Navigating political noise

Foreword

‘A politician thinks of the next election, a statesman thinks of the next generation.’ ― James Freeman Clarke, American theologian and author

This year, more than two billion people are expected to vote in key national elections that could shape their countries' future for generations to come.1 The Economist has even dubbed 2024 ‘the biggest election year in history’, with 76 nations going to the ballot box before 31 December.2

Elections can inspire hope and spark positive change, but they also represent uncertainty for markets. That uncertainty is only magnified in a year where dozens of countries, comprising almost half of the planet's population, will hit the polls.

At the time of writing, elections have already taken place in Taiwan, Russia , Indonesia, Pakistan and Bangladesh, among others. As investors with a global perspective, we carefully monitor how the outcomes of these elections may affect the geopolitical landscape and our strategies.

However, the two elections that are likely to hold the greatest significance for us and our clients are still on the horizon – the US presidential election and the UK general election.

The date for the US election is already set for 5 November. The UK could head to the polls any time between now and January, but Prime Minister Rishi Sunak has indicated he will call an election in 2024.3 If both elections take place this year, it will be the first time since 1964 that the UK and the US decide their next heads of government in the same calendar year.

We invest in several high-quality British and American companies , so the impact of parallel elections shouldn't be underestimated. But we'd like to reassure our clients that we're accustomed to political upheaval at Rothschild & Co. Although past performance is no indicator of future results, we believe we have a long-term track record that shows we have weathered many storms, political or otherwise.

Nathan Mayer Rothschild first established his business at New Court in 1809, and it remains our home to this day. In that time we’ve seen many different US presidents and British prime ministers arrive – 42 on both counts . Throughout that time the family’s philosophy has remained the same, aiming to preserve and grow your wealth for future generations, in good times and bad, regardless of the political backdrop.

Thank you for reading.

Helen Watson

CEO, Rothschild & Co Wealth Management UK

Navigating political noise

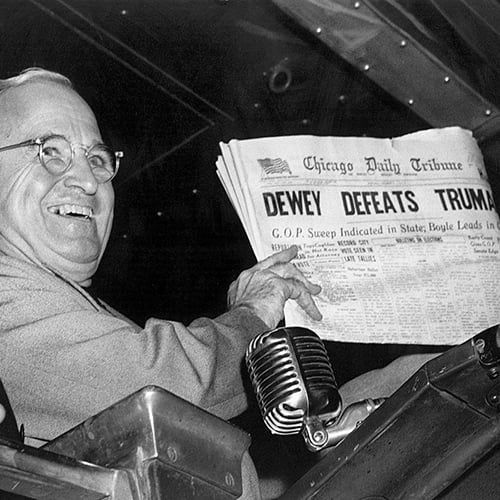

In 1948, US Democratic President Harry S Truman was in the midst of a bruising re-election campaign, and it wasn't looking good.

Within just a year of steering the country though the final months of the Second World War, Truman scored the lowest ever mid-term approval rating (33%) – a record that stands to this day.

The situation had improved by 1948, but barely. The economy was faltering, Truman was facing attacks from both the Republicans and his own party, and the press continually painted the Missouri native as coarse and unrefined.

Almost all the polls predicted that Truman's opponent, Thomas E Dewey, would win a landslide victory. The Chicago Daily Tribune, a Republican-leaning paper, was so confident about the result that it went to press with the headline ‘Dewey Defeats Truman’ on election night before most states had finished reporting their results.

Unfortunately for the paper's editors, they'd jumped the gun. Truman snatched victory from the jaws of defeat in one of the biggest upsets in presidential election history.

His win is often attributed to a 31,000-mile whistle-stop tour across the country, where he made 352 speeches and won over American voters face-to-face with his folksy charm. Photos of a jubilant Truman holding a copy of the Tribune's erroneous early edition are now among the most famous political images of all time .

Truman's unexpected victory can teach us some valuable lessons about both politics and investing as the planet heads to the polls in 2024. Namely, the future is full of surprises, and having too much confidence in forecasting can be a recipe for disaster.

Originally distributed by the Associated Press on 5 November 1948. Byron H. Rollins. Sourced from Creative Commons.

Key election dates in 2024

- April to June – Indian general election

- 2 June – Mexico general election

- 6-9 June – European Parliament election

- 5 November – US presidential election

- Expected in 2024 – UK general election

Polling problems

In the decades since Truman's re-election campaign, political forecasting has become big business. Today, predictive models are more sophisticated, sample groups are larger, and statistical tools can handle a dizzying amount of data.

But pollsters still make mistakes. In 2016, European Union referendum polls consistently predicted a win for the remain campaign, while stateside, many forecasts underestimated support for the Republican nominee Donald Trump in the presidential election.

As we now know, the majority of British voters chose for the UK to leave the EU, and Trump went on to defeat Democrat nominee Hillary Clinton for the presidency, despite losing the popular vote.

Four years later, pollsters still hadn't ironed out all the kinks in their algorithms. National opinion polls ahead of the 2020 US election were the most inaccurate in 40 years, according to the American Association for Public Opinion Research.4

While most pollsters correctly predicted a win for Democrat Joe Biden, his margin of victory was much slimmer than many forecasts suggested.

