Stocks retrace April’s losses

Investment Communications Team, Investment Strategy Team, Wealth Management

Summary

Global equities rose by 4.1% in May (USD terms), while global government bonds edged higher by 0.5% (USD, hedged terms). Key themes included:

- Stock markets rebound, despite elevated bond yields;

- Fed signals a more cautious approach to easing relative to its European peers;

- Geopolitical backdrop remains uneasy in the Middle East, Ukraine and Taiwan.

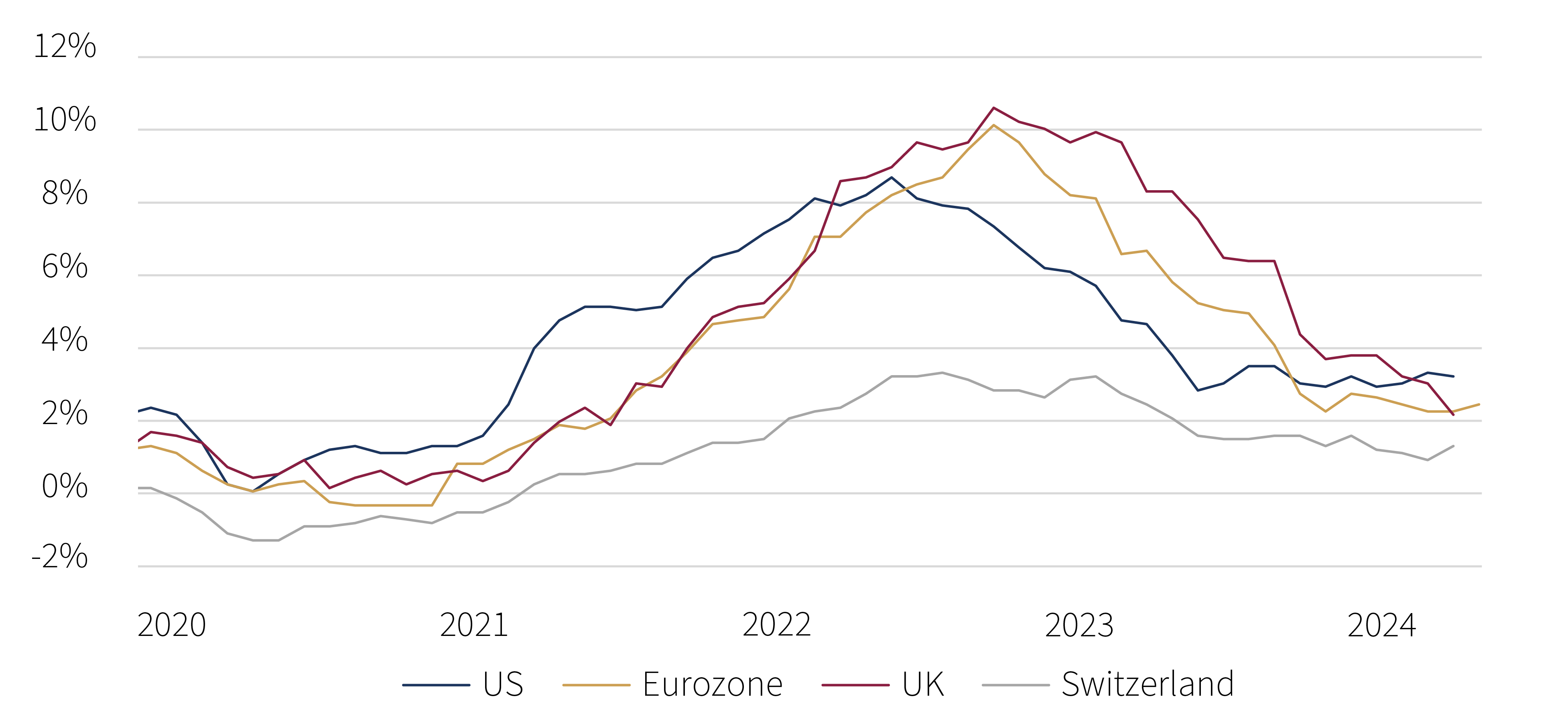

Headline inflation rates - Year-over-year (%)

Source: Rothschild & Co, Bloomberg

Markets: A better month for risk assets

Global stocks rebounded strongly in May, retracing the prior month’s losses – and briefly rising to all-time highs. Stock market participation broadened slightly, though the US mega-cap names continued to lead the market higher. The US first-quarter earnings growth rate was 5.9% (y/y) according to FactSet – stronger than consensus expectations – with significant contributions from those same mega-cap stocks. In fixed income, government bonds initially rallied during the first half of May, though reversed some of those gains later in the month: 10-year government bond yields touched fresh year-to-date highs in parts of Europe, such as Germany (2.7%) and the UK (4.4%) amid sticky inflation data. Commodities broadly continued to move higher, with the notable exception of Brent crude oil which fell by 7%.

