Five Macro Myths

1. AI alone is driving US growth

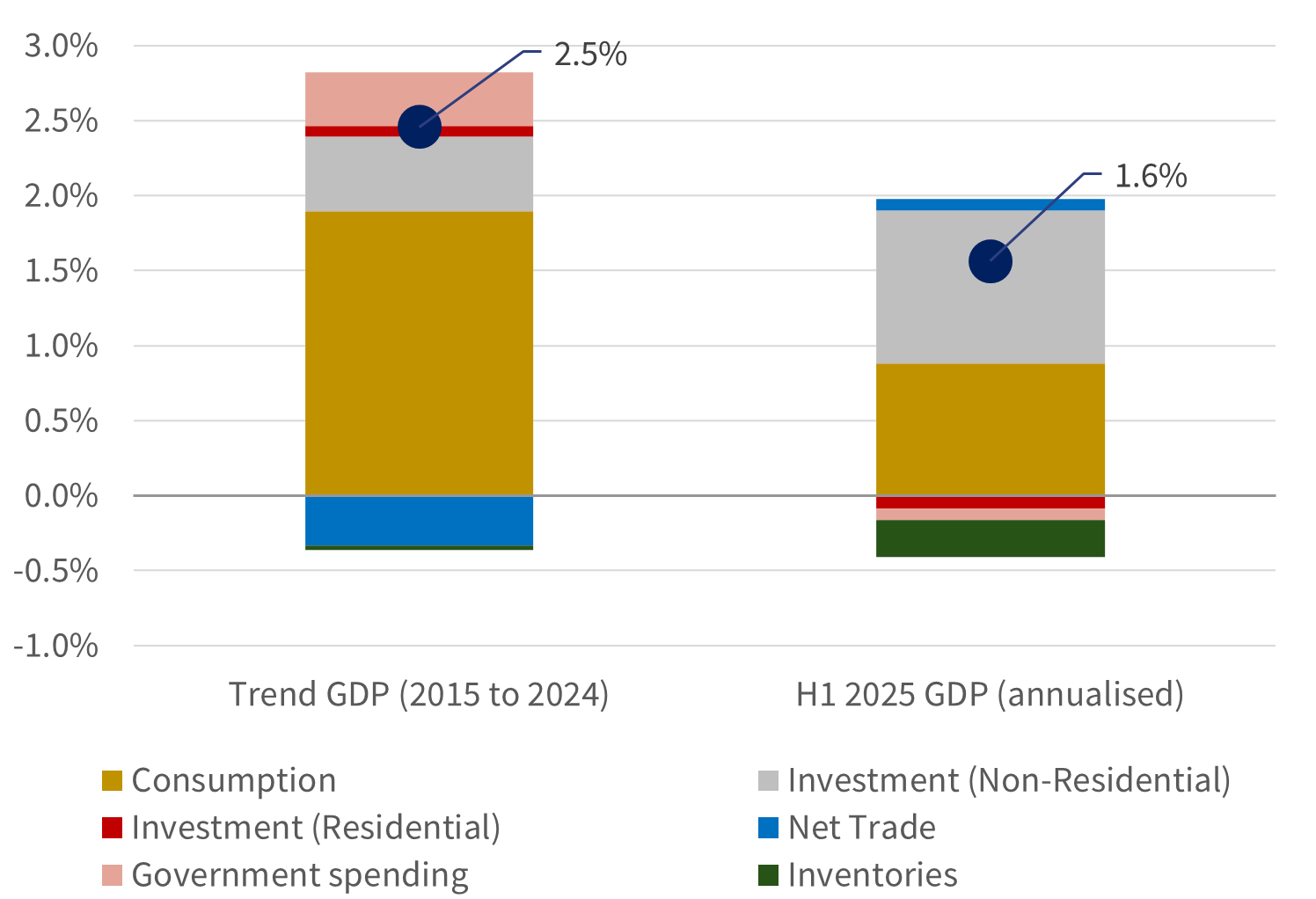

The hyperscalers1 – and the wider AI ecosystem - have been steadily ramping up their spending plans: capital outlays have doubled over the past two years, with little sign of this abating. This AI spending is already having a material economic impact: capital expenditure – measured by non-residential investment – accounted for nearly half of US GDP growth in the first half of 2025.

