Monthly Market Summary: September 2022

Investment Insights Team, Investment Strategist Team, Wealth Management

Investment Insights Team, Investment Strategist Team, Wealth Management

Summary: Another difficult month for stocks and bonds

In September, concerns of a global recession and monetary tightening hit capital markets hard: global equities fell 9.6%, while global government bonds declined 4.7% (both in USD terms, unhedged). Key themes included:

• The Fed and the ECB continued their tightening cycle;

• Recessions risks continued to mount in Europe;

• Rout in global currencies and UK government bond turmoil.

Stocks and bonds came under pressure once again with interest rates and the economic outlook still in focus. Concerns over the vulnerability of Europe's energy infrastructure were heightened due to a suspected sabotage of Russian gas pipelines. In commodity markets, Brent Crude futures were trading below the USD 88 per barrel level (down more than 20% this quarter) and volatile natural gas prices (UK and EU futures contracts) have more than halved from their August peak. Gold steadied around USD 1,661 (about 20% below this year’s high), weighed down by a persistently strong dollar and rising real yields.

US: Fed hikes by 75bps again; Mixed growth; Dollar strength

The Fed continued its hiking cycle, raising its main policy rate by another 75bps to the 3%-3.25% range, pushing borrowing costs to the highest since 2008. Meanwhile, even as headline inflation eased, the annual core (underlying) rate accelerated to 6.3% in August 2022. Activity was negative: The ISM Manufacturing PMI unexpectedly fell to 50.9 in September 2022, pointing to the slowest growth in factory activity since the contractions in 2020 and new orders declined 0.2% MoM in August 2022. Labour market tightness continued with initial jobless claims retreating further. The dollar index rose to a two-decade high of 114.8 (before paring some gains into month-end).

Europe: Inflation yet to peak; ECB hikes by 75bps; BoE intervenes

Annual inflation rate in the Euro Area jumped to 10% in September 2022, reaching double-digits for the first time ever. The S&P Global Flash Eurozone Composite PMI fell to 48.2 in September 2022, suggesting activity momentum continues to slow. The ECB raised interest rates by an outsized 75bps in its September 2022 meeting and suggested similar moves ahead. In currency markets, the euro briefly fell to its lowest level (against USD) in 20 years, while sterling crashed to an all-time low of 1.03 before partially rebounding. The new UK government’s unfunded spending plans forced emergency action from the Bank of England to avoid a systemic risk from emerging in the UK pensions sector. The Bank’s GBP 65bn bond-buying programme eased turmoil within the gilt market, with yields retrenching. In the Italian election, a far-right coalition led by Meloni’s arch-conservative Brothers won a decisive victory.

ROW: Chinese equities weaken; Renminbi falls; Japanese inflation

Chinese equities fell to their lowest levels in almost five months, while the renminbi temporarily fell to the lowest level since 2008 with policymakers unwilling to support the currency. The Caixin China General Manufacturing PMI fell to 48.1 in September 2022 amid the impact of COVID controls. Elsewhere, the annual inflation rate in Japan rose to 3.0% in August 2022 (highest level since September 2014) and the BoJ maintained its key short-term interest rate at -0.1% during its September meeting. The Japanese yen weakened past 144 per dollar, heading back towards its lowest levels in 24 years, but was interrupted by the central bank’s decision to intervene and support the currency.

Performance figures (as of 30/09/2022 in local currency)

