Growth Equity Update

April 2025 – Edition 37

- Strong Q1 for growth equity raises: Our Deal Monitor indicates Q1 US venture capital deals raised $69.3bn, up 348% yoy. Europe was at $11.3bn, up 22% yoy

- US Q1- AI dominates: The US saw 15 AI related deals raising $47.1bn, 68% of the Q1 total, topped by OpenAI’s $40bn raise at the end of March. Even excluding the OpenAI deal, AI was still 24% of US deal value

- Less marked in Europe: The mix of raises was more diverse in Europe with the top five categories being Software, the still-reviving Fintech, Biotech and, in fourth place, AI. Climate Tech slipped to fifth place having led European raises in 2023 and 2024

- New World order- protectionism and the growth equity market: The ‘Liberation Day’ tariffs and subsequent market turmoil will likely adversely affect trading conditions for venture backed firms, the flow of funding into the asset class and valuation. We look at the implications

- Where did the VCs go? Andreessen Horowitz is looking to raise a $20bn fund focused on US AI companies. We ask whether AI is sucking the oxygen out from the rest of the venture market and consider how venture capitalists focus their time

- Mansion House update: The UK government’s report is due in the Spring. We look at the latest developments. Rothschild & Co is hosting a London conference on 10th June – Funding the UK Innovation Economy- Delivering on the Mansion House Compact

- "TARIFF, n. A scale of taxes on imports, designed to protect the domestic producer against the greed of his consumer." Ambrose Bierce

Click here to download a PDF version of Growth Equity Update

A strong Q1 for Growth Equity raises

2025 started strongly for the venture capital/Growth Equity market on both sides of the Atlantic

US$50.5bn of VC deal value in March and US$69.3bn in Q1, up 348% yoy: In the US March closed with 34 Venture capital raises of $100m or above, topped by the $40bn raise for OpenAI on the last day of the month. Even without this deal the US saw a seasonally strong $10bn of raises in March, with other notable raises being $3.5bn for Anthropic and $1bn for xAI.

These strong March totals rounded off a quarter of substantial growth in US venture capital fundraising. In the US to the end of March our Deal Monitor recorded 101 deals at $100m or more in the US raising a total of $69.3bn, up 348% yoy.

Q1 dominated by AI deals. There were 15 US AI related deals raising $47.1bn, 68% of the quarterly total. AI provided three of the six raises of $1bn and above. Metaverse business Infinite Reality raised $3bn. The other two substantial raises were heavily AI related. There was a raise of $1bn for social media platform X, which was subsequently absorbed by xAI. Anti-ageing biotech Retro Biosciences also raised $1bn. It is heavily backed by OpenAI’s Sam Altman who funded the entirety of the company’s previous $185m round.

The other notable sectors in Q1 were Biotech, $4.1bn raised in 18 deals and 6% of the quarterly total; Software $3.1bn raised and 4%; and cybersecurity $1.26bn and 2%.

If we extract the $40bn OpenAI deal out of the quarter’s statistics, then the fund-raising total was $29.2bn, still 89% ahead of Q1 2024. In this scenario AI is still 24% of the funding total of the quarter, but Biotech (14%), Software (11%), Metaverse (10%) and Cybersecurity (4%) become more prominent.

US- $69.3bn raised in Q1 – 3.5x the level of Q1 2024

The US – $50.5bn of US venture backed raises of $100m+ in March

Europe $3.85bn of VC deal value in March and $11.3bn in Q1, up 22% yoy: In Europe, our Deal Monitor recorded $3.85bn of venture capital raises in March, up 28% yoy. The March raises were led by $600m for AI drug developer and DeepMind spin out, Isomorphic Labs, and $521m for Swedish data centre business EcoData Centre.

The sector mix of raises is different from the US with AI having a much less prominent role. There were eight European AI deals of $20m and above in Q1 raising a total of $1.19bn including the largest deal of the quarter, the $600m raised for AI drugs discovery business Isomorphic Labs. This total meant AI was, however, only the fourth largest sector category by value of raises.

Software was the biggest sector in Q1 both by volume and value with 30 raises for a total of $1.85bn led by $200m for the travel software platform TravelPerk and $175m for the decision intelligence business, Quantexa.

Fintech sustained the revival seen towards the back end of 2024 and was narrowly in second place by both volume and value with 23 rounds raising $1.72bn. The biggest was the $500m raise by the Israeli international payments platform, Rapyd. This coincided with the finalisation of its $610m purchase of PayU from Prosus, originally announced in August 2023. The deal valued Rapyd at c$4.5bn, down from the $10bn mark the company hit at its peak in 2021.