US Real GDP: expenditure components

Source: Rothschild & Co, Bloomberg, BEA

Though the headline contribution sounds big, this overstates AI’s impact. Parsing the numbers reveals that capital expenditure is evenly split between: i) equipment (computers and peripherals); and ii) software. Some of the equipment spending reflects domestic industrial production and construction, but most of it reflects chip fabrication, which currently occurs outside of the US (in Taiwan or South Korea). The import drag ultimately mutes the economic gains from those outlays.

In addition, the H1 contribution from investment was amplified by weak consumption growth (which expanded by a meagre ~1% vs ~4% between 2023-2024). The more recent rebound in consumer spending suggests this may have been a temporary aberration.

The point is that even today there are many moving parts shaping the US growth story, and while the scale of the unwavering AI investment boom is immense, many of those pending AI dollars won’t directly benefit US output (equally their absence may not be as keenly felt either).

That said, beyond the direct spending, perhaps of greater significance is the potential and promise of economy-wide productivity gains – if they show up: to paraphrase Robert Solow, you can see AI everywhere but in the productivity statistics.

2. AI is leading to widespread layoffs

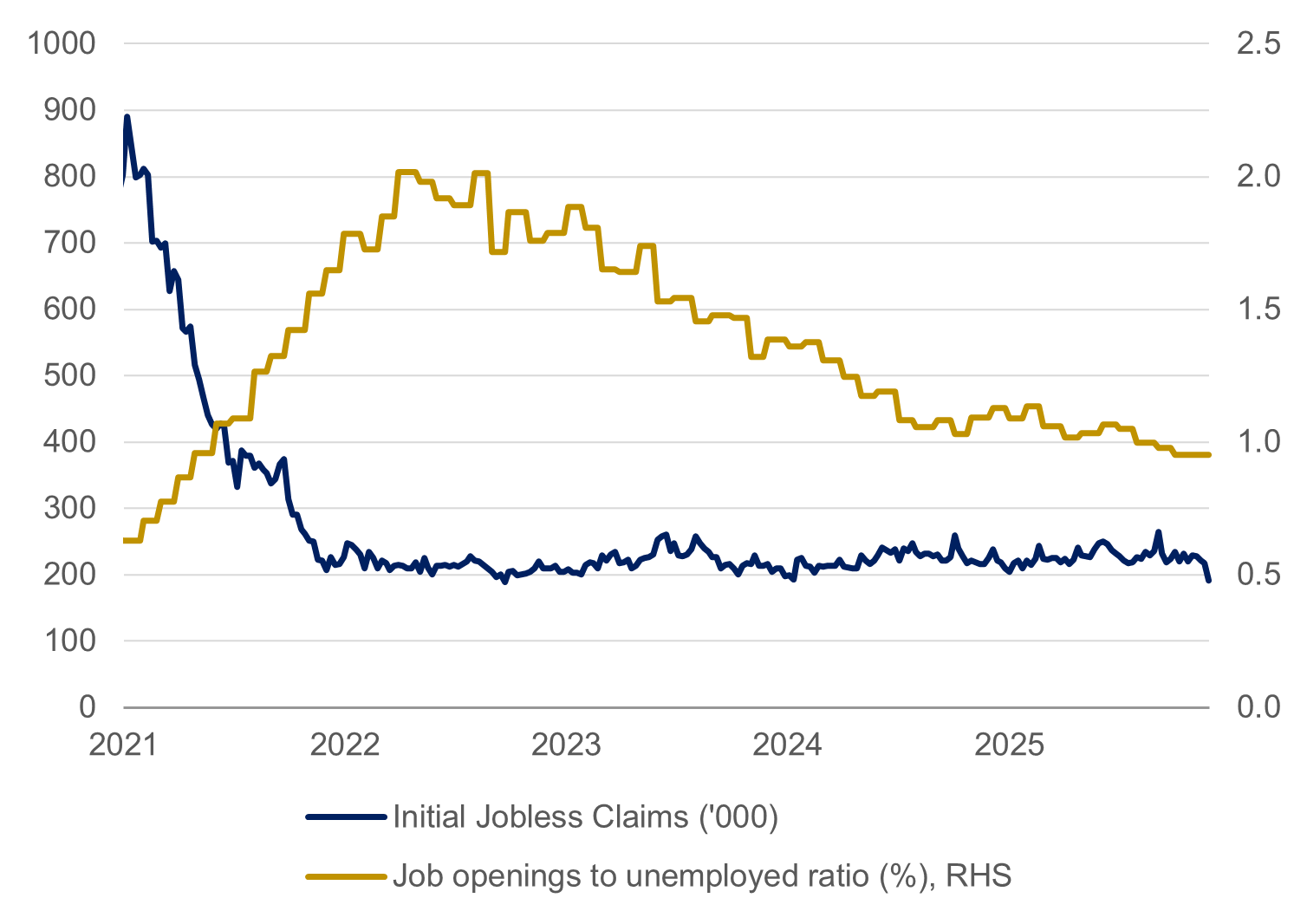

The health of the US labour market has been the source of much consternation and frustration for economists this year. The pace of job gains has slowed dramatically, and unemployment has risen, particularly for younger segments (20-24 year old unemployment has risen from ~5% to ~9% over the past two years). Meanwhile, layoffs are reportedly rising, with white collar jobs supposedly most threatened (according to recent Challenger jobs reports).

But to blame this solely on AI may be premature. US policies, including tariffs and deportations, have had an unusually big influence on the macro story in 2025: the pattern of spending, and both the supply of and demand for labour, have been disrupted.