| Fixed Income | Yield | MTD % | YTD % |

|---|---|---|---|

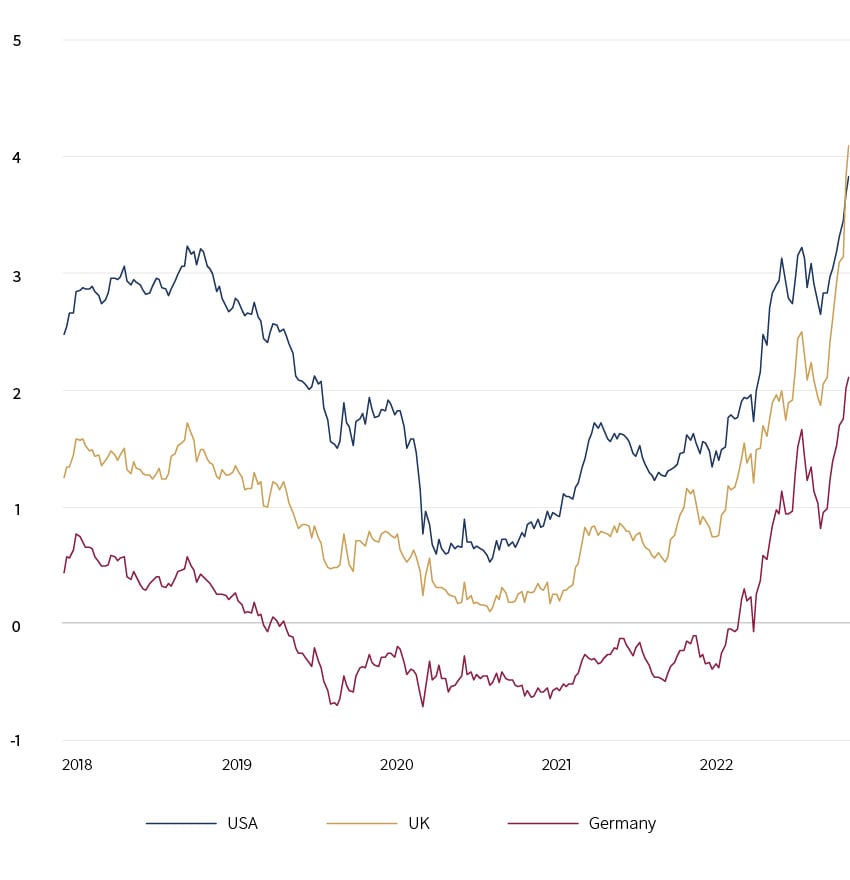

| US 10 Yr | 3.83% | -4.7% | -15.7% |

| UK 10 Yr | 4.08% | -9.7% | -20.8% |

| Swiss 10 Yr | 1.23% | -3.2% | -9.0% |

| German 10 Yr | 2.11% | -4.5% | -16.2% |

| Global IG (hdg $) | 5.38% | -4.5% | -16.7% |

| Global HY (hdg $) | 10.34% | -4.5% | -16.4% |

| Equity Index | Level | MTD % | YTD % |

|---|---|---|---|

| MSCI World($) | 289 | -9.6% | -25.6% |

| S&P 500 | 3,586 | -9.2% | -23.9% |

| MSCI UK | 12,729 | -5.0% | -1.3% |

| SMI | 10,268 | -5.3% | -18.0% |

| Eurostoxx 50 | 3,318 | -5.5% | -20.4% |

| DAX | 12,114 | -5.6% | -23.7% |

| CAC | 5,762 | -5.8% | -17.1% |

| Hang Seng | 17,223 | -13.2% | -24.0% |

| MSCI EM ($) | 443 | -11.7% | -27.2% |

| Currencies (trade-weighted) | MTD % | YTD % |

|---|---|---|

| US Dollar | 3.2% | 12.4% |

| Euro | 0.4% | -2.9% |

| Yen | -1.5% | -13.4% |

| Pound Sterling | -2.2% | -6.4% |

| Swiss Franc | 2.3% | 2.3% |

| Chinese Yuan | -0.0% | -3.3% |

| Commodities | Level | MTD % | YTD % |

|---|---|---|---|

| Gold ($/oz) | 1,661 | -2.9% | -9.2% |

| Brent ($/bl) | 88 | -8.8% | 13.0% |

| Copper ($/t) | 7,683 | -2.1% | -21.1% |

Source: Bloomberg, Rothschild & Co.

Development of 10-year bond yields (in %)

Source: Bloomberg, Rothschild & Co., 01.01.2018 – 30.09.2022

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.