Biotech deals remain prominent with 18 deals raising a total of $1.4bn. Verdiva Bio announced what it dubbed ‘an oversubscribed Series A’ of $411m, co-led by Forbion and General Atlantic in one of Europe’s largest ever Series A rounds. Verdiva acquired the development rights of a pipeline of assets from Chinese biotech Sciwind Biosciences in 2024. These include an oral-based – rather than the more common injection based- GLP-1 anti-obesity drug.

Notably Climate Tech deals dropped to fifth place in the value of raises in Q1 2025. It was the leading sector in 2023 and 2024. Investor appetite for larger deals in long duration, high set up cost businesses appears to have faded since mid-2024 when the difficulties at Northvolt became apparent. Nevertheless, there were some big raises about. The biggest raise in ClimateTech in Q1 was the $420m for green flexibility, a German developer of large-scale battery storage systems led by Partners Group. A complementary debt financing package meant that the total funds raised were more than €1bn.

Europe - $11.3bn raised in Q1 – 22% ahead of Q1 2024, 83% ahead of Q1 2023

Europe - $3.85bn of raises in March 2025

And more to come: Despite the public market turmoil since Liberation Day on April 2nd venture capital and growth equity markets have seen continued strong deal momentum at the start of April. In part this is because the raises are a lagging indicator of work done to attract finance in the previous 3-4 months rather than being a timely indicator of current market conditions.

The next Exhibit which shows our survey of impending raises – drawn from press reports - indicates c.$16.5bn of raises in the offing in growth equity, in the US.

Aspirant AI raises continue. AI search engine Perplexity is looking to raise $500m-$1bn at an $18bn post-money valuation. ARR is c$100m implying a multiple of 180x sales. Perplexity raised money regularly in 2024 with its most recent round being $500m in December 2024 at a valuation of $9bn led by Institutional Venture Partners and backed by Nvidia, New Enterprise Associates, B Capital, and T Rowe Price. The company's Series B round in January 2024, raised US$74m and valued Perplexity at $520m. In April 2024 it raised $250m at a $2.5bn valuation.

Cognition which has developed Devin, a generative AI coding tool designed to enhance coding efficiency by automating repetitive tasks 'the world’s first AI software engineer' is believed to be close to announcing formally a round of several hundred million dollars at a valuation of $4bn led by 8VC.

Another AI coding specialist, Replit, is looking to triple its valuation to $3bn in a $200m round.

Elon Musk’s xAI is reported to be seeking a further $10bn from investors in a round that would value the company at $75bn. Existing investors Sequoia, Andreessen Horowitz, and Valor Equity Partners are said to be considering participation.

Figure AI is an AI led robotics company producing humanoid general-purpose robots. Reuters reports that it is looking to raise $1.5bn at a valuation of $39.5bn ($38bn pre money). This valuation would be 15x the $2.6bn achieved in its $675m Series B raise in February 2024.

Thinking Machine Labs is the company founded by the former CTO of Open AI, Mira Murati. She left in September 2024 and has been joined in her new company by about twenty other former OpenAI colleagues. The nature of Thinking Machine Labs intended product is unclear. Yet the company indicates only that it intends to develop ‘more flexible, adaptable, and personalized AI systems.’ The company is reported to be looking to raise $1bn at a $9bn valuation.

You Tuber Jimmy Donaldson - known as Mr Beast to his 368 million followers - is understood to be establishing a holding company to control his various businesses which include consumer brands as well as his video production company. Press reports suggest a raise of $200m at a potential valuation of $5bn.

Forge Nano a Boulder, Colorado based materials science business involved in battery technologies is believed to be raising money in a round valuing the business at $900m. It is currently backed by GMVentures and VW.

Anysphere is an applied research lab working on automating AI coding and is the developer of the code editor, Cursor. The company is in talks to raise funding at a $10bn valuation with perennial AI investor Thrive Capital said to be leading the round. Anysphere last raised $100m funding in late December 2024 at a $2.5bn valuation.

A couple of impending raises in quantum computing. Helsinki based IQM builds and sells its full-stack Radiance superconducting quantum computers and offers quantum computing access through cloud services. In Europe, its VC counterparts are Oxford Quantum Circuits and Pascal. It is believed to be raising €200m at a valuation well ahead of that in its last raise of $128m in 2022. In the US, PsiQuantum, which uses photonics in its semiconductor manufacturing, is raising US$750m at a US$6bn pre-money valuation supported by Blackrock.

HR software business Rippling offers an all-in-one platform for HR, IT, Payroll and spend management. It raised $200m at a $13.5bn valuation in a Series F led by Coatue in April 2024. It is now said to be raising another $200m-$300m at a valuation of $16.5bn.

Growth Equity – $16.5bn reported upcoming raises

New World Order

We consider the implications of recent tariff announcements on public and private markets.

