Trump Tariffs = earnings downgrades

The first-quarter US earnings season is well underway and is likely to be another solid one. Yet, rather unusually, it may be of little significance for global capital markets, given subsequent events: ‘Liberation Day’ tariffs were unveiled after the quarter ended.

As we’ve noted before, tariffs are bad for the economy and business, and at some point, they will hit bottom-line earnings – more companies will face higher input costs, and/or reduced spending power, than will benefit from any competitive boost. That said, earnings estimates do not adjust instantaneously like stock prices. Index-level forward (or predicted) earnings are compiled from thousands of analysts worldwide, and it takes time for estimates to be revised, collected and processed.

Two questions, then, spring to mind. First, how long might it take for estimates to react? And second, how big could the hit be?

Using 2020 as a parallel

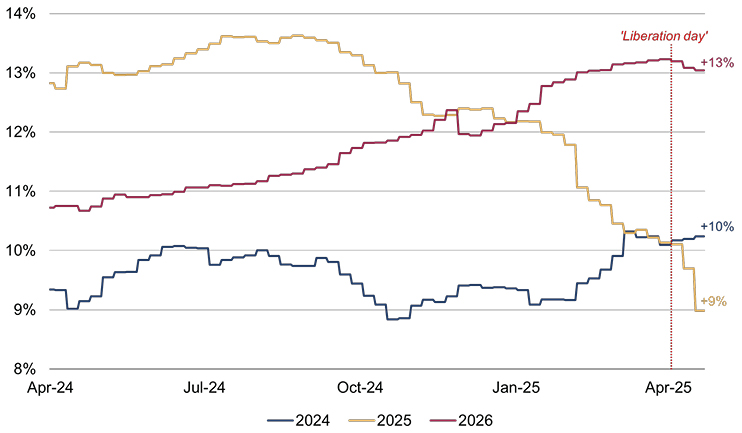

For what it’s worth, analysts were expecting another ‘above-trend’ global earnings growth rate in 2025 prior to the major tariff announcement on 2 April, according to the Institutional Brokers' Estimate System (I/B/E/S) dataset1. While punchy, these estimates were broadly realistic in our view, as the global economic backdrop also appeared robust (figure 1).

Figure 1: Global earnings growth estimates’ evolution

Calendar year estimates (%)

Source: Rothschild & Co, Datastream, I/B/E/S, MSCI

That growth rate had been falling, as the chart above shows, even prior to the big tariff announcement. That probably reflected a mix of earlier, more modest tariff announcements, and simple arithmetic: those negative revisions were associated with upgrades to the outturns for 2024 and 2026. However, 2025 earnings growth expectations have declined further since ‘Liberation Day’, without upgrades to 2026’s estimates, meaning some of that bad news has likely started to filter through.

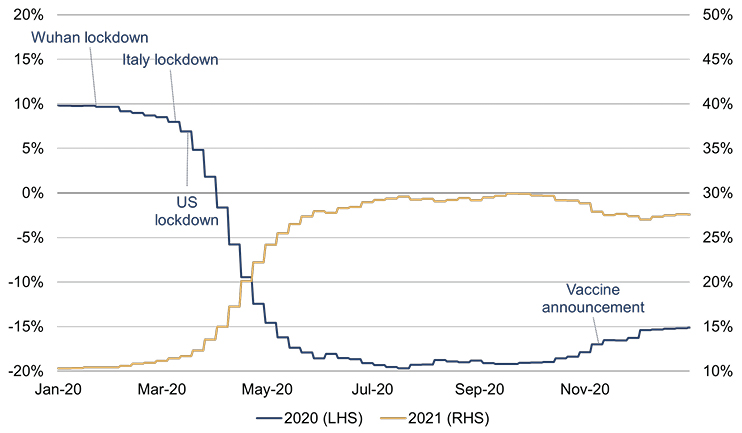

To gauge how long it may take for these analyst estimates to fully adjust, then, it may be useful to track the evolution of earnings estimates from 2020. Back then, the sudden economic news and the stock market sell-off were even more dramatic than after ‘Liberation Day’.