Meanwhile, there have been longer-term trends at play. The post-pandemic hiring boom was well above pre-COVID norms – it wasn’t long ago that labour scarcity was a corporate concern (labour hoarding, anyone?). This suggests that some of this year’s hiring slowdown reflects the cyclically elevated starting point, as well as those ongoing policy-related disruptions.

AI is surely amplifying a sense of unease – and there are indeed some prominent businesses citing AI as a reason for cutting jobs. But while some of this might be genuine AI disruption, some of it might also reflect “managerial cowardice” (as one prominent report notes). AI displacement sounds more commercially compelling, than more routine cost cutting and restructuring.

For AI to be a macroeconomically disruptive force, organizations need to wholeheartedly and comprehensively adopt it. This is not yet happening: AI curiosity and experimentation is the name of the game currently, and this is unlikely to deliver mass unemployment. As noted, the jury is still out on eventual widespread adoption.

More prosaically, the very delayed September US jobs report suggests job gains have re-accelerated after the summer lull, while jobless claims – one way of quantifying layoffs – are moving lower, not higher.

US labour market: less hiring, but not much firing?

Source: Rothschild & Co, Bloomberg, BLS

3. Trump’s fading popularity doesn’t matter

There has rarely been a more fitting political metaphor than the destruction of the East Wing of the Oval Office and Trump’s aggressive policy agenda.

That agenda includes running roughshod over Federal law and constitutional convention, alienating allies, and coarsening an already politically charged social debate. However, set against these more uncomfortable and unorthodox policies, Trump has also managed to pass a sizeable US stimulus package, reduced tensions in the Middle East, and parts of his (to us misguided) industrial policy may slowly be taking a more constructive shape. His methods – or politics – are not to everyone’s taste, especially here in Europe, but he should at least be commended for his energy.