President Trump’s ‘Liberation Day’ on which he announced the US’s new ‘reciprocal’ tariff regime took place on April 2. In the run up to the event, the market had vigorously debated the potential scale of the impending tariffs. It discovered that it had underestimated the intended scope of the ‘Liberation Day’ tariffs which ranged from 10% to 46% for the top 15 trading partners of the US.

The reaction of global stock markets was immediate. In the first week after the tariff announcements the Magnificent 7 dropped by 14%, NASDAQ by 13%, the S&P500 by 12%, the FTSE 100 by 11% and the STOXX600 by 13%.

On Wednesday 9th April – after the close of markets in Europe – the US announced the suspension of the new tariff regime for 90 days and instead a blanket 10% tariff on all countries except for China. This led to an immediate equity market rally with significant one day gains. These in turn faltered as bond markets came under pressure on the 10th and 11th of April and as a tariff war tit-for-tat developed with China. By April 11th US tariffs on Chinese goods had reached 145% with China imposing tariffs of 125% on US imports. On the weekend of 12/13 April the US made a tariff exception for certain Chinese technology products including smartphones and computer equipment while stating that the exemption was potentially temporary.

The equity market has taken heart from this with much of the earlier losses being retraced. In total April 2-14, the Magnificent 7 is down 3.6%, NASDAQ by 3.7%, the S&P500 by 4.4%, the FTSE 100 by 5.5% and the STOXX 600 by 7%.

YTD to April 14 the Magnificent 7 is down 16%, NASDAQ by 12%, the S&P500 by 7.6%, the FTSE 100 by 1.6% and the STOXX600 by 2.1%.

Notably the tariff announcements and sense of uncertainty on policy direction has led to marked weakness in the dollar – down 5.4% against sterling and 9% against the € ytd.

Impact of tariff announcements - Performance of major indices

Events, dear boy, events. Asked by a reporter what was most likely to blow his government off course former British Prime Minister Harold Macmillan replied ‘Events, dear boy, events.’

Accepting that further events may yet change the picture we can make some generic assertions about what has been underlying the moves in markets and how these might affect public and private businesses.

Uncertainty: Markets and businesses dislike uncertainty. Since the start of the year and even prior to Liberation Day, the US had already imposed, suspended, and reimposed tariffs on Canada and Japan. It imposed a new tariff regime on all its trading partners on Liberation Day and then largely suspended it. It has escalated a tariff war with China and then partly retreated.

In the meantime, the US has suspended and then restored arms shipments to Ukraine, expressed its lack of interest in being a backstop for Ukrainian security guarantees and has urged Europe to pick up the slack in terms of additional defence spending. The US has declared ambitions over the territories of allies including Greenland (Denmark) and Canada as well as over the Panama Canal.

Currencies have whipsawed around with the overall trend being the dollar weakening against major currencies and a strengthening in the Euro and sterling.

The suddenness and apparent volatility of decision-making leads to further uncertainty. The level of unpredictability makes business planning very difficult. It encourages companies to pause major decisions on spending projects and initiatives. It causes companies to postpone ordering, to stockpile critical components and in some cases to preserve cash. This is negative to economic activity. A leading CEO of a global business described the situation to us - ‘What a mess.’

Inflationary: Goods imported to the US become more expensive as tariffs are raised. There is not the immediate option to substitute all imported goods with US sourced products. Certain products (bananas is a classic example) will probably never be substitutable within the US. Put simply, the effect of tariffs is inflationary. To gauge the inflationary impact the imposition of the 145% tariff on Chinese imports to the US on its own is estimated to add 67bps to US inflation. Based on current US inflation rates - pre-tariffs- of 2.8%, the imposition of these tariffs on Chinese goods alone would take inflation to 3.5%.

Consumer slowdown: Uncertainty and rising inflation will necessarily have a negative effect on US consumers. Consumer confidence had already been deteriorating ahead of the tariff announcements with the Conference Board index hitting a four-year low in March.

The Conference Board commented in March that ‘Consumers’ expectations were especially gloomy, with pessimism about future business conditions deepening and confidence about future employment prospects falling to a 12-year low. Meanwhile, consumers’ optimism about future income—which had held up quite strongly in the past few months—largely vanished, suggesting worries about the economy and labour market have started to spread into consumers’ assessments of their personal situations.’

The University of Michigan’s consumer sentiment survey published in mid-March saw one year ahead inflation expectations rise to 4.9%, the highest since November 2022. In its updated survey published on April 11 (fieldwork between March 25 and April 8 – before the tariff suspension), consumer sentiment fell 11% to a preliminary reading of 50.8, the second-lowest reading on records going back to 1952. The survey’s director said that ‘This decline was… pervasive and unanimous across age, income, education, geographic region, and political affiliation.'

