Corporate earnings growth broadening?

The third-quarter US earnings season has crept up on us, beginning with the major banks on Friday.

Analysts are expecting a fifth consecutive quarter of year-on-year earnings growth for the market as a whole, albeit at a more modest rate of 4.2%¹ (after Q2’s 11%). Momentum is expected to persist through next year, broadening to other regions and sectors, which seems plausible to us.

America leads the charge

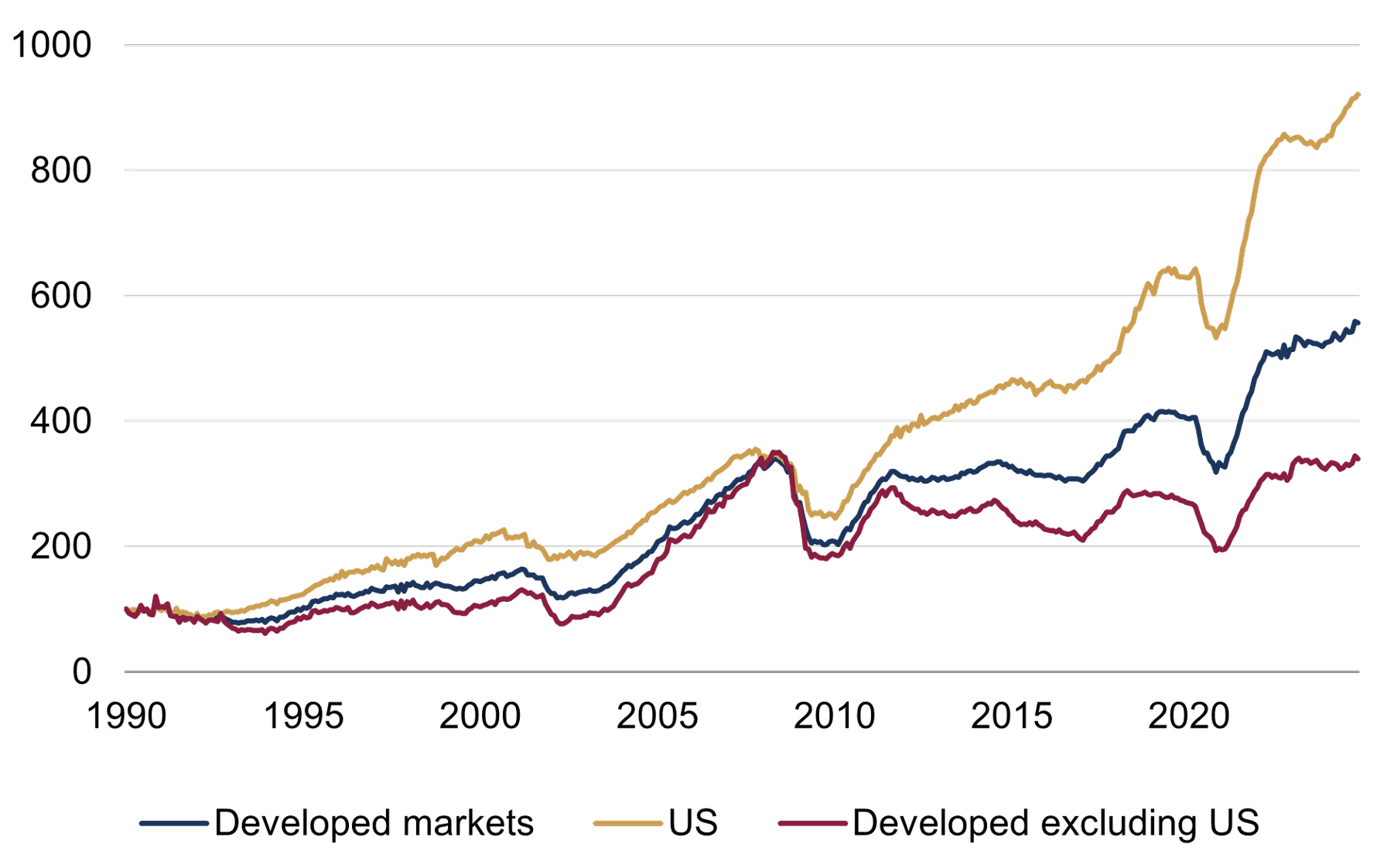

From a global investment standpoint, the US earnings trajectory matters most: its share of global earnings has grown considerably relative to its developed-market peers, particularly after the global financial crisis, and the world’s most valuable companies are listed there. Meanwhile, the 12-month trailing earnings profile for the other major developed markets has been roughly flat over the past two decades, and is yet to return to its 2008 high in nominal US dollar terms (figure 1).

Figure 1: Trailing (actual) earnings per share

Rebased series (100 = January 1990, USD terms)

Source: Rothschild & Co, Datastream, I/B/E/S, MSCI

Since 2020, however, continental Europe – whose historic earnings have lagged due to their greater exposure to slower growing and less profitable ‘value’ sectors – have surprisingly kept pace with the US in dollar terms. In other developed regions, the UK (greater exposure to commodity-producing sectors and almost no technology), and Japan (not a conventionally capitalist or earnings-focused economy), have seen their trailing earnings rise by half as much during that period.

Earnings growth to continue – and broaden?

