China: sentiment turns a corner

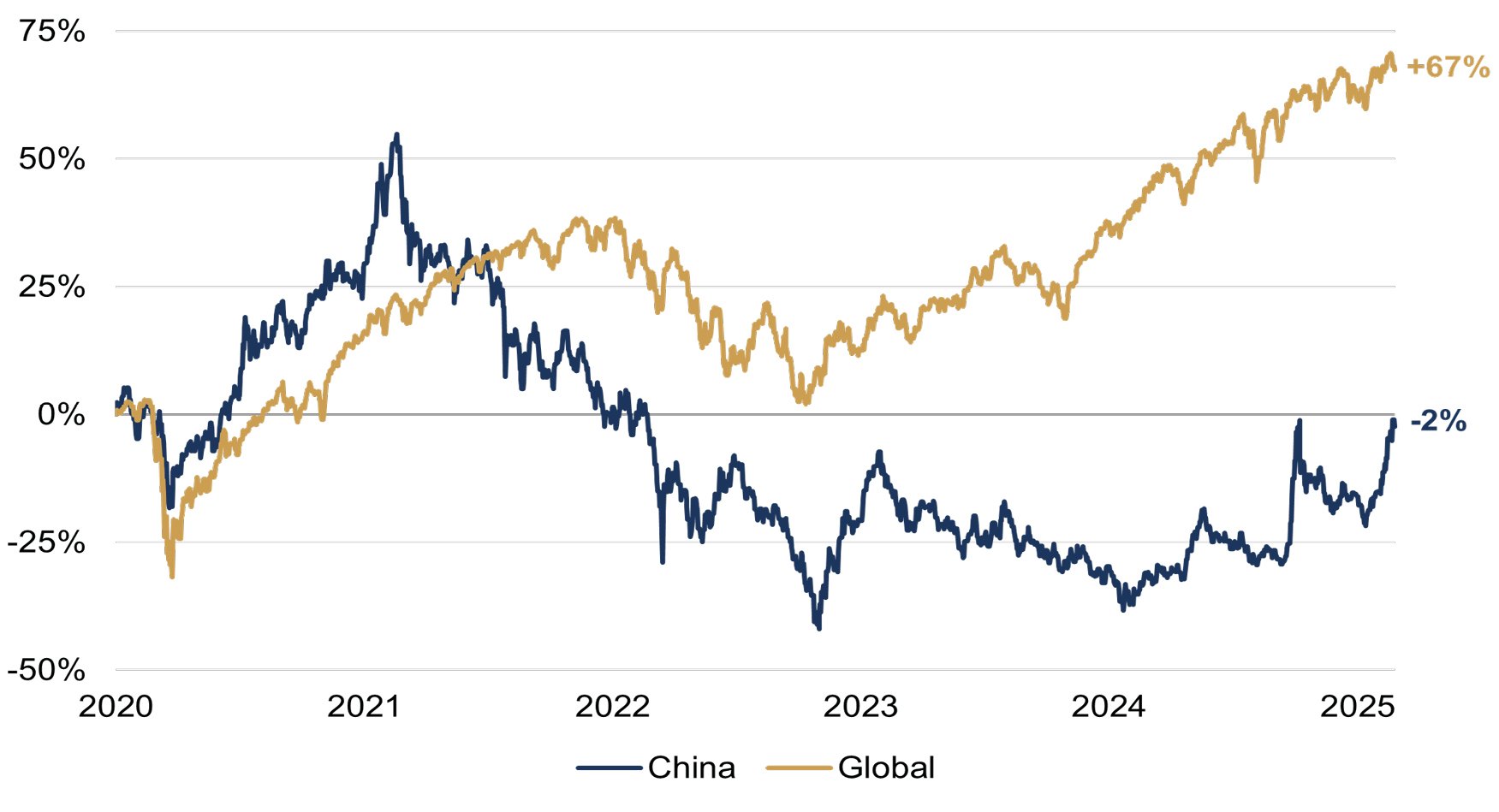

MSCI China has been one of the best performing stock indices this year, surging 16% in US dollar terms and testing its October 2024 high (though it remains two-fifths lower than its all-time peak in 2021). ‘Technology-like’ stocks have outperformed after the news earlier this month of cost-efficient AI models from DeepSeek and other local start-ups.

