Taking stock: a macro update

The latest spike in trade tensions and the return of the dreaded r-word reminds us how quickly optimism turns to caution. What was once fertile has now turned rather more febrile: Monday’s uncomfortable sell-off continued yesterday, with signs of a modest rebound today. To last night’s close, global stocks are down c.7% from their mid-February high, while the tech-heavy Nasdaq is down 13%. Meanwhile, the VIX index hit its highest level in 7 months.

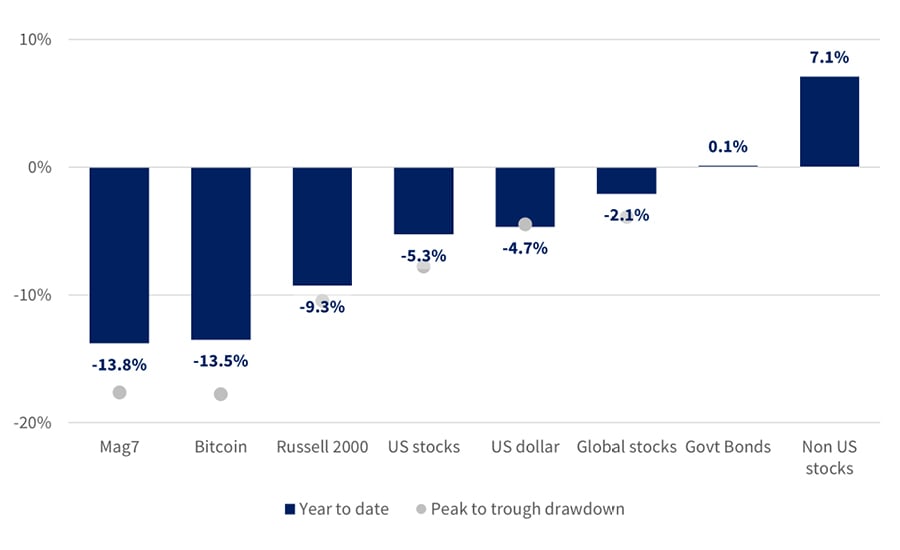

Selected cross-asset returns (USD terms)

Source: Rothschild & Co, Bloomberg. Correct to 11th March 2025

So where has Goldilocks gone?

It wasn’t long ago that risk assets were riding high on the reflationary promise of Trump 2.0, which was set to unshackle the US from an alleged tax and regulatory straitjacket. While we were never convinced about either the diagnosis or the cure, and had turned a little more cautious on stocks in the weeks that followed the election (though not just because of Trump-related uncertainty), MAGA-euphoria has certainly faded. Those assets with a perception of closeness to Trump increasingly look like damaged goods: Teslas are about as fashionable as fur coats, and crypto turmoil reminds us that Bitcoin is not a hedge against anything.

From our top-down perspective, we are not especially surprised by these developments: global stock markets are close to where they were in early November. Trump’s unpredictability is perhaps his most reliable feature, while US stocks have been expensive and interest rates are not the one-way bet many investors have assumed. A tactical retreat, or at least a pause for breath, has arguably been on the cards.

Trump’s gestures and actions should not be trivialised: they can affect the economy and stocks quickly and visibly. But they can be just as quickly reversed. New steel and aluminium duties come into effect today; but for how long, and what of the retaliation? Meanwhile, many other components of the protectionist 'strategy' remain unclear. Is it about action, or deterrence? Exactly what levels, products, countries are to be covered? Who will ultimately pay, US consumers or overseas suppliers? Will retaliation and escalation be exponential or more considered?

Measures implemented to date, if sustained, may not be large enough directly to turn US growth into recession. Our reading of the economic data is that while growth is slowing, it is not collapsing. The modest hit to consumption in the first quarter has largely been on account of the temporary impact of bad weather and wildfires. Surging imports – to avoid later tariff hikes – hit the growth arithmetic, but are not the stuff of which a sustained downturn is made (especially if many of those imports are, as reported, of gold). As yet, there is little sign of a decisive downturn in the labour market – despite DOGE-related layoffs.

As for the stock market’s reversal, Trump’s aggressive policies have clearly dented sentiment, but not yet comprehensively: there has been no big, sinister fall in bond yields. Similarly, few investors have sought refuge in the safety of the dollar or gold over the past month. In Europe, of course, bond yields have actually been moving higher as Trump has convinced leaders there to spend more on longer-term defence, while his outrageous comments on Ukraine seem if anything to have raised the chances of a short-term ceasefire.

