What goes up...?

Summary

-

Global equities have risen sharply since early April, led by AI-related stocks, prompting ‘bubble’ comparisons with the tech-driven Dotcom surge of 2000.

-

The current optimism is partially underpinned by economic strength and earnings growth. And there are many key differences with the late nineties’ episode – valuations, momentum, and leverage are less frothy today.

-

However, it could take considerable time for a wider AI revolution to become a reality, and there is a risk that much of today’s immense investment may not yield the near-term revenue gains, leaving rich valuations vulnerable.

Stock markets have travelled a long way in a short space of time.

Since the Liberation Day low in early April, global stocks have surged a third (in dollar terms), with the technology sector approaching double that. This rally has broadened beyond the fabled ‘Magnificent Seven’, but it is still heavily reliant on a basket of increasingly global AI-related stocks, which include the big semiconductor producers, as well as industrial and energy companies.

But volatility has returned in recent days, and bubble-chatter is getting louder. Many investors are fretting about whether we are at the end – or beginning? – of a stock market ‘melt-up’. Increasingly, comparisons are being drawn with the 2000 episode: then as now, a tech-driven theme pushed valuations higher amidst surging capital outlays.

Today’s stock market optimism is not without foundation – the economic story remains constructive and corporate earnings are still growing briskly. But talk of an AI utopia and productivity boom seem premature. The risk of capital misallocation – and, crucially, the scope for stock market disappointment – continues to rise.

Unhappy Anniversary

It’s been 25-years since the collapse of the infamous Dotcom (or Telecoms, Media, and Technology) bubble, and history is echoing. Then, as now, talk of a new paradigm prompted a dramatic technology-led stock market surge. The promise of the World Wide Web and the information superhighway: mobile comms, digital media, everything online. The internet, some suggested, had abolished scarcity: if you were sceptical, you just didn’t “get it”. Liquidity was abundant, equity valuations were uncomfortable, and credit spreads were tight.

The stock market gains came after a period of above-trend growth, with low unemployment, rising productivity and robust investment. As early as 1996 the Fed Chairman, Alan Greenspan, was warning of “irrational exuberance” in stock prices. After a couple of setbacks – the Asian debt crisis and the LTCM fiasco – liquidity conditions were loosened, and then stayed so as the millennium, and the feared Y2K problem, approached. The major macro difference with today perhaps is that despite liquidity being abundant by the standards of the day, interest rates were materially higher in 2000.

Between 1998 and 2000, the ‘New Economy’ frenzy took hold: capital expenditure boomed, telecom licence auction prices went through the roof, initial public offerings (IPO) and M&A activity surged, and the tech-heavy Nasdaq index (and Germany’s “Neuer Markt”) went exponential. If valuations had looked irrational to the Fed Chairman in 1996, then they had become entirely unmoored by early 2000.

When the music stopped playing, US stocks lost half their value – the Nasdaq collapsed by more than three quarters – over the following two years. Many dotcom companies (and the Neuer Markt) disappeared, and several high-profile mergers had to be written down or unpicked.

It wasn’t until 2015 the Nasdaq index reclaimed its previous high.

What’s in a definition?

There is no technical classification of a bubble, but the notion generally applies to an asset whose price becomes so wildly detached from any sort of reasonable levels that an eventual collapse becomes inevitable. There is unfortunately no clear line in the sand that tells us when those “reasonable” valuations have been exceeded.

Today’s price-to-book ratios and price-earnings (PE) ratios do look elevated: we’ve only been at higher levels than these once before – in 1999/2000. But even if these indicators are looking statistically uncomfortable, the current episode is not yet as outlandish as was the case then: the richly priced US technology sector is trading at close to half its peak dotcom forward PE multiple. Importantly too, as we noted above, today’s lower interest rates – and bond yields - suggest that discounted cashflow-based valuation metrics are less stretched than plain earnings-based multiples.

