Bundestagswahl 2025: The Grand Coalition?

Germany’s snap election on 23 February is fast looming, and change is afoot.

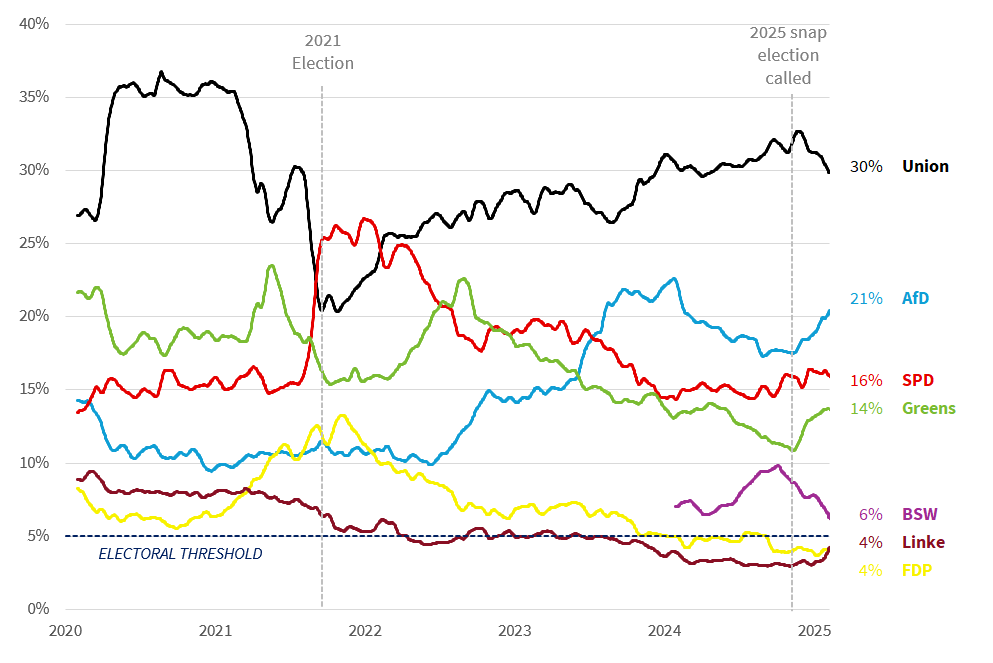

The incumbent Chancellor, the SPD’s Olaf Scholz, faces a big challenge. Friedrich Merz and the Union (comprising the centre-right CDU and CSU) are nine points ahead of their nearest rival, the far-right AfD. With no party set to secure an outright majority – as is customary in the post-war Republic – the most likely scenario seems to be a return to a ‘Grand Coalition’ (of sorts) between the conservative Union and the centre-left SPD.

Opinion polls (%)

Source: Rothschild & Co, Bloomberg, Kantar, Forsa, INSA-Meinungstrend, YouGov, Infratest Dimap/ARD

Note: Reflects 15-day moving average of five key national opinion polls. Limited data for BSW, which reflects a single poll.

However, this looks set to be an unpredictable and highly contested poll. Alternative coalitions are possible, but not necessarily viable – or palatable to many voters. Muddled policies and divergent spending plans plagued the failed ‘traffic light’ coalition – which comprised the SPD, the FDP and the Greens. Two years of infighting culminated in the coalition’s eventual collapse in November, necessitating this early election

The polls are still shifting – the Union has been losing momentum at the expense of the AfD. And there is uncertainty about which parties will surpass the 5% electoral threshold and how this will impact the re-allocated seats in the Bundestag. The liberal FDP, for example, which would be most aligned with the Union, may find itself excluded altogether.

There are myriad issues facing Germany and its electorate – economic, societal, environmental, and now foreign policy challenges, with a bellicose President Trump back in the frame. Not all, of course, are unique to Germany.

Economic concerns at the forefront

Perhaps the most pressing is the stagnant economy, the source of much domestic unease. Output has fallen slightly in two consecutive years, weighed down by increasing competition (particularly in the important auto sector, which is also grappling with the shift to EVs), high energy costs and energy insecurity, and a protracted global manufacturing standstill. German unemployment has been steadily rising (albeit from low levels) and confidence is depressed.

Merz has put economic reform at the centre of his election pitch. He is seeking to restore Germany’s competitiveness, de-emphasise climate objectives, and pursue new foreign policy goals with the aim of increasing defence spending. However, he remains committed to Germany’s traditionally prudent stance on government borrowing, the so-called fiscal debt brake (‘Schuldenbremse’). This position could put him at odds with a potential coalition partner, the SPD, which has been more open to reform (fiscal disagreements were a key factor of the governing coalition’s November collapse, with the Scholz government seeking to borrow more).

However, Merz’s strategy has not been without controversy. He recently failed to significantly tighten Germany’s migration policies – possibly contravening European law – in a bid to ‘triangulate’ to the right. In the process, he not only antagonised many in his party (and his base), but he also upended a long-standing policy of not cooperating with the AfD – which was only too eager to support the motion.

The AfD’s rise: a growing challenge

The AfD has yet to ally itself with any of the major parties – the so-called ‘firewall’ remains intact, for now. But its rise is daunting, not just in the opinion polls but also in making significant gains in various State elections. While ‘Dexit’ – ‘Deutschland Exit’ from the eurozone - is not a serious aim for the AfD, the party’s nationalist ambitions are clear. It has been successful in capitalising on growing frustration with the economy, climate policies, and thorny societal challenges, such as immigration. Merz’s contentious willingness to engage with far-right leaders such as the AfD’s Alice Weidel, arguably gives further impetus to the populist pendulum. While the AfD is yet to play a role in a federal government, by 24 February, it will likely become the second-biggest party in the Bundestag.

Whatever coalition forms – Grand or motley – Germany in reality has plenty of fiscal headroom (arguably, more than any other large economy) if they can overcome the legislative hurdles. Urgent and dramatic reforms may not be as necessary as the public debate currently seems to assume, but inaction on spending, and/or a reluctance to address some of the structural concerns identified recently by the Commission’s Draghi report, may only serve to strengthen the AfD’s hand in the longer term.

In the meantime, as investors we usually view German stocks – which have been performing strongly of late - and bonds as part of a wider view about Europe. On this count we are currently neither especially positive nor negative from a top-down perspective. Often, despite domestic concerns, the prospects for the region and Germany depend more on what happens to world trade, particularly in Asia - Germany is a big exporter. While we are optimistic that growth there can revive, in the short-term of course it is hostage to developments in and around the White House – something beyond the control of any coalition in the Bundestag.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.