‘Politics is not an exact science,’ Germany's first chancellor Otto Von Bismarck once remarked. It appears the same can be said for political polls.

Suffice to say, the road to the White House looks open for both Biden and Trump, and we're expecting a noisy, abrasive campaign ahead.

Second chances

If Trump is re-elected in 2024, he will become the first person to serve two non-consecutive presidential terms since Grover Cleveland, who was both the 22nd (1885–1889) and 24th US president (1893–1897).

In the UK, the outcome of the general election appears to be more predictable. The Labour Party are polling 20 points higher on average than the ruling Conservatives at the time of writing, having maintained a consistent double-digit lead for more than 18 months.5

With Truman's upset victory fresh in our minds, let's not count any electoral chickens before they've hatched. It's also useful to remind ourselves of former Prime Minister Harold Wilson's famous words that ‘a week is a long time in politics’, particularly as there are potentially months of twists and turns ahead.

The perils of short-termism

If past elections tell us anything, it's how difficult it is to predict the future.

Politics, like financial markets, can be fickle, so we at Rothschild & Co avoid placing too much faith in our ability to forecast which way the wind will blow. Often, the speed with which political power changes hands means those winds rarely blow in the same direction for too long anyway.

Short-termism is already a well-known problem in politics. Most leaders only have a relatively brief window of time in office, during which they usually focus on implementing quick, popular policies that will win over the electorate today.

Any thankless, long-term tasks that won't reap dividends in the immediate future become less of a priority, so it's tempting to kick the can down the road for others to pick up.

Even when leaders have the appetite to tackle generational issues, they may lack public support or enthusiasm. After leaving office, former US President Barack Obama acknowledged this difficulty in relation to climate change.

‘One of the hardest things in politics is getting a democracy to deal with something now where the payoff is long term or the price of inaction is decades away,’ he said.8

Jean-Claude Juncker, the former president of the European Commission, was more candid when talking about economic reforms: ‘We all know what to do, we just don't know how to get re-elected after we've done it.’9

It is perhaps unfair to only pick on politicians. Business leaders and investors can also be guilty of short-term thinking.

For example, in one survey of more than 400 US chief financial officers, 78% said they'd be willing to make decisions that would damage their company's long-term value in order to hit upcoming earnings targets.10 And those are only the ones that admitted it.

Among investors, meanwhile, the average holding period for shares on the New York Stock Exchange peaked at nearly eight years in the 1960s but has since fallen to approximately 10 months.11

In his book The Long View, journalist Richard Fisher says this trend is hardly surprising, given the average age of an S&P 500 company has plummeted from almost 60 years in the 1950s to around 20 years today.

In an unfortunate twist of fate, the research he cites was conducted by Credit Suisse, which itself would collapse shortly before The Long View was published.

According to Fisher, a key turning point in the shift towards short-term thinking was the US introducing mandatory quarterly reporting in the 1970s. Quarterly reporting has since become common practice across many nations and industries.

‘When senior leadership is forced to make promises to the market, so frequently, it's almost inevitable that this discourages the long view,’ Fisher explains.

Politics is not an exact science, Germany’s first chancellor Otto Von Bismarck once remarked.”

Looking to the long term

Unpredictable politics, polling problems and the long shadow of short-termism. As investors, how do we account for these challenges as dozens of democracies head to the ballot box this year?

As we've mentioned, Rothschild & Co is no stranger to tumultuous times. Over more than 200 years, our businesses have survived some of history's biggest political and economic shocks, including world wars, global depressions and the birth of new nations.

Indeed, our company was established not long after the United States of America itself.

Thomas Jefferson, who drafted the Declaration of Independence, finished his second term as US president in March 1809, which is the same month and year that Nathan Mayer Rothschild founded the London house of Rothschild at New Court, St Swithin's Lane .

At the time, Abraham Lincoln was just a few weeks old, and George III was still on the British throne.

The value of long-term leaders

Franklin D Roosevelt was the longest-serving US president, clinching an unprecedented fourth term in 1945.6 During his 12 years in office, he not only oversaw the ‘New Deal’ – a series of ambitious reforms and infrastructure projects – but also guided the US through most of World War II.

FDR's popularity has stood the test of time. He recently ranked second in a new poll of best presidents.7 Notably, every other president in the top ten, aside from John F Kennedy, served two terms.

We do not believe this is a coincidence. At Rothschild & Co, we view longevity as a clear indicator of quality in leaders. It signifies commitment, stability and resilience, all of which suggest a management team that is focused on delivering over the long term.

Take John Deere as an example. The company was founded in 1837, and during that time it's had fewer leaders (10) than there have been popes (12). The average tenure of a CEO at John Deere is nearly 19 years.

Many of our third-party fund managers have similarly long-serving leadership teams. Ward Ferry, which invests in dynamic small companies across Asia, has been led by Scobie Ward and Vineet Mitera since 2005.

So, it's fair to say we've seen a lot of change and disruption throughout our long history, and yet our goal remains the same: to preserve and grow our clients' wealth, in real terms, over many years and indeed generations.

