Fed independence: Q&A

Despite constant browbeating from President Trump, the US Federal Reserve’s (Fed) independence remained intact through 2025. Fallouts between US Presidents and Fed Chairs are not that uncommon – a famous example was the rumoured physical encounter between Lyndon Johnson and Bill Martin in 1965 – but the latest jab from Trump was arguably the most threatening we’ve seen in recent times.

Last week, the US Department of Justice opened a criminal investigation into the Chair of the Fed, Jerome Powell, related to over-spending on the institution’s building renovations (it is unclear if the move was actually directed by Trump). The response – by central banking standards – was spectacular. Powell issued a video statement, implying that the action was politically charged; all (living) former Fed Chairs published a joint rebuke, likening the situation to “emerging markets with weak institutions”; and lawmakers, including some Republicans, expressed their discontent with the move.

Perhaps surprisingly, the reaction from financial markets was muted again (perhaps because, as noted, this wasn’t the first time that the Fed’s independence has been challenged by the new administration). Nonetheless, it prompts a few questions.

Why does Trump want lower interest rates, and what are the macro risks?

Probably to boost his popularity: low interest rates are generally a ‘good thing’ – especially for voters struggling with mortgages or other debts – and the US midterm elections are looming, with the Republicans currently projected to lose their ‘red wave’ in Congress. Note that rates have been falling anyway, probably not because of Trump’s browbeating but because the Fed independently thinks they should do.

If rates are cut further just to win votes, any near-term boost to popularity and economic activity could eventually be followed longer term by inflation and a loss of monetary credibility (ultimately pushing borrowing costs higher, not lower, and undermining the currency). Such things do happen – see Turkey as a real-life example.

Can Trump exert significant control over the Fed?

The lack of a market response to date may partly reflect the practical and legal complexities which surround the governance of the Fed.

Criminal investigations aside, Powell’s term as Fed Chair is set to end in May, and it is indeed the President’s job to nominate his successor, with the candidate thereafter ratified by the US Senate. A Trump-loyalist Chair is a real possibility, and Kevin Hassett, currently Director of the National Economic Council, appears to be a politically-aligned frontrunner.

