China: the long and winding road

China’s stock market is on track for its best calendar year performance since 2020, with the MSCI China index rallying ~28% in 2025 (in USD terms) – nearly double the return of the global stock market. Its economy is still growing perhaps three times as fast as the developed world, and it has plenty of fiscal and monetary space to meet it’s 5% target.

Despite this, many of China’s deep-seated structural issues are set to persist. Today’s growing pains – property, debt, and deflation – are being amplified by geopolitical quarrels. Trade negotiators may have kicked the can down the road, but China could still be confronted by one of the highest tariff rates with its biggest trading partner.

It often feels like China’s economy is at a crossroads, but weaning itself from investment and credit-led growth and mollifying a mercurial Mr Trump at the same time is no mean feat.

Bamboo does not break… but it does bend

Despite the huge uncertainty surrounding trade policy, China’s economic momentum has remained relatively resilient through the first half of the year – and slightly faster than in 2024. This is largely on account of buoyant exports boosting industrial output - China has benefitted, if only temporarily, from tariff front-loading (the same front-loading which hit the US economy). The weaker renminbi (which has tracked dollar weakness) has also provided a helpful boost to non-US exports, particularly to other Asian economies. For now, China has staved off a tariff-induced slowdown - external demand remains intact.

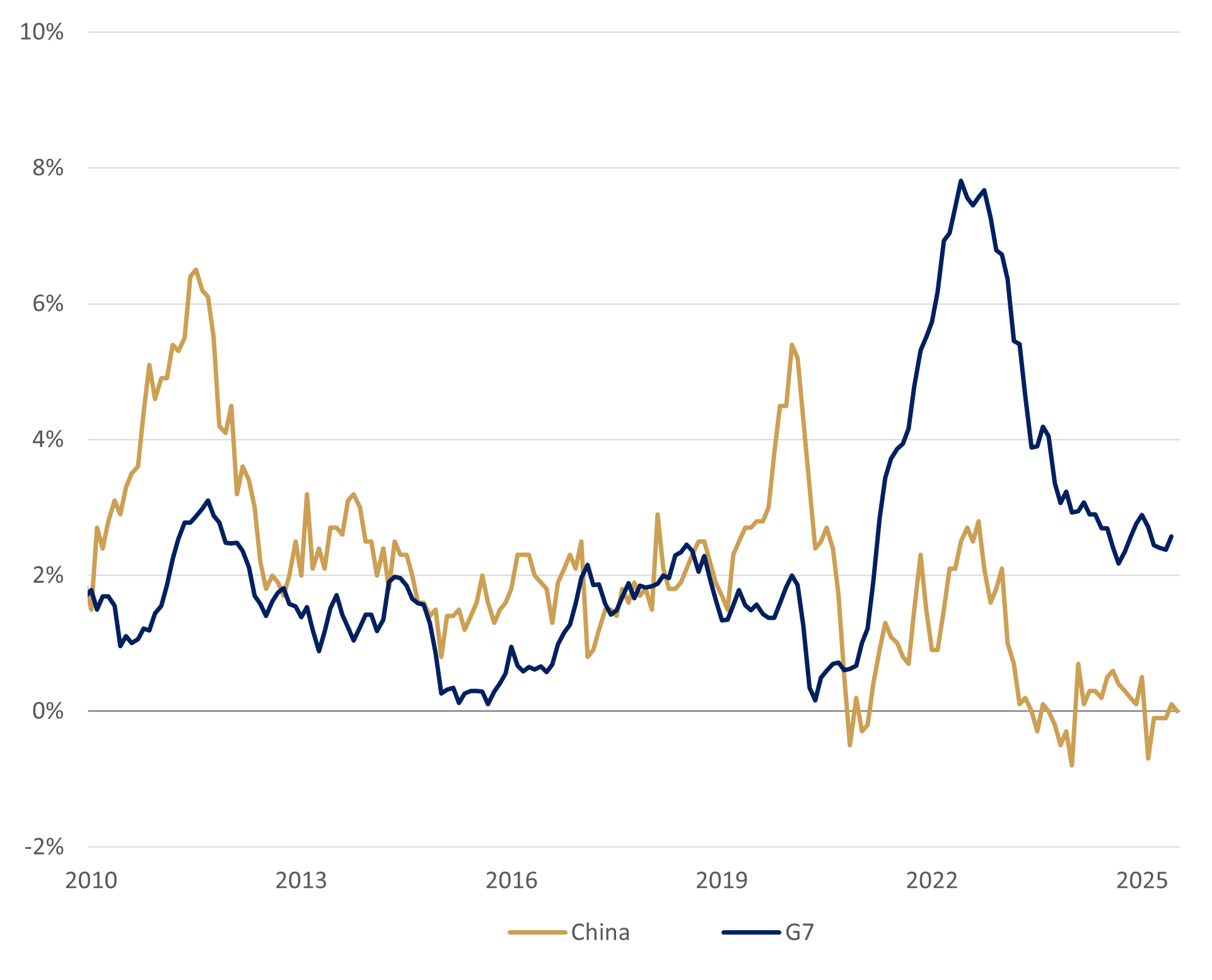

Headline inflation (CPI, y/y %)

