2025: a year of resilience

It was a tumultuous year: protectionism, conflict, political dysfunction, bank jitters, and even asset bubble concerns. Despite such visible challenges, the global economy remained remarkably resilient through 2025. Growth continued, interest rates fell and some of the simmering geopolitical threats perhaps faded as we progressed through the year.

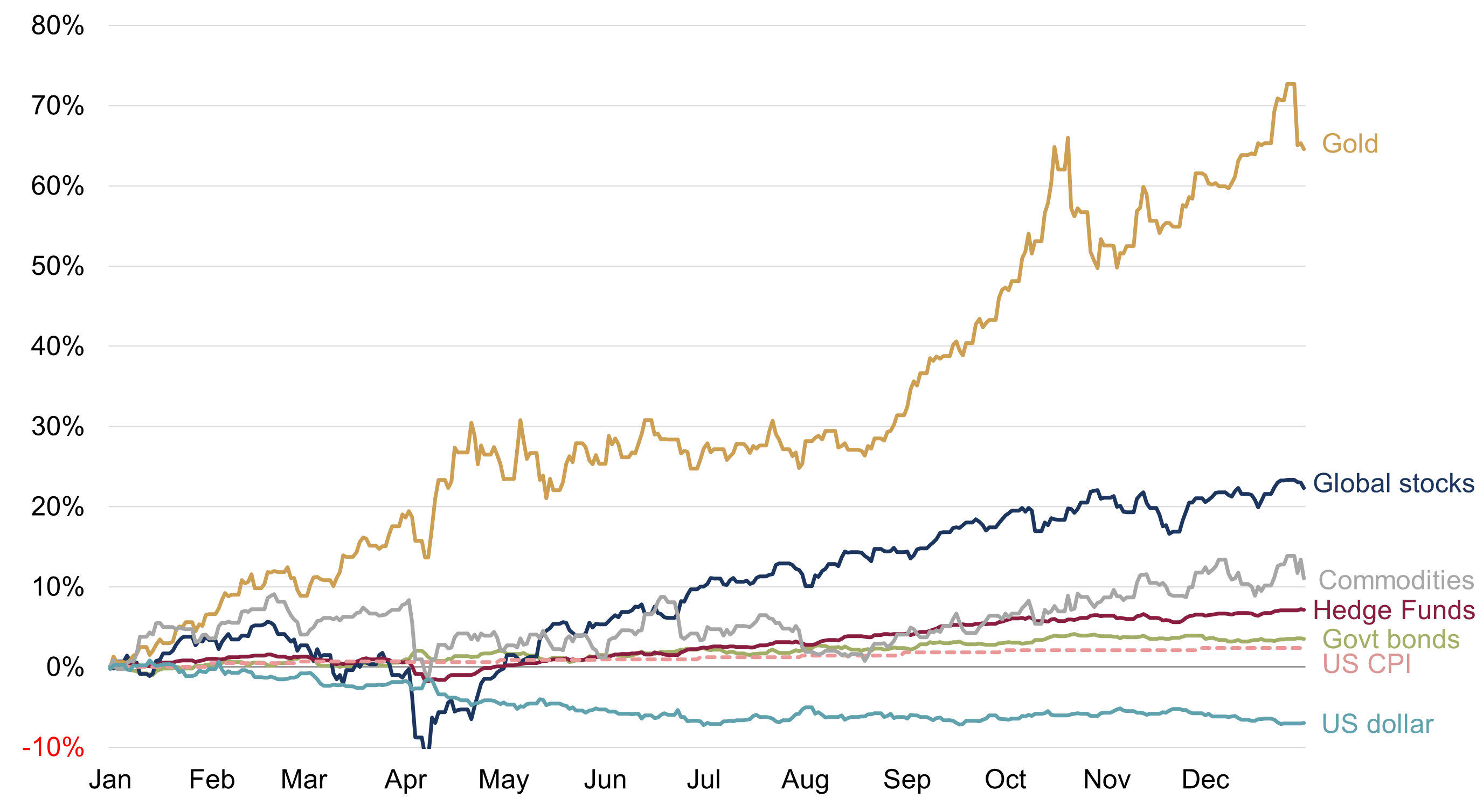

Such resilience was supportive of capital markets, in what was generally a positive year for most asset classes (figure 1). Here we unpack 2025’s five major market developments and their drivers.