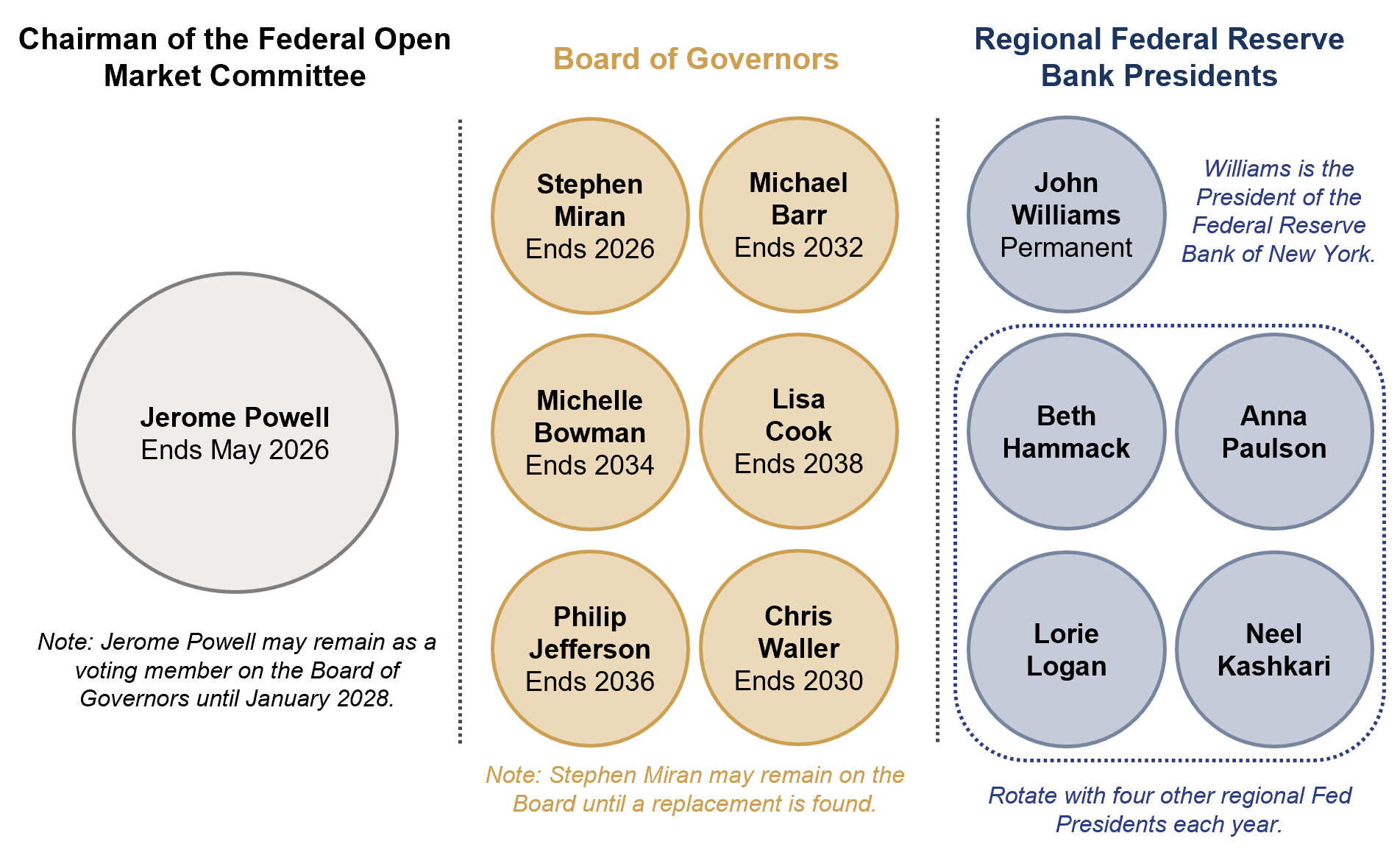

That said, in light of recent developments, the Senate Banking Committee have suggested they are now wary of approving candidates who have a history with the President. And interest rates are not selected by the Fed Chair alone: the main interest rate is determined by twelve Federal Open Market Committee (FOMC) members – the Fed Chair, six Board of Governors, and five regional Fed Presidents – in a majority vote, and so a politically-oriented Chair may not necessarily have a determining influence on the trajectory of US interest rates anyway (figure 1). Note that Powell can also technically remain on the Board of Governors until 2028 and may be encouraged to do so after recent events (so long as the criminal ruling does not go against him).

Figure 1: 2026 Federal Open Market Committee (FOMC)

Source: Rothschild & Co

But can Trump influence the other two segments of the FOMC?

Firstly, as with the Chair, it is the US President who nominates a new Board of Governor when their term ends. However, as figure 1 shows, most of the Board of Governors have tenures that exceed Trump’s presidential term, and so again his influence may be limited – unless those Governors voluntarily resign. That can happen, and last year a pro-Trump nominee took a vacant seat. In this case, the vote is just one of the remaining eleven, and not necessarily any more decisive (the new governor, Stephen Miran, has only temporary tenure on the committee). Of course, some of the existing FOMC Governors were nominated by Trump during his first term – including Powell to the Chair position – but they seem to have conducted monetary policy without perceived political bias.

Given the Governors’ long terms, the administration could attempt more forceful removal. This is technically possible: the Federal Reserve Act of 1913, which established the institution, states that a member of the board can be removed “for cause”. One of the Board of Governors, Lisa Cook, is currently being investigated on this count, but the case has now dragged on for several months and she has continued to serve on the FOMC in the meantime. There is ambiguity around what can be deemed “for cause”, with little established precedent.

Secondly, the regional Fed Presidents appear more insulated from government. For context, there are twelve in total, only five of which vote each year (the New York seat is permanent; the other four spots rotate annually). These Presidents are appointed internally, subject to approval from the Board of Governors, so any hiring decisions are fully separated from government (so long as the main Fed Board is not full of pro-Trump candidates of course). The US Treasury Secretary, Scott Bessent, recently suggested that a three-year residency rule may be introduced for regional Fed Presidents, but it is difficult to see how this potential legislation could prevent them from acting independently. Bessent himself even previously said that Fed independence is a “jewel box that has got to be preserved”.

A wildcard scenario is that Trump asks Congress to change segments of the Federal Reserve Act to make executive firing easier, or worse, suggests that they try to abolish the Fed. However, the probability of these scenarios occurring seems extremely low: there will likely be very little appetite from lawmakers – including Republicans, as demonstrated by an abolishment bill last year that gained no traction – and there is not much time to do so given the midterms are in November.

Do these developments matter for markets?

As noted, the Fed was established in 1913 through the Federal Reserve Act, as a guardian of financial stability following a wave of bank runs and failures several years prior. However, it arguably only became independent in 1951, after the Treasury-Fed Accord was signed. The Accord essentially allowed the Fed to run monetary policy without government approval: in the decade prior, the Fed was forced to keep government borrowing costs low to finance the US’s war efforts, though at the expense of double-digit inflation (remarkably, the Treasury Secretary was even on the Fed Board until 1935).

Today, if the Fed were to somehow lose its post-war independence in setting interest rates, then the likely financial market reaction would be tumultuous. That’s because the Fed is the most important central bank for global capital markets, and the US currency is the biggest reserve asset. The Fed’s main interest rate – and expectations around how it may evolve – is arguably the main driver of US treasury yields (which investors perceive to be the world’s ‘risk-free rate’) and the US dollar (the world’s ‘reserve currency’). A loss of US monetary credibility would undoubtedly have huge knock-on effects across financial markets.

We will be watching legal developments closely. If Powell or Cook’s case goes in Trump’s favour, then market volatility might increase, as the chances of a politically-tilted FOMC might rise (though, as noted, perhaps not that far).

And we have seen that the threat of such volatility may matter to Mr. Trump: market volatility, not economic logic, was arguably what caused him to backtrack from his initial ‘Liberation Day’ tariff proposals in April 2025.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.