What is the relationship between flows and performances?

In the financial markets, the question of causality between performances returned by financial assets and buying inflow into the assets under consideration is still far from being resolved. Intuitively, investors are still tempted to believe that financial flows drive performances, by deforming the buying or selling volumes they trigger. In fact, (past) performances frequently provide the momentum driving current flows, which should (normally) imply future performances.

Currently, in a context of highly volatile markets, also characterised by heavy sector rotations in 2022, we can therefore ask ourselves whether flows cause performances, or if performances impact investment flows.

Taking the recent surge over recent years in so-called socially responsible investing (SRI) as an example, investment flows have been redirected towards certain types of stocks and sectors which are considered to be more virtuous than their peers.

For almost a decade, we have seen a wave of official programmes encouraging, or even obliging investors to choose these types of investments, with the aim of partly financing the cost of energy transition within companies. New specific labels have also been created to identify the funds adopting the best environmental, social and governance practices. For example, in order to comply with these constraints, most investment funds have decided to put sector exclusions in place in several industries, including weapons, fossil fuels (notably oil stocks), mines and tobacco. Financial flows are therefore automatically steered away from these sectors and directed towards segments and stocks favoured by the integration of these new aspirations or constraints.

In Europe, with two trillion invested in SRI at the end of 2021, these assets represented almost a quarter of distributed funds. Portfolio managers therefore actively sought the most “responsible” stocks in which to invest this abundant inflow. The imbalance between supply and demand, due to the investment universe being limited and strong growth in inflow towards SRI investments, therefore distorted performances between sectors and stocks until 2021. This observation has clearly demonstrated that investment flows drove the outperformance staged by SRI funds until 2021.

The French life insurance market provides a contrasting example however. Most contracts are composed of both euro-denominated funds and also unit-linked contracts, which are inherently more volatile. The ACPR1 reported net outflow of €12.3 billion from euro-denominated funds in 2021, while unit-linked contracts saw net inflow of €30.6 billion. Part of the inflow into unit-linked contracts, which are invested chiefly in equities and bonds, was to the detriment of euro-denominated funds, in a context of persistently lower yields over preceding years. This provides an illustration of past performances from investment supports (considered too disappointing) directing flows and determining their reallocation towards other more promising assets.

We therefore deduce that asset performance and investment flows are inextricably linked.

Flows driven by …

Of course financial flows remain strongly influenced by official decisions from governments and stock market authorities and regulators. Other factors may also have a strong influence on cashflows between the different financial asset classes however.

The leading role played by the central banks is clearly the most important of these factors. When monetary policy becomes more accommodating, central banks are likely to buy massively into bond markets, with the aim of pushing prices higher and, in doing so, driving down yields, i.e. the level of interest rates in the financial markets. Conversely, in 2022, the year of the U-turn among leading monetary policies, the central banks decided to abruptly halt their bond repurchase programmes and not renew purchases on bonds reaching maturity. Demand for sovereign and corporate bonds therefore automatically fell sharply. The sudden withdrawal of demand from the hitherto buyer of last resort partly accounts for the poor performance posted by US corporate bonds over 2022, which closed the year down 15.4%.

