The return of the gold bugs

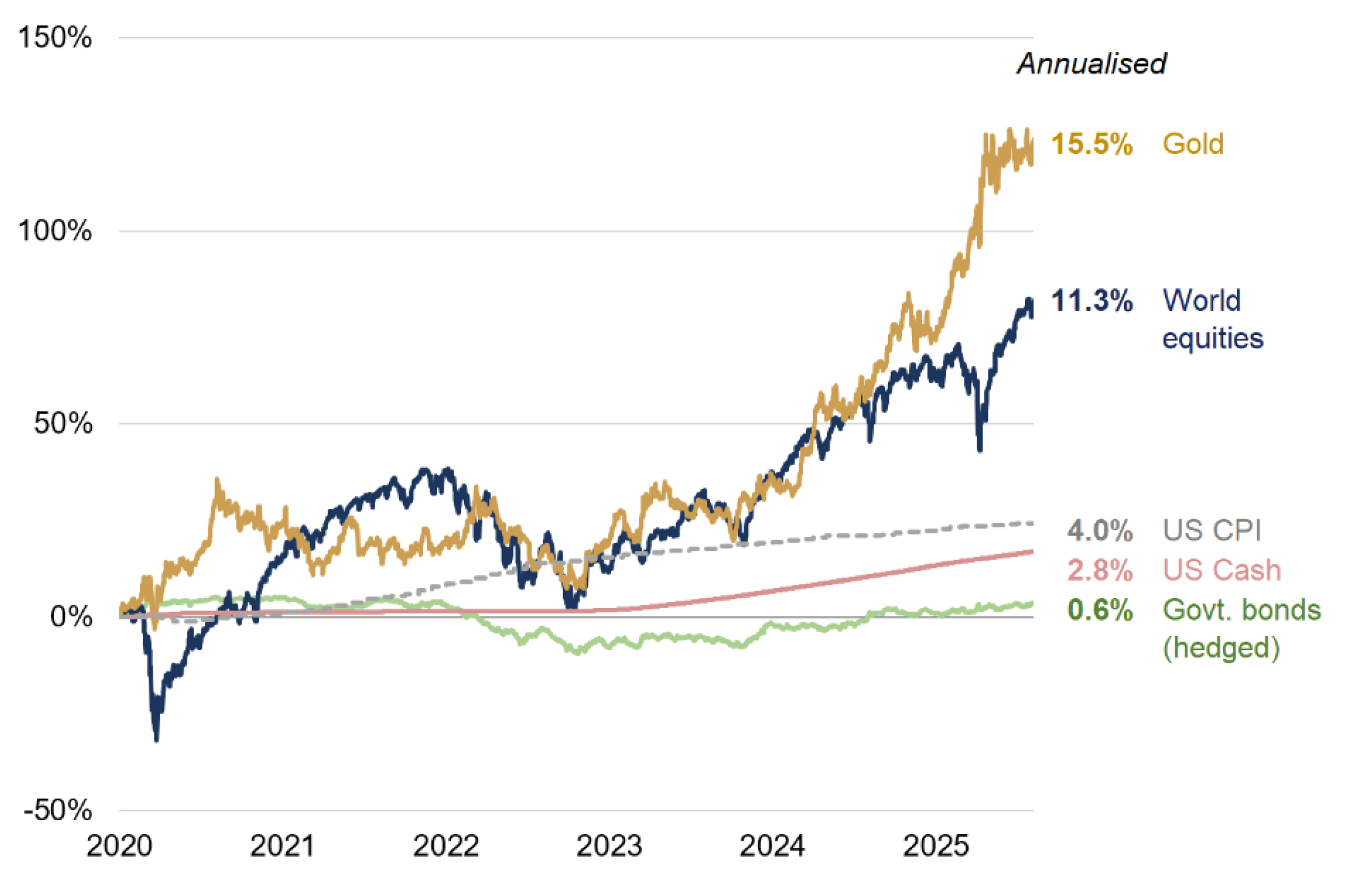

Gold is having another bumper year. The shiny metal is up by more than a quarter in 2025, and on track for a third consecutive year of double-digit returns – a winning streak not seen since the mid-noughties.

Gold has outperformed all other major asset classes in recent years

Total return (USD terms) │1st January 2020 to 8th August 2025

Source: Bloomberg

But this climb has been anything but stable – or predictable. Gold has lost touch with its traditional drivers like real yields and the dollar, with demand shaped by the geopolitical maelstrom – including protectionism and wider conflict. Yet despite ongoing attempts to reshape global trade – and even talk of a renewed gold arbitrage - prices have been flatlining for several months now.

So how should we view gold from a portfolio standpoint?

Clearly gold (more so than other precious metals) has played an important investment role. Historically it has been a long-term store of value over several millennia, lending monetary institutions their credibility (rather than vice versa) and acting as a key medium of real wealth protection. It can also act as a financial panic button, a sort of last-resort asset at times of crisis. Amidst fears of US default (as in 2011), banking collapse (2008) or runaway inflation (1979) it has strongly outperformed securities markets. Almost overlooked amidst its investment role, it also has intrinsic uses in industrial and ornamental applications, though these form a very modest part of today’s global demand.

But it is impossible to value objectively. Arguably this is true of all assets, but the absence of a yield makes it particularly difficult for gold and other commodities: discounted cashflow analysis is correspondingly impossible. This might not matter if the real price were stable, but it isn't. Current mining costs are not a useful guide to value – supply is inelastic and most gold traded is already above ground.

Nonetheless, when interest rates rise, the price of gold can be affected: its lack of a yield can count against it. Intuitively, this reflects the opportunity cost of owning gold relative to other 'risk-free' assets such as treasuries. But this hasn’t often been the case in the last few years, with gold unusually rising alongside higher yields. Nor is gold’s relationship to the dollar always helpful: dollar weakness this year may explain some of gold’s ascent, but the same cannot be said of late 2024 – when all around dollar strength should have been a headwind, but gold continued to surge (relative to all major currencies).

Other, more qualitative factors can also affect the gold price. Most obviously, perhaps, geopolitical risk, and/or central bank buying. A number of mostly emerging economies, particularly China, have been big buyers of gold in recent years as they look to ‘de-dollarise’. On this count, a disruptive President Trump suggests gold will remain a crucial currency diversifier ahead.

However, there are two possible headwinds to be mindful of. First, the economic story remains constructive: we don’t think stagflation, or a big economic downturn is likely or imminent – two scenarios that would benefit gold meaningfully. US growth is (still) respectable and although inflation has started to edge higher, tariffs aside, it will likely remain manageable. This suggests to us that the Fed’s easing cycle is likely to be relatively short-lived from here. The current ongoing idea of rates being ‘higher for longer’ points to elevated real yields and at some stage (possibly) a rebounding dollar – which might temporarily constrain gold’s advance.

Meanwhile, Bitcoin’s ascent and wider crypto competition to gold as 'debasement hedges' remains an obvious (if unconvincing…) threat. Recently passed US regulation is set to further legitimatise stablecoins, which may encourage more enthusiasm for unbacked coins. But in the Bitcoin vs gold debate, we strongly prefer the latter: we see our role as investment advisers being not to help our clients 'get rich quickly' but rather to stay so.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.