Why time in the market beats timing the market

What you need to know

- Financial markets are often volatile

- They can be hard to predict over the short term

- Staying invested over longer time periods can help avoid this volatility

- Timing the markets and getting it wrong can significantly impact your wealth

Imagine for a moment that it’s January 2008. You’re sitting down in your favourite armchair with a cup of coffee to read the day's news. You open the Financial Times and see this headline:

The worst market crisis in 60 years

As an investor, you would no doubt be concerned. But perhaps it's just a one-off headline? Simply a case of media sensationalism? Sadly, over the coming weeks and months, a slew of similar stories would make your morning news catch-up a rather gloomy affair.

2008 in headlines

- We are in the worst financial crisis since Depression, says IMF, The Guardian, 10 April 2008

- S&P 500 plunges in worst day this year, Financial Times, 9 September 2008

- Dow plunges a record 777, LA Times, 30 September 2008

- Stock markets around world suffer worst year on record, The Guardian, 31 December 2008

After a year of relentlessly bleak financial headlines, even the hardiest of investors could be forgiven for wanting to sell their stocks and retreat to the safety of cash.

In doing so, however, they would have cemented their losses at likely the worst point and thwarted their chances of benefiting from the eventual recovery in stock prices. Indeed, the market rebound was swift – and uninvested individuals would have been left behind.

On New Year's Eve 2009, just 12 months after the 'worst year on record' for markets, the BBC led with a more upbeat headline:

By 2013, both the Dow Jones and the S&P 500 were closing at record highs.1,2 Meanwhile, European stock markets and the FTSE weren't far behind.

This is not a one-off case. Take the Covid-19 pandemic, for example. In March 2020, many media headlines had a similarly bearish tone as during the financial crisis. The BBC led with 'Global shares plunge in worst day since financial crisis' on 9 March.3

A few days later, the Financial Times said: 'US stocks fall 10% in worst day since 1987 crash'. The following week, they plummeted another 12%, with the FT using an almost identical headline.4

But by July 2020, within just four months, stock markets had recovered to their pre-crash levels. In fact, despite its severity, the Covid crash was one of the shortest in history.5

