Few US stocks drive global markets

Investment Communications Team, Investment Strategy Team, Wealth Management

Summary

Global equities rose by 2.2% in June (USD terms), while global government bonds returned 0.9% (USD, hedged terms). Key themes included:

- Stock markets rose further, mostly led by the US mega-cap names;

- The ECB commenced its easing cycle. The Fed is expected to follow this year;

- European politics moved into focus with Macron’s snap election decision.

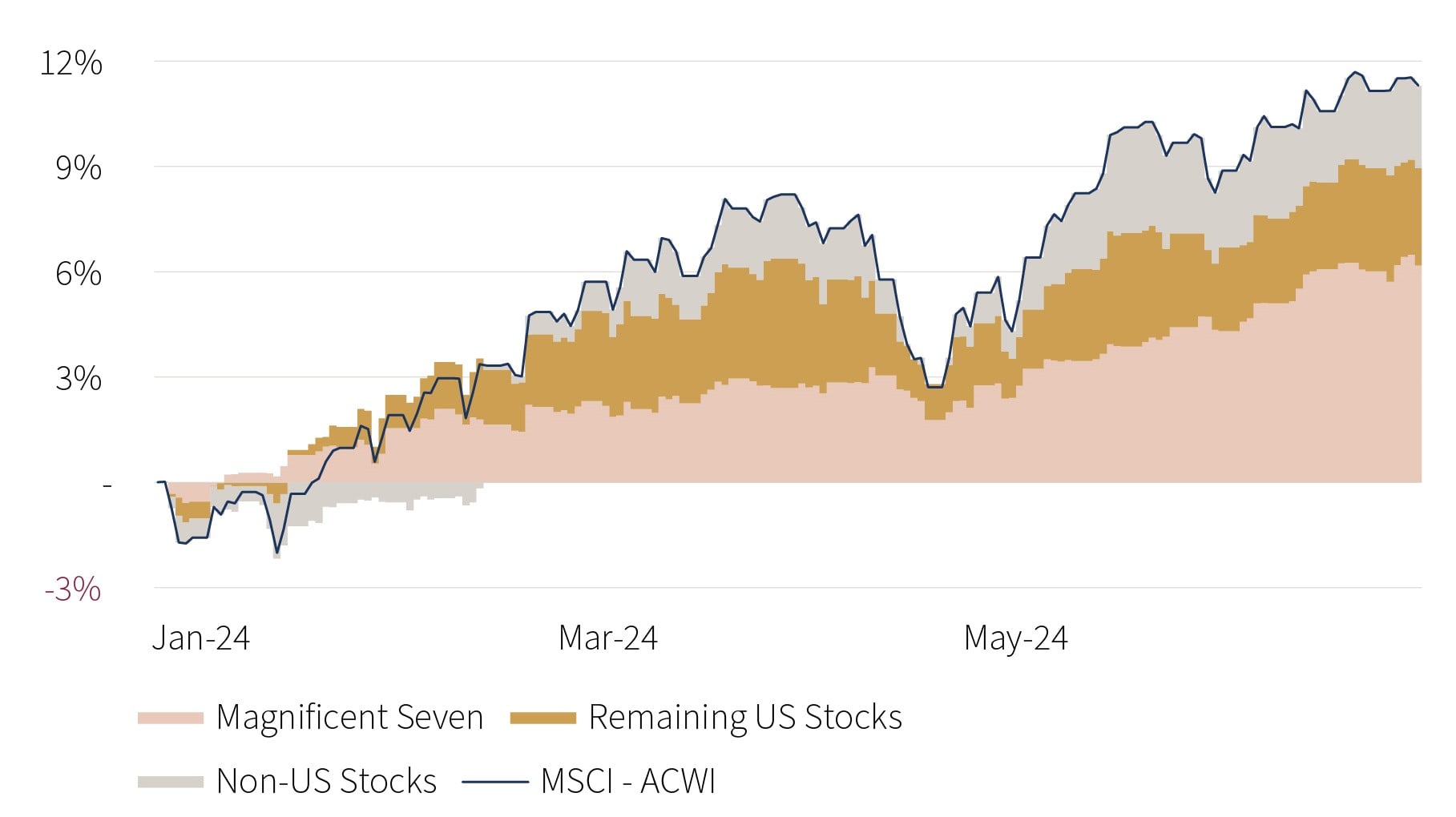

Global stock market contribution - Year-to-date (%pts, USD)

Source: Rothschild & Co, Bloomberg

Chart note: The Magnificent Seven consist of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