Source Rothschild & Co, Bloomberg, S&P Global. Note: Past performance is not indicative of future performance and the value of investments and income from them can fall as well as rise.

In some qualitative ways too, the backdrop is different today. Most of the businesses leading the way up recently are profitable, with healthy cash flows and clean (debt-free) balance sheets. Many equivalent dotcom businesses didn’t have revenues – let alone earnings. Business viability mattered far less than effective branding – the suffix ‘.com’ was a potent fundraising tool. Pets.com serves as the poster child for dotcom exuberance – going from IPO to liquidation in less than a year. But bandwagon behaviour was widespread: a number of large stocks, including Qualcomm, surged more than tenfold in 1999 in the great ‘melt-up’ phase.

Price momentum today falls well short of the nineties herding and there is no sign of the frenetic deal-making activity or stock issuance. Much of today’s corporate activity is confined to smaller - and perhaps less systemically-important - private markets. Crucially, leverage also seems absent from today’s excesses – aggregate corporate debt is more subdued now (according to macro data which includes both public and private markets).

Great Expectations

In recent years, the US stock market has experienced a secular trend of improving profitability, reflecting not just corporate performance but also a shift towards less capital-intensive output as the technology sector and digitisation has led the product cycle. But as the AI ecosystem – encompassing hardware, infrastructure, and software – has started to deploy immense amounts of capital in order to secure its access to processing capacity and energy, this trend may be going into reverse.