Source: Rothschild & Co, Bloomberg, OECD

However, this is a transient boost, as noted, and other growth drivers remain decidedly lacklustre. Consumers remain cautious entering the third quarter: confidence surveys are depressed, the jobs market is soft, and household spending is tepid – despite ongoing government subsidies. With demand so weak and manufacturing overcapacity keeping a lid on goods prices, deflation is close, and for many observers this poses a real risk.

Ironically, manufacturing investment has been a rare bright spot, expanding briskly, but this is overshadowed by a moribund property market. Real estate investment is still contracting sharply, and infrastructure spending is stagnating.

Property pain: still unresolved

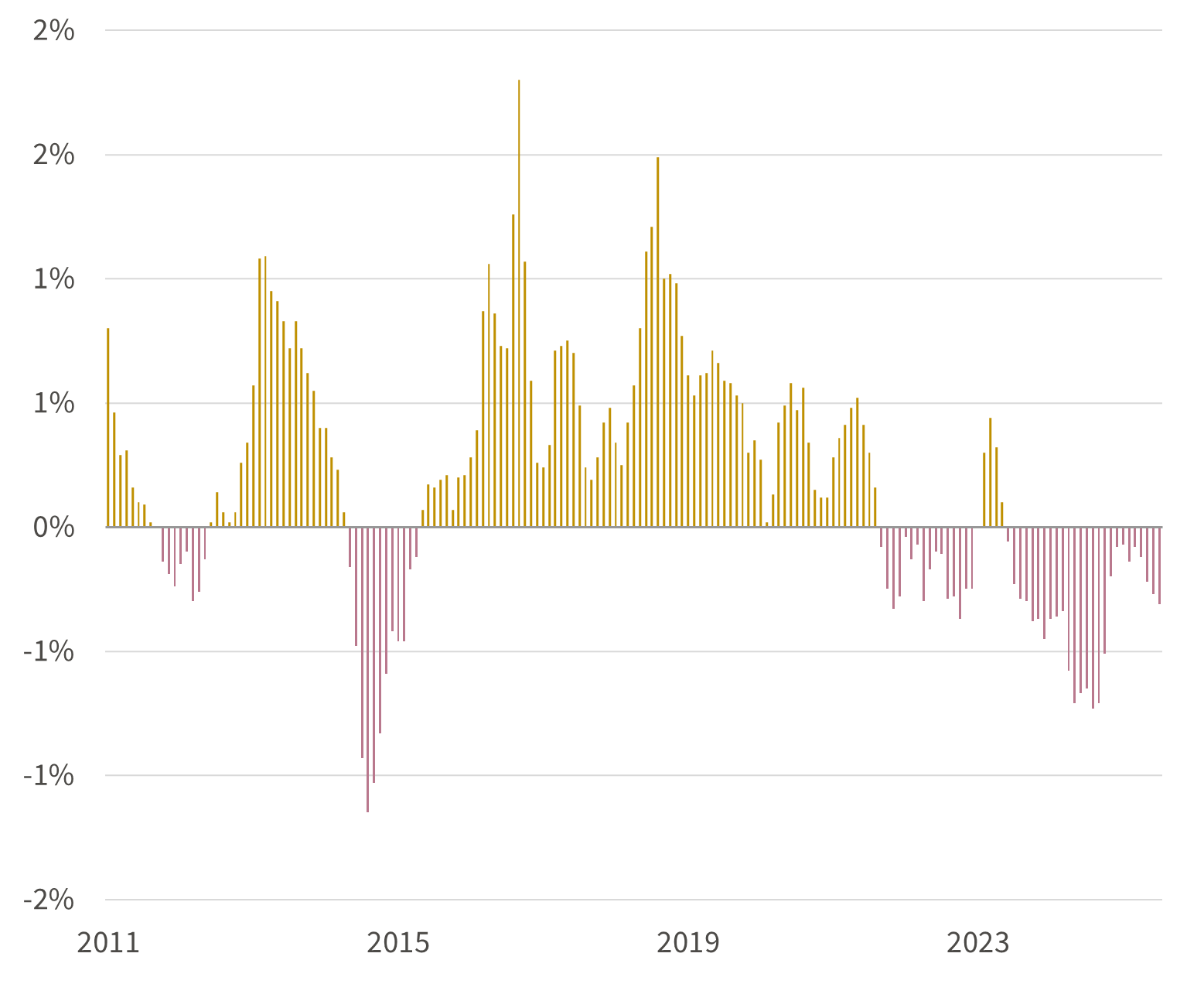

Property has long been a cornerstone of China’s economic engine and still remains both the cause and (part of the) solution to China’s domestic malaise. Signs of a tentative housing market recovery have given way to a renewed downturn in recent months – new home prices have been contracting for over two years now. And with two-thirds of urban household assets tied up in property, spending is likely to remain depressed.

Selling prices of newly-built commercial residential buildings

(monthly change, %)

Source: Rothschild & Co, Bloomberg

Property developers are also in balance sheet ‘repair mode’. Low sales volumes continue to weigh on anaemic cashflows, and the situation is unlikely to improve: incoming regulations are set to ban questionable ‘pre-sales’. But it’s the sheer scale of shadow inventory, with as many as 1.6 homes per household, that remains the bigger structural challenge. Unresolved, it suggests growing debt burdens will necessitate further restructuring. Of course, the risk of a “Minsky moment” – that systematic Lehman-like event – is still small, in our view. Government debt is low, and China can restructure liabilities at will – catastrophisers take note.

Policy continues to be supportive, but targeted. Most stimulus measures announced last autumn are still aimed at propping up demand for property, with limited success. Meanwhile, the People’s Bank of China continues to support the government’s growth policies, through a very gradual easing of key policy rates. Subdued loan growth – restrained by ongoing household deleveraging – is likely what policymakers want to see, for fear of promulgating another big credit cycle.

All of this suggests that the days of property investment leading China’s growth are likely over.

The second China shock

The trade surplus in manufactured goods is the subject of intense US scrutiny, with the so-called second China ‘shock’ a persistent gripe. Unlike its noughties predecessor, which was characterised by low wages and cheap products, this latest ‘shock’ reflects an oversupply of higher value-added products pushing export prices down.

