Growth Equity Update

December 2024 – Edition 33

- Venture Capital in 2024: We review the biggest deals in venture capital and growth equity fundraising in 2024 on both sides of the Atlantic.

- Strong year in the US: A strong end to the year meant our US Deal Monitor recorded 113 deals of $200m+ raising $82.1bn in 2024, well ahead of 2023’s 74 and $44bn.

- Flat in Europe: Europe started strongly and then faded. Our Deal Monitor shows a 2024 ytd total of $32.3bn, c2% ahead of the $31.8bn of 2023.

- Artificial Intelligence dominated: AI drove the US public markets in 2024 and it drove activity in US private markets. US VC AI deals raised $30.5bn with an accompanying surge in valuations. In November xAI raised $6bn at a $50bn+ valuation, up from $18bn in May and Anthropic raised at a c$30bn valuation, up from $18bn in January. AI related businesses like data centres and semiconductors attracted substantial investment. AI absorbed a third of US VC funding in 2024, perhaps to the detriment of other sectors.

- ClimateTech, AI and Software in Europe remained the top three categories with AI doubling in funds expended in 2024 vs 2023, Climate Tech halving and Software flat.

- Markets still enthused by Trump: In the month post the election (November 5th - December 6th) NASDAQ was up 7.5% and the S&P 500 by 5.4%. Year to date NASDAQ is now up 34%, and the S&P500 is 29%.

- A flurry of rate cuts: December saw a further 25bps cut at the ECB, 50bps in Switzerland and Canada and an expected 25bps in the US.

- Wall Street strategists go bullish for 2025: Having greatly underestimated the prospects of the S&P500 at the start of 2024 Wall Street’s strategists are now more optimistic with predictions looking for an average further 10% advance in 2025.

- ‘We know not through our intellect but through our experience’. Maurice Merleau-Ponty

Click here to download a PDF version of Growth Equity Update

Peering into 2025

Further interest rate cuts and a positive response to the US election result have encouraged Wall Street strategists to be more positive about the 2025 outlook for markets.

The first month post the US election was a strong one for markets coming off the back of the removal of political uncertainty, a Fed rate cut and a flurry of interest in sectors deemed a beneficiary of a Trump victory on the back of less regulation and lower taxes.

In the month post the election (November 5th - December 6th) NASDAQ was up 7.5% and the S&P 500 by 5.4%. Year to date NASDAQ is now up 34%, and the S&P500 29%.

European markets continue to lag with low economic growth, concerns around trade tariffs and with political uncertainty in France and Germany. Nevertheless both the European STOXX 600 and the FTSE 100 were up 2.2% in the month following the US election, bringing the ytd performance to +9% and +8% respectively.

Year to date to the start of December the global equity market return is 20%.

Another Fed interest rate cut to come in 2024: At its meeting on November 6-7 the Fed cut US interest rates by 25bps to 4.5%-4.75%. Fed Governor Andrea Kugler commented at the start of December that “Given how the economy has developed this year, most notably the continuation of disinflation and a modest cooling in the labour market, I see the Fed's dual-mandate goals of maximum employment and price stability as being roughly in balance.”

Subsequent to that the December 6 jobs data showed that the US economy added 227,000 jobs in November plus there was an upwards revision of the October number from 12,000 to 36,000. This reassured the markets, with the CME Group's FedWatch indicator implying a 90% chance of a 25bps rate cut at the December Fed meeting, up from 68% prior to the release.

This was then reinforced by the November inflation numbers. US inflation was 2.7% in November, marginally higher than the 2.6% of October but in line with market forecasts. The market found this reassuring with the FedWatch indicator rising to a 98% chance of a rate cut in the December meeting.

It appears then that a further Fed cut, taking rates down to 4.25%-4.5%, is a near certainty at its meeting on December 17-18.

Thereafter the prospect of further rate cuts at the start of next year is much more slender. The Fed’s official dot plot looks for a cut of 25bps in December and a further fall of 100bps in rates to 3.25%-3.5% by the end of 2025. The market’s prospect of a cut at the January meeting (the date is the 31st) is put though at only 27%. The market is expecting a much more gentle process of rate cutting in 2025, inflation has remained above the 2% target and there are some inflationary risks like tariff imposition. Fed Chair Jay Powell has indicated the Fed may be ‘a little more cautious’ about rate cuts in 2025.

Thus far the Fed seems to have done a good job in controlling inflation while encouraging growth and guiding the US towards a soft landing. A potential threat to the inflation/growth mix is the possibility of higher tariffs under the incoming Trump administration, although many commentators appear anxious to downplay both the extent of the potential tariffs and the impact on inflation. A reassuring note is that it appears that while the Trump administration will bring change in terms of tariffs, tax cuts and possible deportations there will be continuity at the head of the Fed. President elect Trump has indicated that he will not remove the Fed Chair Jay Powell before his term ends in May 2026.

Meanwhile rate cuts to respond to signs of slowing economic growth are being seen in Europe and Canada. The ECB started cutting rates in June, reducing the core rate from 4% to 3.75%. Further 25bps rate cuts followed in September and October taking the rate down to 3.25%. The ECB pressed on, bringing up a hat-trick of cuts with a further 25bps reduction to 3% at its meeting on December 12. The ECB is concerned about a slowing economy with its forecast for 2025 GDP growth lowered to 1.1% (was 1.3%) with just 1.4% and 1.3% expected for 2026/7. Meanwhile inflation is forecast at 2.1% in 2025, 1.9% in 2026 and 2.1% in 2027 running in line with the ECB’s 2% target.

As a result the head of the ECB, Christine Lagarde was clear that a path of further rate cuts is likely observing that ‘The element which has changed is the downside risks, particularly the downside risks to growth.’

Market forecasts look for five further 25bps rate cuts in 2025 to take the rate down to 1.75%. There is even speculation that the ECB may indulge in a jumbo rate cut of 50bps at some stage.

Switzerland and Canada are two countries that led the way on rate cuts and they continue to indulge. On December 12 the Swiss National Bank lowered its interest rate by an unexpectedly large 50bps, reducing the rate from 1% to 0.5%, the lowest since late 2022. The official SNB forecast looks for the rate to hold steady at 0.5% through 2026. Swiss GDP growth is sluggish with 0.4% in Q2 followed by just 0.2% in Q3.

To much less surprise Canada also reduced rates by 50bps at its mid-December meeting. This was the fifth successive cut and took rates from 3.75% to 3.25% meaning that Canada has cut by 175bps in the course of 2024. GDP growth in Q3 was just 1% versus forecasts of 1.5% and unemployment hit 6.8%.Canada also faces the prospect of a potential 25% tariff on all imports to the US under the Trump administration.

Strategists forecasts – how did they do?

The next table looks at the expectations of the major investment banks set at the start of 2024 for the level of the S&P500 index by the end of 2024.

The S&P 500 index started the year at 4,770. The median expectation of 20 major investment banks for the 2024 closing level of the S&P 500 was 4,875, upside of just 2%.

The highest forecast, Yardeni Research’s 5,400, represented upside of 13%. Eight of the 20 strategists forecast the S&P 500 at the same level or lower by the end of 2024. As was the case in 2023, the targets at the start of 2024 were typically set too low and were upgraded sharply through the year.