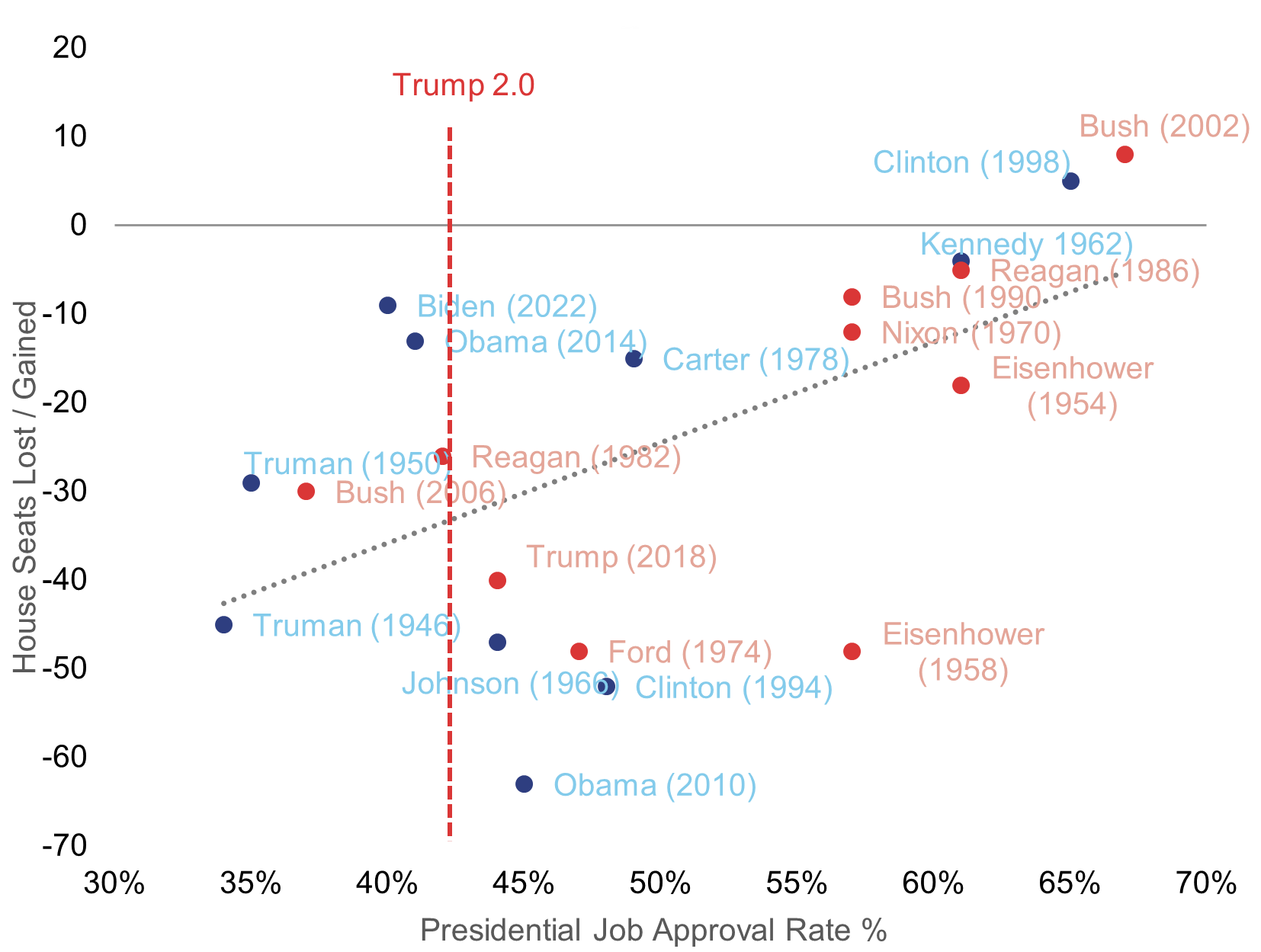

But now nearly a year into the job, it seems this policy of moving fast and attempting to break things may be running out of road. Trump’s approval ratings are amongst the lowest of any recent President (including himself in his first term) and he may be losing his vice-like grip on the Republican party. The GOP is still reeling from a string of losses to the Democrats, and some MAGA loyalists have resigned. Crowd-pleasing deflection strategies – talk of fiscally reckless $2000 “tariff-dividends” – are not having the same populist potency they once had.