Former Treasury Secretary Lawrence Summers, stated post Liberation Day that it’s “more likely than not” tariffs cause a US recession, adding that it would potentially lead to an extra two million unemployed in the US (versus 7.1 million unemployed at end March) and a $5,000 or greater decline in annual household income.

The tariff announcements, volatile stock markets, rising prices, business disruption and greater fear of unemployment are all factors that risk hitting consumer confidence further.

Index of US consumer sentiment – April (University of Michigan)

Fed interest rate cuts shelved or accelerated? Prior to Liberation Day, the market had been anticipating two more interest rate cuts in 2025 in line with the official Fed dot plot. The official line from the Fed in March was that tariffs had not yet had an impact and were not factored into the current thinking with Fed Chairman Jay Powell saying that on policy decisions the Fed will ‘patiently watch and understand and see how it plays out’.

The administration is pressing for the Fed to cut rates. The President has stated that ‘Oil prices are down, interest rates are down (the slow-moving Fed should cut rates!), food prices are down, there is NO INFLATION.’

The Fed has two areas of focus in its rate setting – inflation and the employment figures. It now faces a conundrum. Typically impending rising inflation would be a deterrent to cutting interest rates. A tariff induced economic slowdown has the opposite effect – it should encourage the Fed to cut.

Christopher Waller, a Fed Governor, has said that if the Liberation Day tariffs were reimposed the Fed might have to carry out a series of ‘bad news’ rate cuts’ saying ‘If the slowdown is significant and even threatens a recession, then I would expect to favour cutting the policy rate sooner, and to a greater extent than I had thought’.

The market took heart from this and appears to be pencilling in two to three rate cuts by the year end. To cut rates to offset a recession seems less optimal than rate cuts in response to falling inflation. The next Fed meeting is on May 6th.

Dollar weakness: Unusually for a period of perceived financial crisis, the US is not being seen as a safe haven and the dollar has weakened against major currencies. This has the unfortunate effect of making imports into the US yet more expensive. In turn this exacerbates the impact on US consumers and US businesses reliant on imported materials and finished goods. It is also likely to have a negative impact on the margins of UK and European business exporting to the US.

Earnings downgrades: The natural consequence of all this will be falling demand for discretionary goods and services, a slowdown in activity in financial markets, stresses on supply chains and the reining in by businesses of discretionary expenditures. This will progressively lead to earnings downgrades.

Initially the Q1 results season, reporting the period to the end of March, will see earnings largely unscathed (the period is pre the blanket tariffs) and perhaps guidance maintained (too soon to gauge the effect). Companies though, facing unpredictable but deteriorating trading conditions, are likely to produce cautious forward commentary to reflect the uncertainty. In fact, we have already seen some capital goods companies reporting early and negatively in response a slowdown in order activity in the last couple of weeks in March as tariff uncertainty increased.

By Q2 – reported in mid- late July - the downgrades will start to come in and Q3 will see the effect fully underway - with companies running out of road to make their 2025 guidance. This promises months of negative earnings revisions.

Cost of borrowing rises: Tariffs have the potential to weigh heavily on companies’ input costs and margins. The cost of debt will become more expensive for more affected companies and those with higher leverage. There will be increased pressure on corporate balance sheets and credit ratings. Companies may respond with cost cutting- which in turn hits labour markets and other corporates’ profitability. Banks will come under pressure with loan books scrutinised for signs of weakness. The cost of debt will thus rise, most notably for more leveraged companies but with short term financing costs rising across the board. In turn this has implications for investment and M&A.

‘Trumpcession’: We noted in our last Growth Equity Update that the Atlanta Fed’s GDP Now model had predicted that US GDP in Q1 would contract by 2.8%, a shift from earlier forecasts of +2.3% and giving rise to fears of ‘Trumpcession’. At heart, the impact of the US’s flirtation with a new tariff regime is to risk the likelihood of shifting the US into recession with a negative impact on global growth as well.

A survey of 46 economists carried out by Wolters Kluwer Blue Chip Economic Indicators (after Liberation Day but before the April 9th suspension of the new tariff regime for most countries) estimated a 47% chance of US recession, up from 25% in February.

On April 9th - pre the tariff regime suspension - Blackrock CEO Larry Fink stated that ‘Most CEOs I talk to would say we are probably in a recession right now- The reality is 62 percent of Americans now invest in equities — the market impact is impacting Main Street. This is going to freeze more and more consumption; I think we’re going to start seeing that really quickly.'

Even after the suspension he commented 'I think you’re going to see, across the board, just a slowdown until there’s more certainty. And we now have a 90-day pause on the reciprocal tariffs — that means longer, more elevated uncertainty.’

Also, on April 9 pre-suspension JPMorgan Chase CEO Jamie Dimon stated a tariff induced recession is a 'likely outcome'. He noted 'recessionary talk' amongst CEOs to whom he had spoken.