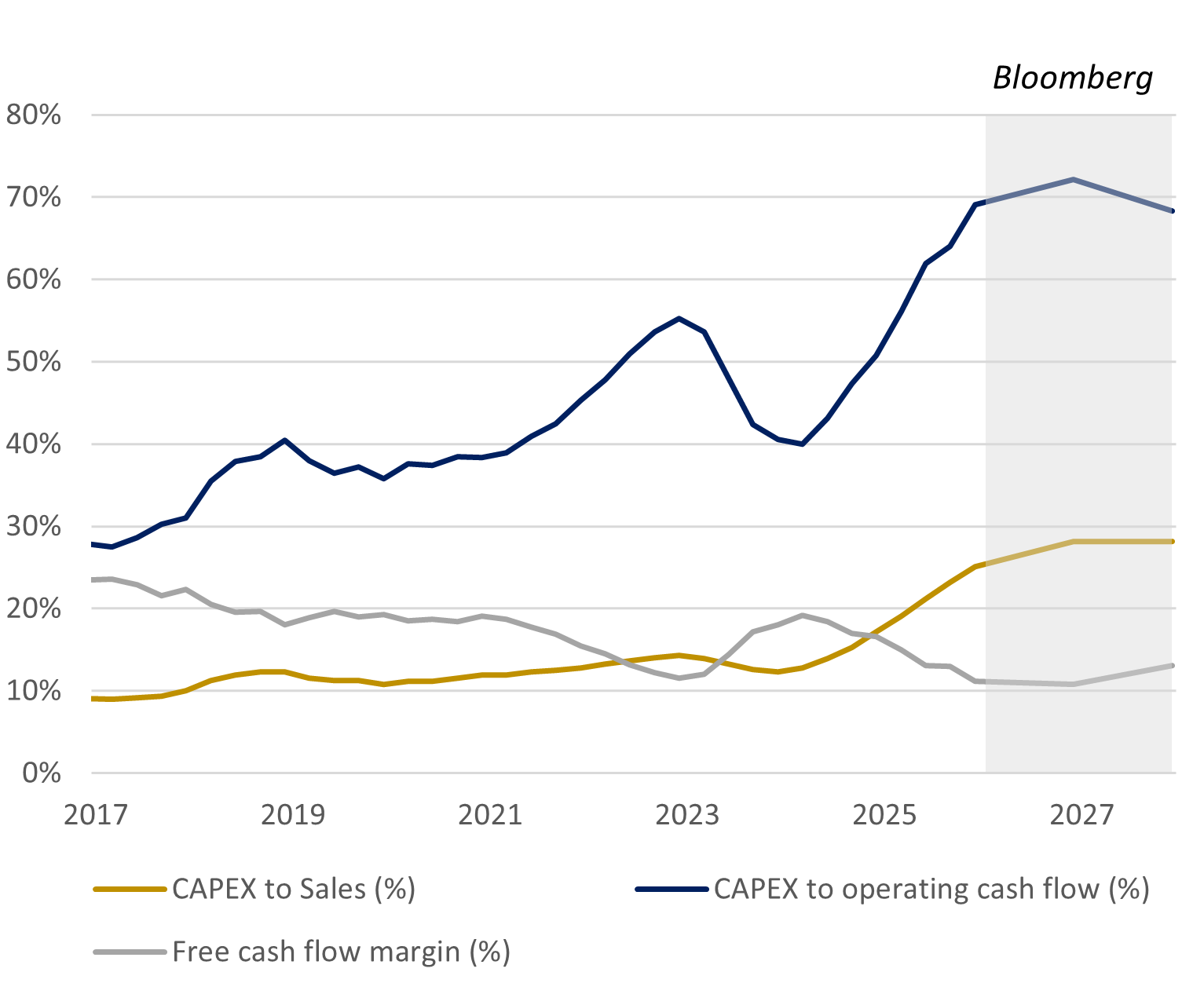

The large hyperscalers’ superior free-cash-flow margins – one of their most attractive investment qualities – has fallen sharply in the past five years, and some of the capital outlays that are consuming it risk becoming obsolete within a few years (unlike, for example, the late nineties fibre rollout that is still being utilised today).

Hyperscalers: Rising capital intensity

Hyperscalers’ include Microsoft, Alphabet, Amazon, Meta, and Oracle. Reflects aggregated trailing 4Q data, calculated to Q3 2025. Consensus estimates are derived from Bloomberg for FY 2025, 2026 and 2027

Unless today’s Large Language Models quickly drive a widespread breakthrough in productivity trends – which is looking unlikely as we write – there is a risk that much of today’s investment will prove unprofitable for both the purveyors and users of today’s AI, leaving valuations looking vulnerable.

AI proponents suggest demand is insatiable, that wider adoption is only constrained by a lack of supply. This is true insofar as the scaling of AI’s computational intensity is outpacing the supply (efficiency) of chips, as well as the electricity supplies to support them.

But even setting aside the immense capital requirements for such ambitions, this tells us little about the ultimate destination. Will the activities facilitated by those chips themselves prove profitable in due course? How many business problems are “computable” to begin with? Is Big Data necessarily going to solve those which are?

Meanwhile, increasingly visible circular transactions are raising the spectre of “vendor-financing” – businesses funding their customers’ purchases. This may well reflect a practical business strategy - helping customers maintain cashflows in the course of their operations – but it could also suggest that demand is not appearing as quickly as the hyperscalers hope or need. Business adoption rates for AI seem to have cooled, and a tidal wave of insipid textual content may be fuelling user scepticism.

Time to meet your (chip) maker?

Even if AI delivers, it could take considerable time for a wider AI revolution to become a reality. The advent of earlier general-purpose technologies was followed by a considerable lag before they delivered a transformative economic impact (indeed, this turned out to be true of the internet). Widespread adoption – and the subsequent productivity benefit – is dependent on a whole host of factors alongside the technology itself, including social attitudes, government policy, and consumer behaviour.

The parallels with the dotcom episode may be incomplete and we don’t know when the AI investment flywheel is likely to slow. But our inclination is not to chase this market higher. Stocks have a way of looking across the valley, but today it feels as if we are looking across not one, but two peaks. And while those elevated valuations may not be a useful short-term timing tool, currently there is not a lot that separates stocks from bonds – or even liquidity.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.