Markets: A narrow stock market ascent

Global stocks rose to fresh highs in June, though this was again largely driven by the US market – and within it, some of its (AI-related) mega-cap names. Global stocks excluding the US were flat in June, as was the equal-weighted US index. The EM Asia cohort also stood out, with the two big semiconductor-intensive nations – Taiwan and Korea – outperforming. In fixed income, 10-year government bond yields modestly drifted lower across the US and Europe – a prominent exception being France, where the OAT spread over Germany widened after Macron’s surprise snap election decision (however, the spread remained tighter than during the eurozone debt crisis). In currency markets, the euro softened against most major currencies, yet it was the Japanese yen which stood out: it weakened to multi-decade lows against the US dollar and to a record low against the euro. Commodity prices fell in June – particularly industrial metals and agriculture – but Brent Crude oil rebounded by 6%, to $86 p/b.

Economy: Inflation patchily abating

Real-time US GDP estimates continued to suggest another quarter of solid economic growth, with retail sales and industrial production expanding in May, though the closely-watched ISM manufacturing PMI remained subdued in June. The labour market also remained tight and jobs growth in May surpassed economists’ expectations. US inflation continued to cool: the headline rate edged lower to 3.3% (y/y), while core inflation fell to 3.4% – its lowest reading in three years. In Europe, the timelier business surveys softened in June, but continued to signal economic expansion. UK hard data remained robust: monthly GDP stagnated in April, but this was ahead of consensus, and May retail sales rebounded strongly. Inflation developments were mixed. Eurozone inflation moved higher in May, though both the headline and core rate remained below 3%. Services inflation reaccelerated, and remained the stickiest CPI category on both sides of the Atlantic. Promisingly, UK headline inflation fell to the Bank of England’s 2% target, while core inflation moved lower as well, albeit to a higher rate of 3.5%.

Policy: ECB and SNB cut rates; Macron’s gambit?

Several developed-market central banks began their easing cycles in June. Among those, the European Central Bank unsurprisingly cut its deposit rate by 25bps, to 3.75%, while the Swiss National Bank lowered its main policy rate for the second consecutive meeting. Conversely, the US Federal Reserve and Bank of England left their interest rates unaltered – but both suggested that they were still likely to move lower this year. The former’s updated interest rate projections were more hawkish, showing just one cut in 2024. Meanwhile, the Bank of Japan’s ultra-loose policy stance was unchanged.

It was a busy month within the election cycle: the first US presidential debate took place – which featured a concerning performance from Biden – and incumbent parties retained power in India, Mexico and South Africa. In the European Parliamentary election, there was a shift to the right, with the centre-right EPP – and far-right parties – gaining seats at the expense of the centre-left and green parties. However, the major surprise was Macron’s decision to call a snap parliamentary election in France, in which Le Pen’s Rassemblement National gained a third of votes in the first round (Macron’s alliance obtained just over 20% of the vote). Elsewhere, the UK was set for its general election on July 4th, with Labour remaining well ahead in the polls.

Performance figures (as of 28/06/2024 in local currency)

| Equity (MSCI indices $) | Month | Year |

|---|---|---|

| Global | 2.2% | 11.3% |

| US | 3.5% | 14.6% |

| Eurozone | -2.9% | 6.4% |

| UK | -1.8% | 6.9% |

| Switzerland | 0.0% | 1.8% |

| Japan | -0.7% | 6.3% |

| Pacific ex Japan | 0.3% | 0.7% |

| EM Asia | 5.0% | 11.0% |

| EM ex Asia | -0.1% | -5.1% |

| Fixed income | Yield | Month | Year |

|---|---|---|---|

| Global Govt (hdg $) | 3.36% | 0.9% | -0.1% |

| Global IG (hdg $) | 5.04% | 0.7% | 0.3% |

| Global HY (hdg $) | 8.26% | 0.7% | 3.9% |

| US 10Y | 4.40% | 1.3% | -1.6% |

| German 10Y | 2.50% | 1.5% | -2.4% |

| UK 10Y | 4.17% | 1.3% | -2.6% |

| Switzerland 10Y | 0.60% | 2.7% | 1.4% |

| Currencies (NEERs) | Month | Year |

|---|---|---|

| US Dollar | 1.7% | 4.7% |

| Euro | -0.7% | 0.4% |

| Pound Sterling | 0.2% | 2.9% |

| Swiss Franc | 1.6% | -3.4% |

Table note: NEERs under ‘currencies’ are the JP Morgan trade-weighted nominal effective exchange rates

| Commodities ($) | Level | Month | Year |

|---|---|---|---|

| Gold | 2327 | 0.0% | 12.8% |

| Brent Crude oil | 86 | 5.9% | 12.2% |

| Natural gas (€) | 34 | 0.8% | 6.6% |

Source: Bloomberg, Rothschild & Co.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.