China: down, but not out

It seems enough is enough for Beijing’s policymakers. After a series of half measures in recent years, the government and central bank have announced with a multi-pronged attempt to stimulate the market and revive the sluggish economy. China’s onshore ‘A shares’ market, where sentiment has been chronically depressed for some time, has responded vigorously, surging a quarter over the past week.

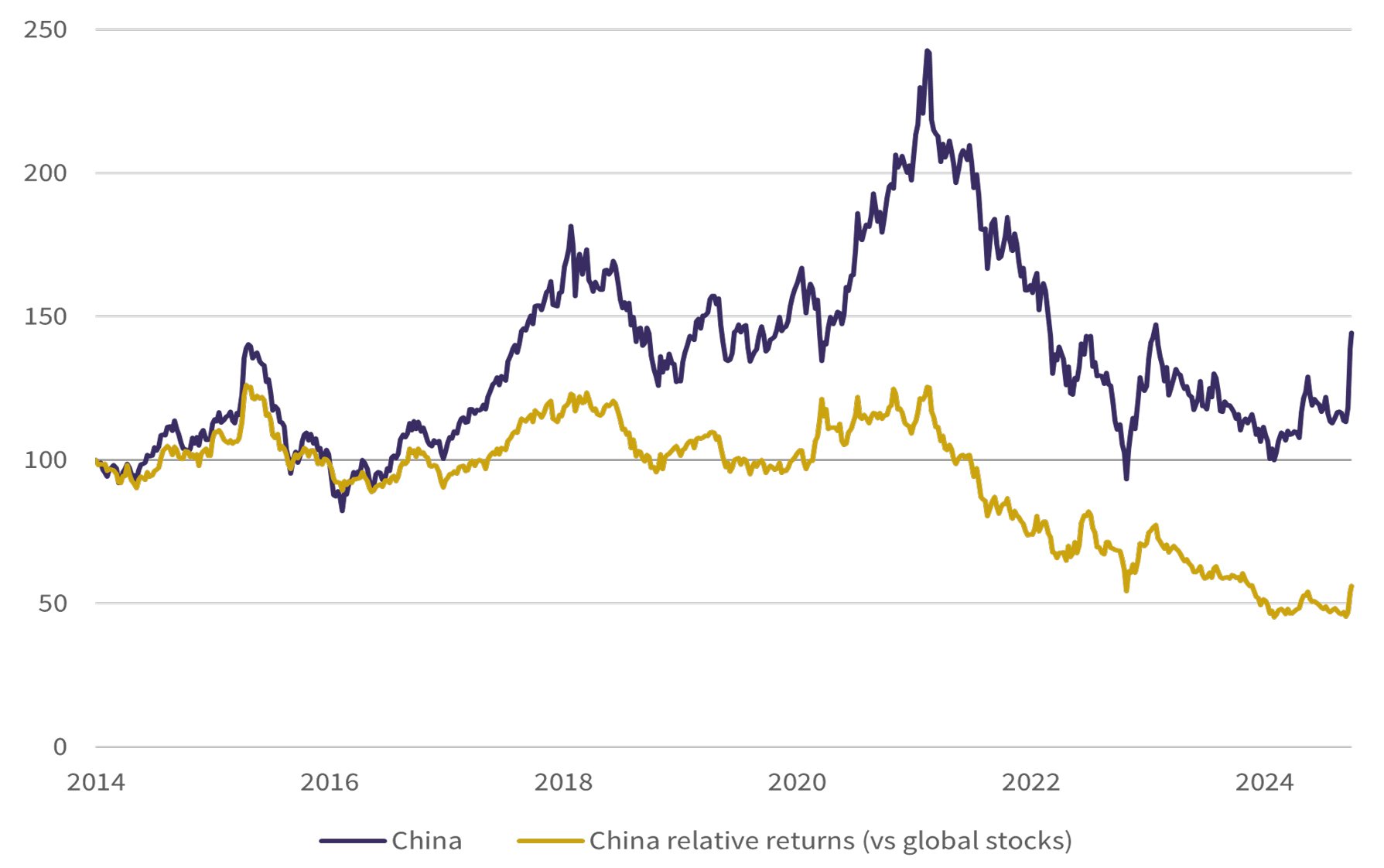

China’s stock market: the last 10 years

Total returns, indexed (in US dollar terms): 1 Jan 2014 to 30 Sep 2024

Source: Rothschild & Co, Bloomberg, MSCI

Past performance is not a reliable indicator of future performance.