Speaking at the Goldman Sachs results on April 14 its CEO David Solomon said that the new trade policies from the Trump administration 'reset the prospect of forward growth pretty significantly all over the world' and that the prospect of a recession 'has increased'.

Stock market effects: A real-world slowdown, whose barometer is the equity markets, will also see some market related effects which in turn may feed the sense of deterioration.

- One of the factors supporting the advances of the US stock market has been the reinforcing effect of share buybacks. A natural consequence of deteriorating conditions is a desire to adopt a conservative approach and reduce leverage – discouraging companies from returning as much cash to shareholders.

- Financial blow ups amongst market participants. Sudden swings in markets tend to reveal structural weaknesses in the financial sector, as the demise of Long-Term Capital Management in 1998 revealed. Sudden market volatility tends to find out structural weaknesses in the market and its participants.

- One of the phenomena we saw in 2021 was the impact of falling public markets on private holdings. Many funds are limited in the percentage of their funds that they can own in private assets. As public valuations fall, while private valuations remain unchanged awaiting their next mark, this drives up the percentage of a fund’s holdings held in private assets reducing or removing the headroom for further allocation to privates.

We repeat this excellent summary from Rothschild & Co strategists Kevin Gardiner and Anthony Abrahamian highlighting the potential impacts of some of the Trump administration’s initiatives:

Trumponomics - An overview of the headline policies

The impact on Growth equity

The FTSE Venture Capital Index which measures the performance of the US venture capital industry, with a strong sector weighting towards technology, was in early February up 10% ytd at 22,477 just 6% off its highs of August 2021. It is now down 12.5% ytd.

Deal announcements remain robust for now: Most growth rounds are the result of several months work and so the short term trend in these announcements is not a reflection of tariff affected conditions For what it is worth the week ended April 11 was a decent one for US raises with five deals of over $100m with the largest deal being at $200m. April 14 saw Alphabet and Nvidia invest in AI business Safe Superintelligence at a valuation of $32bn.

It will be more interesting to see the progress on the $65bn of impending raises across 14 deals that had been reported as being in the offing prior to Liberation Day. Progress on completion of these deals will be a good gauge of continued private market activity post the tariff uncertainty.

Liquidity issues: The turmoil in markets has led to the postponement of several planned IPOs in the US. General partners remain under pressure to provide liquidity to limited partners. The IPO markets have already been functioning at a low level for the last three years amid a weak overall environment for exits. There had been hopes for a reopening of IPO markets in 2025 as well as a revival in M&A led exits. Post the market disruption around tariffs the IPO market has swung firmly shut once more while the rising cost of debt is a potential obstacle to M&A led exits. Without the liquidity produced by active levels of exits the ability to raise and reinvest in new growth equity funded companies is reduced.

Secondary market weaker: The same liquidity issues are likely to affect valuations in the secondary market. With the routes to IPO and M&A exit blocked there is likely to be a growing demand to exit via the secondary market. In turn that means that the discounts at which companies trade in the secondary market will widen – reversing the strength seen in secondary market prices in the last year.

Pressure on fundraising and valuation: It is an almost inevitable consequence of the volatility in the public markets that investment levels and valuations in the private markets will be adversely impacted. Venture and growth investors will assume that the ramifications of the tariff uncertainties will hit venture backed companies as they would public companies and that the effect on these smaller, arguably more vulnerable businesses-often reliant on a narrower range of customers and with less financial flexibility than their larger peers – may be greater.

Investors will reduce their revenue growth assumptions for VC backed companies and push back expectations of the timing of profitability. In turn this will lead them reassess the amount of funding a company might require reaching break-even. This will affect both the decision on whether to make fresh investment and the valuation that they are prepared to pay. Processes are likely to take longer.

VC advice to venture backed companies: Faced with revenue uncertainty and with extra funding likely to be more difficult to obtain, the advice of VCs to their investee companies is likely to follow a familiar route. The guidance will be to adopt a conservative approach, to focus on the core business, to restrain costs, preserve cash and to plot a route to free cash flow break even. Many VC backed companies have already been on this path since 2021. The corollary of lower revenue growth though tends to be lower valuations in the next funding round.

Where did the Venture capitalists go?

"AI is a transformative force that makes these companies better. The way to think about it is ‘can these businesses reasonably grow 10x from where they are?’ The answer with all of these is yes, so they are reasonably priced.” Hemant Taneja, chief executive General Catalyst- March 2025

The statistics for Q1 show that 74% of US venture capital/growth equity investment in Q1 2025 went to AI companies. Even stripping out the $40bn OpenAI deal the industry saw 24% of funds raised for AI. We have heard from some companies in other industries who are in the US looking for funding that they feel crowded out by AI – that investors are interested in little else.