We are not at the year-end yet – so things could still change. Nevertheless to the 6th December the S&P 500 was up 28%, confounding the generally cautious strategists’ expectations. The market has been surprised by the continued strength of the major technology stocks as the AI inspired stock boom continues – the Magnificent Seven is up 65% ytd. The Fed has successfully charted a seemingly impossible course between controlling inflation while encouraging growth and guiding the US towards a soft landing. The US election result has refuelled market optimism on the basis that President Trump’s administration will imply less regulation and lower taxes, and despite the risk of higher tariffs, sent certain sectors of the stock market notably higher, including banks, energy stocks, smaller companies and some tech stocks. Crypto related stocks have been big beneficiaries of the expectation of lower regulation.

Finally the market has been resistant to the many geopolitical threats to its equanimity in 2024 – the year of many elections and which has seen the broadening in conflicts involving Israel to include Lebanon and Iran, the collapse of the Syrian regime, the resurgence of Russia in its war with Ukraine, the temporary declaration of martial law in South Korea as well as the election of a Labour Government in the UK, the collapse of the French government and substantial political uncertainty in Germany.

In the end the strategists’ early expectations were cofounded – an average 2% upside predicted for the S&P 500 at the start of 2024 turned into a+28% outturn.

Wall Street strategists’ S&P 500 forecasts at start 2024

So what are the early prognostications for the markets in 2025?

The next Exhibit shows the Wall Street forecasts for the 2025 year end level of the S&P500 from the strategists of 14 leading firms.

There’s nothing like a year of strong performance of an index to make people more bullish. Having greatly underestimated the prospects of the S&P500 at the start of 2024 the strategists have compensated with more optimistic forecasts, with the predictions looking on average for a further 10% advance in the market in 2025.

Yardeni Research was the most optimistic forecaster at the start of 2024 with its prediction of a 13% advance. They again lead the pack with a forecast of a 15% advance in the S&P 500 going into 2025. Yardeni highlights the ‘animal spirits’ that have infused the market since the Trump re-election. (We recall that the Rothschild & Co Growth Equity Update started citing the effect of animal spirits as early as March this year.) The firm also says “Trump 2.0 represents a major regime change that’s bullish for the economy and stocks."

Other optimists include Wells Fargo, symbolically top of the expectations list with a 7,007 S&P 500 target. It cites a favourable US macro environment and continuing falls in Fed rates as driving potential performance.

Capital Economics allies a relatively optimistic forecast of 7,000 with cautious notes about the impact of Trump’s election on US and global growth. It concludes though that it will not be a sufficient negative to stop the US economy from growing, or what it describes as the ‘artificial intelligence bubble’ from continuing to inflate – hardly reassuring. Deutsche Bank’s 7,000 target is prognosticated on beneficial later cycle effects that are yet to kick in – factors such as re-stocking, the expansion of non tech capex, and a return of M&A.

Bank of America’s oddly pitched 6,666 S&P 500 target is based on a breathless concatenation of bullish factors . "Get ready for a cyclical inferno. Nine reasons: (1) Red sweep, (2) Fed cuts, (3) accelerating profits, (4) re-shoring, (5) productivity cycle, (6) shift from everyone spending on Tech to Tech spending on everything, (7) municipalities refurbishing to court corporates, (8) tight capacity / decades of underspend in manufacturing, and (9) lightest positioning in cyclical sectors since at least the GFC."

Expressed in more bloodless style RBC observes in commentary on its 6,600 forecast "The story the data tells us is that another year of solid economic and earnings growth, some political tailwinds, and some additional relief on inflation (which should keep the S&P 500’s P/E elevated) can keep stocks moving higher in the year ahead."

The most pessimistic forecasts that we have seen thus far come from Morgan Stanley and Goldman Sachs, both of whom put the 2025 year-end level of the S&P 500 at 6,500, still up 7% on current levels. Morgan Stanley appears to anticipate market leadership changes – presumably a reference to the strength of tech stocks coming to an end, as well as to uncertainty post the US presidential election. The firm has a range of potential outcomes - from 4,600 at the low end to 7,400 at the high end. In market parlance it’s a range that you could drive a coach and horses through and is clearly designed to cover all eventualities. At the low end it anticipates a near 25% fall in the market.

Morgan Stanley looks for 13% eps growth in 2025. The Goldman Sachs 6,500 forecast is ‘predicated on continued U.S. economic expansion’ but looks for just 11% earnings growth with the impact of higher tariffs offset by lower corporation tax rates.

Wall Street’s forecast for the S&P 2025 year end level – up 10%

Rothschild & Co strategist Kevin Gardiner thinks the prospect of further significant market gains are becoming less likely as we enter 2025 observing:

"The response to Trump is not a huge surprise: tariffs are an obvious threat…… but may be offset (again) by lower taxes and deregulation (hence the banks’ rally). Meanwhile, the macro backdrop remains broadly constructive for business and stock… but inflation risk may be rekindling. US valuations now look pretty full… and AI hype is starting to look frothy. In macro-led portfolios we have taken profits on stocks, and are now neutral."

He summarises the current key drivers of the market in this graphic:

The Biggest Venture Capital deals of 2024

The end of the year is traditionally a period of review and we succumb to the temptation to look back at the trends and largest deals in venture capital on both sides of the Atlantic in 2024.

The key trends of the year were:

It was a big year for venture capital raises in the US. In 2024 our Deal Monitor recorded 113 deals of $200m or above raising $82.1bn, well above 2023’s total of 74 and $44bn.The average value of the 2023 deals was $589m, in 2024 it was $726m. The number of larger deals in Europe, by contrast, fell. 2024 saw 23 European deals of $200m+ with a value of $9.1bn. In 2023 there were 26 such deals with a value of $11.5bn.

The US closed the year on a strong note; The US VC market hit a crescendo in October and November with two $16bn months fuelled by substantial raises for Artificial Intelligence LLM providers (Open AI, xAI, Anthropic).

Seasonally the VC market started strong in Europe and faded yoy in the second half. Our Deal Monitor, which captures all deals of $20m+ in Europe, is showing an early December ytd total of $32.3bn, c 2% ahead of the $31.8bn of 2023. H1 was up 36% yoy. H2 faded.

The rise and rise of artificial intelligence. Just as AI drove the US public markets so it drove activity in US venture capital markets in 2024.The year was studded by substantial AI deals for the large language models businesses with ever higher valuations. Open AI’s valuation went from $29bn in January 2023 to $157bn in October 2024; Anthropic from $18bn in January 2024 to $30bn in September and xAI from $24bn in May to $50bn in November. In total AI absorbed around a third of total US VC funding in 2024.

But mainly in the US: Narrowly defined US AI deals raised $30.5bn in 2024.In Europe the equivalent figure, even if we include Europe’s largest deal, the $1.05bn raised for autonomous vehicle company Wayve, was at just $3.4bn.

And AI related. Away from the large language model players there was a surge of funding for AI associated businesses, particularly data centres, semiconductors and leading AI applications like autonomous vehicles. Data centres need to scale to accommodate the demands of AI and the sector saw the biggest deal of the year, a $9.2bn equity investment for Vantage Data Centers. There were substantial raises for AI oriented semiconductor businesses like Tenstorrent, Rivos and Groq. AI applications started to infuse businesses throughout the VC spectrum.

Starving the rest? Rapid gains and intense interest in the VC community for the mould breaking potential of AI meant that by the end of the year companies seeking VC backing in the US were remarking that doors appeared to be largely closed for all but AI focussed businesses. Given that in total AI absorbed over a third of total US VC funding in 2024 these observations may be justified.