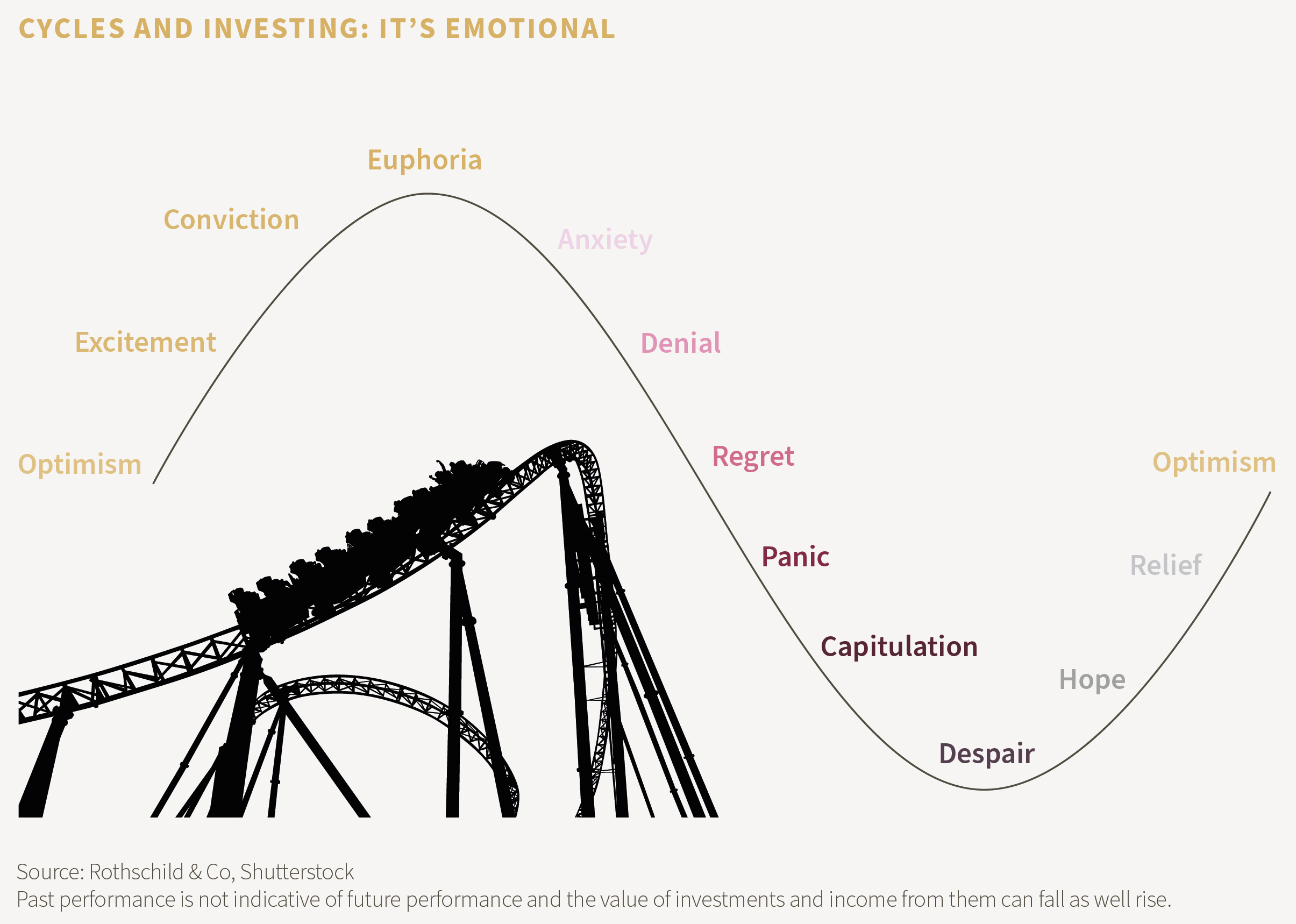

Riding the cycle

What investment lessons can we learn from our thought experiment?

Firstly, a year can feel like a lifetime for investors during a crisis. A steady stream of negative news often makes it difficult to tune out market noise, which can lead to emotions clouding our judgement when investing.

However, it's important to remind ourselves that markets are cyclical. Stocks rarely move in a straight line nor do they move neatly with the economic cycle – sentiment can be fickle and temporary reversals are part of routine volatility.

It can be perilous to make predictions about how markets will behave on any given day, month or year. As Niels Bohr, the Danish physicist once quipped: “prediction is very difficult, especially if it’s about the future!”

A steady stream of negative news often makes it difficult to tune out market noise, which can lead to emotions clouding our judgement when investing."

At Rothschild & Co, we believe that time in the markets is a more reliable way to preserve and grow your wealth than timing the markets.

Put simply, our view is that you have a far better chance of achieving above-inflation returns by keeping money invested in the markets over the long term, rather than speculating on the ideal moment to enter and exit your holdings to maximise gains. Mistiming could have a significant – and irreversible – negative impact on your wealth.

We know cash can be attractive during periods of market turbulence. But there is an opportunity cost to keeping ‘cash under the mattress’. As an asset class, we do not expect cash to outperform stocks over the long-term time horizons that we favour.

We are confident that investing in strong, well-managed companies with sustainable competitive advantages via our ‘bottom-up’ investment approach remains the best way to achieve 'real' returns over the long term for many of our clients.

As an asset class, we do not expect cash to outperform stocks over the long-term time horizons that we favour."

We do not say this because we are keen to sell certain investment 'products' or 'solutions'. While some wealth managers pay bonuses or commission to their client advisers and portfolio managers for promoting particular services, we firmly believe this encourages short-term thinking and creates conflicts of interest.

We understand that everyone's investment priorities are different, which is why we think it's important to make an investment plan that's tailored to your unique needs, risk appetite and time horizons.

Our focus is on making sure you, your family and future generations are financially secure. As a wealth manager, we think that is best achieved by spending as much time in the markets as possible, preserving and growth your wealth against the eroding force of inflation.

Ready to begin your journey with us?

Citations

[1] How the Dow Jones surged back, BBC, 6 March 2013

[2] U.S. Markets Enjoy Another Winning Month; S&P 500 Posts a New Record, Nasdaq, 30 April 2013

[3] Global shares plunge in worst day since financial crisis, BBC, 9 March 2020

[4] US stocks fall 12% in worst day since 1987, Financial Times, 16 March 2020

[5] Covid Crash the Shortest in History, Morningstar, 22 March 2021

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.