China is adept at marshalling its resources and labour force. Arguably its ‘Made in China 2025’ strategy – an industrial policy to dominate high-tech manufacturing – was a little too successful. Patent-intensive industries and rapid research and development (in pharmaceuticals and electric vehicles) are displacing traditional ‘old economy’ industries at home, and competing abroad. But subsidising unprofitable enterprise and exporting excess capacity is no longer politically viable. Anti-dumping investigations by its trading partners – against a variety of materials and finished goods (particularly EVs) – are not just confined to the US.

China is seeking to address some of these imbalances through its recent anti-involution campaign, which seeks to curb excessive competition and ultimately overcapacity. Beijing’s objective is not to deindustrialise to pacify Trump, but rather it is an attempt to end the threat of domestic stagnation and deflation (though the two are not mutually exclusive). But it’s possible that such policies may do more damage in the short term – forcing businesses to produce less may even add to deflationary pressures.

The road less travelled

The reallocation and diversification of manufacturing output - perhaps to other Asian hubs - will likely continue. However, China’s role at the centre of global supply chains is unlikely to change overnight. It currently accounts for 30% of global manufacturing output and it has more people working in goods-producing industries than the next ten biggest economies combined.

China is coming to the end of its 14th Five-Year plan, with the next iteration set to focus on prioritising economic resilience. Boosting household consumption – particularly within services – is an inevitable part of China's economic evolution.

Part of this very gradual shift to a consumption-led economy is constrained by government policy, inequality, and societal attitudes to spending. China has one of the highest household savings rates globally (at close to one third of disposable income), though this partly compensates (ironically perhaps) for its relatively small welfare state.

Regressive tax policy prioritises low income tax rates but places a heavy reliance on indirect taxation and mandatory social security contributions, which act as forced savings. Gradual improvements in that social safety net – notably medical costs and the more recent child subsidy – may start to alleviate the need for those precautionary savings. However, reforming income tax rates will likely face consider resistance from wealthier households, which have considerable political sway.

Investable, but not compelling

There is some debate as to whether China’s current predicament mirrors the painful restructuring of the 1990s. Back then, privatising the stagnant SOEs and reforming the banking sector eventually led to a robust economic resurgence. Today, this applies not just to the real estate sector, where an extensive debt build-up is evident, but also to China’s wider export-led growth model.

Through this lens, China’s challenges are surely not insurmountable. That said, there may be no quick fixes either.