Meanwhile, many voters seem deeply dissatisfied with Trump’s “beautiful, normal inflation” (the fact that prices are rising more slowly may register less than the level of prices still being significantly higher than they were a few years ago).

Perhaps a silver lining is that as a result, Mr Trump is as open as ever to compromise: the recent tariff exemptions for key staples once again reminds us that those schedules were not written in indelible ink after all.

US election cycles are short, and the looming “midterms curse” does not bode well for a President with an approval rating close to 40% and a wafer-thin majority in the House of Representatives (gerrymandering aside). There are limits to Trump’s executive power – SCOTUS is flexing its constitutional muscles today – and without Congress, the effective reign of Trump 2.0 may well be approaching the end. Lame duck status may have arrived a lot sooner than he – or the Republican Party – hoped.

Presidential popularity and change in House seats at the midterms

Source: Gallup, The American Presidency Project

4. The UK is an emerging market

The year and a half since Labour swept to power can be most tactfully described as a series of unfortunate events, indecision, and perhaps a lack of political direction (and/or courage). Growth ambitions have morphed into a “same old” ‘tax and spend’ agenda, with the fiscal albatross taking centre stage.

But such political misfortune does not mean that the fiscal pantomime and near mass-hysteria which surrounded the recent budget has been warranted. The pundits’ tropes – talk of fiscal doom loops and IMF bailouts – are still very wide of the mark. The UK economy has not collapsed (indeed, it has continued to outperform Germany’s, though this is admittedly not a very high bar of late); government borrowing costs (as gauged by 10-year gilt yields) and sterling (on a trade-weighted basis) are little changed from when Labour took power last summer. Even the UK stock market has outpaced global stocks over this period (25% vs 22% in sterling terms), though admittedly this likely has little to do with domestic growth or policies.

When the budget brouhaha eventually fades from view, and normal life resumes, next year’s local elections may well prove to be a watershed moment for Messrs Starmer and Reeves. Labour and the Conservatives are both jockeying for poll position in the unpopularity contest. Meanwhile, the Reform Party are maintaining a sizable ten-point lead, and even the left-inclined Greens are staging something of mild rebound, suggesting that the UK is not immune from what has become an increasingly polarised political debate.

Of course, nothing is written in stone (with apologies to Ed Miliband and his Edstone…), and a lot more might happen between now and the next General Election in three years’ time.

5. The Santa Rally

“On Wall Street, the bulls give a jubilant cheer. While bears hibernate, their mood unclear”

After a tumultuous – and at times traumatic – twelve months, we appear to be on track for another vintage year. 2025 would mark a third consecutive year of ~20% returns at the global level.

