The ‘K shaped’ stock market

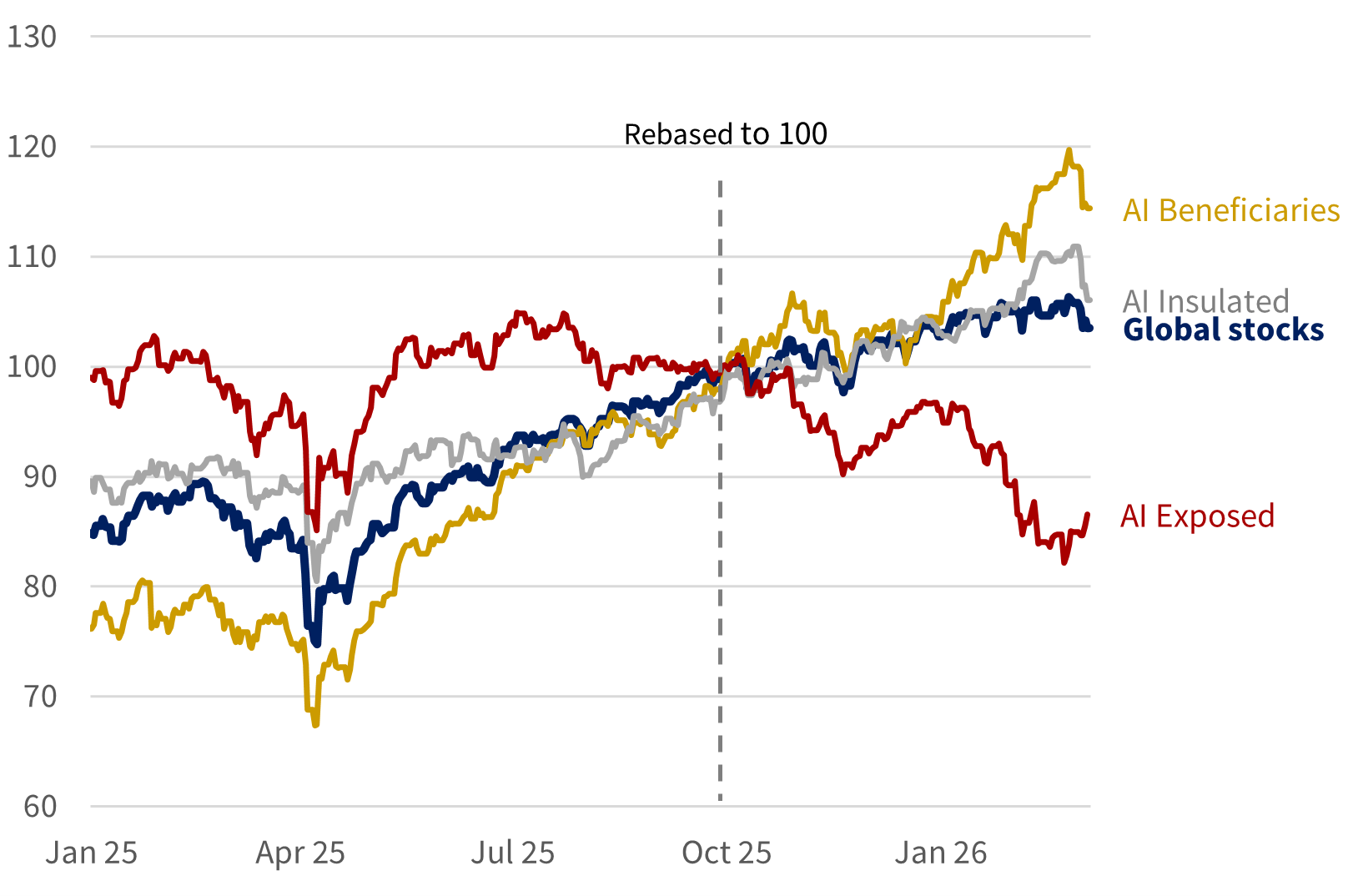

Before the market mood darkened, an unusual and potentially significant story had been emerging in recent months. Within the global stock market index - which (for now) is still showing year-to-date gains - lies a fiercely bifurcated market, with AI hopes and fears driving an unusually big wedge between winners and losers. Losers for a change include US stocks – to February – which had underperformed non-US stocks by 14% since the start of October.