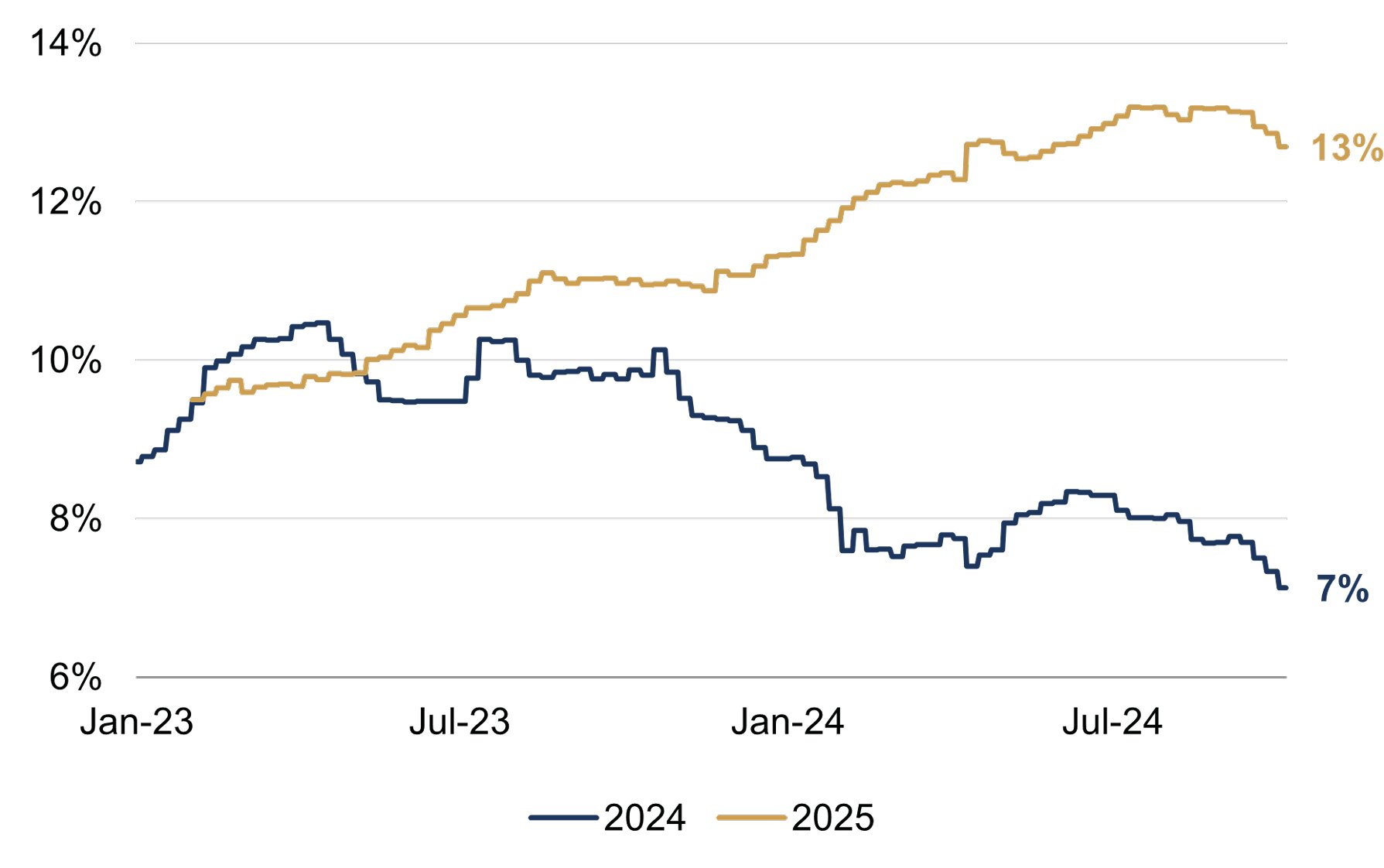

Overall, developed-market earnings are expected to grow by around 7% this year² (figure 2). While analysts have downgraded their annual estimate over the course of this year, it is still in line with its pre-pandemic (2010-19) trend growth rate – and certainly an improvement from its flat profile in 2023.

Figure 2: Developed market earnings per share growth estimates

Annual estimate evolution (%)

Source: Rothschild & Co, Datastream, I/B/E/S, MSCI

Next year’s estimates are eye-catching, with earnings growth expected to accelerate to 13% (figure 2). The US is predicted to continue to lead, with an above-trend earnings growth rate of 15%. Within the US, earnings growth is expected to broaden from the mega-cap ‘Magnificent Seven’ cohort³ to other non-technology sectors (the former have contributed significantly to year-over-year earnings growth in the first half of this year).

Analysts are also anticipating broad-based gains across other developed market regions next year. Developed-market earnings excluding the US are forecast to grow by 9%, almost double its 2010-19 average growth rate.

