Japan: change of leadership

Sanae Takaichi, a close ally of the late Shinzo Abe, is looking to become Japan’s first female PM after unexpectedly winning the latest Liberal Democratic Party (LDP) leadership race.

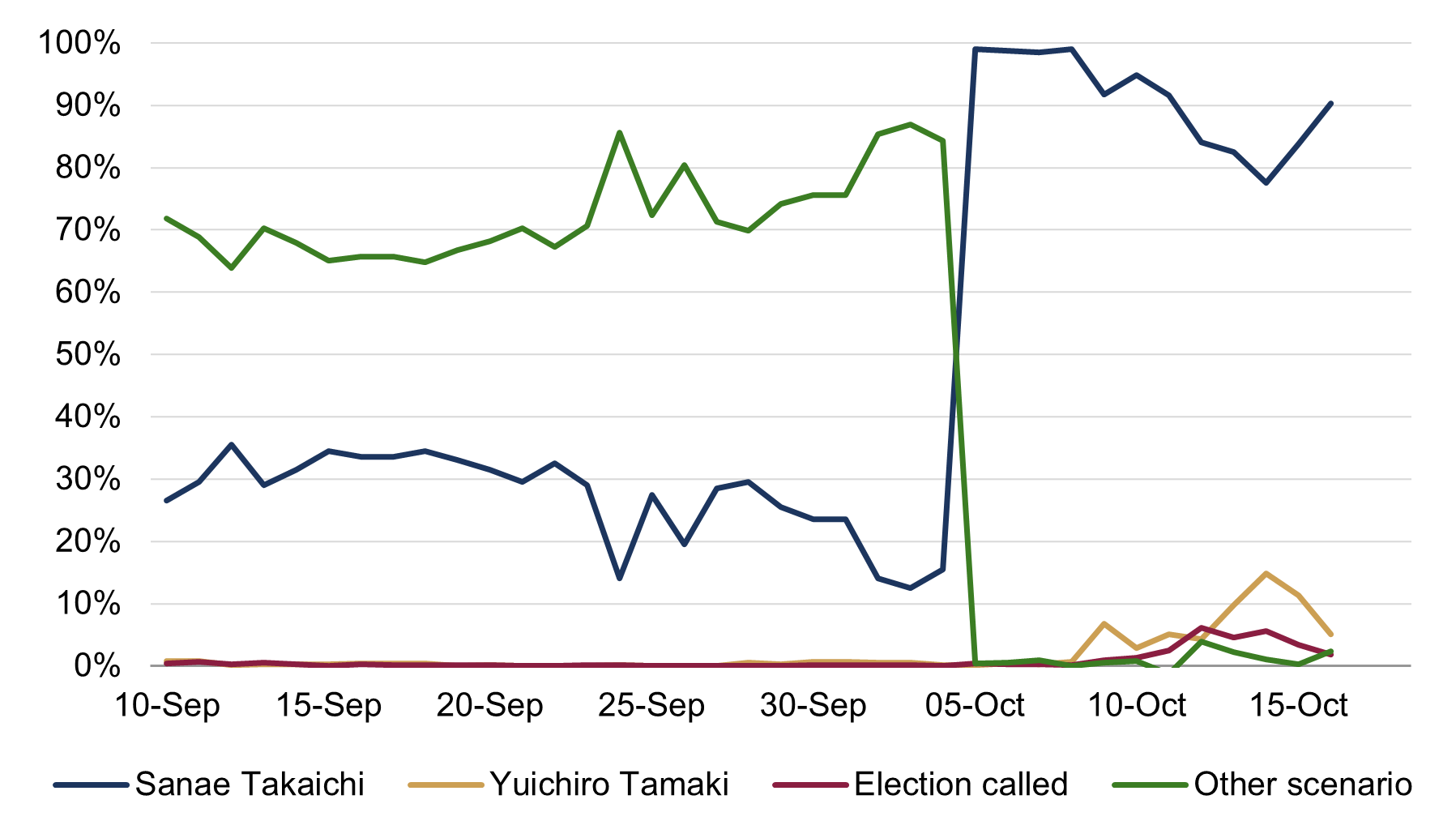

The party is undoubtedly looking to reverse its fortunes. In recent years, the LDP’s popularity has plummeted, following its ‘Slush Fund’ scandal, above-target inflation, and rising migration and tourism levels. In fact, public dissatisfaction culminated in the LDP losing both its upper and lower house majorities in the Diet (Japan’s parliament) earlier this year – for the first time in the party’s history. To make matters worse, its long-standing coalition partner, Komeito, recently broke its ties with the party. This move has created a low-probability scenario, where rival parties could group together and nominate an alternative PM, with the DPP’s Yuichiro Tamaki the current frontrunner (figure 1). This would be remarkable because the LDP has been in power for all but six years of its 70-year existence, most recently since 2012.