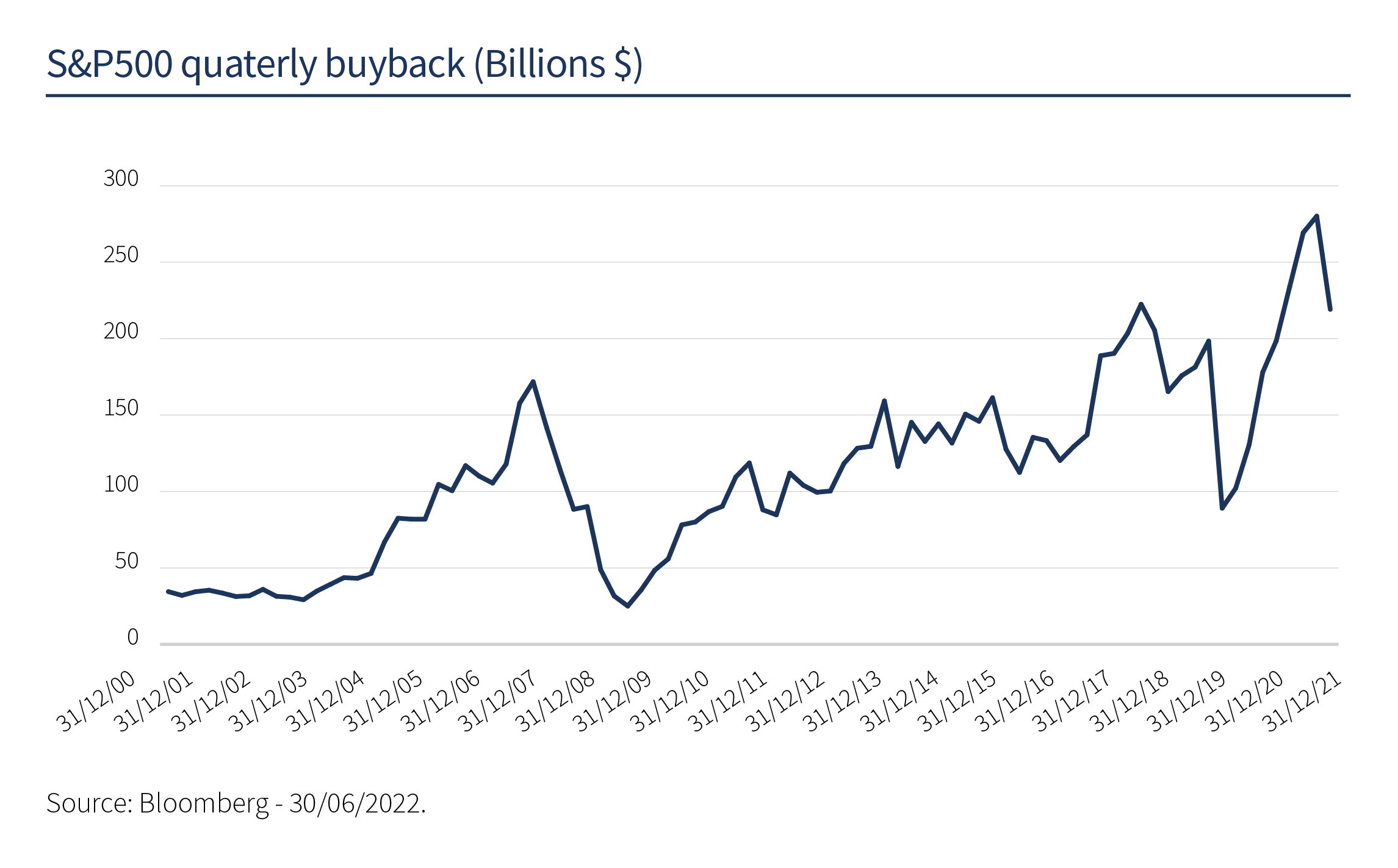

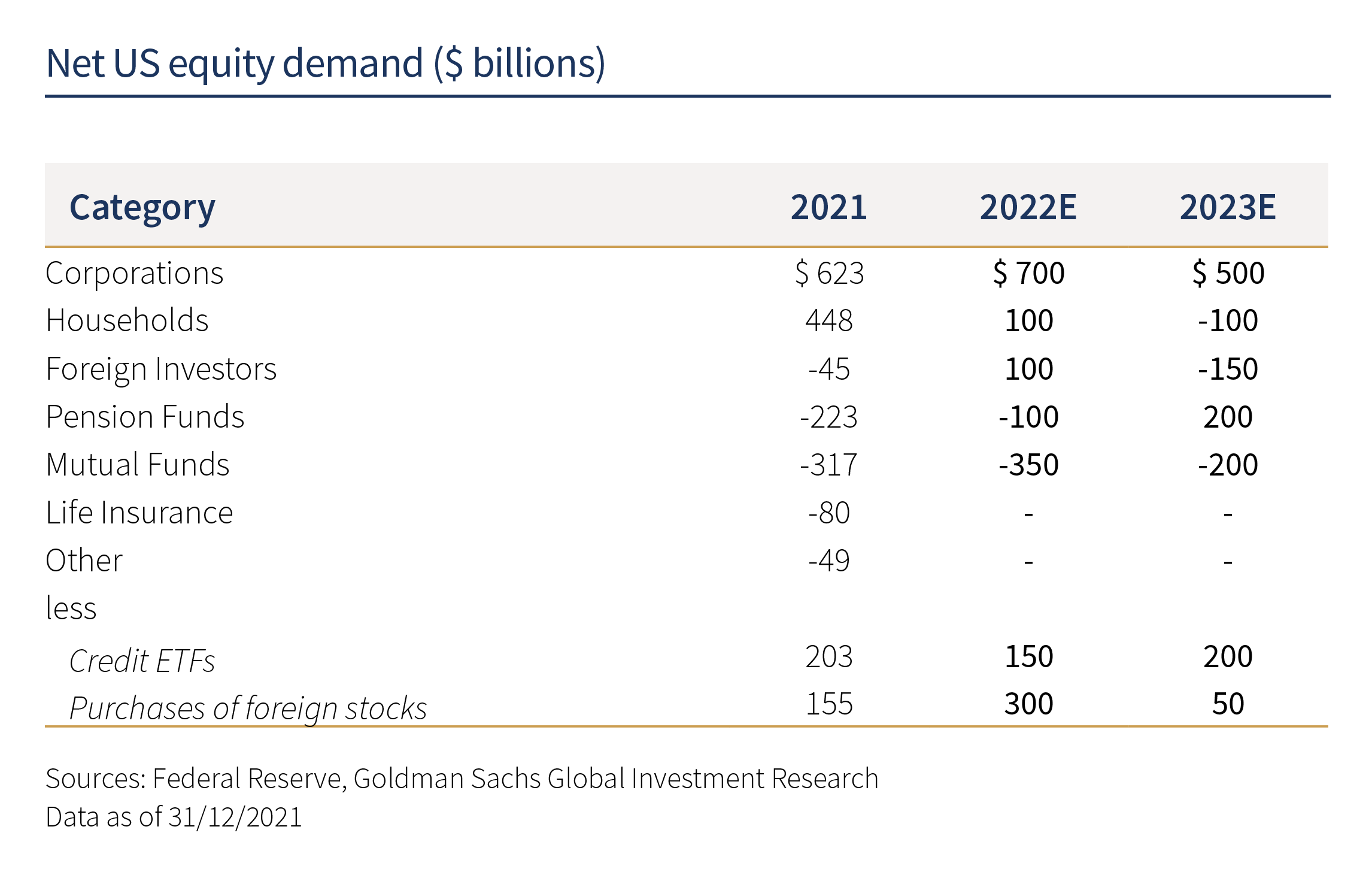

Both in the US and also in Europe, companies also play a key role in demand for certain financial assets. Over the past few years, share buyback programmes launched by companies have progressed steadily (see US chart below) and, in 2021, on both sides of the Atlantic, corporates were the leading equity buyers, followed by households, foreign investors and then pension funds (see table below). These flows clearly participated in the excellent market performance recorded by beneficiaries of buyback programmes ratified by general shareholder meetings, particularly in the healthcare sector and among banks and blue-chip tech stocks. However, with interest rates steepening and the economy slowing at the same time, companies are tempted to reduce the pace of their share buyback programmes, incurring a risk of consolidation in the markets, due to reduced buying interest.

Along similar lines, major allocation decisions taken by pensions funds and their timing (see below) may prove to be a determining factor for financial markets, which have to honour liabilities to their investors and are seeking to align their engagements with the characteristics of the assets they hold. The level of interest rates towards which we are currently heading in the US (5 - 5.5% in the short term) are beginning to match the yield requirements of certain pension funds, which could encourage them to reduce their weightings among US equities, following strong capital gains over the past five years, in order to increase their “risk free” portfolio allocations.