Climate Tech treads water: Proportionally Climate Tech is a bigger sector in Europe than in the US VC ecosystem. It topped the sector charts for European investment in 2024 as it did in 2023 although the $3.3bn invested in European Climate Tech in 2024 was less than half the $6.8bn of 2023. The largest European Climate Tech deal in 2024 was $550m for German electrolyser manufacturer, Sunfire whereas in 2023 ClimateTech deals were led by a $1.65bn raise for H2 Green Steel and $1.3bn for Northvolt. The appetite for substantial deals in capital hungry, long duration, new technology businesses may have been stunted by the difficulties faced by Northvolt which led it to file for Chapter 11 bankruptcy protection in November 2024.

Fintech activity remains subdued. Silicon Valley Bank in late October observed in late October that fundraising by fintech oriented VC firms has dropped by over 90% since its peak in 2021. In the US we counted just $0.7bn of $200m+ raises in 2024. Europe fared better with eight deals raising $1.56bn in 2024 up from seven raising $1.1bn in 2023. All a far cry from 2021.

Slushtastic: Hope springs eternal in the human breast. On a positive note the largest European VC conference for founders and investors took place in a snowy, dark Helsinki in late November. We joined 5,500 start up founders and operators and 3,300 investors and marvelled at the energy and innate optimism of the venture capital ecosystem.

The Biggest Venture Capital deals of 2024 -the US

The biggest 15 deals in US venture capital are shown in the table. In total the 15 $1bn plus deals raised a total of $48bn. Illustrating the dominance of AI the industry saw 7 raises in this group with proceeds of $25.7bn, over half the total. In addition, the largest deal was AI related, the $9.2bn raised for Vantage Data Systems. Autonomous vehicles, Climate Tech, Defense , Gaming, Software, biotech and Cybersecurity had one deal each in the top 15.

Top 15 US VC deals in 2024 raise $48.3bn

Looking at the trends by sector:

Artificial Intelligence leads the way again: As in 2023 the biggest category of US VC fundraising in 2024 was for artificial intelligence businesses. In total the twenty US deals of $200m+ in AI in 2024 raised almost $31bn, twice the level of the AI deals in 2023.

The biggest raises were for the large language model players led by the $6.6bn raise for Open AI orchestrated by Thrive Capital in October at a valuation of $157bn. It was closely followed by two $6bn fundraisings for xAI- one in May at a valuation of $24bn and a second in November at a $50bn valuation. Anthropic had a $4bn raise in November 2024 at a valuation of c$30bn which followed its $750m raise in January at a valuation of c$18bn.

Scale AI, a data foundry for AI applications providing high quality training data for AI applications like self-driving cars and AR/VR raised $1bn in a deal led by Accel in May. Safe Superintelligence, the AI research lab founded by the OpenAI co-founder Ilya Sutskever, raised $1bn in a deal valuing the business at $5bn in September.

Smaller , but still substantial deals include $900m at a valuation of $3bn for the AI legal applications business Clio and $650m at a $4bn valuation for the AI driven market intelligence platform AlphaSense.

The speed of valuation change for AI associated companies is demonstrated by Glean which has an AI powered work assistant (chatbot) for use in enterprises. Chatbots are a common first application for AI techniques. Glean claims that its Glean Chat saves an average 2-3 hours per employee per week. Its $200m Series D in February was led by Kleiner Perkins and Lightspeed and valued the company at $2.2bn. Its $260m Series E seven months later in September included new investors like Altimeter and DST Global and more than doubled the valuation of the company to $4.6bn.

The top US AI deals in 2024 –20 deals of $200m+ raising $30.5bn

Data Centres – fuelled by the AI boom: There was a surge of funding for AI associated businesses, notably for data centres. Indeed, the biggest deal of the year in the US was the $9.2bn equity investment led by DigitalBridge Group and Silver Lake in Vantage Data Centers. Vantage works with hyperscalers, cloud providers and large enterprises whose demand in turn is being led by AI compute requirements.

Coreweave is a cloud computing business that specialises in providing infrastructure to AO developers. It raised $1.1bn in a Series C led by Coatue in May, conducted a $7.5bn debt deal in the same month, established a further $650m credit facility in October and completed a $650m secondary in November, valuing the business at $23bn, up from $7bn a year earlier.

The energy demands of AI are also being addressed by Crusoe Energy. Its mission states ‘AI requires a tremendous amount of energy. Taking an "energy first" approach to building and operating clean computing infrastructure, Crusoe reduces both the costs and the environmental impact of the world's expanding AI needs.’ The company aims to deliver ‘gigawatts of new data centre capacity.’ Crusoe raised $500m in a Series D in October led by Founders Fund that valued the business at $3bn.

Lightmatter’s high powered photonics interconnect layer (30 terabits) enables 1024 GPUs to operate simultaneously speeding up the performance of AI datacentres. Its $400m Series D in October was led by T Rowe Price and Google Ventures and valued the company at $4.4bn. Lambda sells AI infrastructure and has an ambition to be the number one global AI compute platform. Its $320m Series C in February was led by the US Innovative Technology Fund.

The top US deals in Data Centres/Cloud in 2024 –five deals of $200m+ raising $11.5bn

Autonomous vehicles – a narrowing field. The funding of autonomous vehicle solutions is a tough gig for private capital. These businesses require substantial investment pre revenue, the revenue build up is relatively slow, the industry is subject to high levels of regulation, and accidents involving the vehicles are liable substantially to stunt the progress of projects.

There were two big raises in this industry in 2024. Cruise has raised $15bn since its inception in 2016. Its $2.75bn round in 2021 was the largest in the US that year. The business has been majority owned by General Motors since 2016 and in 2022 General Motors bought out SoftBank for $2.1bn. Later that year an accident with a pedestrian led to the suspension of Cruise’s self-driving taxis. In the aftermath of that GM said it would cut its spending on Cruise. Despite having absorbed operating losses at Cruise of $5.8bn 2021-3 GM led an $850m June 2024 round designed to get the Cruise programme up and running again in Phoenix, Houston and Dallas with the aim of restoring public confidence in the technology.

The strategy rapidly changed. After announcing another $1.3bn loss at Cruise for the first nine months of 2024 GM stated in early December that “considerable time and resources…would be needed to scale the business" and announced that it would no longer fund the Cruise robo-taxi service and would focus its development instead on AV for personally owned vehicles.

Waymo by contrast raised $5.6bn in an October 2024 Series C led by Alphabet and including Andreessen Horowitz, Silver Lake, Fidelity, Tiger Global, Perry Creek, and T. Rowe Price. Its previous raise was $3.2bn in 2020. By contrast with Cruise, its robotaxi service is fully operational and expanding with services running in San Francisco, Los Angeles, Phoenix, Austin and Atlanta.

The top US deals in Autonomous vehicles in 2024 –two deals of $200m+ raising $6.5bn

Semiconductors – AI focus: There were three sizeable semiconductor deals in 2024, each focused on the particular compute requirements of AI. In December Tenstorrent raised $693m in a Series D valuing the company at $2.6bn in a round led by Samsung Securities and AFW Partners and backed by Jeff Bezos. Tenstorrent is designing AI chips for specific applications in an attempt to challenge Nvidia with a focus on open source and interoperability with other technology providers.

In August Groq, with its AI accelerator ASIC called the language processing unit, raised $640m at a $2.8bn valuation. The deal was led by BlackRock Private Equity Partners and strategics Cisco and the Samsung Catalyst Fund. The inference capabilities of Groq improve the speed at which LLMs can respond to questions. The $250m Series A-3 round for Rivos in April was led by Matrix Capital Management. The company designs RISC-V-compatible chips for generative AI and data analytics workloads, typically targeting smaller installations not requiring the incremental expense of Nvidia GPUs.