As Kyle Stanford, Pitchbook’s director of American venture research comments ‘The U.S. market has become very bifurcated between a handful of companies able to raise an endless amount of money and the rest of the market, which continues to struggle through a capital shortage.’

Really, this should come as no surprise. As far back as 1998 Bob Zider, founder of the Berta Group, wrote an illuminating article in the Harvard Business Review, ‘How Venture Capital Works’. One of his key messages was to emphasise that venture capitalists aim not to invest in individuals but rather that they aim to invest in the best emerging industries. He writes:

‘One myth is that venture capitalists invest in good people and good ideas. The reality is that they invest in good industries—that is, industries that are more competitively forgiving than the market. In 1980, for example, nearly 20% of venture capital investments went to the energy industry. More recently, the flow of capital has shifted rapidly from genetic engineering, specialty retailing, and computer hardware to CD-ROMs, multimedia, telecommunications, and software companies. Now, more than 25% of disbursements are devoted to the internet space. The apparent randomness of these shifts among technologies and industry segments is misleading; the targeted segment in each case was growing fast, and its capacity promised to be constrained in the next five years. To put this in context, we estimate that less than 10% of all U.S. economic activity occurs in segments projected to grow more than 15% a year over the next five years.

Growing within high-growth segments is a lot easier than doing so in low-, no-, or negative-growth ones, as every businessperson knows. In other words, regardless of the talent or charisma of individual entrepreneurs, they rarely receive backing from a VC if their businesses are in low-growth market segments. What these investment flows reflect, then, is a consistent pattern of capital allocation into industries where most companies are likely to look good in the near term.’

In the current context the revolutionary nature and explosive growth of artificial intelligence is naturally attracting venture capital investors.

At the start of April Andreessen Horowitz revealed it is seeking to raise about $20bn for what would be its largest ever fund to be dedicated to growth-stage investments in AI companies and targeting global investors keen on investing in American companies.

We are continuing to see large sums devoted to backing the leaders in large language models. We are also seeing the spread of backing for a range of AI inference businesses- the apps of artificial intelligence – often smaller businesses offering an opportunity for VC firms outside the largest to participate in industry growth.

This is not to say that founders and the executive team in a VC backed business are not important. We have already seen some notable examples of controversy in the AI industry with startup companies being accused of over inflated sales and capability claims. Strong execution remains key.

We know also that venture capitalists are driven by the VC power law where the majority of the returns in a venture capital fund are made by a tiny proportion of the investments. VenCap has analysed more than 200 early-stage venture funds raised between 1995 and 2015 with funds invested in more than 9,000 portfolio companies. The return distribution of these 9,000 plus companies is shown in the chart.

More than 60% of these investments generated a negative return for their investors. Just under 5% of companies generated 10x cost or higher. The ultimate prize is a ‘fund returner’ - an investment that returns more than 100% of the total capital of the investing fund. Only 0.9% - or c80 companies out of the 9,000- achieved this status.

The VC Power Law

Top 1% of exits by volume produce c50% of total exit value of VC investments

To make up for the very high percentage of underperforming company investments the VC industry requires the relatively few successful companies to generate significantly outsized returns for their investors. Over the last decade, the top 1% of VC-backed exits have generated c50% of the total exit value created by the venture capital industry globally.

Back to Bob Zider in the Harvard Business Review. He describes the process of why the prospect of success is so proportionately low in startup companies.

Having invested in areas with high growth rates, VCs are then placing their risks with the ability of the company’s management to execute. Even with a good industry and strong management, the chances of failure of a young startup company are high given the prospects of its success are limited by the need to be successful across a range of critical factors.

Even with an 80% probability of success within each of eight critical factors, the overall prospect of success of the venture is reduced to just 17%. If just one of the variables drops to a 50% probability, the combined chance of success falls to 10%.

Early-stage companies – the prospect of success

In the meantime, venture capitalists are making their returns in c5-6% of the companies in which they invest. The mix of investment performance in turn explains how venture capitalists spend their time.

There is a bell curve effect. At one extreme there are the relatively few, best companies – well positioned, well run and highly successful. These require monitoring but little time on active intervention. The worst performing companies – and these might eventually be 60% of the total – receive no additional money and time.

Instead, the VC allocates significant time to the portfolio companies in the middle, assessing whether and how the investment can be turned around and whether to continue to fund it.

In the meantime, venture capitalists have a lot else to do. They need to identify and attract new deals, monitor existing deals, allocate additional capital to the most successful deals, and deal with exit options.

Here’s Bob Zider’s analysis of how VCs generically spend their time. Though time has moved on, this breakdown may not have changed much. If we assume that a partner in a VC firm is looking after 10 companies and works 12 hours a day for 50 weeks (3,000 hours) of the year with 40% of that time spent with portfolio companies then that allows 120 hours per year per company—less than 2.5 hours per week.

