The AI trade loses some steam

Investment Communications Team, Investment Strategy Team, Wealth Management

Summary

Global equities moved higher by 1.6% in July (USD terms), while global government bonds returned 1.8% (USD, hedged terms). Key themes included:

- Modest stock market returns disguise sharp mid-month rotation;

- The US Federal Reserve stays the course for a September rate cut;

- Biden ends his re-election campaign, with VP Harris in nomination contention.

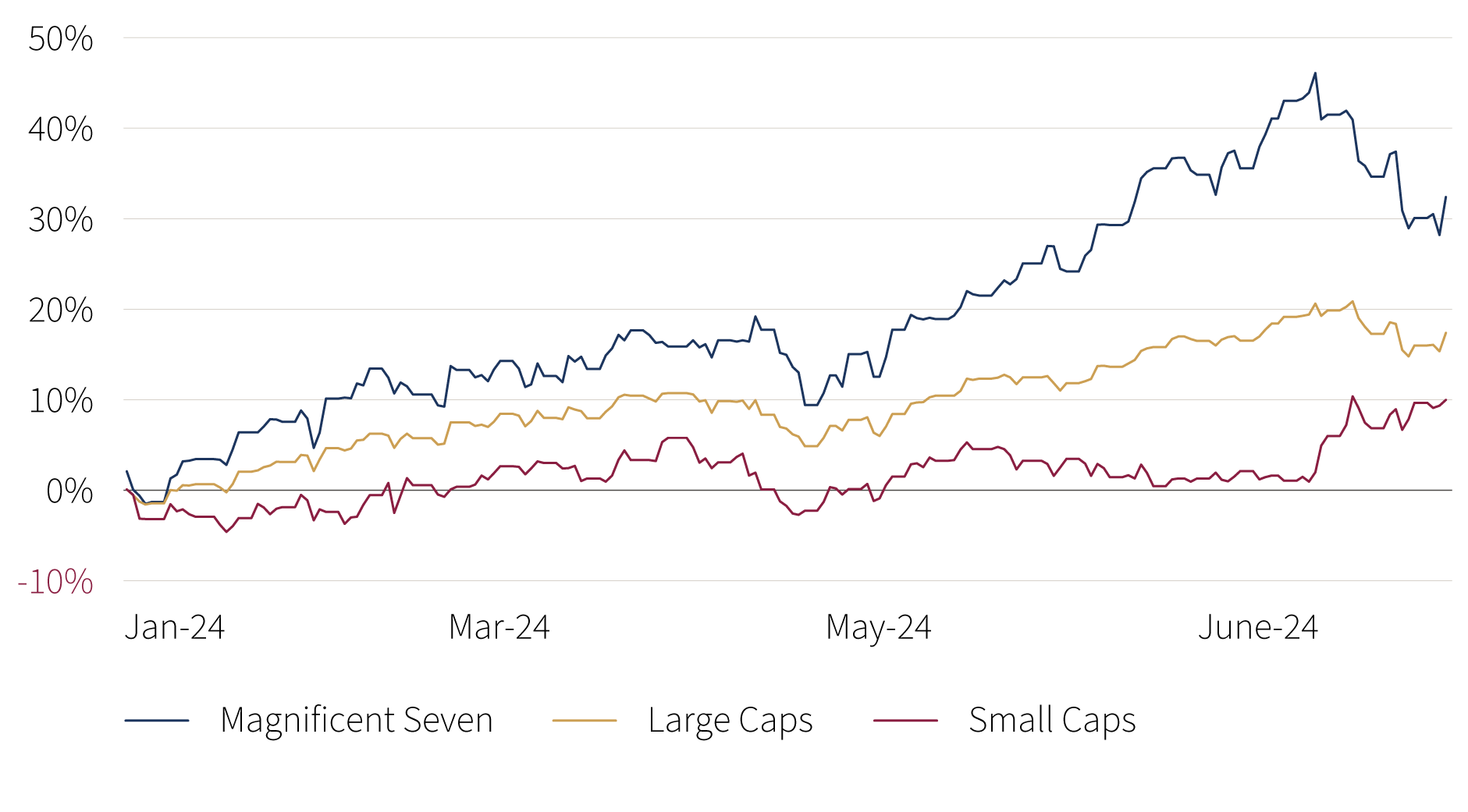

Key chart: US stock market returns

Year-over-year (MSCI indices, USD,%)

Source: Rothschild & Co, Bloomberg, MSCI

Note: Magnificent Seven is Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla (cap-weighted index).