The top US deals in Semiconductors in 2024 –three deals of $200m+ raising $1.6bn

A quantum of Quantum: It seems appropriate to wind up this AI and tech related segment with a bit of deeptech. There were two significant quantum computing raises in the year, totalling $920m. Quantinuum raised $300m at a $5bn valuation in January in a deal led by JP Morgan, Mitsui & Co and major shareholder, Honeywell. The business is the product of the 2021 merger of Honeywell’s Quantum Solutions division and the UK’s Cambridge Quantum Computing. The company aims to build the world’s first universal fault-tolerant quantum computers.

PsiQuantum Corporation is based in Palo Alto California but has plans to build a utility scale quantum computer in Brisbane, Australia. This explains the decision of the Australian Commonwealth and Queensland Governments to provide a package of $620m of funding for the business in April 2024. The CEO of PsiQuantum, Professor Jeremy O’Brien observed that “A utility-scale quantum computer represents an opportunity to construct a new, practical foundation of computational infrastructure and in so doing ignite the next industrial revolution.”

PsiQuantum announced a more conventional Series D in July led by Blackrock and supported by Microsoft’s VC firm, M12, and others including Ballie Gifford, Blackbird Ventures and Temasek. With this raise PsiQuantum stated it had the entire range of capital it will need to move from concept to reality with the Q1 quantum computer, which had just entered manufacturing at GlobalFoundries. This time Professor O’Brien made the case for quantum computing rather than AI being the transformational industry of its age.

"Our plan is to become a truly great company, not to be acquired. We uniquely have a path to the most profoundly world-changing technology that humans have uncovered to date. We are categorically not building an incrementally better chip delivered none months later, this is the foundation of a future economy and a transformation in how humans go about doing things. It’s not unprecedented but it is akin to major revolutions in the past.”

The top US deals in Quantum Computing in 2024 –three deals of $200m+ raising $1.4bn

Biotech -resurgence continues: One of the features of 2024 has been the resurgence of biotech deals. In 2023 there were 13 deals of $200m or more in US biotech raising $3.2bn. In 2024 there were 17 such deals raising $5.7bn. Again AI had an influence with many of these companies using AI techniques to accelerate the process of drug discovery.

The biggest deal in the group was the $1bn raised for Xaira Therapeutics in April in a deal led by ARCH Venture and Foresight Capital and it is a strong example of the influence of AI on the biotech world. The company emerged from stealth to develop new foundational models to design molecular structures and identify new therapeutic targets and which, when fed with the appropriate data in biology and medicine, can accelerate the process of drug design. Xaira hopes to do more than just drug discovery aiming to transform the whole drug development pipeline process, from new biology and designing molecules to running clinical trials. Other companies raising for AI platforms for drug development included the $120m for Terray Therapeutics in October and the $142m for Evolutionary Scale’s LLM for creating novel proteins in June.

A feature of the biotech start-ups was the surge of money going to businesses addressing the treatment of obesity and related conditions.

ARCH Venture Partners was again present leading the $290m funding of Metsera in April. GLP-1 agonists are a class of medication that helps manage blood sugar levels in type 2 diabetes and can also be used to treat obesity - the best known is Novo Nordisk’s Ozempic. Metsera has an injectable GLP-1 receptor agonist, Met-097, an oral product MET-002 and MET-233i, an injectable product used for monthly treatments. The enthusiasm was such that a second round – this time a $215m Series B – was led by Wellington Management and Venrock Healthcare Capital Partners in November. Kailera Therapeutics which has oral therapies for the treatment of obesity raised $400m in a Series A led by Atlas Venture and Bain Capital Life Sciences in October.

The top US deals in Biotech in 2024 –17 deals of $200m+ raising $5.7bn

Climate Tech deals fade: By contrast Climate Tech deals in the US continue to slip down the pecking order, perhaps responding to the pushback seen in some areas against the ‘green agenda’. For instance, eleven US states, including Texas, are suing major investment firms like BlackRock, State Street and Vanguard accusing them of acting against traditional energy sources. The state attorney general of Texas accused the investment companies in late November of ‘illegal weaponisation of the financial industry in service of a destructive, politicised environmental agenda.’ At the same time, venture investors have become wary (except in AI) of companies requiring heavy front end loaded investment pre substantial revenues as is required in many Climate Tech companies.

There were nine US Climate Tech deals of $200m+ in 2024 raising $4.2bn in total, down from eleven such deals raising $5bn in 2023. The largest deal of the year was the $1.5bn raised by Generate Capital which works with developers to finance and operate sustainable infrastructure projects. The deal in January was led by the California State Teachers’ Retirement System.

The second largest deal in the group looks really like a disguised AI related deal, Amazon funding X-energy with $500m for the development of small modular nuclear reactors for clean energy generation. The company is a developer of small modular nuclear reactors and AWS will use X-Energy’s reactors to power its datacentres with 5 GMW/pa of power planned to come on stream by 2039.

Other ClimateTech deals were the $405m raised in a Series F by Form Energy led by T Rowe Price and GE Vernova. Form uses an iron-air battery system for long term energy storage. BrightNight raised $440m in a strategic investment from Goldman Sachs Alternatives. BrightNight has a 31-gigawatt renewable power project portfolio, including solar, energy storage, and hybrid solutions.

The top US deals in ClimateTech in 2024 –nine deals of $200m+ raising $4.2bn

Software – overshadowed by AI? Large software deals remain relatively few in number although valuations appear to be rallying. The sector may well be overshadowed by AI with investors preferring to focus their efforts there rather than delve into more traditional software models. Software is also relatively capital light – a focus on large deals fails to highlight that attractive characteristic of these businesses. Nine software deals of $200m + raised $3.4bn in 2024.

The largest deal of the year was the November raise for Tricentis, a business that performs testing and quality engineering for software releases by enterprises. It raised $1.3bn at a valuation of $4.5bn in a deal led by GTCR. In April Buyers Edge Platform raised $425m in equity as part of a total $1.1bn refinancing package. The company is looking to transform the food service industry through technology, with its procurement software, purchasing and data analytics.

The top US deals in Software in 2024 –nine deals of $200m+ raising $3.4bn

Cybersecurity – A flurry of activity: The Cybersecurity market appeared by contrast to come back strongly in 2024. There was a regular flow of deals through the year. The largest was in May with the four year old US-Israeli business Wiz raising $1bn at a $12bn valuation in a deal led by Andreessen Horowitz, Lightspeed Venture Partners, and Thrive Capital. The cloud security company indicated that it hit $100m of annual recurring revenue (ARR) after 18 months in existence and reached c$350m in ARR by the end of 2023. Shortly afterwards Wiz received and rejected a $23bn offer from Alphabet at almost twice the May valuation. The offer appeared to be a strategic move by Google to burnish its cloud security credentials. The offer was turned down by Wiz on the grounds of potential antitrust issues and given Wiz’s stated ambition to reach $1bn in ARR and to pursue an IPO.

Kiteworks, which has tools to secure email, file sharing and other areas where sensitive data is in use raised $456m from Insight and Sixth Street Growth in August 2024. Like Wiz, its stated intention is to use part of the proceeds in a series of acquisitions.

AI connections are never far away in tech related businesses. The enjoyably named Abnormal Security which raised a $250m Series D in August at a $5.1bn valuation, uses machine learning and AI to understand and assess human behaviour while looking to block attacks on email and other communication systems using its human behaviour AI platform.