However, we have seen several false dawns here of late. For example, the end of Covid-related restrictions in late 2022 triggered a 60% rally followed by a renewed and prolonged 35% drawdown. More recently, the unexpected government stimulus package in late 2024 saw a (almost) two-fifths spike in the index in less than a month, only for it then to fall back by one fifth.

As noted, after all this volatility, the MSCI China index is still well below its all-time high in early 2021, and flat since the start of 2020 (figure 1). Meanwhile, the global stock index has risen by almost 70%, with few significant reversals. So what do we expect of China’s stock market from here?

Figure 1: China and global stock market returns

Total returns since the start of 2020 (%, USD terms)

Source: Rothschild & Co, Bloomberg, MSCI

A respectable economic backdrop

By Western standards, China’s macroeconomic backdrop has been robust over this period. Real GDP grew by 5% in 2024, in line with the government’s target, and economists predict a similarly strong 2025. Commentators have talked of ‘Japanification’, following a recent flirtation with deflation, but the economy is obviously not stagnating (unlike Japan’s did in the 1990s).

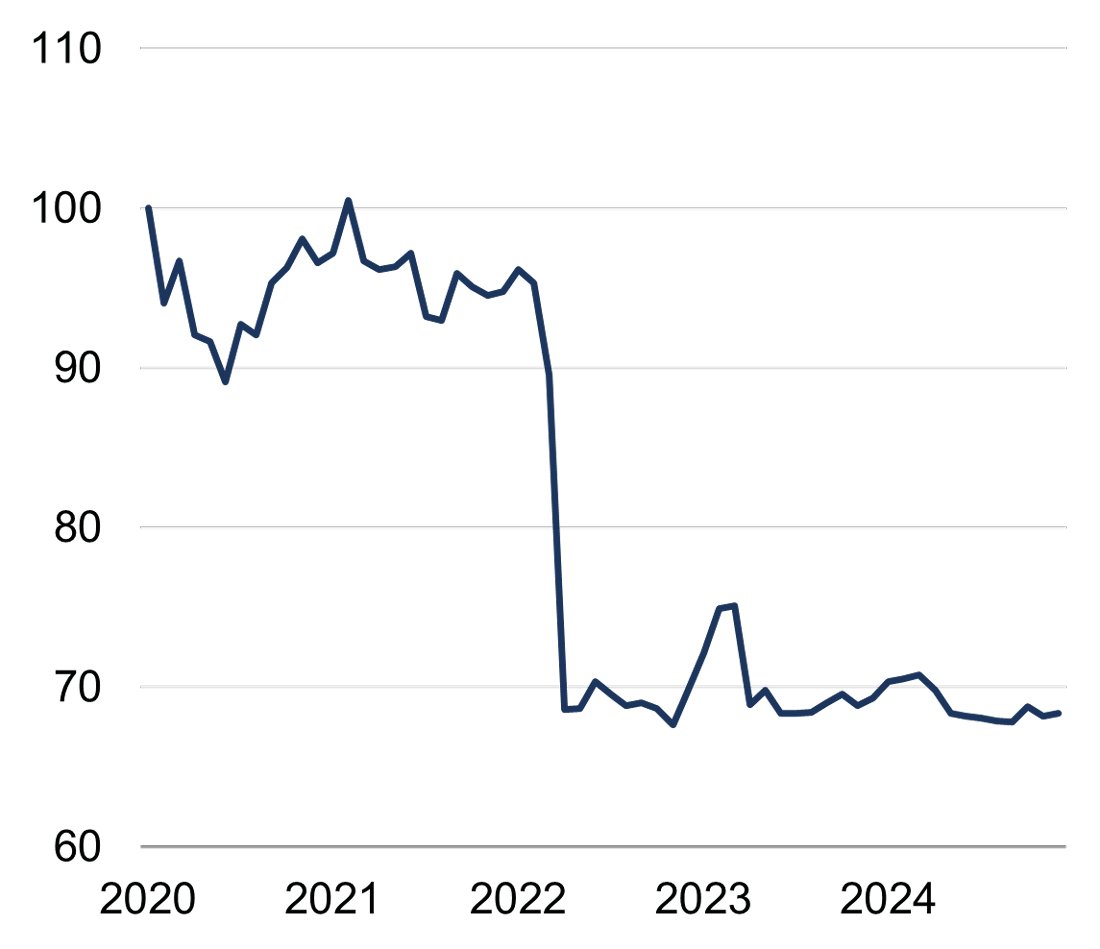

It has admittedly been tricky to assess China’s economy since the turn of the year. The Lunar New Year holidays lead to some important data being delayed, with figures for January and February together not being published until March. Of the available indicators, there was a slight uptick in core CPI inflation in January. Indeed, a rebound in consumer spending would be welcome as it weakened during 2024. Consumer confidence has been at historically depressed levels, with plenty of room to revive (figure 2).