Figure 1: Selected asset class returns in 2025

US dollar terms (%)

Source: Rothschild & Co, Bloomberg, MSCI, Citi, HFR

1. Trump 2.0 and the dollar

A year ago, US stocks and the dollar were flying high.

Mr. Market had confidently asserted that the second Trump administration would deliver a pro-business policy stance. Those animal spirits quickly faded, however, as economically-troubling proposals within the ‘Make America Great Again’ agenda – most notably the dreaded ‘T-word’ (you guessed it, tariffs) – moved centre stage. The US-led market setback culminated in early April, following Trump’s so-called tariff ‘Liberation Day’.

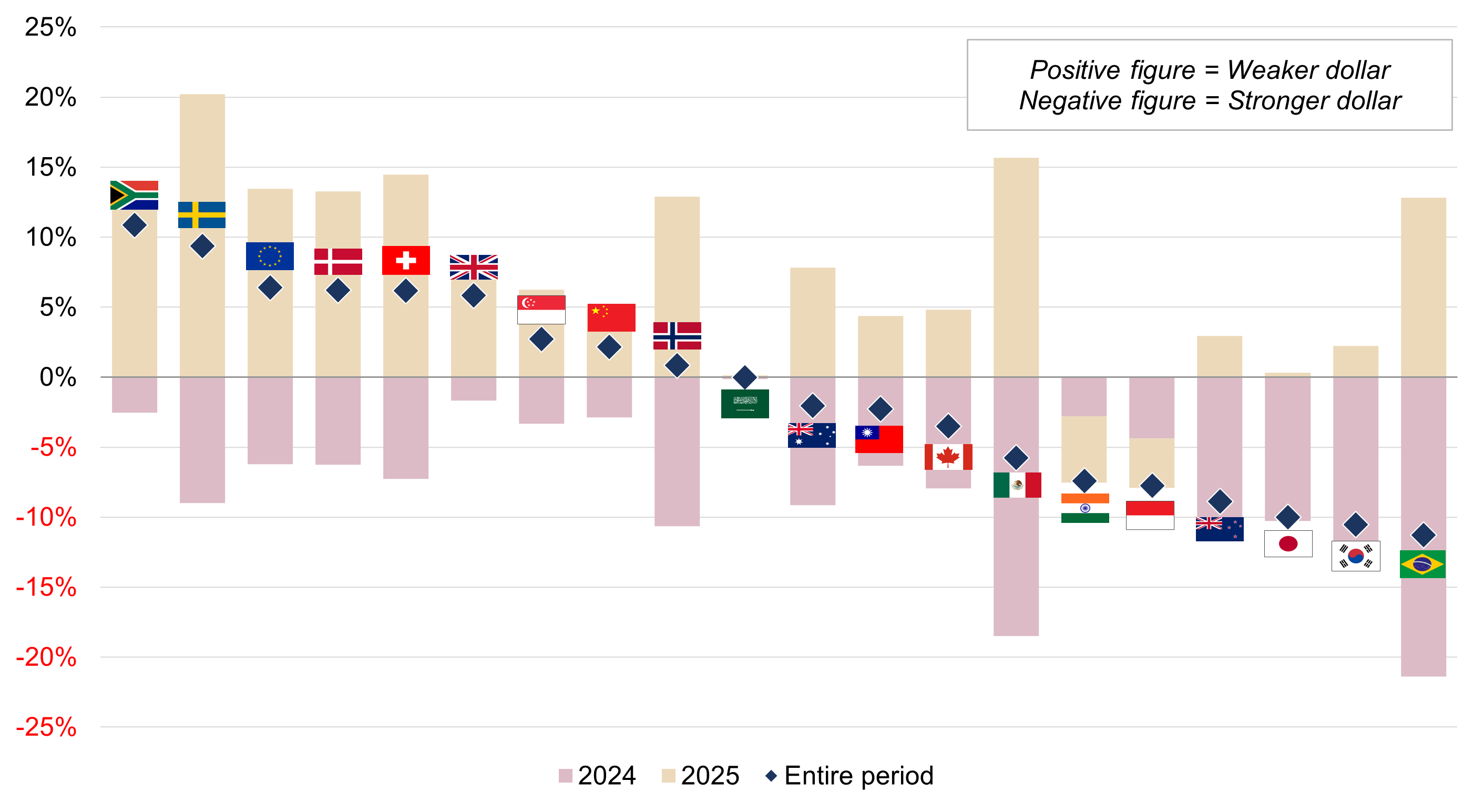

Fortunately, the US President moderated his proposed duties, perhaps mindful of his approval ratings, after which the US stock market quickly rebounded (more on this later). In contrast, the US dollar continued its descent until the middle of the year before stabilising: overall it was down by 7% on a broad, nominal trade-weighted basis in 2025 (that is, comparing its value with a range of other currencies). Its decline was more pronounced against some of the major currencies, including the pound sterling (-8%), euro (-13%) and Swiss franc (-14%).

However, while currency volatility was higher than usual, the greenback’s decline was not that striking. The US nominal effective exchange rate fell by a similar magnitude during the first year of Trump 1.0 in 2017. What’s more, the dollar had appreciated greatly in 2024, meaning, on a two-year view, its moves against most currencies look less remarkable, albeit mixed (figure 2). The pound, euro and Swiss franc have admittedly still strengthened against the dollar by ~6% during this window, but this sort of volatility is still small when set alongside routine stock market volatility, for example (which is usually the case over longer time periods anyway).

FX markets are highly ‘efficient’, meaning that all available public information is already ‘priced-in’, and accurately predicting the direction of the US dollar is difficult at the best of times. That said, we continue to think that talk of the dollar’s strategic demise is overstated, just as it was at the start of Trump’s first term (more on this here). In fact, the dollar then went on to rally vigorously in the following couple of years of his first term...

Figure 2: Spot currency returns

Relative to the US dollar (%)