In July, the month when CrowdStrike received unwanted publicity on a failed security update, three cybersecurity businesses (Vanta $150m at a valuation of $2.45bn), Chainguard ($120m at a valuation of $1.12bn) and Kandji ($100m at a valuation of $850m) raised $370m between them.

The top US deals in Cybersecurity in 2024 –nine deals of $200m+ raising $3.3bn

Healthcare raises subdued: A similar outturn in Healthcare to 2023 with four $200m+ deals raising $1.32bn in 2024 versus five deals for $1.35bn in 2023. The biggest 2024 deal was, however, a refinancing plan for Radiology Partners in February which involved a $720m equity raise. It was accompanied by a series of debt refinancing transactions. Radiology Partners is a physician-owned and -led business which employs 3,600 physicians who service 3,300 hospitals and outpatient facilities across all 50 US states

The top US deals in Healthcare in 2024 –four deals of $200m+ raising $1.3bn

Fintech funding still depressed: A report from Silicon Valley Bank in late October observed that fundraising by fintech oriented VC firms has dropped by over 90% since its peak in 2021 with investment into VC backed fintech companies remaining muted.

We counted four deals of over $200m in 2023 raising $7.3bn, led by the $6.5bn Stripe raise in March 2023. The absence of a similar big round in 2024 meant that the total has slumped to three deals raising just $0.7bn. The largest deal was for mortgage release company Splitero which raised $300m in a deal led by Antarctica Capital in October.

A focus on primary deals though may give a misleading picture of the underlying appetite for FinTech assets. There was healthy activity n the secondary market. In March 2024, Stripe facilitated the sale of shares by employees by establishing a tender offer with the participation of Goldman Sachs Growth Equity and Sequoia together with some funds from Stripe’s own resources. The tender offer for c$1bn of stock valued the company at $65bn, 30% higher than the March 2023 level.

In August Revolut announced a secondary share sale to provide employee liquidity. The deal which was led by new investors Coatue and D1 Capital Partners and existing investor Tiger Global was done at a $45bn valuation, up from the $33bn recorded at the July 2021 raise. Press reports suggest that the total size of the deal was $500m with the CEO of Revolut, Nik Storonsky, accounting for c40%-60%.

The top US deals in Fintech in 2024 –three deals of $200m+ raising $0.7bn

The US 2024– 64 VC deals of $300m+ raising $71bn in total

The Biggest Venture Capital deals of 2024 - Europe

In 2024 our Deal Monitor has recorded (to early December) 86 European deals of $100m+ raising $17bn. It’s a similar outturn to 2023 when 69 deals of $100m+ raised $16.1bn.

Our broader Deal Monitor capturing all deals of $20m+ is showing an early December ytd total of $32.3bn, c2% ahead of the $31.8bn of 2023 . The VC market in Europe in 2024 looks therefore to be just very modestly ahead of the levels of 2023.

These are Europe’s biggest deals of $200m and above in 2024. There are 23, and they raised $9.2bn.

Europe 2024– Top 23 VC deals of $200m+ raising $9.2bn in total

In addition there were another 63 deals of $100m-$199m raising $7.9bn. These are outlined in a table at the end of this section.

Seasonally the VC market started strongly in Europe and faded yoy in the second half. This was the opposite of the US which, buoyed by a string of significant AI raises, accelerated towards the end of the year closing with a couple of $16bn months ( Open AI, xAI, Anthropic) in October and November.

Looking at the biggest deals in Europe in 2024 we see that AI’s influence is on a much more modest scale than in the US. If we include the $1.05bn raise ( Europe’s biggest of the year) for autonomous vehicle business Wayve, six of the top 23 $200m+ raises were for AI businesses with a value jointly just short of $3bn.

ClimateTech is more prominent than in the US with five of the 23 leading raises at a value of $1.9bn. Otherwise there is no clear trend in the leading deals. There are a couple of software deals – jointly raising $0.9bn, a couple of online grocery deals (Picnic expanding and Getir consolidating back to Turkey) raising $0.6bn and a couple of fintech deals raising $0.7bn led by the $430m raise for Monzo.

Europe 2024– Top 23 VC deals of $200m+ raising $9.2bn in total

Looking at all European deals of $100m and above by sector:

Climate Tech leads less convincingly: In all deals in Europe of $100m plus Climate Tech leads by value, as it did in 2023. The lead though is much less convincing. In 2023 there were 15 Climate Tech deals of $100m+ which cumulatively raised $6.8bn. In 2024 there were 17 such deals but they raised less than half the 2023 total at $3.3bn.

The biggest equity deal was the $550m Series E for German electrolyser manufacturer, Sunfire. Its solid oxide electrolysis technology is deployed in large scale green hydrogen projects. The company finished the year with a flush of orders including 50MW of pressurised alkaline electrolysers for use in a Finnish e-methane project and a 100 MW pressurized alkaline electrolyser for RWE in Germany.

The second largest equity deal was that in which French asset management business Mirova invested $528m to become a significant minority investor in the independent power producer RP Global which is commissioning 2.5GW of solar, wind and storage assets by 2029.

The biggest deal in terms of overall funding was the $5.2bn funding for H2 Green Steel in January. This consisted of a $330m equity raise led by the Microsoft Climate Innovation Fund, Munea and Siemens Financial Services. There was a $275m grant from the EU Innovation Fund. The bulk of the package though was a $4.6bn debt financing from a group of 20 banks including BNP Paribas, SocGen and ING. This brought the total raised so far by H2 Green Steel to €2.4bn in equity and €4.7bn in debt. In 2023 it had the largest equity round in Europe, a €1.65bn raise led by ltor, GIC, Hy24 and Just Climate. The proceeds are earmarked for the construction of the company’s flagship large-scale green steel plant in Boden Sweden which will include Europe’s first giga-scale electrolyser. H2 Green Steel, now rebranded as Stegra, expects to begin steel production in mid-2026 with an initial aim to supply 2.5m tonnes pa, rising to 5m tonnes by 2030.

The top European deals in ClimateTech in 2024 –17 deals of $100m+ raising $3.5bn

Artificial Intelligence - substantial yoy growth: In 2023 AI was the third largest sector for European VC raises with seven deals raising $1.8bn. In 2024 AI rose to be narrowly in second place with ten deals raising $3.4bn, almost twice the 2023 total.

The total is boosted by the $1.05bn Series C from the AI- led UK autonomous vehicle software company Wayve. The deal was led by SoftBank and including Nvidia and Microsoft. Wayve was founded in London in 2017 and aims to launch the first embodied AI technology for self-driving vehicles. Embodied AI allows automated vehicles to learn from and interact with a real-world environment, including the ability to anticipate unexpected and irregular behaviours by other road users.

Three of the raises were for companies producing LLM models. France’s AI champion is Mistral AI, set up in May 2023 by a team who had formerly worked at Google and Meta with a plan to launch its first LLM in 2024. It is led by Arthur Mensch who has a PhD in machine learning and functional magnetic resonance imaging and who did two years of postdoctoral studies in mathematics before joining Google DeepMind for two-and-a-half years. The company raised €105m ($113m) in Europe’s largest ever seed round in June 2023 which valued the four-week-old business at $240m. In December 2023 Mistral closed a $415m Series A round valuing the company at $2bn, led by a16z. In June 2024 Mistral completed a $640m Series B led by General Atlantic at a valuation of $6bn.

Mistral has focused on open source LLMs with its open weight models Mixtral 8x7B and Mixtral 8x22B. Mistral’s most advanced LLM, Mistral Large, is a direct competitor to GPT-4. At present its reputation is of being less functional than GPT-4 but also cheaper.