Is this enough to make overseas investors reconsider what many have seen as China’s ‘uninvestable’ status?

The measures: ‘Stop the decline’

China’s stimulus barrage includes a number of fiscal and monetary policy measures – most of which are centred around reviving the enfeebled property sector.

Most prominently, the central bank, the People's Bank of China, has delivered a significant easing package – at least by China’s standards. Not only in cutting the core policy rate by an outsized 0.2 percentage points to 1.5% (and in turn the medium-term facility rate), but by also announcing a reduction in the required reserve ratio that stipulates what level of capital banks must hold. In theory, this could translate to more lending and lower mortgage rates. In addition, they’ve also reduced the deposit needed to buy a second home. Beyond the property sector, there was explicit support for the equity market, which includes a new lending facility to enable companies to buy back their own stock, as well as a swap facility for institutional investors.

On the fiscal side, China’s Politburo – the 24-man committee in charge of governing - has until now been reticent to intervene. But sluggish activity data – with China’s 5% growth target now looking increasingly ambitious – alongside looming deflation risks may have finally spurred them into action. Beijing has now committed to further spending to stabilise the property sector and offer support directly to households. While the exact size – and nature – of the stimulus package is yet to be unveiled, one figure being mooted suggested it might be in the order of RMB 1-2tn – a not insubstantial 1-2% of GDP. Other measures include attempts to constrain new developments, while supporting the long tail of unfinished (and some yet to be developed) residential projects.

Unresolved challenges

There’s no doubt that it’s been an uncomfortable and disappointing few years for China: a property market downturn, a manufacturing slump and more recently rising unemployment.

China has always had ample fiscal and monetary headroom to support the economy should it need to. These latest stimulus measures are broad and perhaps the most decisive we have seen in recent years. To Beijing’s credit, it has at least temporarily revived market expectations. And it is possible this latest stimulus may yet stem – possibly even reverse – the downturn in the property sector, and in turn, revive that relatively depressed cyclical picture.

However, we do not (yet) fully share the market’s seemingly unbridled enthusiasm. Even if these (unspecified) stimulus measures revive the cyclical story, they do little to resolve the bigger – and unanswered – structural challenges. Beijing appears to be reverting to type – prioritising short-term growth over sectoral weaknesses. While demand-side measures to support the property market may lift economic confidence in the near-term, it fails to address the structural oversupply that still exists. The reality is that some businesses and sectors still have too much debt, despite the defaults and restructurings in recent years. Policies designed to prop-up over-leveraged quasi state-owned enterprises will hamper productivity and long-term growth.

While the systemic risks are likely manageable, as we’ve noted before, it does challenge the notion that China is able to wean itself from its investment and infrastructure-led growth, towards something that is more sustainable.

As for the long-awaited revival in the stock market, it remains unconvincing. Arguably, the stock market rout in recent years is more attributable to the increasingly authoritarian government and its various interventions, than it is about sluggish domestic growth (which is of course still relatively strong by western standards). The ‘visible hand’ of state capitalism has eroded nascent shareholder protections and the room for free enterprise to gather pace. Questionable stock market interventions may stabilise share prices in the short term, but the effectiveness of earlier targeted support was not enduring. Until the risk of heavy-handed intervention has decisively faded, international investors are unlikely to be drawn back to China’s (still) inexpensive stock market. We shouldn’t forget that we’ve seen false dawns before over the past three years – for now, we are happy to be patient.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.