Source: Rothschild & Co, Bloomberg

2. Stocks: a vintage year for some

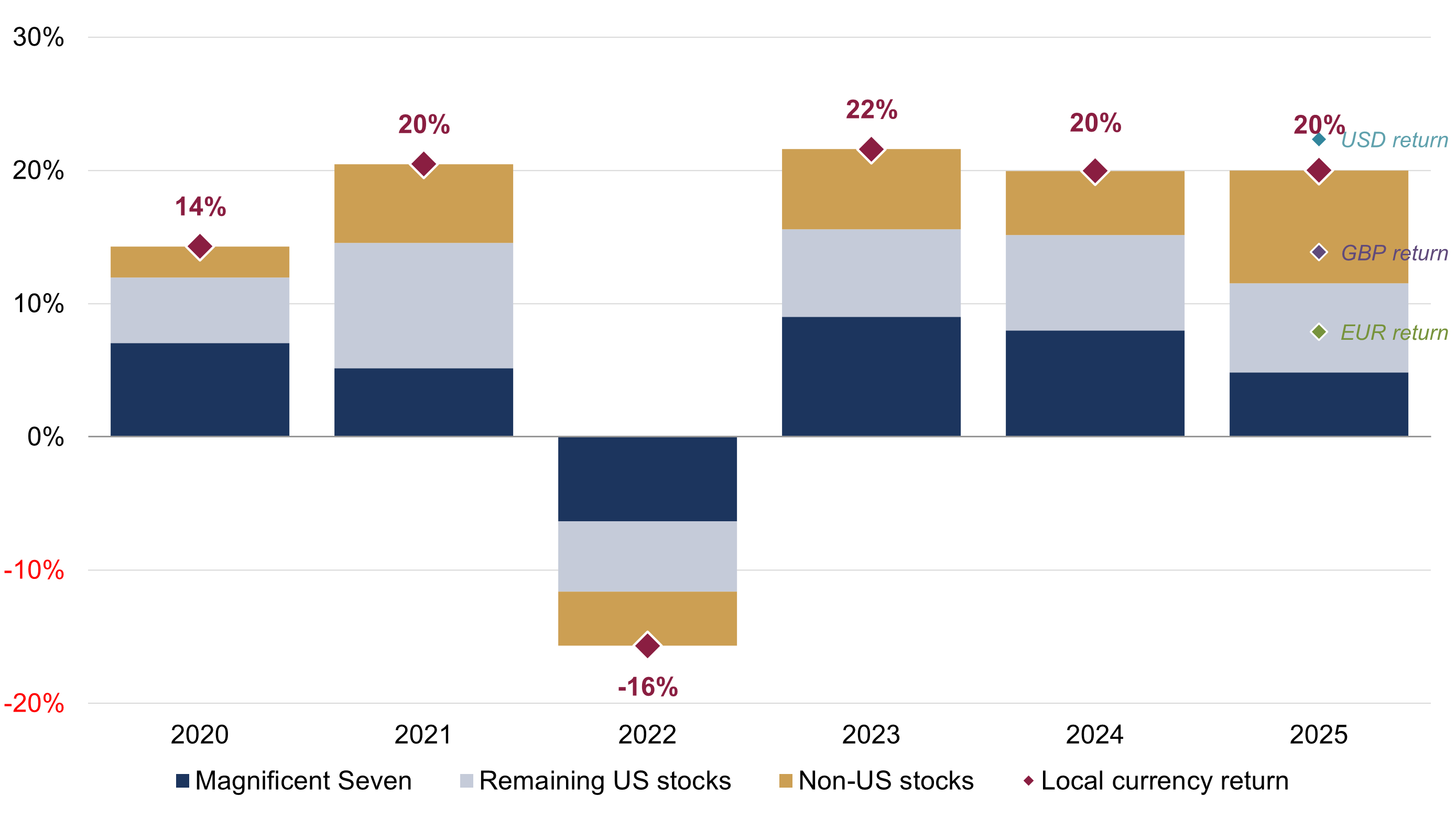

Despite initial technology (DeepSeek in January) and tariff-related jitters (in April), market nerves quickly morphed into a vigorous rally and new highs. 2025 ended up being something of a vintage year for stocks – a third year of double digit returns at the global level in dollar terms. There have only been a handful of episodes in the past half century where we have seen a similar (or better) rolling three-year return (~20% per annum). It hasn’t been entirely plain sailing: an unusually weak dollar (as noted above) has amplified or depressed those global equity returns depending on your base currency.

AI-driven momentum has once again been a prominent theme – particularly in the aftermath of April’s ‘Liberation Day’ turmoil – but it has been far more fragmented and volatile than in previous years. The ‘Magnificent Seven’1 moniker has become a little passé: five of this highly disparate cohort have failed to outpace the wider market in 2025. Collectively these juggernauts now account for a fifth of the global equity market (close to all-time highs), yet their contribution to overall returns is the smallest in recent memory (figure 3).

To some extent, this reflects a broadening of the AI story beyond the US’s largest companies to a wider AI ecosystem, including global semiconductor players, as well as industrial and energy companies across the US and Asia. But 2025 has also been a year in which many previous trends been put on hold: global value and