French AI start-up H (previously Holistic AI), announced a $220m seed round in May just a few months after the company’s inception. Charles Kantor, the co-founder and CEO, was a university researcher at Stanford and the four other co-founders previously worked for Google’s DeepMind. H intends to develop AI agents, ‘automated systems that perform tasks traditionally undertaken by people.’ Investors include a medley of billionaires, Eric Schmidt, Xavier Niel, Yuri Milner, Bernard Arnault and Motier Ventures (Galeries Lafayette). VC investors include Accel, Bpifrance, Creandum, Elaia Partners, Eurazeo, FirstMark Capital and Visionaries Club. Industrial investors include Amazon and Samsung.

DeepL, a German/Polish business building an AI powered language platform for translation and writing (it translates texts & full document files instantly) raised $300m at a valuation of $2bn. The round was led by Index Ventures, with participation from ICONIQ Growth and Teachers Ventures as well as existing investors IVP, Atomico and WiL. Founded in 2017 it says its translation technology has ‘a customer network of 100k+ businesses, governments, and other organisations worldwide’ including Zendesk, Nikkei, Coursera and Deutsche Bahn.

Defence AI company Helsing raised $226m at a valuation of $1.65bn in September 2023 in a deal led by General Catalyst. In July 2024 it followed this up with a $487m round led by General Catalyst valuing the company at $5.4bn.Helsing was founded in 2021 and describes itself as ‘a new type of defence company, developing AI-based capabilities to protect our democracies.’ It uses AI to process vast amounts of battlefield data to create a decision-making picture.

The top European deals in Artificial Intelligence in 2024 –10 deals of $100m+ raising $3.4bn

Software – still prominent: In 2023 the top three fundraising sectors were Climate Tech, software and AI. The top three are the same in 2024 although software drops to third after being substantially overtaken by AI. In 2024 thirteen software deals produced funding of $2.7bn, virtually identical to 13 deals raising $2.7bn in 2023. As the breakdown shows the software category fell into two parts with eight software and cybersecurity deals for a broad range of industries raising $1.4bn, and the substantial sub category of travel software applications raising $1.3bn in five deals.

French HR software business HR Path raised $550m in July in the largest deal in the sector. It was led by Ardian. The company provides consultancy services, HR systems implementation and payroll outsourcing, enabling companies to optimise their HR functions. The company earmarked a substantial portion of the proceeds for international expansion and acquisition and followed up the raise with the purchase of IN-RGY, a Canadian HR consulting firm in October and Mexican payroll management business Pay Human Group in December.

Another French business Pigment raised a $145m Series D led by Iconiq Growth. Its previous $88m round in June 2023 was also led by Iconiq. The company offers a business planning platform used to gather business data, create reports and assist business planning. The company includes Unilever, Merck, Datadog and Keolis amongst its customers.

Bending Spoons, the Italian owner of the MeetUp and Evernote apps, raised $155m in a deal led by Durable Capital Partners in February It valued the company at $2.55bn.

The top European deals in Software in 2024 –8 deals of $100m+ raising $1.4bn

It was a strong year for raises in travel and booking management software. Travelport competes with Amadeus and Sabre as a global distribution system, acting as an intermediary between airlines and travel sellers. It raised $570m in January in a deal led by Elliott Investment Management and Davidson Kempner Capital Management designed to strengthen its post pandemic balance sheet.

In early December KKR led a $500m Series C in Lighthouse (formerly OTA Insight). Lighthouse is a commercial intelligence platform for the hospitality industry. Its products provide accommodation owners with tools to drive incremental bookings and streamline operations. The platform is underpinned by proprietary technology that processes over 400 terabytes of travel and market data daily.

Swedish business Visit Group supplies collaborative commerce software to ‘experience vendors’ such as lodgings, day tours, attractions and amusement parks. PSG Equity established a majority stake with its $110m investment. Mews provide SaaS based software tools to hotels covering functions like room booking, check-in, payments, reservations and housekeeping management. It raised $110m at a $1.2bn post money valuation in a round led by Kinnevik in March. Its previous end 2022 $185m raise was at an $865m valuation.

Kinnevik also led the $104m Series D raise by TravelPerk, the Spanish business travel platform in January at a valuation of $1.4bn. Travel Perk offers a comprehensive platform aimed at SMEs allowing them to book, manage and report all their domestic and international travel.

…plus five deals in Travel software applications raising $1.3bn

Fintech – better, still subdued: It was a better but still subdued year for primary fintech deals in 2024 with five deals raising $1.3bn versus seven raising $1.1bn in 2023.

The leading light in 2024 was neobank Monzo which announced two primary raises, $430m at a valuation of $5bn in March and $190m in May at a $5.2bn valuation. Monzo has 9m plus retail customers and 0.4m corporate customers in the UK and has targeted part of the funding for expansion in the US. In addition to the primary deals Monzo had a secondary offer in early October, which valued the business at $5.9bn. The shares were mainly sourced from existing employees with buyers including StepStone and GIC of Singapore.

Elsewhere Zepz, an international money transfer platform – it owns WorldRemit and Sendwave- raised $267m from Accel, Leapfrog and IFC in October. Insurtech Alan is a digital health insurance company which aims to revolutionise health insurance by improving user experience while providing an strong price-quality ratio health plan. It raised $190m in a Series F at a valuation of $4.4bn in a deal led by Belfius in September. It was last valued at €2.7bn when it raised a €183m Series E in 2022.

As in the US, the underlying appetite for the sector was confirmed by the secondary deals seen in 2024. As well as the Monzo deal, Moneybox, the UK savings and investment platform, announced a secondary share sale in October with the Apis Global Growth Fund III and Amundi jointly investing c£70m in a deal valuing it at £550m, up 84% over the March 2022 Series D valuation and almost three times the level of its July 2020 Series C. Another UK fintech, GoCardless, is in the process of arranging a secondary sale for employees, worth as much as $200m.

The top European deals in Fintech in 2024 –8 deals of $100m+ raising $1.6bn

Online grocery delivery -No picnic: Share prices in the quoted online food and grocery delivery businesses largely marked time in 2024 and it was a similar mixed picture for their private equivalents.

The big event of the year was the retrenchment at Getir. Founded in 2015 the super-fast grocery delivery business Getir operated initially in Turkey but explosive pandemic growth combined with VC backing of $2.25bn between January 2021 and September 2023 for international expansion followed. In March 2022 Getir raised $768m at a valuation of $11.8bn. At end April 2024 Getir announced its withdrawal from the US and Europe and its re-focus on Turkey where "the opportunities for operational profitability and sustainable growth are stronger." It raised a further $250m in a deal led by major shareholder, Mubadala, to facilitate the retrenchment.

Mubadala also led a deal alongside BOND in September to raise $115m at a valuation of just under $1bn for German quick commerce business, Flink. Flink, a company supported by the German supermarket chain, Rewe, US food delivery group DoorDash as well as Mubadala had briefly entered merger talks with Getir in May 2023. Flink will use the proceeds to consolidate its business in Germany and the Netherlands in partnership with Just Eat Takeaway.

Dutch eco-friendly online supermarket Picnic had the biggest raise of the group in 2024, $389m in January backed by the German supermarket chain, Edeka and the Bill & Melinda Gates Foundation. Picnic, which operates in the Netherlands, France and Germany, uses electric vans to deliver, has a substantial own brand offering and offers free delivery.