When the major economies announced lockdowns in March 2020, analysts’ earnings growth estimates were tracking at a trend-like pace (figure 2). By early April, those earnings growth estimates had turned negative, and by the end of the month were suggesting more than a 10% decline. Interestingly, there were upgrades to the next year’s earnings estimates during that period, but not enough to offset the 2020 downgrades.

Figure 2: Global earnings growth estimates’ evolution during 2020

Calendar year estimates (%)

Source: Rothschild & Co, Datastream, I/B/E/S, MSCI

If that episode is anything to go by – and the economic news follows a similar trajectory of course – then we could see the bulk of the adjustment to earnings estimates within a month or so. Of course, uncertainty may be more pervasive now, and it may take longer for earnings estimates to ‘settle’ than they did in 2020.

How big a hit?

This second question is more open for debate.

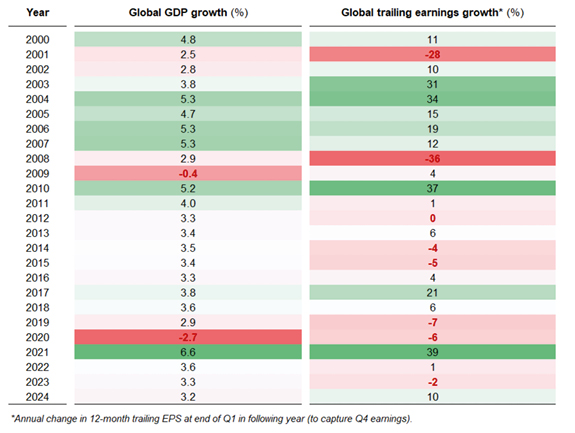

At the risk of stating the obvious, index-level earnings growth can easily turn negative during economic setbacks: a blow to total spending, incomes or production usually translates to lower corporate earnings. For example, the levels of global economic activity and earnings both fell in 2020, then rebounded in 2021, as economies respectively closed and reopened from the pandemic.

However, as figure 3 shows, the link between GDP and trailing (or actual) earnings growth outturns since 2000 has been relatively loose. Large differences in country weightings between global GDP and the MSCI All-Country World Index – the US’s weighting is around a quarter for the former, and more than 60% for the latter – may be a factor, yet the correlation between US GDP growth and corporate earnings was also similar over this period. That means other things must also influence corporate earnings.

Figure 3: Global GDP growth and trailing (actual) earnings outturns

Calendar year figures (%)

Source: Rothschild & Co, Datastream, I/B/E/S, MSCI, IMF. Note: Shading is based on each variable’s history after 2000.

For example, there was a big decline in corporate earnings in 2001, out of all proportion to any disappointment on economic growth: this was because huge asset write-downs in the aftermath of dot-com M&A excesses had a big impact on profit and loss accounts, but next to no impact on GDP. Similarly, during the Global Financial Crisis the hit to earnings was massively amplified by balance sheet write-downs at major banks and insurers. GDP also took a hit, but not until 2009, by when earnings had stabilised. In the other direction, US corporate earnings (rather than global) grew more vigorously than domestic GDP might have suggested in 2018 – after a stellar prior year – largely due to Trump’s corporate tax cuts.

Today, a trade war will impact economic growth and subsequently earnings to some extent. But recessions can vary in magnitude and length – and the jury is still out on how big a GDP hit we face. More positively, tariff revenues could eventually be recycled as tax cuts, while fiscal policy appears to be loosening in other parts of the world, most notably in Germany. A collapse in earnings is far from a done deal.

Finally, it’s worth noting that when earnings expectations are as uncertain as they are currently, price-to-earnings ratios, even – or especially – those based on forward earnings, are less reliable than usual. This is one of the reasons we favour longer-term stock valuation metrics, such as the cyclically-adjusted price-to-earnings (CAPE) ratio (which uses a 10-year trend in trailing earnings as the denominator, looking through the business cycle). Currently, the latter is suggesting the global stock index is now closer to trend – or ‘fair value’ – though not outright ‘cheap’.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Citations

[1] I/B/E/S (Institutional Brokers' Estimate System) gathers and compiles the different earnings estimates for publicly traded companies made by over 19,000 stock analysts.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.