equal-weighted indices have matched or very modestly outpaced their growth and market capitalisation weighted counterparts. The prize for the best performing industry group in 2025 goes to the banks (though semiconductors were only marginally behind).

Perhaps the most notable development is that underperformance of the mighty US stock market, which had been mostly leading the market higher until recently. The demise of US exceptionalism may be overstated, but as this year has demonstrated, the US and its technology titans are not the only game in town.

Figure 3: Contribution to annual global stock returns

Local currency terms (%)

Source: Rothschild & Co, Bloomberg, MSCI

3. Bonds and budgets

Concerns around fiscal discipline – and talk of ‘bond vigilantes’ looking to punish reckless governments – persisted on both sides of the Atlantic in 2025.

In the US, Elon Musk’s Department of Government Efficiency (DOGE), as expected, failed to rein-in government spending and debt. Instead, the Trump administration passed the ‘big, beautiful’ bill which is set to result in even more borrowing than would otherwise have been the case in the years ahead (which may become even more bloated, if the President’s mooted ‘tariff dividends’ – cheques for households – become reality). In Europe, the UK’s recent ‘austerity’ budget will in fact deliver modest fiscal loosening in its early years, before an eventual (and modest) tightening around 2029. France delayed its pension reform to prevent another government collapse, and Germany is about to embark on a huge spending splurge.