In June Czech business Rohlik raised $170m led by the European Bank for Reconstruction and Development and Sofina. The valuation is said to have exceeded the $1.3bn mark set in its previous round in 2022. Rohlik has operations in the Czech Republic, Austria, Germany Hungary and Romania and has a target of reaching €1 billion in revenues and positive cash flow by the end of 2024

The top European deals in online grocery delivery in 2024 –5 deals of $100m+ raising $1.0bn

Biotech – Revival continues: There were ten deals of $100m+ in European Biotech in 2024 up from seven deals raising $845m in 2023. By the nature of the business biotech deals tend to be of a smaller size than those in many other sectors.

The sector closed the year with some of its larger deals. In November Alentis Therapeutics raised $181m in a Series D funded by Orbimed, Novo Holdings and Jeito Capital. Alentis is developing breakthrough treatments for CLDN1+ tumours. Adcendo which is developing antibody-drug conjugates for cancers raised $135m in a Series B led by TGCX, TPG Life Sciences and Orbimed. July was another strong month with seven deals raising $712m including those for Beacon Therapeutics ($170m), CatalYm ($150m), Myricx Bio ($114m) and Ascenreuron ($100m).

The top European deals in biotech in 2024 –10 deals of $100m+ raising $1.1bn

The closely associated field of Healthcare and medical devices saw seven deals raise $0.85bn.

The biggest raise in this group was $200m for Flo Health, a fertility tracking app with 70m active users. The Series C was backed by General Atlantic and valued the business at more than $1bn post money. Its previous round was a Series B of $50m in 2021. Its founder Dmitry Gurski gave an excellent exposition of the challenges he has faced in moving from his first job on a potato farm to running a unicorn at the Slush conference in Helsinki in November.

Medical device business Mainstay Medical raised $125m in February in a deal led by Gilde Healthcare and Viking Global Investors. The company is using the money to commercialise its key product, ReActiv8, an implantable restorative neuromodulation system for adults with intractable chronic low back pain.

Gilde Healthcare, along with Sofinnova also led the $1205m Series B for Purespring Therapeutics in October. The company is developing gene therapy for kidney diseases.

The US saw a lot of funding for companies looking to solve obesity problems using GLP-1 drugs in 2024. In Europe Six Peaks Bio has therapies that help preserve muscle in patients who achieve substantial weight loss. It has an activin receptor antibody that aids weight loss while preserving skeletal muscle mass which can be used in conjunction with GLP-1 antagonists. The company’s total $110m raise announced in May combined a $30m Series A led by Versant Ventures with a strategic collaboration with AstraZeneca providing financing of up to $80 million over the next two years.

The top European deals in healthcare and medical devices in 2024 –7 deals of $100m+ raising $0.9bn

Semiconductors steady: A missed opportunity to use the ‘chips are down’ headline as the $0.544 bn raised in three deals in Europe in 2024 marginally exceeded the $0.541bn in four deals in 2023.

German business Black Semiconductor raised a $276m (€254m) Series A with the bulk of the money, €230m, coming from the federal government and the state of North Rhine-Westphalia. Porsche Ventures led the balance of the funding which will be used to expand Black’s operations in the production of graphene-based chips. The state funding comes from the €8.1bn European IPCEI Microelectronics programme.

Nearfield Instruments is one of a cluster of semiconductor and photonics businesses based in and around Rotterdam. It raised $148m in a Series C in July led by Walden Catalyst and Temasek but also encompassing regular investors in that cluster, Innovation Industries, Invest-NL, and ING.

April’s $120m raise for Israeli business Hailo is AI related. The company designs semiconductors which carry out chips execute AI tasks with lower memory usage and power consumption than a typical processor making them useful for smaller mobile environments and applications.

The top European deals in semiconductors in 2024 –3 deals of $100m+ raising $0.5bn

Three smaller categories:

There were two SpaceTech deals of $100m+ in 2024. D-Orbit, an Italian in-space logistics company which specialises in the orbital transfer vehicle (space tug) market raised $166m in from Marubeni Corporation, CDP, and Seraphim Space in September. The European Space agency signed a €119m contract with the company to start commercial life extension services for geostationary satellites.

Space services business The Exploration Company which has developed Nyx, a reusable space capsule, raised $165m at a $465m post money valuation in a deal led by Balderton Capital.

The top European deals in SpaceTech in 2024 –two deals of $100m+ raising $0.3bn

There were three deals in drones and Aerospace at $100m+. Quantum Systems describes itself as a global leader in EVTOL (electric vertical take-off and landing) drones specialising in the collection of aerial data for use by military, government, and commercial users. The German business raised $110m in a Series B with Norton Capital and Porsche. Skyports is developing landing sites for flying taxis. Its so-called vertiports are being established in Dubai International Airport, Palm Jumeirah, Dubai Downtown and Dubai Marina. Its Series C of $110m was backed by infrastructure and construction business ACS group.

The mission of Heart Aerospace is to electrify regional air travel. The Swedish business raised $107m in a deal supported by Bill Gates’ Breakthrough Energy Ventures, the European Innovation Council Fund, United Airlines and Air Canada. Its first hybrid-electric plane awaits certification with first flights targeted for 2028. Its planned 30 seater plane, the ES-30 has an all-electric range of 200km and a hybrid-electric range of 400km.

The top European deals in Drones and Aerospace in 2024 –three deals of $100m+ raising $0.3bn

We have used the term automotive to capture the activity of the next two businesses.

Croatian business Project 43 Mobility, since June renamed Verne, aims to launch an autonomous electric taxi (robotaxi) in Zagreb in 2026. The company aspire to "redefine urban mobility" and "build an urban ecosystem for autonomous, safe, and effortless movement." Notably the founder is Mate Rimac, the founder and CEO of the electric sports car maker Rimac Group, and of Bugatti Rimac. The other notable feature was that its $110m Series A in January saw the first investment outside Saudi Arabia of TASARU Mobility, part of the Saudi Arabia Public Investment Fund.

Also in January FINN, a company that operates a new car subscription business in Germany, raised $110m in a Series C led by Planet First Partners. New cars are offered on one year subscriptions – a shorter timescale than most leasing arrangements (3-5 years) but much longer than a typical car rental. Prices range between €430 and €1200 per month.

The top European deals in automotive in 2024 –two deals of $100m+ raising $0.2bn

Six other notable deals: We capture six businesses that sit outside the sector categories above.

In November marketing technology business Insider raised a $500m Series E led by General Atlantic. Insider describes itself as an omnichannel experience and customer engagement platform. The Turkish company aims to develop further its marketing software offering, invest in AI related R&D and to grow its staff base and geographic footprint.

Everphone, a German platform for corporate smartphone and tablet management raised a total of $297m in equity and debt in a January Series D.

German connected fitness business EGYM raised $200m in its Series G led by L Catterton and Meritech, in a deal valuing the company post money at $1.2bn. It last raised $225m in July 2023 in a deal led by Affinity Partners. Back then, its corporate health network operation, Wellpass had more than 2.5 million users. Now it has 17,000 sports partners (gyms), 14,000 corporate customers, and 3 million 'eligible' users.

French flexible storage business Lockall raised $170m in funding from Starwood Capital to develop itself storage site network across the Ile-de-France.

Build a Rocket Boy, the Scottish games business raised $110m in January led by Redbird Capital.

Razor Group, an e-Commerce aggregator raised $100m in a deal led by Presight Capital in March

Other top European deals of $100m+ in 2024

2024 European deals of $100m-$199m – 63 deals raising $7.9bn

November – another big month in the US for VC raises.