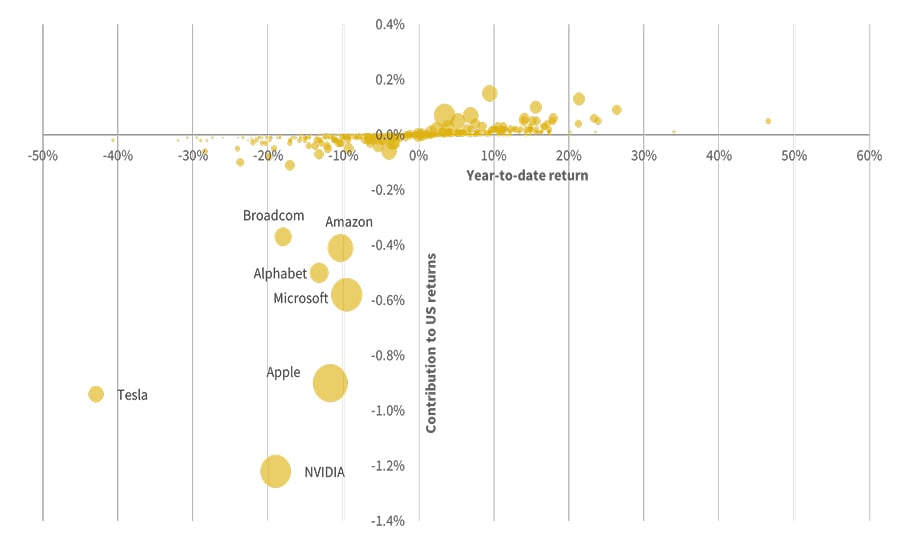

Meanwhile, recent volatility has arguably also come at a time when stock market leadership was ripe for a change. Since the start of the year there has been a big rotation away from the US and its increasingly jittery ‘technology’ stocks - again, it is those megacap stocks which remain in the driving seat. While a little over half of US stocks are down this year, the ten biggest detractors account for the entirety of the five-percentage point decline in the S&P 500 index in 2025. The demise of the Magnificent Seven et al – is a potent reminder that nothing grows to the sky – not even the fabled AI stocks.

US stock returns vs contribution: year-to-date

Bubble size scaled by market capitalisation

Source: Rothschild & Co, Bloomberg. Correct to 11th March 2025

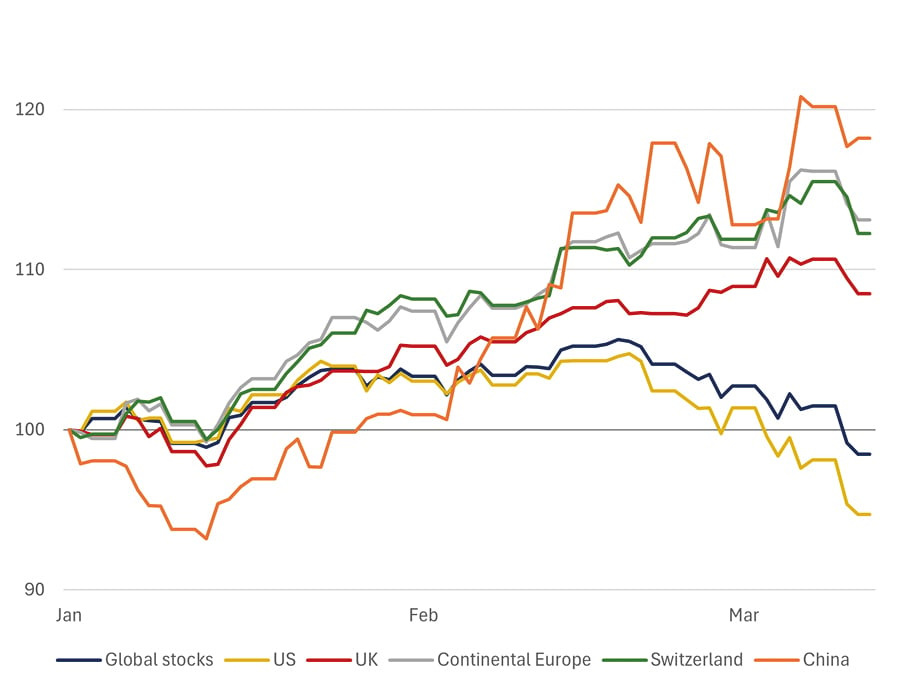

Nonetheless, this reappraisal has been to the benefit of other regions and sectors, many of which have been trending higher. Switzerland, Europe and China are pulling ahead - partly flattered by dollar weakness when viewed in common currency terms - with more defensive and value-tilted segments outperforming their cyclical and growth counterparts.

US exceptionalism may have run far enough for the time being.

Selected regional stock market returns: year-to-date

(indexed, USD terms)

Source: Rothschild & Co, Bloomberg, MSCI. Correct to 11th March 2025

Sitting tight

We have often argued that politics matters less than the business cycle to markets – the outlook for profits and interest rates is often affected more by routine business trends than by the White House. But it is of course entirely possible that a wider trade war does take hold, and a more protracted slowdown ensues. If so, sentiment could drive a wider sell-off.

For now, however, we remain in the cautious 'wait and see' mode we entered back in November. The risks are not all one-sided. As noted, here in Europe a temporary cessation of hostilities in Ukraine is reportedly pending; Germany is belatedly getting ready to spend more, and on infrastructure, not just defence; and surveys seem to suggest that European animal spirits have bottomed. If corporate profits continue to hold up – and broaden - there may be room for further rotation ahead.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.