a better balance of growth, profitability and cash flow and the delivery of interest rate cuts have led to increased optimism and enthusiasm for growth equity. Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment led to a sharp impact on valuations in private markets. The scale of the fall in the FTSE Venture Capital Index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023 and slow recovery in 2024.

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, semiconductors) supporting the development of AI.

Enthusiasm for AI and related technologies drove the overall level of the FTSE Venture Capital Index in February 2025 back to within 6% of its highs of August 2021. - Outside the AI space the VC market is selectively regaining confidence with a revival of interest in fintech, biotech and software being notable. Certain investors remain highly active in the space with substantial funds to deploy. There remains substantial dry powder in the VC industry.

- The speed of the investment process has slowed since 2021-22. The level of diligence on new deals has stepped up.

- 2023 and 2024 saw more downrounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these.

- It seems likely that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses.

- Valuation priorities have shifted with investors having moved away from an emphasis on revenue growth and revenue multiple emphasis. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and an emphasis on DCF and comparative based multiples.

Read the previous editions:

May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024, January 2025, February 2025.

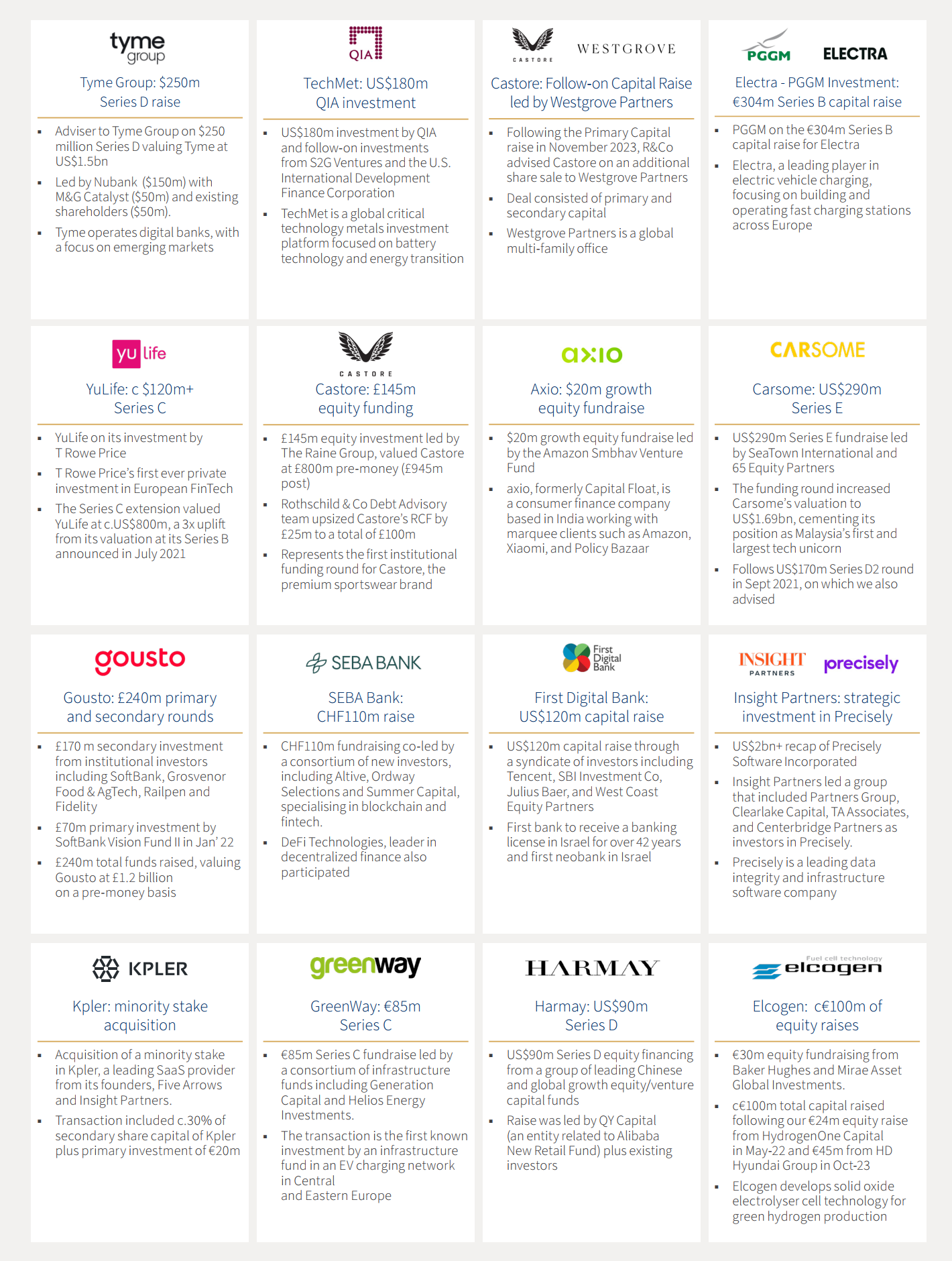

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Chris Hawley

Global Head of Private Capital

chris.hawley@rothschildandco.com

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Advisory

patrick.wellington@rothschildandco.com

+44 20 7280 5088

+44 7542 477 291

Thomas Chung

Head of Private Capital, North America

thomas.chung@rothschildandco.com

+1 212 403 5559

+1 917 594 7208

Mark Connelly

Head of North American Equity Markets Solutions

mark.connelly@rothschildandco.com

+1 212 403 5500

+1 917 297 5131

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.