Figure 1: Next Japanese Prime Minister odds

(%)

Source: Rothschild & Co, Polymarket. Note: ‘Other scenario’ is defined as all other candidates or a ‘no PM’ outcome.

Takaichi is nonetheless the favourite to be the next PM, with a vote possibly occurring next week. The local stock market initially responded positively after her LDP leadership victory, probably because she has long supported Abe’s pro-growth policies, known as Abenomics (the fact that she plays drums in a ‘heavy metal’ band does not seem to have hurt her chances…). Exactly how successful Abenomics was for the economy and stock market, however, is debatable.

Revisiting the Abenomics playbook

Abe’s ‘three arrows’ approach from late 2012 to 2020, during his second stint as PM, was aimed at reviving domestic growth.

The first two arrows were monetary and fiscal policy. The former consisted of a huge quantitative easing programme (the purchasing of bonds and other securities from the market) from the Bank of Japan during which its assets roughly quadrupled (its negative interest rate policy was not that economically significant, given the starting rate was already close to 0%). Fiscal stimulus included big spending packages, mostly focused on infrastructure, but was partly offset by a doubling in the sales tax rate.

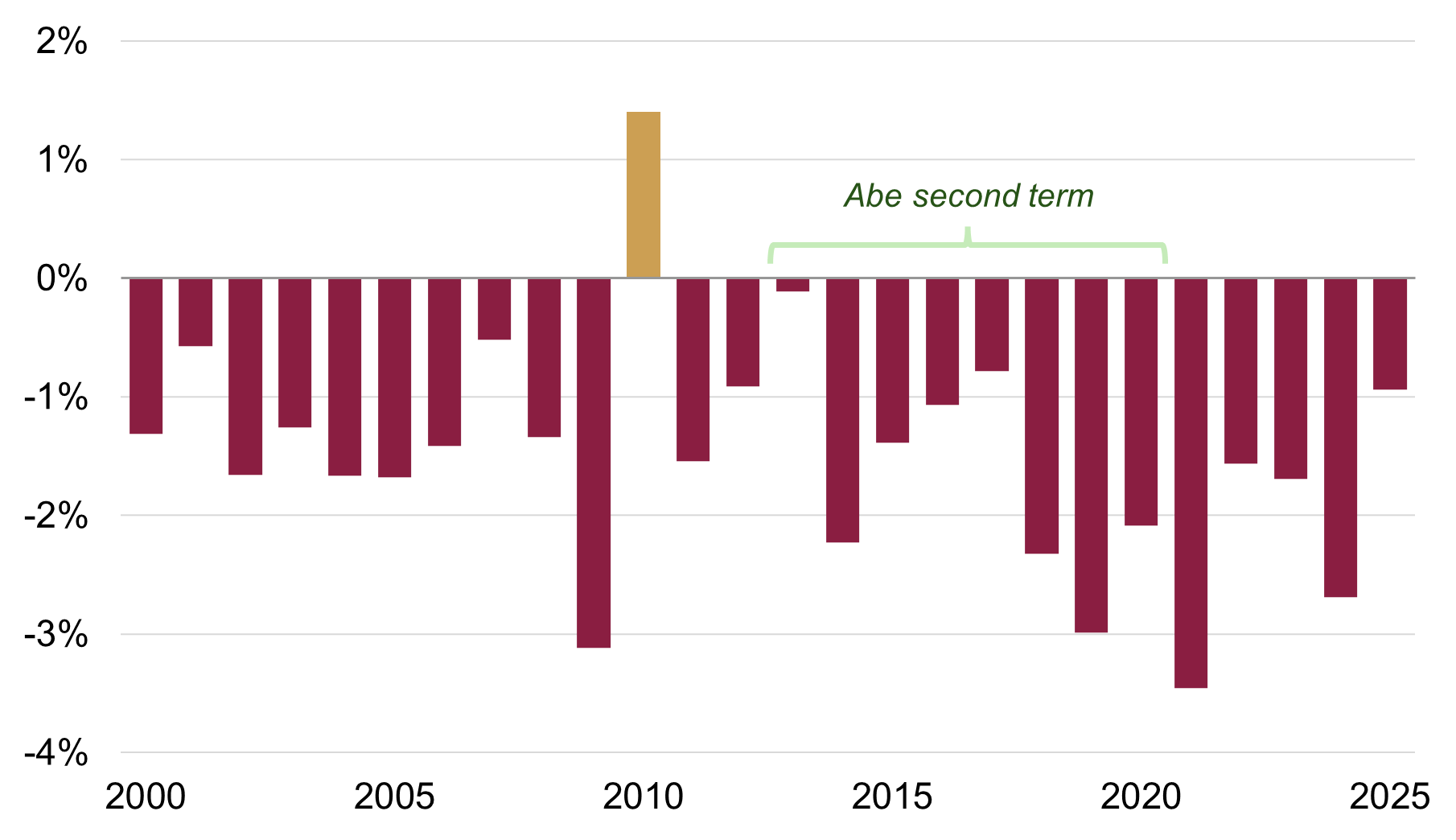

However, despite a relatively strong outturn for GDP growth initially, Japan’s economy remained relatively subdued. It has in fact only outpaced US economic growth once since the turn of the century – which is particularly striking considering its ‘lost decade’ was supposedly in the 1990s (figure 2). For context, Japanese GDP growth was actually relatively stronger in the first two years of that decade, but in subsequent years the magnitude of underperformance was far greater: Japan’s GDP growth was on average 3 percentage points weaker than the US’s between 1992-1999, compared to an average underperformance of 1.5 percentage points between 2000-2024.

Figure 2: Japan-US GDP growth gap

Difference in annual growth (percentage points)

Source: Rothschild & Co, Bloomberg, IMF. Note: 2025 data uses the IMF estimates.

Meanwhile, the final arrow of Abenomics focused on structural reforms, aiming to make corporations more ‘competitive’ (rightly or wrongly – more on this later). As noted elsewhere, Japanese companies have historically operated with little regard to commercial or conventionally capitalist considerations: market share and stability were prioritised over ‘shareholder value’, and many corporations held ‘excess cash’ on balance sheets. As a result, despite occasionally strong earnings growth, return on equity (RoE) – a gauge of corporate profitability – has remained relatively weak.