And rounding up activity in November…

Another very strong month for venture capital raises in the US. Our Monitor recorded 26 deals at $100m or more topped by another two substantial AI raises in the aftermath of the $6.6bn raise for OpenAI in October.

xAI raised $6bn from investors at a valuation of more than $50bn.This followed its previous raise, also of $6bn, which took place in May this year and which valued the company at a pre -money valuation of $18bn. The business started in July 2023. Names of the investors were not revealed but the number was, there were 97 investors in the round, some with stakes below $100k. Larger investors in the round are believed to have been the QIA, Valor Equity Partners, Andreessen Horowitz and Sequoia.

Anthropic raised $4bn in November, this time from a single investor, Amazon in a deal said to value the company at $30bn-$40bn. This matched the size of Anthropic’s previous Amazon-backed round - $4bn in September 2023. In between Anthropic raised a $1.2bn Series D led by Menlo Ventures in January 2024 valuing the company at $18bn.

In total US venture raises for the month stood at $16.4bn, the biggest month of the year to date.

The US – $16b.4n of US venture backed raises of $100m+ in October

There were a further four deals of $400m or above.

Tricentis , a business that performs testing and quality engineering for software releases by enterprises raised $1.3bn at a valuation of $4.5bn in a deal led by GTCR.

LogicMonitor is an IT monitoring business which manages complex IT infrastructures in hybrid and multi-cloud environments like data centres. It raised $800m at a $2.4bn valuation in a deal led by PSG Equity and Golub Capital.

Third party reinsurance business, Ruby Re raised $480m in a funding round led by AllianceBernstein, EnTrust Global, and Enstar Group.

AI robotics business Physical Intelligence which is developing practical artificial intelligence models to create “brains” for robots raised $400m in a funding round led by Jeff Bezos, Thrive Capital and Lux Capital which valued the company at $2.4bn post-money. Its previous round was a $70m seed round in March led by Thrive Capital.

Europe: Our Deal Monitor recorded $2.2bn of venture capital raises in Europe in November, down 25% yoy. Cumulatively though YTD 2024 European raises stood at $31.3bn at end November, up 11% yoy.

The month’s biggest raises were:

KKR led a $500m Series C in Lighthouse (formerly OTA Insight). Lighthouse is a hospitality's commercial intelligence platform for the hospitality industry.

Two biotechs next. Alentis Therapeutics raised $181m in a Series D funded by Orbimed, Novo Holdings and Jeito Capital. Alentis is developing breakthrough treatments for CLDN1+ tumours. Adcendo which is developing antibody- drug conjugates for cancers raised $135m in a Series B led by TGCX, TPG Life Sciences and Orbimed.

Tessl is building a system of record for AI native development – an open platform that enables and accelerates the work of AI-native developers. The UK AI company announced $125m of fundraising – consisting of a £$25m seed round by boldstart and GV in April and a new $100m Series A led by Index and Accel.

ChapsVision is a software business which handles the data operating systems of large companies and administrations. The French business raised $90m in a funding round led by Tikehau Capital, Qualium Investissement and Bpifrance.

Europe - $2.2bn of raises in November

Our views on the state of the venture capital markets

The combination of global inflation, rising interest rates, and increased geopolitical risk substantially impacted the venture capital market in 2022 and 2023. As we have moved through 2024 adaptation to the ‘new normal’, the refocusing of venture-backed companies to achieve a better balance of growth, profitability and cash flow and the delivery of interest rate cuts have led to increased optimism and enthusiasm for growth equity. Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment has had a sharp impact on valuations in private markets. The scale of the fall in the Refinitiv VC index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023.

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models, the applications of AI and industries (data centres, semiconductors) supporting the development of AI.

- Best-in-class companies, addressing critical requirements, continue to attract support. There are still hotspots for investment most notably in Artificial Intelligence and Climate Tech. Certain investors remain very active in the space with substantial funds to deploy.

- The speed of the investment process has slowed. The level of diligence on new deals has stepped up.

- 2023 saw more downrounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these. These have continued into 2024.

- There is substantial dry powder in the VC industry. This though appears to be prioritised to support existing rather than new investments

- It seems likely that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses.

- Valuation priorities have shifted with investors having moved away from an emphasis on revenue growth and revenue multiple emphasis. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and an emphasis on DCF and comparative based multiples.

Read the previous editions:

May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024

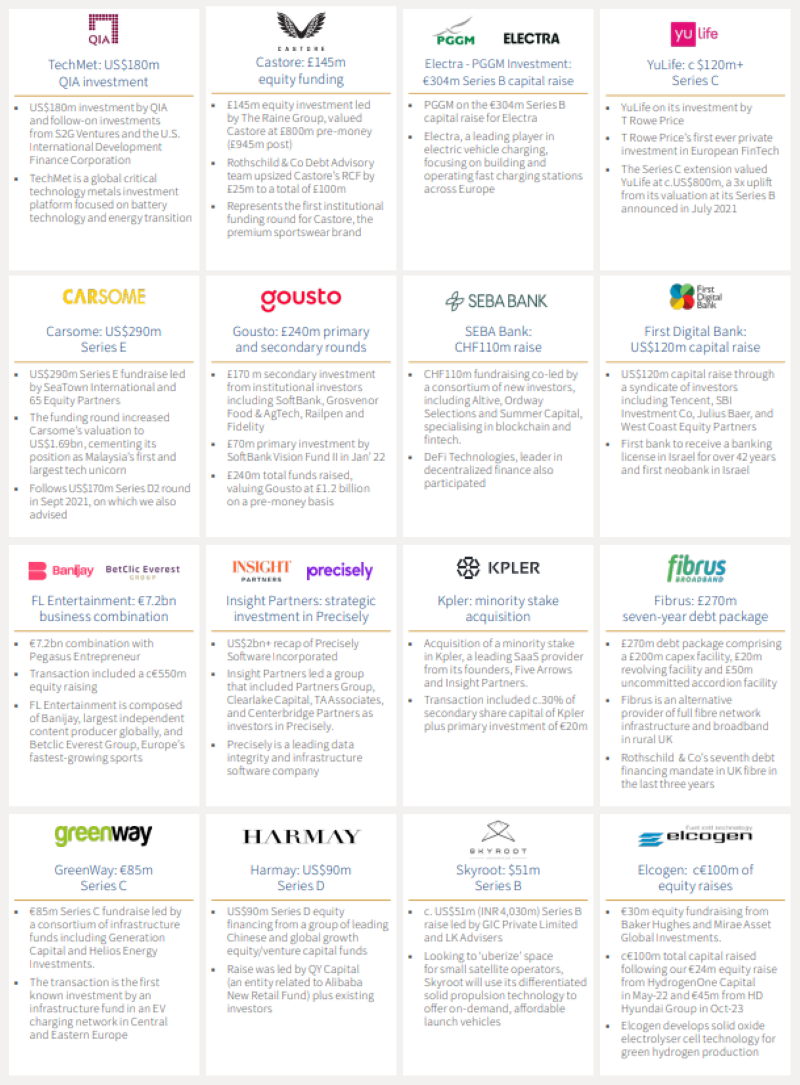

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised

For more information, or advice, contact our Growth Equity team:

Chris Hawley

Global Head of Private Capital

chris.hawley@rothschildandco.com

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Advisory

patrick.wellington@rothschildandco.com

+44 20 7280 5088

+44 7542 477 291

Mark Connelly

Head of North American Equity Markets Solutions

mark.connelly@rothschildandco.com

+1 212 403 5500

+1 917 297 5131

Stéphanie Arnaud

Managing Director – France

stephanie.arnaud@rothschildandco.com

+33 1 40 74 72 93

+33 6 45 01 72 96

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.