Trump and the US labour market

The US labour market has been under pressure this year from Trump’s policies – and not just tariffs.

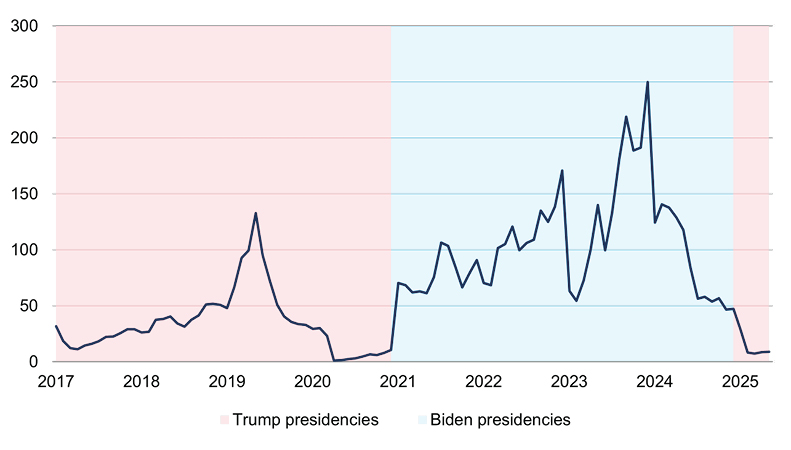

The Department of Government Efficiency (DOGE) – formerly headed by Elon Musk – attempted an early assault, firing tens of thousands of federal government workers. Stricter immigration controls were also enforced, particularly on US borders, coinciding with a sharp fall in illegal entrants (figure 1). Moreover, Immigration and Customs Enforcement (ICE) agents ramped up their deportation efforts, including controversial workplace raids. The administration has even suggested that ‘naturalized’ US citizens – those with citizenship but not through birth – may be at risk of deportation.

Could these measures produce a significant shortage of labour, and hit the economy?

Figure 1: US South West border apprehensions

Thousands

Source: Rothschild & Co, Bloomberg, US Customs and Border Protection

DOGE’s economic impact to date has actually been negligible, despite all the media attention. Efforts to reduce the size of the government were short-lived – Musk stepped back from his role after six months – and somewhat unsuccessful. Federal government payrolls only fell by 2% in the first half of 2025, and account for less than 2% of total non-farm US employment anyway. That modest decline could also reverse, as some federal agencies have reportedly been looking to rehire since Musk’s departure. Strikingly, total government jobs – which include the larger local government payroll pool, along with state-level payrolls – have actually increased through 2025.

Tighter immigration controls may have a longer shelf life, particularly after the One Big Beautiful Bill Act (OBBBA) increased funding for border and immigration enforcement. The economic impact could also be more meaningful: a recent paper from the Federal Reserve Bank of Dallas suggested that US GDP growth could be close to a percentage point lower than it otherwise might be this year due to a fall in net unauthorized immigration.

However, even if immigration stalls, there is no shortage of labour in the US: the employment-population ratio, for instance, has been much higher in the past, not so much because unemployment is high – it isn’t – but because inactivity rates have risen. Regressive measures in the OBBBA, such as cuts to Medicaid, could indeed force some inactive workers back into the labour pool. Further labour productivity gains are also possible amid ongoing AI-related progress, especially in certain services-related sectors. (Non-participation or economic inactivity is also a current talking point of course here in the UK).

Deportations arguably have the potential to do the most economic damage, with Trump reiterating this year that he will carry out the single largest mass deportation programme in US history. An analysis by PIIE last year suggested that US GDP could flatline between 2024-28 if all eight million (estimated) undocumented workers were deported over that period – a figure equivalent to roughly 5% of the total non-farm payroll. If Trump manages (as he has threatened) to extend the deportations to ‘naturalized’ citizens, which are a multiple of the prior figure, then the hit would be even greater.

That said, there are huge logistical, legal and monetary challenges when it comes to deporting illegal entrants on mass – let alone ‘naturalized’ US citizens. The ICE director reported 65,000 deportations in the first 100 days since Trump’s inauguration, which would extrapolate to a full-term figure of just under one million people. For context, the earlier PIIE analysis suggested that deporting just over a million undocumented workers – the prior record under the Eisenhower administration – would translate to a much more modest economic hit of 1% of GDP over a four-year window. The President may indeed be satisfied with those sorts of deportation figures, as he could claim an immigration-related ‘victory’ with little economic damage (not all deported persons will be in employment anyway – a point which does not appear to be taken into account in PIIE’s analysis). Finally, as with so much of his agenda, Trump’s stance may change amid voter backlash: he has already softened his tone on certain sectors which employ a high share of illegal workers, such as agriculture.

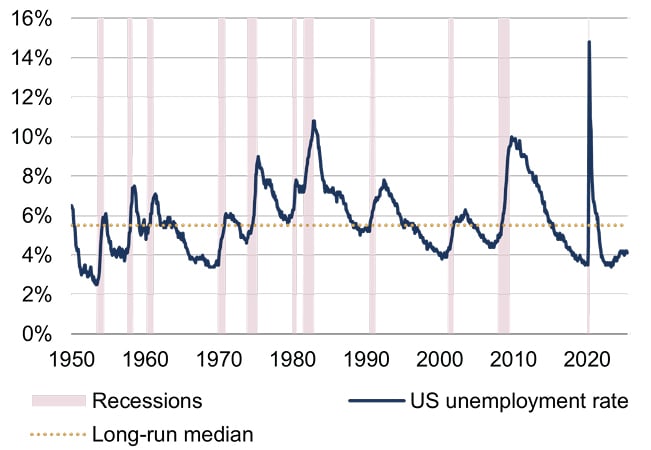

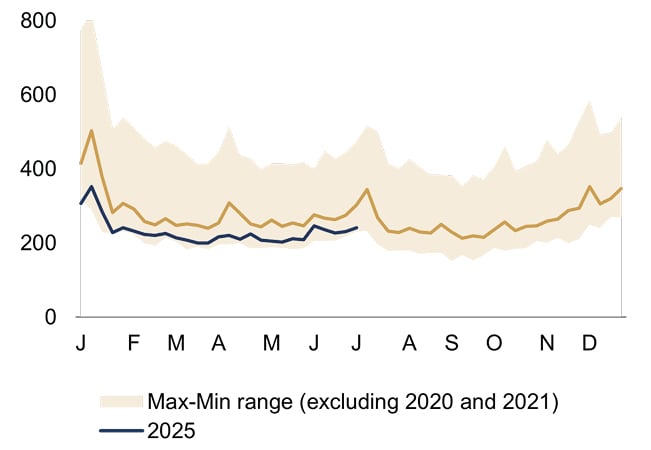

The new US administration inherited a strong labour market, and there has been little evidence to suggest that has changed since Trump’s inauguration. The US unemployment rate remains low, well below its post-war median; overall employment has stayed near record highs in absolute terms; jobs are still being created each month; jobless claims have remained subdued (figures 2 and 3).

|

Figure 2: Unemployment rate

Source: Rothschild & Co, Bloomberg, US Bureau of Labor Statistics, The National Bureau of Economic Research |

Figure 3: Initial jobless claims

Source: Rothschild & Co, Bloomberg, US Department of Labor |

We will of course be closely monitoring further policy announcements, but actions – or, in this case, the economic data – usually speak louder than words, and there are few signs yet of major labour market stress.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.