Beneath the surface, the software sector had been hit particularly hard - somewhat ironically, by fears of dramatic AI-driven disruption. If the hype is to be believed, many companies there are going out of business. It wasn’t long ago that people were fretting about asset bubbles, yet now we’re talking about the sector imploding as open-source, AI-compiled coding replaces tailor-made enterprise software. Alongside this, the so-called hyperscalers – which include many of the ‘Magnificent Seven’ names – have also been under pressure in recent months, even as global technology stocks (outside of the US) have marched higher.

Selected global stock returns

Total return in USD (100 = 1st Oct 2025) │1st January 2025 to 5th March 2026

Source: Rothschild & Co, Bloomberg. Footnote: AI baskets based on qualitative assessment of selected MSCI ACWI sub-sectors and industry groups. ‘AI Beneficiaries’ include Capital Goods, Semiconductors and Utilities; ‘AI Insulated’ include Autos & Components, Staples (Food, Beverage & Tobacco), Pharmaceuticals, and REITS; ‘AI Exposed’ includes Media, Diversified Financials and Software & Services. Baskets have been equal-weighted and calculated in USD terms.

Some of those trends have paused in recent days, but there remains a big divide between the different cohorts. At the more excited end are the immediate AI-beneficiaries (so-called ‘enablers’) – the businesses involved in the AI infrastructure rollout, which have performed best (and which partly explains why Asia was – until the weekend – having its best start to the year in over three decades). Towards the middle are a cohort of ‘old economy’ and defensive sectors which may be either benefitting and/or insulated from perceived AI competition (and sometimes referred to as ‘HALO’- Heavy Asset, Low Obsolescence). And at the more uncomfortable end, the knowledge and data-based industries seem to be facing a bigger reckoning. The once revered – and now enfeebled – US software sector, including such esteemed names as Microsoft and Salesforce – is still down just under a fifth this year.

The trigger for the indiscriminate – at times dramatic – price falls have been off-the-beaten-path research reports and ad hoc comments from business leaders. Where businesses are perceived to be at risk of disintermediation, share prices have been condemned – the investment narrative is ‘guilty until proven innocent’.

On closer inspection, other supposedly AI-exposed companies have also been hit hard, including media companies, insurers, wealth managers and even private market asset managers – all caught by their reliance on proprietary software and credit (also, many of the smaller software names have been using borrowed money, private credit markets have also suffered in the fallout).

AI will doubtless continue to improve and surely will indeed disrupt many businesses. But it is too soon to say which, and in the meantime the market is vacillating from AI boom to AI doom – attempting to discount imminent creative destruction – before we have seen a change in the operating environment.

Just because every man and his dog can vibe code doesn’t mean that software companies are going out of business. Software is not just about code – but about interoperability, security, and reliability (BSOD anyone?). Elsewhere, wealth managers, for example, arguably add value with holistic advice, judgement, and ongoing engagement, not just data-processing. Selecting long-term investments is less about big data than about providing perspectives and context – which are not algorithmic reasoning’s strongest suits.

There is little doubt that AI developments are moving fast: dramatic and impressive refinements in the foundational Large Language Models, the launch of more sophisticated agentic AI, and the staggering levels of investment that underpin the datacentre rollout. But even here, as noted, the big hyperscalers – are facing greater scrutiny of their rising capital expenditures (and diminishing free cash flows). This is arguably a healthy development keeping those (previous) equity market bubble ‘melt-up’ fears at bay.

Our general advice, faced with such polarised views, is usually to avoid getting swept up by the latest big “new paradigm”, whether it is imminent salvation or the end of times. AI could prove wildly (and widely) transformative, but only if consumers and businesses embrace it – and if their pressing problems are computable to begin with. Meanwhile, a small silver lining to these recent lopsided returns is that some important valuations are perhaps looking a little less egregious than they once were. Remarkably, the global technology sector now trades at a discount to the industrial sector.

For now, however, those AI trends and valuation considerations are being overshadowed by rather more pressing geopolitical concerns. US stocks – and some of those ‘AI-exposed’ segments - have emerged as the ‘safe haven’ of choice through this volatility. It remains to be seen if that revival persists.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.