How venture capitalists spend their time

Although perhaps AI itself will help. As Douglas Laney of Forbes observes ‘We're not far from a world in which AI agents play the role of chief-of-staff, triaging the deluge of pitch decks and launch announcements that hit VC inboxes each day to help investors prioritize which founders to meet.’

Meanwhile the incentive for a VC to look beyond the most attractive growth industries where there are a plethora of opportunities becomes much less. Faced with burgeoning opportunity in AI – particularly in the US – the focus of VCs on this industry to the apparent exclusion of others is explained.

Sources: ‘How Venture Capital Works’ Harvard Business Review - Bob Zider;

Venn Capital The Mansion House Reforms – What pension funds need to know before building a Venture Capital investment programme: here

Venture Funds – More substantial AI focused fund raising

In the midst of the tariff turmoil Reuters reported on April 8th that Andreessen Horowitz (a16z) is looking to raise a $20bn fund focused on US AI companies. The fund will be designed to give global investors the opportunity to invest in growth stage investments in US AI businesses.

The fund would be substantial both in the context of a16z and other venture capital funds in the market. For a sense of scale a16z currently has $45bn of assets under management with its single largest fund being a $5bn growth fund raised in 2022. The largest current VC funds are the SoftBank Vision 1 and 2 Funds (respectively $100bn and $55bn) and the c$56bn run by Sequoia.

The Reuters report suggests that a substantial part of the capital raised would be earmarked for follow on investments in existing portfolio companies. These include Open AI, xAI, Safe SuperIntelligence, Mistral and Databricks.

Unsurprisingly, it is suggested that the proposed fundraising will take some months to complete. It will be interesting to see the level of international appetite for this US based fund given the apparent cooling towards US assets by some international investors seen as a result of the recent US tariff initiatives.

Largest VC funds raised since 2014

On a smaller scale and focused on earlier stage businesses, venture capital firm SignalFire has just completed a $1bn fund raise. The funding will be devoted to seed to Series B investments in applied AI. The founder and CEO of SignalFire Chris Farmer commented:

‘Our investors see what we see — applied AI is the defining opportunity of our time. With this new capital, we’re doubling down on the next generation of category-defining AI startups tackling the world’s biggest challenges.’

Hitherto SignalFire has invested in applied AI companies like Grow Therapy, EvenUp, Stampli, Horizon3.ai, and Grammarly.

SignalFire emphasises its use of AI techniques in its portfolio management process with the firm’s Beacon AI platform being ‘a proprietary machine learning platform powered by talent data’ tracking over 650m employees and 80m organisations.'

Mansion House Update

Rothschild & Co is hosting an event Funding the UK Innovation Economy: Delivering on the Mansion House Compact on Tuesday 10 June 2025 in London.

Summer 2025 will mark the second anniversary of the Mansion House Compact. At its heart is an agreement signed by ten of the UK's largest pension providers to commit 5% of their 'default' funds from defined contribution pensions to private companies, initiatives, and start-ups by 2030. It is hoped that this will unlock £50bn of new funding for UK based businesses in science, technology and innovation further developing the UK's growth company ecosystem and providing a boost to highly skilled jobs and economic growth.

Rothschild & Co is hosting this event to bring together senior level policy makers, pension fund allocators, regulators, UK venture and growth investors and UK based innovation businesses. We will discuss progress towards achieving the 5% target, the barriers which still exist, and the UK sectors with sustainable competitive advantage best placed to benefit from this new capital.

The background to the Mansion House reforms was covered in the March Growth Equity update (Growth Equity Update - March 2025). The final report of the pensions investment review is due in the Spring.

A couple of recent developments worthy of note:

UK pensions minister Thorsten Bell gave an interview to the FT in mid-March. He stressed that the government is encouraging a wide spread of pension funds to invest more in private markets telling the FT that he is in “very active discussions” with managers of defined contribution schemes to invest more in private assets - “encouraging investing in a wider range of assets, not instigating….. Every percentage point matters when this investment can deliver not only returns for savers but also contribute to economic growth.’’

Mr Bell also confirmed that he would hold England and Wales’s £392bn public pension scheme to a deadline of March 2026 to pool all its assets into vehicles regulated by the Financial Conduct Authority.

The ten DC pension schemes signed up to the ‘Mansion House Compact,’ representing around two-thirds of the UK’s DC workplace market, are Aviva, Scottish Widows, L&G, Aegon, Phoenix, Nest, Smart Pension, M&G, Aon, and Mercer. At present such funds invest just c0.5% of their c$500bn of assets in unlisted UK companies.