From an investment standpoint, the long-awaited revival in its inexpensive stock market remains unconvincing. Although we disagree with the popular view a couple of years back that China has become “uninvestable”, renewed enthusiasm from local investors may not be sustainable, particularly with margin leverage building once again. Meanwhile, Beijing’s more authoritarian approach to capitalism may be less in evidence these days, but in its place geopolitical threats have emerged.

For now, with domestic growth likely under pressure – and with the outlook for corporate profits, which rarely grew strongly even when GDP growth was much higher – the investment outlook does not yet look compelling.

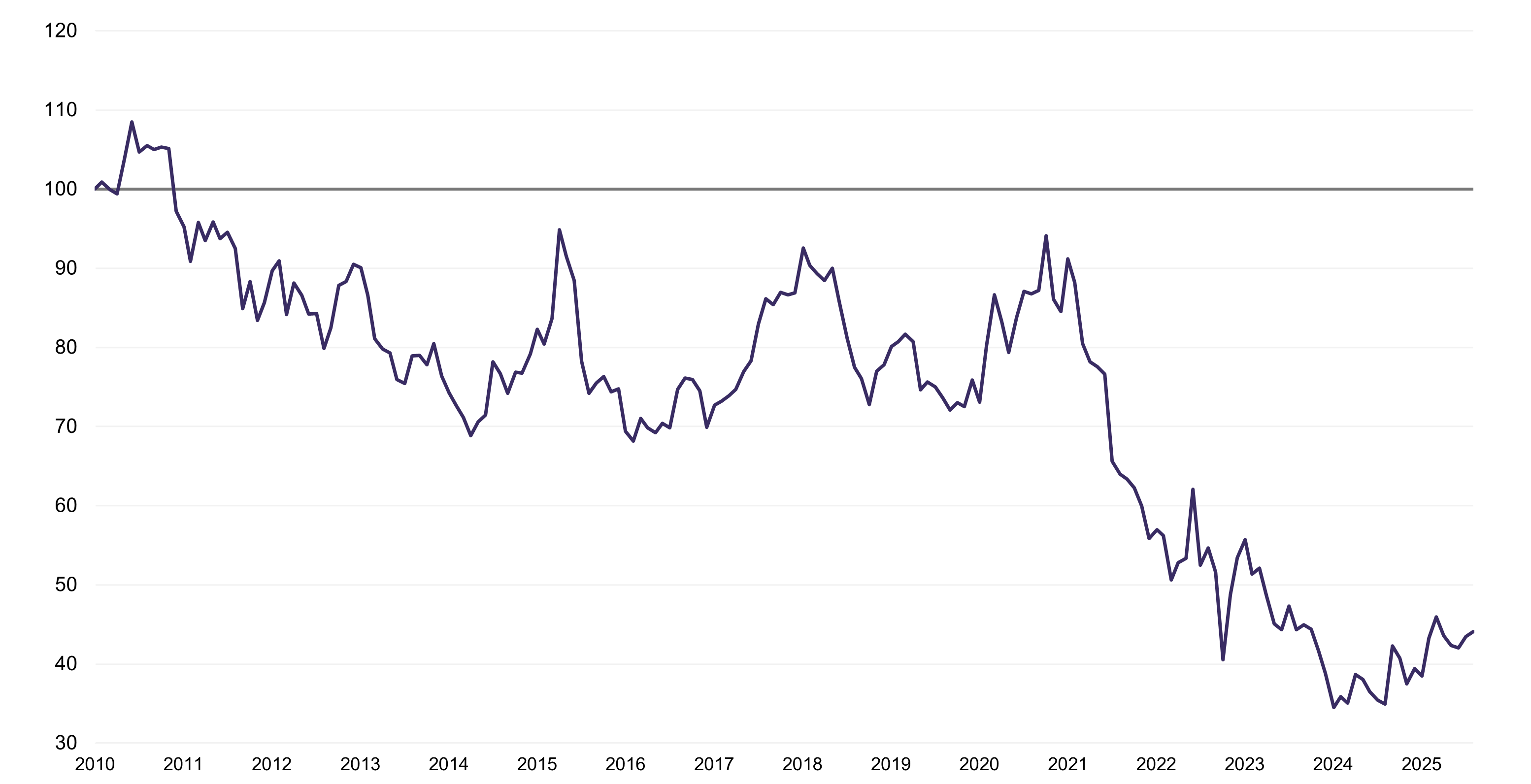

China’s long-term relative stock market performance

MSCI China vs MSCI World: 2010-2025 YTD (USD terms, indexed)

Source: Rothschild & Co, Bloomberg, MSCI

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.