More surprisingly

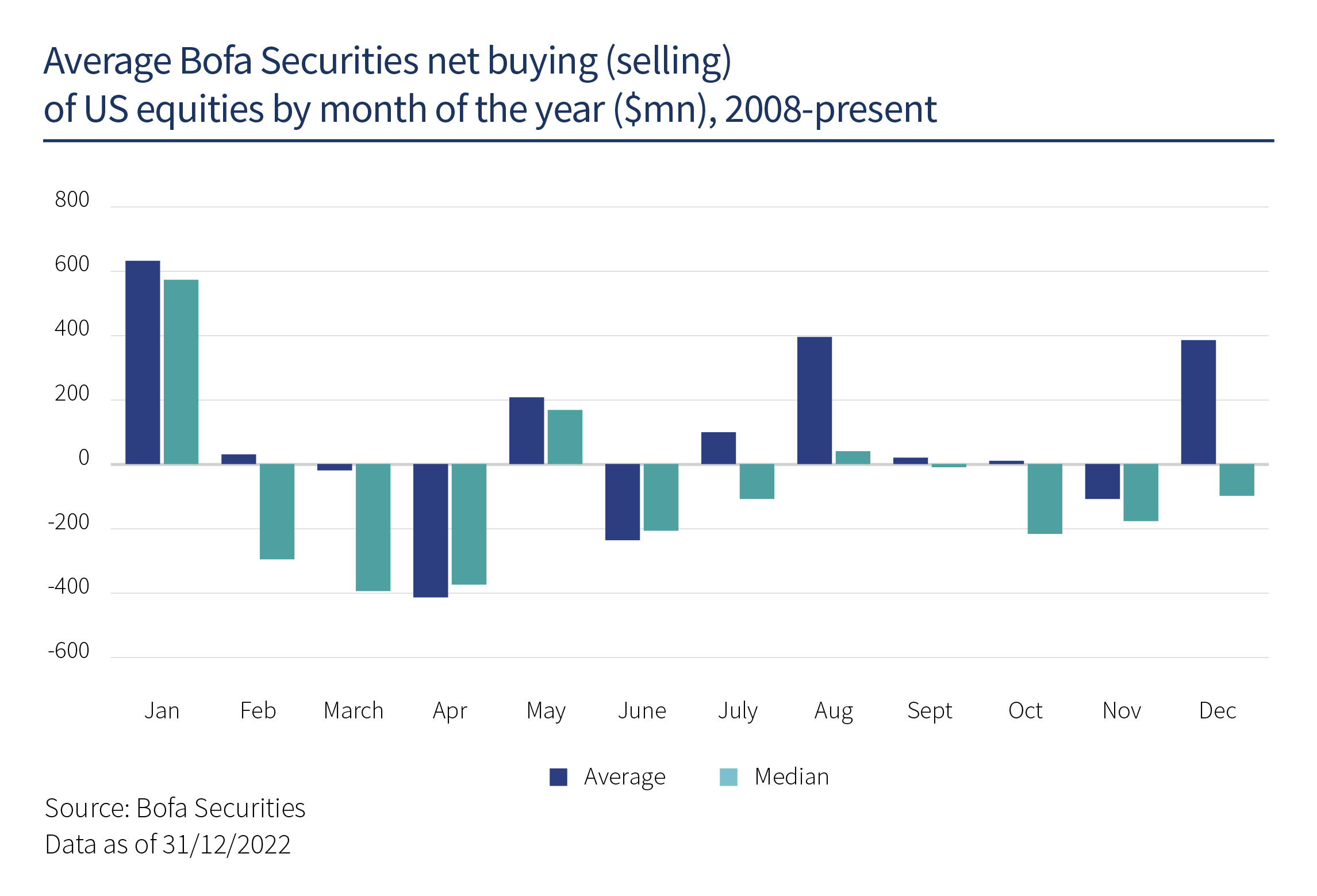

As surprising as it may seem, there are effectively positive and negative “seasons” among financial markets, or rather a type of “seasonality”. For example, January is renowned for being a positive month following a bearish year. This trend is associated with bargain hunting by retail investors, as this is the period when households buy most into equities, according to a study published by Bank of America (see monthly inflow data chart). More experienced investors are also aware of the saying “sell in May and go away”, as during the era before the existence of “robo-advisors” and other high-frequency trading programmes, market volumes were thinner during the summer so volatility increased, as market professionals were on vacation. A question of flows once again.

Demographics and wealth per inhabitant also prove to be determining factors accounting for capital flows in one direction or another. With the emergence of the middle classes in China since the 90s, there are now 400 million individuals in this category, with sufficient resources to enable them to access savings products or mutual funds, which was unimaginable a few years ago. There is little doubt that this population will play an increasingly important role in flow trends.

Lastly, the structure of the investment vehicles available in the market may also prove to be a key issue in gauging future flows and therefore the potential impact on certain assets, in terms of their performance. The proportion of US equities held by index funds and ETFs2 in 2021 exceeded actively managed funds’ holdings. Passively-managed investments, which replicate the indices very closely, tend to create investment bubbles among certain assets, by extremely fluidly driving capital in one direction. For example, in 2020, supports investing in renewable energies saw record inflow. The Ishares Clean Energy tracker3, managed by Blackrock, took in two billion dollars during December alone. As the investment universe is inherently limited and often of modest size, some stocks recorded sharp gains, such as Energias de Portugal Renovaveis and NEOEN, rallying 45% over the month, driven by the powerful rapid inflow of capital.

Flows are therefore of vital importance in determining performances among the underlying assets which benefit from inflow, or on the contrary, which see huge outflow from certain segments. Future flows will therefore have to be anticipated, in order to predict the sources driving forthcoming performance spreads. This will be a challenging task, judging by the broad range of determining factors.

So, what is simpler (or more intuitive)? Forecasting flows or performances?

1 The Autorité de contrôle prudentiel et de résolution (ACPR) is the French banking and insurance supervisory body.

2 Exchange traded funds (ETFs) are financial instruments designed to faithfully replicate upside and downside variations in an index.

3 Like ETFs, fund trackers replicate fluctuations in a given stock or index.