Amongst the signatories Nest has an unusually high private market exposure of c17%. Of this c8% is invested in infrastructure and private equity, c6% in UK property and 3% cent in private credit, including loans to small companies. It targets taking this exposure up to 30% over the next five years.

This month though the CIO of Nest, Liz Fernando, stressed in an interview to the FT that this target is ‘an ambition, not a guarantee. We’ll do it if the opportunities arise… We want to maintain the tension of making sure we are buying great assets at good prices and have no interest in just shoving money out of the door to hit a target.'

If you would like an invitation to the Funding the UK Innovation Economy: Delivering on the Mansion House Compact event on June 10 please contact Tim Brenton or Patrick Wellington.

Our views on the state of the venture capital markets

The combination of global inflation, rising interest rates, and increased geopolitical risk impacted the venture capital market in 2022 and 2023. 2024 saw some adaptation to the ‘new normal’. The refocusing of venture backed companies to achieve a better balance of growth, profitability and cash flow and the delivery of interest rate cuts has led to increased optimism and enthusiasm for growth equity. Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment led to a sharp impact on valuations in private markets. The scale of the fall in the FTSE Venture Capital Index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023 and slow recovery in 2024.

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, semiconductors) supporting the development of AI.

- Enthusiasm for AI and related technologies drove the overall level of the FTSE Venture Capital Index in February 2025 back to within 6% of its highs of August 2021.

- Outside the AI space the VC market is selectively regaining confidence with a revival of interest in fintech, biotech and software being notable. Certain investors remain very active in the space with substantial funds to deploy. There remains substantial dry powder in the VC industry.

- The speed of the investment process has slowed since 2021-22. The level of diligence on new deals has stepped up.

- 2023 and 2024 saw more downrounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these.

- Recent initiatives by the US to impose tariffs on its trading partners are likely to impact US and global economic growth and to negatively affect the fund-raising environment for venture backed companies.

- It seems that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses.

- Valuation priorities have shifted with investors having moved away from an emphasis on revenue growth and revenue multiple emphasis. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and an emphasis on DCF and comparative based multiples.

Read the previous editions:

May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024, January 2025, February 2025, March 2025

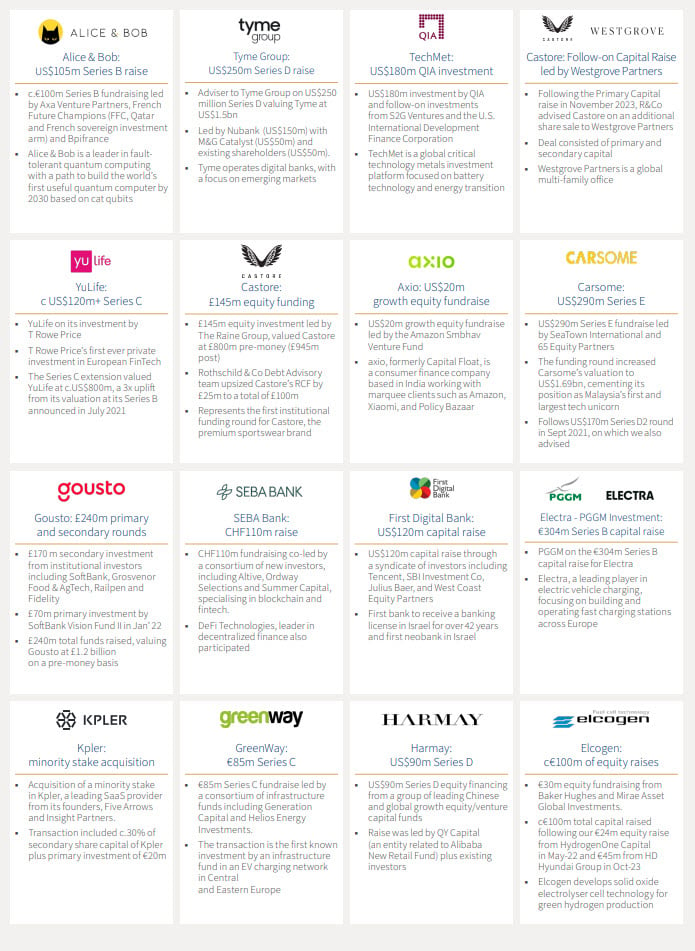

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Chris Hawley

Global Head of Private Capital

chris.hawley@rothschildandco.com

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Advisory

patrick.wellington@rothschildandco.com

+44 20 7280 5088

+44 7542 477 291

Thomas Chung

Head of Private Capital, North America

thomas.chung@rothschildandco.com

+1 212 403 5559

+1 917 594 7208

Mark Connelly

Head of North American Equity Markets Solutions

mark.connelly@rothschildandco.com

+1 212 403 5500

+1 917 297 5131

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.