We have successfully served our clients' best interests through the tenures of many good political leaders, some even great. But, just as importantly, we've been able to support our clients through the premierships of those who were not so good.

This is because our investment approach, which is ‘bottom up’ rather than ‘top down’, is designed to weather all market conditions and help us achieve strong performance in the long term.

BOTTOM-UP INVESTING

For top-down investors, timing is everything. They seek to anticipate changes in political and macroeconomic currents, so they can evaluate the downstream effects in an effort to buy and sell assets at the best times.

But as we've seen, predicting what will happen tomorrow is a tricky task that even the best forecasters frequently get wrong. Even if a prediction turns out to be right, there's still no guarantee how markets will react on any given day.

Our bottom-up investment approach doesn't try to time the markets in this way. Instead, we believe that competitively advantaged companies with strong management teams, resilient business models and sustainable business practices are more likely to succeed and gain value over the long term than their competitors.

When priced attractively, these are the high-quality companies that we want to own and hold for a very long time. The average holding period of a company in our portfolios is seven years, which is far closer to the average for investors in the 1960s than today.

By concentrating on longer time horizons, we seek to cut through much of the short-term market noise and political playmaking that can muddy investment decision-making.

We have successfully served our clients’ best interests through the tenures of many good political leaders, some even great."

The 'Lindy effect'

According to statistician and essayist Nassim Nicholas Taleb, a good way to predict the life expectancy of non-perishable things, such as businesses, ideas or technology, is to examine how long they have already existed.

He calls this the 'Lindy effect' – the longer something has lived, the longer it will live on. The concept derives its name from Lindy's delicatessen in New York, where it was originally theorized.12

If that's true, some of the businesses we invest in can be expected to thrive for many more centuries to come. Companies such as John Deere, S&P Global and American Express have histories as long as our own, while many others in our portfolio are more than 100 years old.

Finding exceptional companies requires patience. It also involves extensive proprietary research and analysis, as well as ongoing review, to be confident that we continue to invest only in high-quality holdings.

Furthermore, these growth-oriented investments – our 'return assets' – are balanced with diversifying assets to protect our portfolios against the risk of large losses during inevitable market downturns.

Ultimately, our aim is to own investments that we expect to perform well across a range of political and economic scenarios. Experienced investors know that past performance is no indicator of future returns. At the same time they also know the value of seeking wealth managers who can demonstrate a strong track record.

Asset Risk Consultants (ARC) has been collecting data on wealth managers for the last 20 years. As one of the founding data contributors, we can use the ARC statistics to demonstrate the long-term growth we’ve offered clients in that time.

Based on the return of a typical sterling ‘steady growth’ investment strategy, a portfolio would have grown by 195% over the 20 years to December 2023. An investment into a Rothschild & Co portfolio over the same 20-year period would be worth 257%.

Stable stewardship

New governments represent change. Their policies both at home and abroad can shape a country's society and economy for many years, if not decades, so it's easy to fear for the future when market noise reaches fever pitch during an election year.

And 2024 is perhaps the election year.

At Rothschild & Co, we remain vigilant to any factors, political or otherwise, that may affect our investments now or in the future. However, we also recognise that politics, like financial markets, is so often cyclical.

For example, much has changed since 1964, when the US and the UK last elected their leaders in the same year, but there are many similarities too.

Some 60 years ago, the UK public voted in Harold Wilson's Labour government after 13 years of Conservative rule. Fast-forward to today, and a Sir Keir Starmer-led Labour looks similarly well-poised to topple the Tories after more than a dozen years on the opposition benches.

Our strategy team continually reviews global trends, and we regularly publish our latest thoughts on how key events, including upcoming elections, may affect portfolios.

These strategic insights can influence some of our investment decisions. However, our focus, as always, remains on long-term horizons, because we are confident these create the best value for our clients.

With this in mind, we will continue to serve as custodians of our clients' wealth through whatever challenges the 2024 elections may bring, just as we did through the US elections in 1824 and 1924. And we hope to be in a position to do the same in 2124 and beyond.

Ready to begin your journey with us?

Citations

[1] Protecting Democracy Online in 2024 and Beyond, Center for American Progress, 14 September 2023

[2] 2024 is the biggest election year in history, The Economist, 13 November 2023

[3] Rishi Sunak rules out a 2025 general election: ‘2024 will be an election year’, The Independent, 19 December 2023

[4] Task Force on 2020 Pre-Election Polling, American Association for Public Opinion Research, November 2022

[5] Poll of Polls, Politico, February 28 2024

[6] The 22nd Amendment was introduced in 1947 to prevent future presidents from seeking more than two terms, so FDR's record will likely stand uncontested

[7] Official Results of the 2024 Presidential Greatness Project Expert Survey, Brandon Rottinghaus and Justin S. Vaughn, 2024

[8] Obama on Obama on Climate, New York Times, 8 June 2014

[9] The quest for prosperity, The Economist, 17 March 2007

[10] The Long View: Why We Need to Transform How the World Sees Time, p 77, Richard Fisher, 2023

[11] Ibid, p68

[12] The Lindy Way of Living, New York Times, 17 June 2021

Past performance is not a guide to future performance and nothing in this blog constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.