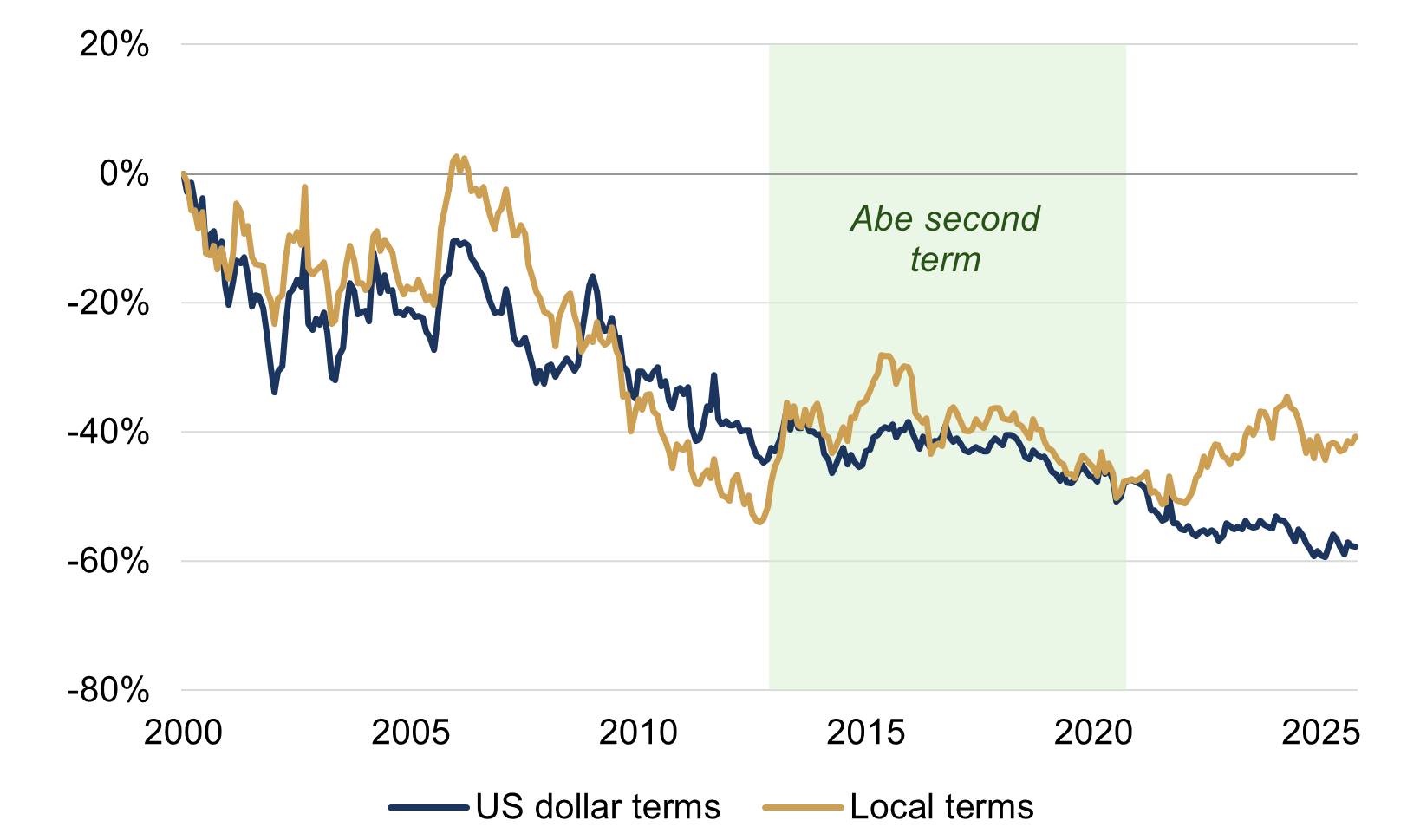

A mix of governance codes and guidelines were subsequently introduced by authorities, to try to align Japanese companies with commercial incentives. Nonetheless, macroeconomic performance remained relatively poor, with the stock market following suit, underperforming the global benchmark during Abe’s eight-year tenure (figure 3).

Figure 3: Relative returns since 2000

Japan vs All Country World Index (MSCI indices, %)

Source: Rothschild & Co, Bloomberg, MSCI

Takaishi’s Castle?

‘Takanomics’ may not be any more successful than Abenomics. While the incoming PM is eager to loosen policy – she has hinted at tax reliefs and expressed discontent with the Bank of Japan hiking its interest rate (despite the negligible increase) – she may be more restricted than Abe.

The Bank of Japan is unlikely to lower interest rates with inflation still hovering well above target (mostly driven by higher food prices, however, rather than a ‘hot’ economy) and it is also reducing its asset holdings. Fiscal support may even be limited given the LDP falls well short of a majority in both houses of the National Diet, though a new coalition partner may help to mitigate that risk.