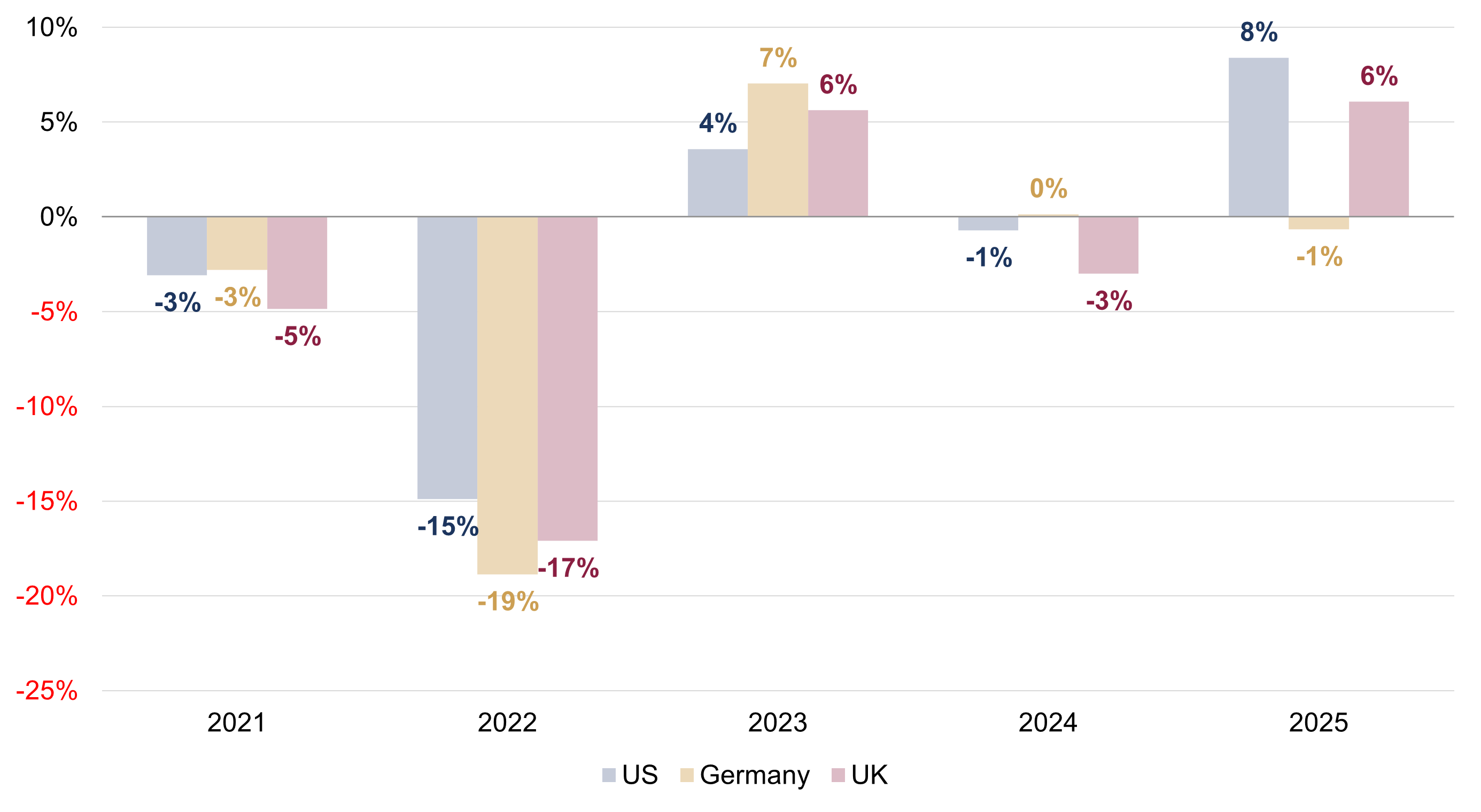

Yet, despite these fiscal concerns, most government bonds registered solid returns in 2025 (figure 4). US 10-year government bond returns were the strongest since 2020, with yields falling across most segments of the curve. Even in the much-maligned UK – where interests rates and inflation are the highest in the G7 – 10-year gilts delivered their best return since 2016. However, German bunds – where yields have been moving higher after announcing its planned stimulus – delivered a negative return.