Economy: Ongoing growth; sticky inflation

While US hard data were generally softer in April, real-time second-quarter GDP estimates continued to suggest another quarter of economic growth. The manufacturing survey data were mixed in May, with the ISM series edging lower to 48.7, yet the S&P Global series continued to signal expansion. There were tentative signs of labour market slackness in April: the unemployment rate crept up to 3.9% – still low by historical standards – while jobs growth and vacancies cooled. Encouragingly, US inflation met (rather than exceeded) expectations for the first time this year with April’s release. Both headline and core inflation moved lower, to 3.4% and 3.6% (y/y), respectively. In Europe, growth indicators continued to hold steady. The eurozone Composite PMI signalled a faster rate of growth in May, while the UK equivalent remained in ‘expansion’ territory. The UK GDP data also confirmed that it exited its brief technical recession at the turn of the year. Inflation data were stronger than expected, however: headline inflation accelerated in the eurozone (to 2.6%) and Switzerland (1.4%). UK headline inflation fell sharply to 2.3% following another drop in the Ofgem energy price cap, but services inflation (and wage growth) remained stubbornly high. In China, economic data were robust – consensus 2024 GDP estimates were tracking at close to 5% – but property sector issues remained unresolved, despite further government support measures.

Policy: Interest rates still poised to fall

The Federal Reserve left interest rates unaltered yet again in May, with Powell signalling that easing was postponed – but not cancelled. Conversely, in Europe, a more dovish narrative emerged: Sweden’s Riksbank was the second developed-market central bank to begin its easing cycle (after the Swiss National Bank), while the European Central Bank stood poised to cut in June. The Bank of England struck a more balanced, albeit divided tone: money markets were anchoring towards an autumn cut.

Meanwhile, the geopolitical landscape remained tense. Conflict in the Middle East showed few signs of resolve, Putin warned NATO on the use of their weapons provided to Ukraine, and China held military drills around Taiwan. Biden also announced further tariffs on China in critical areas, including semiconductors and electric vehicles. In the political sphere, Trump was found guilty on all counts in his “hush money” trail, making him the first former president to be convicted. In the UK, Sunak unexpectedly announced a general election for July, despite the Conservative’s weak local election results.

Performance figures (as of 31/05/2024 in local currency)

| Equity (MSCI indices $) | 1M % | YTD % |

|---|---|---|

| Global | 4.1% | 8.9% |

| US | 4.7% | 10.7% |

| Eurozone | 4.3% | 9.2% |

| UK | 3.6% | 8.8% |

| Switzerland | 8.1% | 1.7% |

| Japan | 1.3% | 7.0% |

| Pacific ex Japan | 3.4% | 0.4% |

| EM Asia | 1.4% | 5.8% |

| EM ex Asia | -2.7% | -5.0% |

| Fixed income | Yield | 1M % | YTD % |

|---|---|---|---|

| Global Govt (hdg $) | 3.43% | 0.5% | -1.0% |

| Global IG (hdg $) | 5.10% | 1.4% | -0.4% |

| Global HY (hdg $) | 8.29% | 1.2% | 3.2% |

| US 10Y | 4.50% | 1.8% | -2.8% |

| German 10Y | 2.66% | -0.2% | -3.8% |

| UK 10Y | 4.32% | 0.8% | -3.8% |

| Switzerland 10Y | 0.93% | -1.3% | -1.3% |

| Currencies (NEERs) | 1M % | YTD % |

|---|---|---|

| US Dollar | -0.7% | 3.0% |

| Euro | 0.5% | 1.1% |

| Pound Sterling | 0.8% | 2.7% |

| Swiss Franc | 0.2% | -4.9% |

Table note: NEERs under ‘currencies’ are the JP Morgan trade-weighted nominal effective exchange rates

| Commodities ($) | Level | 1M % | YTD % |

|---|---|---|---|

| Gold | 2,327 | 1.8% | 12.8% |

| Brent Crude oil | 82 | -7.1% | 5.9% |

| Natural gas (€) | 34 | 17.5% | 5.8% |

Source: Bloomberg, Rothschild & Co.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.