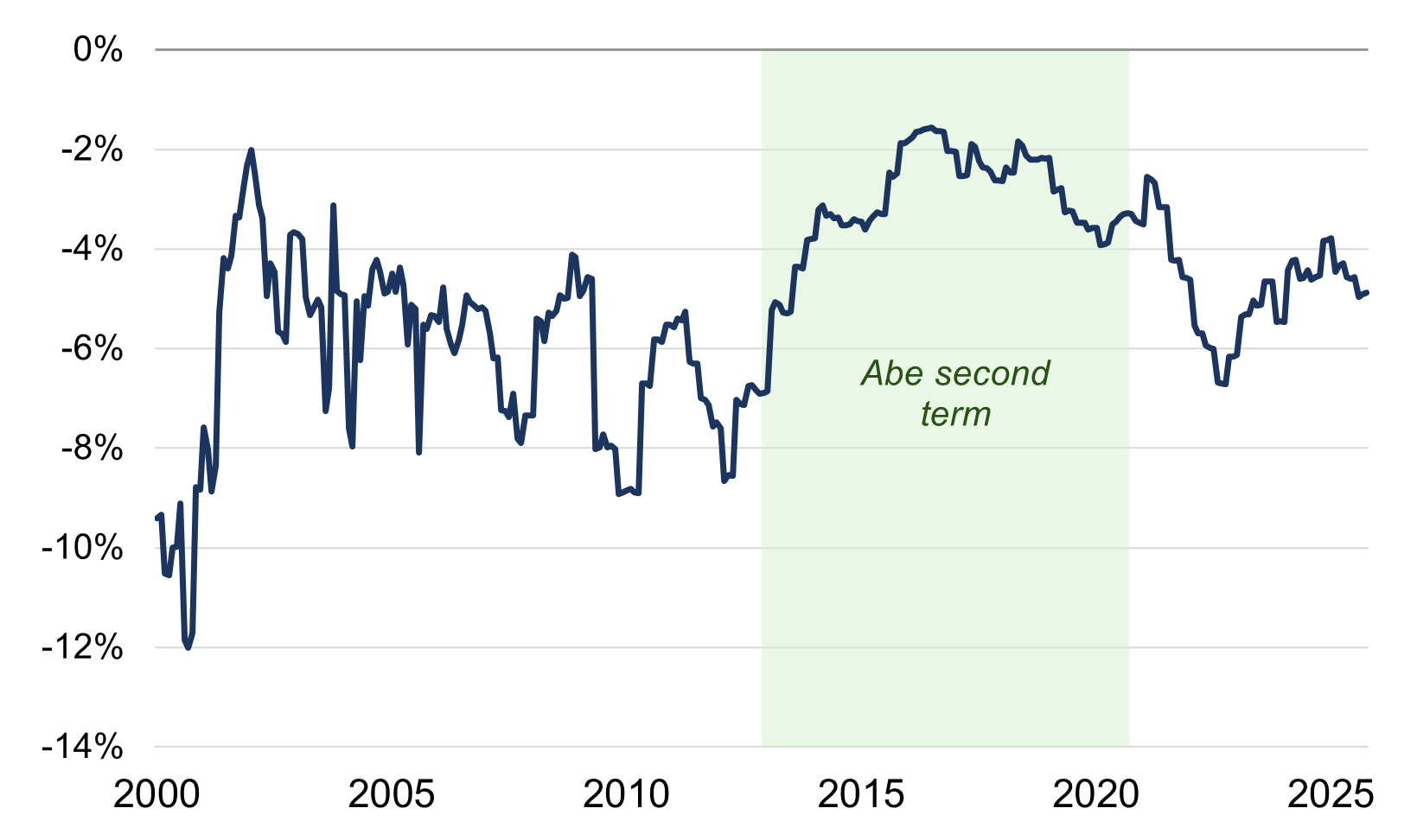

That leaves the structural reform lever. Abe’s successors continued to implement further corporate reforms, which have led to an improvement in some governance metrics over time. There has, for instance, been a reduction in cross-shareholdings and more independent directors on listed companies’ boards. Subsequently, profitability appears to have improved a little in recent years: Japanese RoE is currently hovering towards the higher end of its historical range, at around 10%. However, it remains several percentage points below the global RoE (figure 4). While ongoing reforms are likely under Takaichi, this would have probably also been the case under other LDP candidates.

Figure 4: Relative RoE gap

Japan vs All Country World Index (MSCI indices, percentage points)

Source: Rothschild & Co, Bloomberg, MSCI. Note: the relative RoE gap narrowed during the first few years of Abe’s tenure, seeming to suggest that his policies may have worked to an extent. That said, it may have partly been due to developments elsewhere – the MSCI All Country World Index’s RoE briefly declined modestly then – while Japan’s RoE was starting from a very low base.

Conclusion: no Great Wave

While Japanese stocks have roughly matched global returns this year – in both local and common currency terms – the nomination of Takaichi may not necessarily lead to a sea change. Some of this year’s Japanese stock ascent may for example be related to renewed AI-related momentum, rather than local political optimism.

It’s also possible that Takaichi fails to become the next Japanese PM, instead supplanted by a rival coalition candidate (as noted). If anything, the DPP nominee may push for even more stimulus, which while good for growth (and likely stocks), could unsettle the local bond market a little. Political instability would likely remain a feature as well, given the potential rival coalition’s diverse views on topics ranging from nuclear energy to national security. There was indeed a similar scenario in 1993, where a makeshift rival coalition managed to nominate a PM, but they unsurprisingly had a very short shelf life.

Politics aside, we continue to watch Japan’s profitability trends closely. It is worth noting, however, while business practices are not perceived to be optimal for the stock market, Japan still has many world-class businesses providing high-quality goods and services. Unemployment has also been remarkably low by Western standards – even through the pandemic. ‘Shareholder value’ is not the only benchmark of success.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.