Often, it is the business cycle, not the amount of borrowing, that tends to matter most to bond prices. The huge markdowns registered by government bonds in 2022 – on a scale not seen for decades – were mostly due to the sharp ‘normalisation’ of interest rates, amid a surge in inflation. And 2025’s positive returns for US and UK government bonds coincided with rate cuts from their respective central banks and a shift lower in market-implied rate trajectories (relative to the start of the year), as policymakers bet that inflation risk had subsided (with bonds’ more supportive valuations after that earlier normalisation of yields doubtless offering some support too).

Looking ahead, we feel that inflation may remain sticky and growth intact, which may limit returns from government bonds.

Figure 4: Government bond returns by calendar year

7-10 year bond index (local currency, %)

Source: Rothschild & Co, Bloomberg

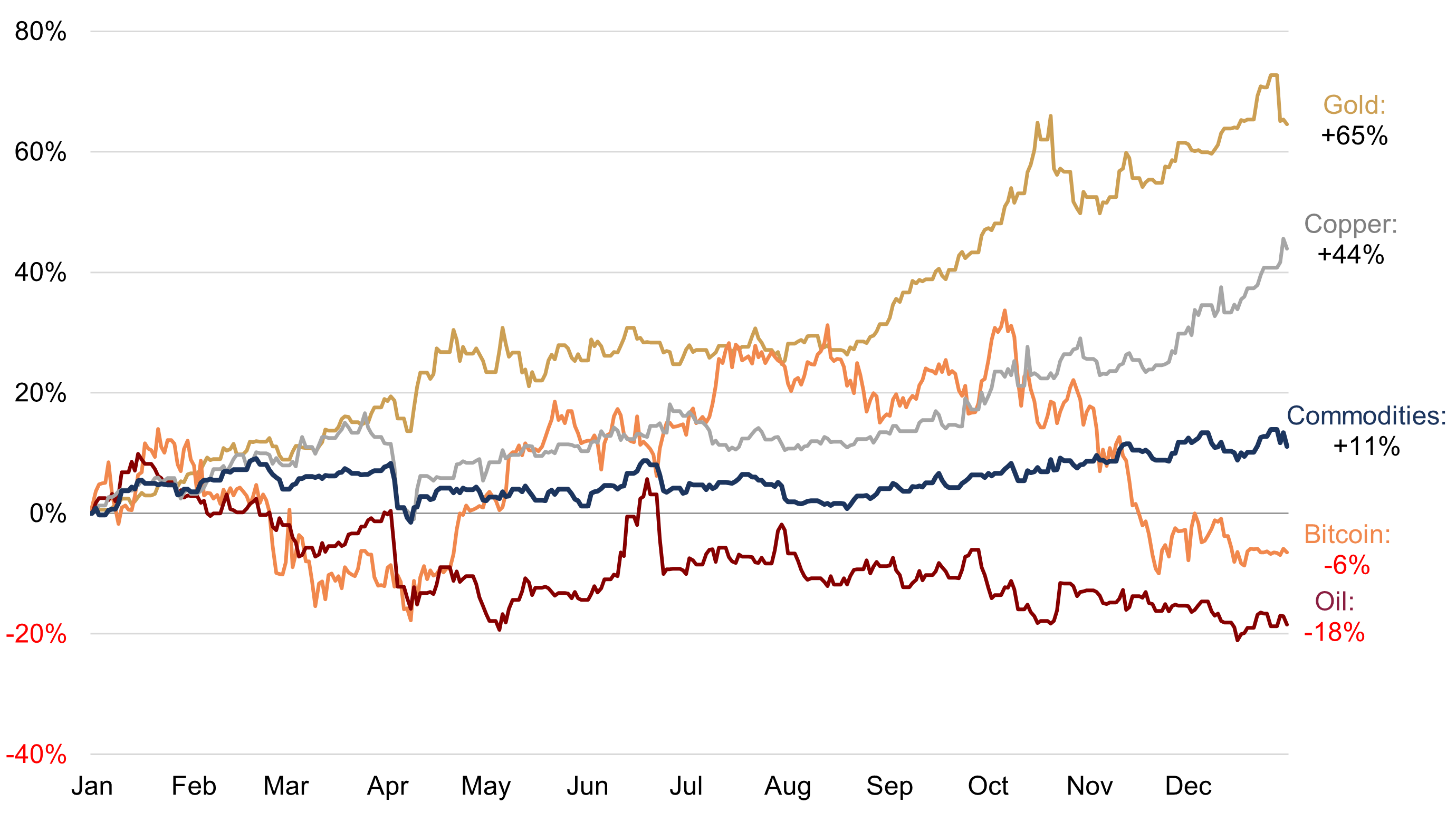

4. Commodities, crypto and the gold rush

Commodity prices are erratic at the best of times, and the relatively pedestrian ~11% index return belies what has been an unusually lumpy year. Wholesale energy prices, including oil and natural gas, have fallen sharply, while some industrial metals, including the electrically-relevant copper, have moved to fresh highs (figure 5). Both developments seem to be related to supply-side considerations rather than a big change in demand for such inputs.

At the more extreme-end, gold has had a stellar 2025. The shiny metal has surged by two thirds over the past year – outperforming every other major asset class – with the spot price (~$4300/oz at year-end) more than doubling since the start of 2024. And it’s not just gold: the whole precious metal universe has moved to new highs – including silver and platinum (alongside the mining stocks, which have benefitted handsomely).

There are no shortage of possible explanations for gold’s surge: geopolitical turbulence, the weaker dollar, central bank buying, or perhaps just ‘FOMO’. Interestingly, gold has lost touch with its traditional drivers in recent years: the spot price’s rise has coincided with rising ‘real’ yields and risk assets since the start of 2024.

Meanwhile, another purported ‘debasement hedge’, Bitcoin, has fallen almost a third from October’s all-time high – with many other so-called ‘alt-coins’ down considerably more. The onset of another crypto winter (the last such episode being 2022 following the cascade of failures, including the collapse of Terra and FTX) reminds us that Bitcoin is a speculative risk asset, and highly correlated with stock prices (particularly US technology stock prices). It is not a hedge against inflation, monetary disorder, and certainly not a risk asset diversifier.

Figure 5: Spot commodity and cryptocurrency returns in 2025

US dollar terms (%)

