Asset Management Europe: Monthly Letter – December 2019

Marc-Antoine Collard, Chief Economist, Head of Economic Research, Asset Management, Europe

Economic environment

The latest data showed that factory output has been particularly weak on the back of the continuing high level of uncertainty, with trade policy tensions taking an increasing toll on confidence and investment. That said, several transitory shocks are also to blame. Specifically, a large labour strike in the automotive sector has weighed on US industrial production growth, while a consumption tax hike and a typhoon have severely hit Japanese production. As a result, global industrial production is expected to drop in Q4 2019. However, amid a choppy stretch of anaemic growth this year, the global manufacturing sector showed tentative signs of life in November. The Markit business confidence index posted a sevenmonth high of 50.3, moving back above the 50-threshold - which divides expansion from contraction - for the first time since April 2019. While the level of confidence is perhaps best described as precarious, it is nonetheless consistent with the consensus view that the global slowdown is bottoming out.

Click the image to enlarge

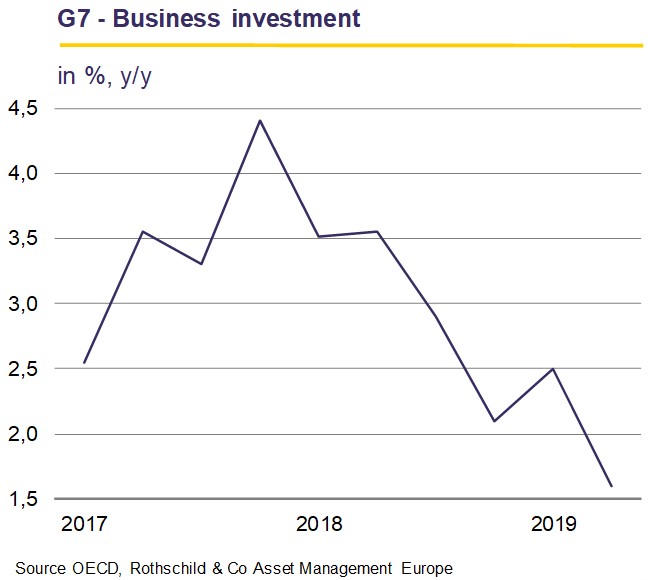

In fact, market participants expect two related developments to form the foundation for a rebound which should take hold by earl 2020. First, business sentiment should strengthen as corporates' fears about US-China trade and idiosyncratic shocks in other larg economies (e.g. Italy, Brexit) fade. Moreover, synchronised monetary policy easing is loosening financial conditions which, combined wit China's stimulus measures, should spur economic activity. As these forces begin to turn the tide toward growth, the lift should als reinforce firms' decision to start normalising global capex which ha decelerated markedly, with investment growth in the developed countries slowing to only 1% in Q2 2019.

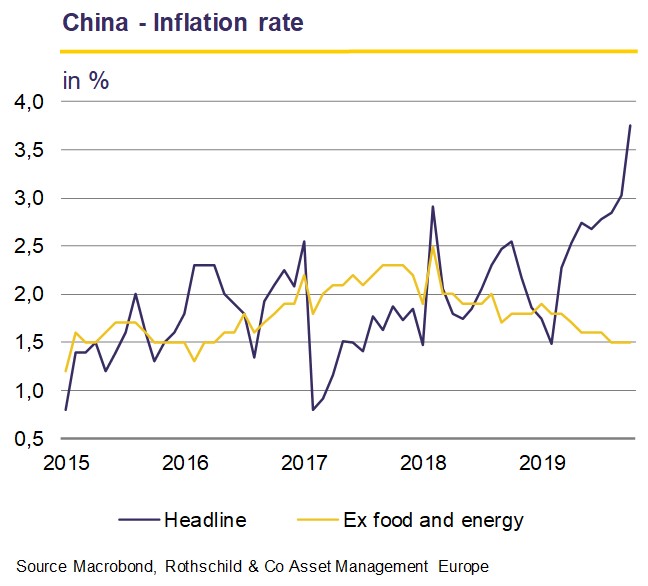

And yet, the timing and magnitude of this rebound remain uncertain. They way Chinese policymakers have balanced the tradeoff between growth and debt might once again surprise most investors. Their tolerance for slower growth has been much higher than most had anticipated and, as China remained reluctant to boost credit growth in a major way, it has instead continued to focus on containing financial risks. Thus, after a temporary rebound in September, growth momentum slowed again in October amid external headwinds and the limited impact of policy stimulus, repeating the pattern seen at the beginning of each quarter this year: industrial production, fixed asset investment and real retail sales all decelerated more than expected. Retail sales were also hurt by higher inflation - reaching almost 4% in October, a sevenand- half year high, driven by rising food inflation, particularly pork prices. Goods export volumes also grew at a slower pace in October, while import volumes continued to decline.