Markets: Stock market rotation

After initially rising to fresh highs, global stocks retraced some of their monthly gains during the second half of July – led lower by the ‘Magnificent Seven’. Protectionist rhetoric and another friendly US inflation release – boosting the chances of the Federal Reserve easing from September – may partly explain the sharp rotation away from the mega-cap, ‘technology’-related names towards small caps. Meanwhile, the US Q2 earnings season had a strong start: the blended earnings growth rate was tracking close to 10% (y/y), after two-fifths of S&P 500 companies had reported. In fixed income, government bond yields continued to drift lower, with shorter dated bonds moving most visibly. In FX markets, some of the major currencies strengthened against the US dollar: the Japanese yen caught the eye (again), this time appreciating by almost 7% vis-à-vis the greenback. Commodities continued their broad-based decline, including Brent Crude oil, despite the escalating conflict in the Middle East. Precious metals bucked the trend, with gold rising to another high in US dollar terms.

Economy: Ongoing economic resilience

The US economy expanded by a stronger-than-expected 0.7% (q/q) in Q2, marking the eighth consecutive quarter of growth. Business surveys were mixed in July, but subdued manufacturing was offset by more upbeat service sector activity. Promisingly, the CPI inflation data were better than anticipated for the second consecutive month: the headline rate fell to 3% (y/y), while the core rate edged lower, to 3.3%. European economic growth continued, albeit at a softer pace than in the US. Second-quarter GDP expanded by 0.3% in the eurozone, while the forward-looking Composite PMI signalled modest expansion in July (German activity remained notably weak). UK output held steady, as monthly GDP expanded by 0.4% (m/m) in May, and the business surveys suggested a strong start to the third quarter. Inflation also remained more subdued than in the US, though the euro area headline inflation edged up to 2.6% in July. UK headline inflation stayed at 2% in June – core inflation was still elevated at 3.5% – while inflation moved closer to 1% in Switzerland. Elsewhere, in China, second-quarter activity was weaker than expected, but it was still on course to achieve the government’s “around 5%” 2024 GDP target.

Policy and politics: A gradual easing cycle; Harris vs Trump?

The US Federal Reserve left its policy rate unaltered, but Powell hinted that easing might begin in September. The European Central Bank also left its deposit rate unchanged – it had already reduced it in June – though the Bank of England lowered its base rate by 25 basis points (bps), to 5.00%. In Asia, the Bank of Japan modestly raised its policy rate target from a range of 0.00-0.10%, to around 0.25%, while the People’s Bank of China conversely lowered interest rates amid ongoing property sector issues (inflation remained muted there).

Another turbulent month in the political arena saw Trump’s popularity briefly surge following the assassination attempt in Pennsylvania. But the polling gap quickly reversed after Biden’s withdrawal and endorsement of Vice President Harris. On the other side of the pond, the far-right Rassemblement National fell to third place in the second-round of the French parliamentary election. No party secured an absolute majority, which resulted in a hung parliament. Unsurprisingly, the Labour party returned to power in the UK for the first time since 2010.

Performance figures (as of 31/07/2024 in local currency)

| Equity (MSCI indices $) | Month | Year |

|---|---|---|

| Global | 1.6% | 13.1% |

| US | 1.2% | 16.1% |

| Continental Europe ex. Switz. | 0.8% | 7.2% |

| UK | 4.2% | 11.4% |

| Switzerland | 4.8% | 6.7% |

| Japan | 5.8% | 12.4% |

| Pacific ex Japan | 1.6% | 2.3% |

| EM Asia | -0.3% | 10.7% |

| EM ex Asia | 2.7% | -2.6% |

| Fixed income | Yield | Month | Year |

|---|---|---|---|

| Global Govt (hdg $) | 3.11% | 1.8% | 1.7% |

| Global IG (hdg $) | 4.70% | 2.2% | 2.5% |

| Global HY (hdg $) | 8.00% | 1.8% | 5.7% |

| US 10Y ($) | 4.03% | 2.9% | 1.3% |

| German 10Y (€) | 2.30% | 1.8% | -0.6% |

| UK 10Y (£) | 3.97% | 1.9% | -0.7% |

| Switzerland 10Y (CHF) | 0.45% | 1.0% | 2.4% |

| Currencies (NEERs) | Month | Year |

|---|---|---|

| US Dollar | -0.6% | 4.1% |

| Euro | 0.4% | 0.8% |

| Pound Sterling | 0.6% | 3.6% |

| Swiss Franc | 1.2% | -2.3% |

Table note: NEERs under ‘currencies’ are the JP Morgan trade-weighted nominal effective exchange rates

| Commodities ($) | Level | Month | Year |

|---|---|---|---|

| Gold | 2,448 | 5.2% | 18.6% |

| Brent Crude oil | 81 | -6.6% | 4.8% |

| Natural gas (€) | 36 | 4.0% | 10.9% |

Source: Bloomberg, Rothschild & Co.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.