Source: Rothschild & Co, Bloomberg

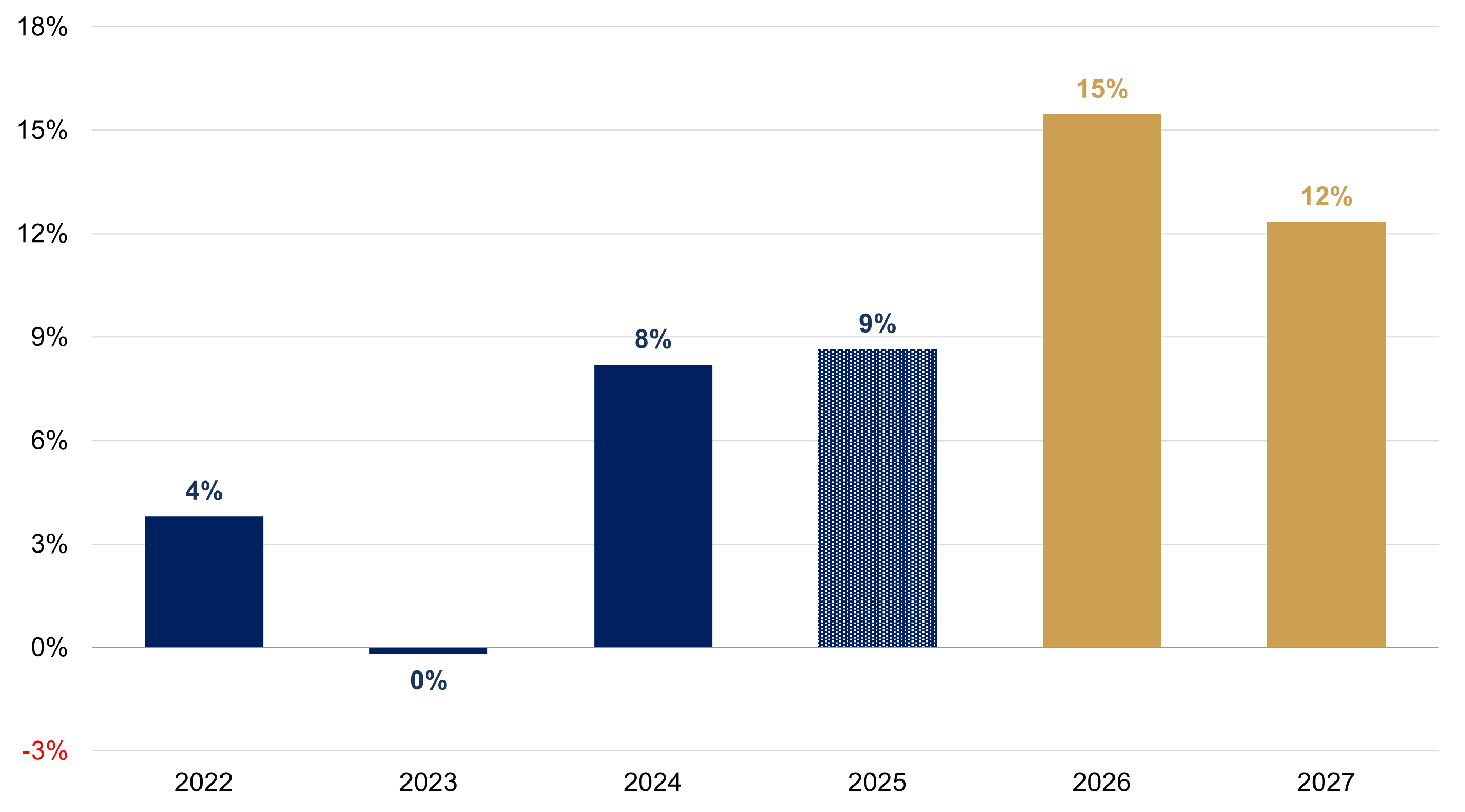

5. Fundamentals still matter

We started 2025 feeling that equity valuations were expensive, and that the positive consensus on AI and Trump’s reflationary policies were running ahead of reality.

Twelve months on, those valuations are even more expensive: the global equity forward price-to-earnings multiple has re-rated from 18x to 19x today – the lofty US market is at 22x. Yet the bulk of this year’s total return is underpinned by robust earnings growth, with calendar year EPS on track to expand by a tenth in 2025 (similar to 2024’s outturn). Behind the scenes, a strong supporting role has been played by healthy margins: aggregate net income margins have risen from 11.5% to 12.5%, their highest levels on record.

Expectations for 2026 and 2027 are even more upbeat, with recent upward revisions pushing expected EPS growth to 15% and 12%, respectively (figure 6). Importantly, after many years where rising US – and technology-related – profitability has been in the driving seat, earnings growth is expected to broaden to other sectors and regions.

Looking ahead, we don’t know whether today’s AI growing pains will persist, but the possibility of a prolonged consolidation feels higher after such a run. However, if those earnings can continue to grow – and broaden – in the way that analysts’ expectations suggest, there may yet be headroom for the market, and for a further rotation away from the previous market leaders.

Figure 6: MSCI All Country World Index annual earnings growth

Actual and estimated (US dollar terms, %)

Source: Rothschild & Co, Bloomberg, MSCI

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Footnote

[1] ‘Magnificent Seven’ refers to Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

Figure 1: ‘Global stocks’ are the MSCI All Country World Index (net total returns); ‘Commodities’ are the Bloomberg Commodity Index; ‘Hedge Funds’ are the HFRX Global Hedge Fund Index; ‘Government bonds’ are the Bloomberg Global Aggregate Treasuries Index (USD, hedged terms); ‘US dollar’ is the Citi US Dollar Broad Nominal Effective Exchange Rate.

Figure 3: Global stock contributions are derived from an MSCI All Country World Index ETF, so figures may differ slightly from the actual index return.

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.