The Sino-US trade conflict remains a wild card. The deferral of the tariff increases that were set to take effect in mid-October, as well as the ongoing trade talks (Phase One), are positive developments. That said, not only is there a gulf in perceptions on what US and China have achieved, but it is difficult to reconcile the comments from both sides. It is uncertain whether the delayed tariff hikes will be postponed indefinitely and whether the existing tariffs will be lifted soon as required by China in order to sign any deal. US President Donald Trump recently signalled he would be willing to wait for another year before striking a trade agreement with China, casting doubt on the likelihood of a Phase One accord before year end and on the deferral of the December 15 tariffs on Chinese goods. Meanwhile, the US Congress adopted two new laws - the Xinjiang bill, regarding human rights, and the Hong Kong bill, which supports protesters - prompting China to threaten possible retaliation which could undoubtedly disrupt trade talks.

Click the image to enlarge

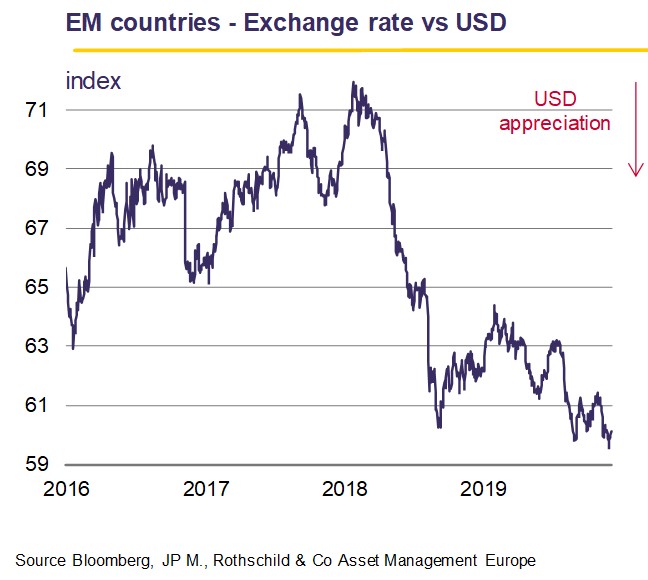

In addition, Trump also reinstated tariffs on steel and aluminium from Argentina and Brazil, criticising the depreciation of their currencies against the dollar. Yet, both countries have been trying to strengthen their currencies in a context where several emerging economies have reached new lows against the greenback due to the high level of nervousness of forex investors. In fact, the origin of Trump's decision may lie in the domestic political consequences of his trade war as US farmers, a key component of his re-election strategy, were among the first victims of China's retaliation on soya and other agricultural products, as it allowed their Brazilian and Argentine peers to profit from the situation.

Click the image to enlarge

The upshot is that notwithstanding the recent truce, tariffs imposed by the US since 2018 are inflicting pain through different channels. Economic uncertainty has become a pressing concern for firms around the world and the increasing unpredictability of trade policies is likely to be a persisting drag on activity for a prolonged period. In fact, the disruption to trade, cross-border investment and value chains harms potential GDP growth by reducing business investment and thus productivity, which in turn weakens mediumterm growth prospects. In other words, trade wars not only depress short-term economic activity, they have far-reaching long-term consequences.

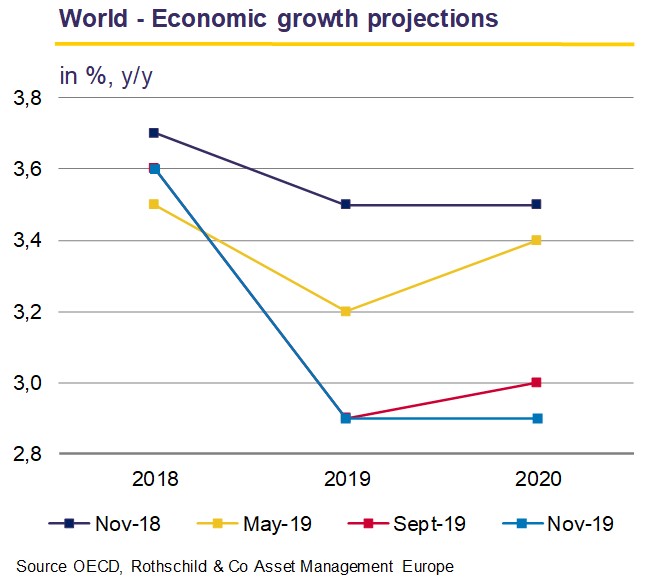

Overall, investors in the equity markets seem utterly convinced that easier financial conditions, combined with abating geopolitical risks, should support business confidence, hence bolster economic growth in 2020. Are they once again overconfident regarding next year's growth as they were regarding 2019 which, it has turned out, exhibited the weakest pace since the Great Financial Crisis? Although activity in the service sector has held up until last summer, helped by steady growth in consumer spending, we have seen growing signs of softer developments from survey data. Meanwhile, a further period of weakness in the industrial sector is not without risks, as it could result in a downturn in hiring intentions, reducing working hours and placing downward pressure on household incomes and spending, and ultimately reinforcing the slowdown in demand for services.

Click the image to enlarge

Download the PDF version Monthly Letter (626 KB)