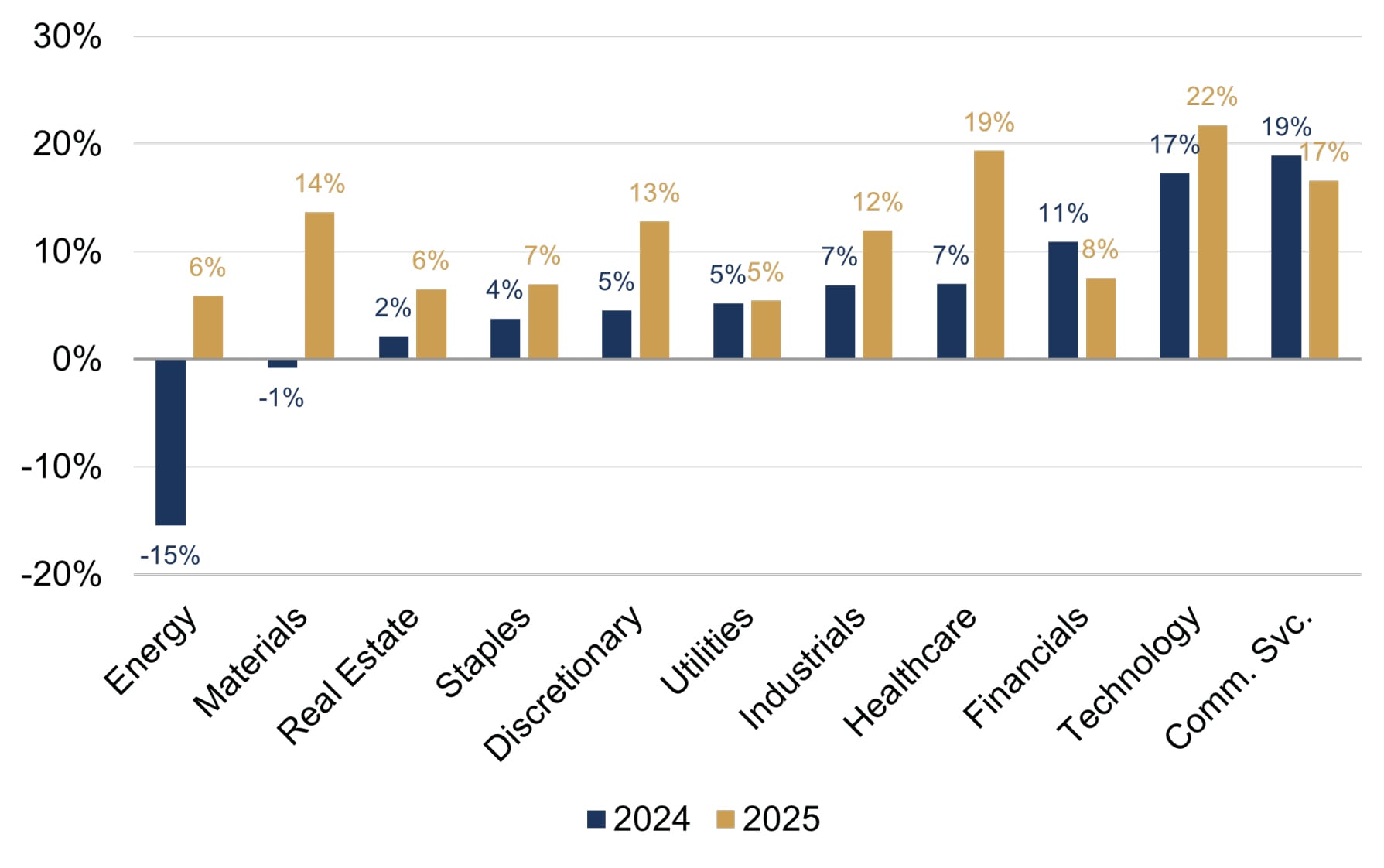

In fact, most sectors’ earnings growth rates are expected to accelerate in 2025 (figure 3). The technology sector is forecast to have the strongest earnings growth rate – perhaps unsurprising given the US observation noted above – followed closely by healthcare and communication services, which are also viewed as ‘growth’ style sectors.

Figure 3: Developed market sectors’ earnings per share growth estimates

Annual estimates (%)

Source: Rothschild & Co, Datastream, I/B/E/S, MSCI

Are analysts overly optimistic?

Of course, earnings expectations are fallible – a lot can happen over the course of a year – and there has historically been a tendency for analysts to overestimate earnings, according to this dataset at least. Still, even if analyst forecasts are revised a few percentage points lower, earnings would grow at a respectable pace. And analysts’ overly-optimistic track record has not noticeably restrained the stock market’s long-term advance.

More fundamentally, we don’t expect interest rates to fall quite as much as market pricing through 2025, and so if that scenario does play out, analysts may temper their estimates. Even so, we see few signs of a looming downturn – the big risk to earnings – and ‘higher for longer’ interest rates may not matter so much if economic resilience persists. As we see it, rates will be ‘higher for longer’ because that resilience may persist.

As we have often said, corporate profitability is the main driver of long-term stock market returns. But earnings are important in the near term, too: arguably the valuation re-rating which has driven the stock market rebound since the start of 2023 has been anticipating them.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Citations

[1] Quarterly S&P 500 earnings data is from FactSet.

[2] The IBES dataset compiles different projections made by thousands of stock-market analysts on the future earnings for publicly-traded companies.

[3] The ‘Magnificent Seven’ include Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.