|

Figure 2: China consumer confidence index

Source: Rothschild & Co, Bloomberg, National Bureau of Statistics of China |

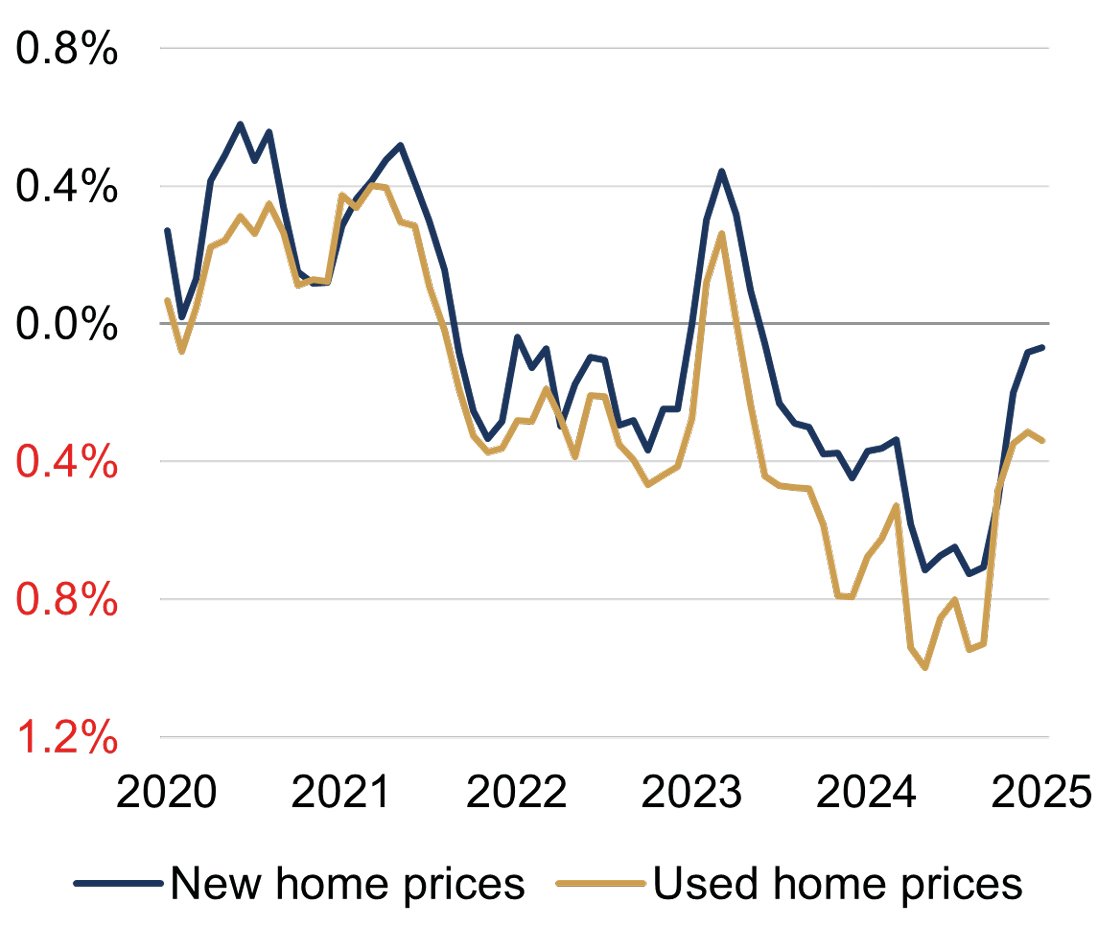

Figure 3: China house prices

Source: Rothschild & Co, Bloomberg |

The big fall in confidence came with renewed government-imposed lockdowns in 2022, but property sector issues have doubtless helped keep it subdued. China has one of the highest home ownership rates globally, and many households have experienced big losses in recent years: residential property prices have been falling since 2021 (figure 3), while balance sheet issues have spread to state-owned property developers such as Vanke.

The worst of this distress may nonetheless be behind us: the pace of house price declines has slowed, and the authorities have ramped up monetary and fiscal support, stating that ‘boosting household consumption’ is their top economic objective for 2025. A bottoming out of the property downturn may well boost consumer sentiment and spending.

The tariff threat

That said, someone on the other side of the Pacific may spoil the party.

Donald Trump has swiftly ordered a 10% additional tariff on all imports from China, while encouraging other countries – such as Mexico – to do the same. Beijing has retaliated with its own set of tariffs on US goods, prompting fears of another trade war.

A full-blown conflict would of course hit Chinese growth – and profitability – as the US is its number one customer, but much would depend on the scale, duration and coverage of the tariffs. (We should keep in mind that China is itself the most protected big economy to begin with: arguably Trump has a point, even if he expresses it in an aggressive way).

As yet, the measures have actually been more lenient than feared. In his election campaign, Trump had signalled a China tariff closer to 60%, and he has already hinted that a deal could be struck, just as with the ‘Phase One’ agreement at the end of his first term.

Moreover, proposed tariffs are often avoided. They can be rescinded in negotiation, importers can misreport the origins of their suppliers, and China’s exports can be redirected through other EM Asia countries – all of which happened to some extent during Trump’s first presidency.

A bigger geopolitical risk to growth in our view comes from China’s non-negotiable claim on Taiwan. But an escalation of tensions here – perhaps leading to sanctions or worse – would make a big dent in China’s economic well-being (and the rest of the world’s, of course), which is why we think President Xi may remain patient. Another consideration is the growing reality that Taiwan’s current market-leading semiconductor capabilities might not survive a change in political ownership – the US and others are already looking to establish alternative supplies, though it will take years to achieve scale.

A not so profitable market

It may face problems, then, most notably in its real estate sector and that potential trade threat, but China’s economic growth remains relatively healthy. But even after its recent rebound, as noted, the local stock market has underperformed significantly in the post-pandemic world.