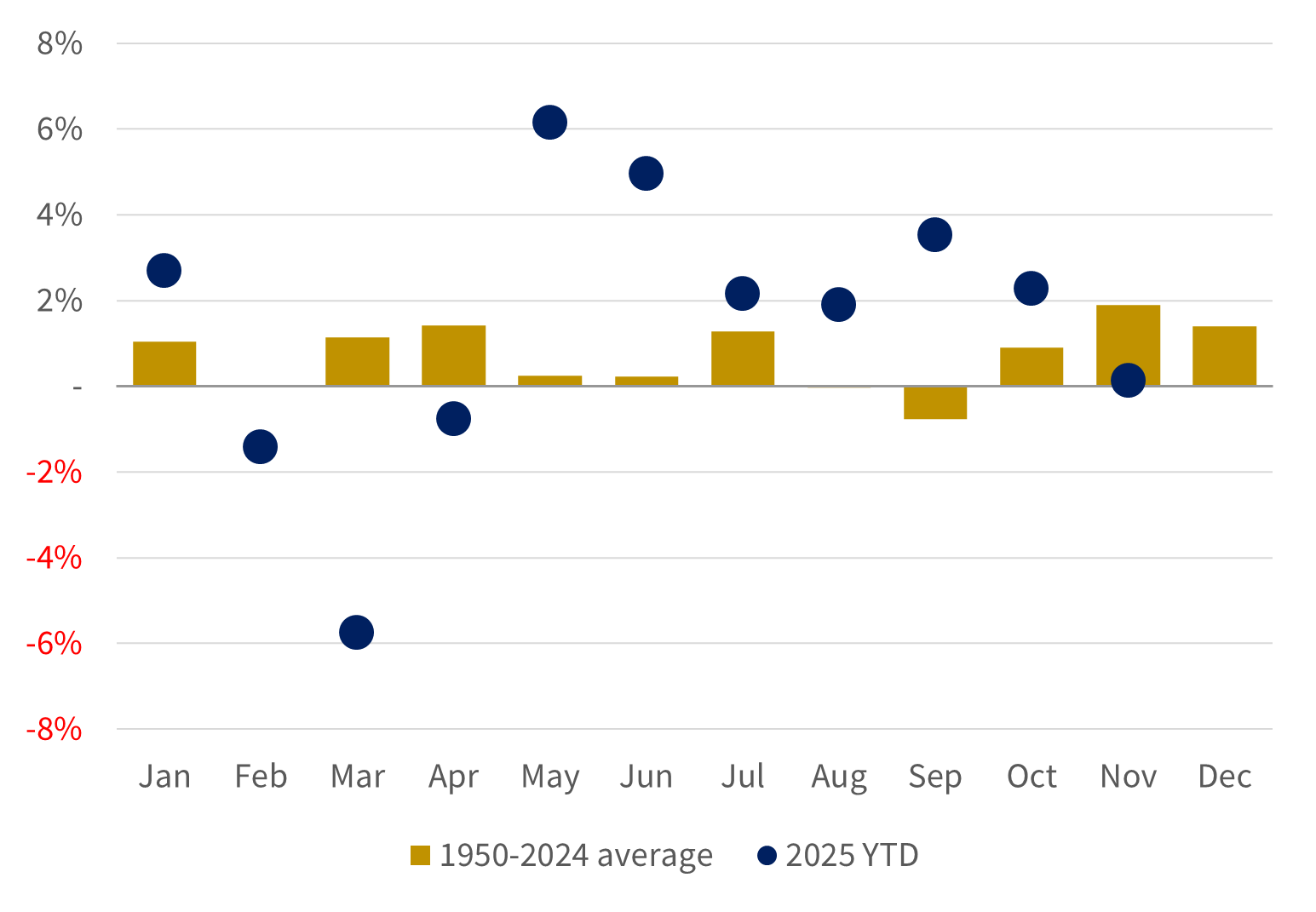

As is customary this time of year, talk of a “Santa Rally” is doing its seasonal media rounds. Christmas-cheer, thin liquidity and year-end portfolio rebalancing are frequently cited as a cause for year-end stock market optimism. Stocks, on average, do tend to perform better in December – but they also do well in most other months (quelle surprise).

US stocks: average monthly returns (1950 to 2025)

Source: Rothschild and Co, Bloomberg

Its perilous – and ultimately futile - to make any sort of prediction about the direction of markets over such a short period. That said, while we have ourselves been focusing for much of 2025 on downside risks, it remains eminently possible that stocks find themselves on a firmer footing as we enter 2026. The Fed is poised to ease again (possibly as soon as this week), macro indicators have remained relatively upbeat (despite the paucity of US data), and we are even seeing some signs of improving stock market breadth.

The AI story has become more fragmented during 2025 – some of the big tech names continue to lag after November’s setback – and the onset of another crypto winter suggests sentiment may have turned a more discerning corner in the final few months of 2025. There are tentative signs of a more cyclical rotation taking hold, which is making itself felt regionally as well as across sectors. There are still plenty of reasons to be optimistic, even if Santa doesn’t make an appearance in the coming weeks.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.