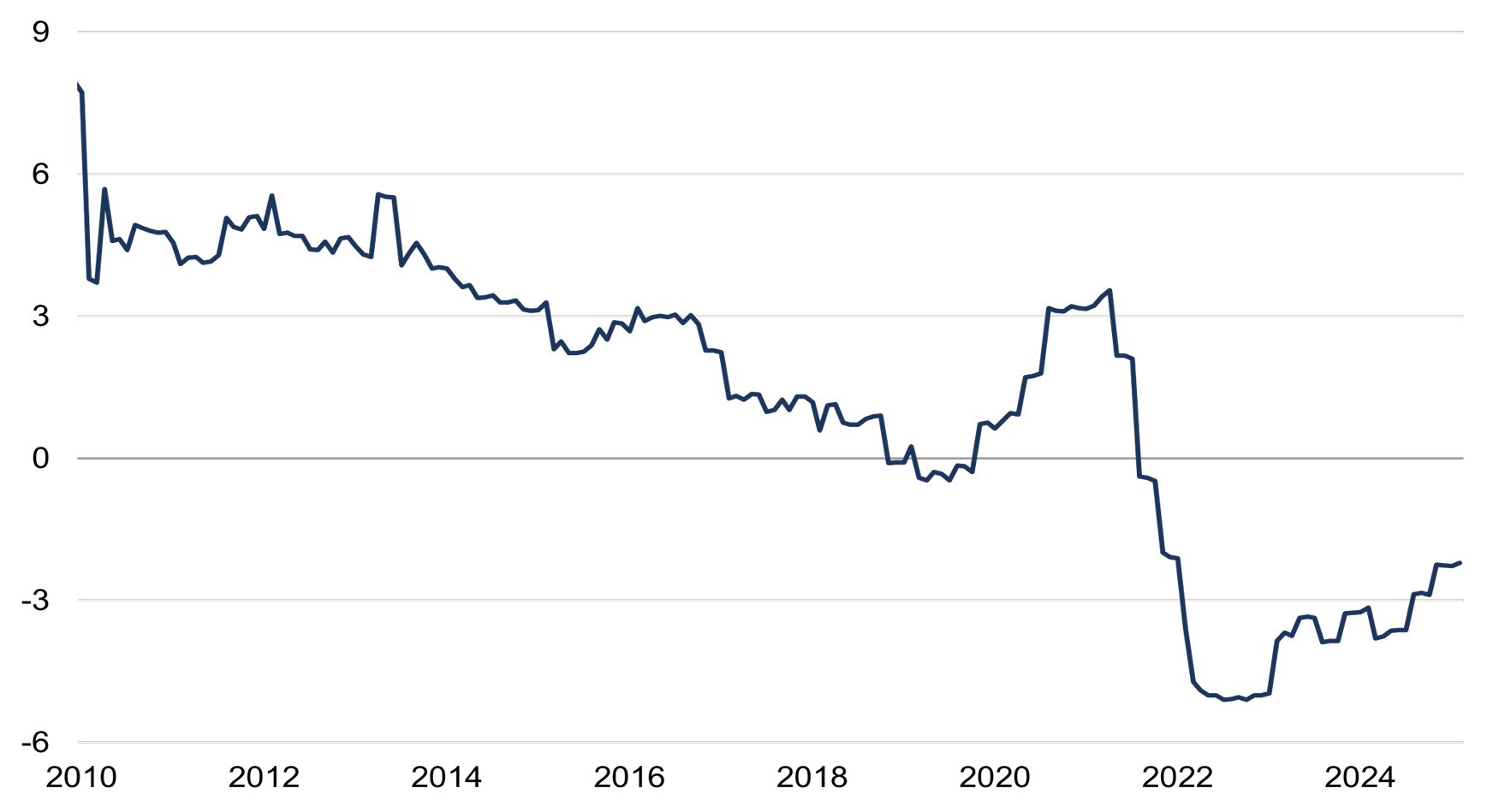

This has partly reflected the government’s increasingly heavy-handed interventions in business. Return on equity (RoE) – a gauge of profitability – has indeed trended lower on a relative basis over the past fifteen years, with a sharp decline around the time when Xi began his ‘common prosperity’ crackdowns, and it is now below the global RoE (figure 4).

Figure 4: Return on equity (RoE) gap between China and global stocks

Percentage points

Source: Rothschild & Co, Bloomberg, MSCI

More recently, the RoE gap has started to improve, and there are tentative signs that the government’s ‘visible hand’ of state capitalism may be wavering. A week or so ago, President Xi held a meeting with the largest ‘technology’ company executives, including Alibaba’s Jack Ma (who had disappeared from the public gaze a few years ago). This development, coupled with the reported local breakthroughs in large language AI models, could maybe spark a resurgence in profitability.

If the worst is avoided on tariffs, further government fiscal support is forthcoming, and the real estate market continues to settle, China’s stock market could look more enticing: even after the latest bounce, MSCI China is trading on a forward price-earnings ratio of just 11x (global: 18x). China is of course part of the broader EM Asia region, which we continue to see as strategically attractive on account of its ongoing dynamism.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.