Energy price shock?

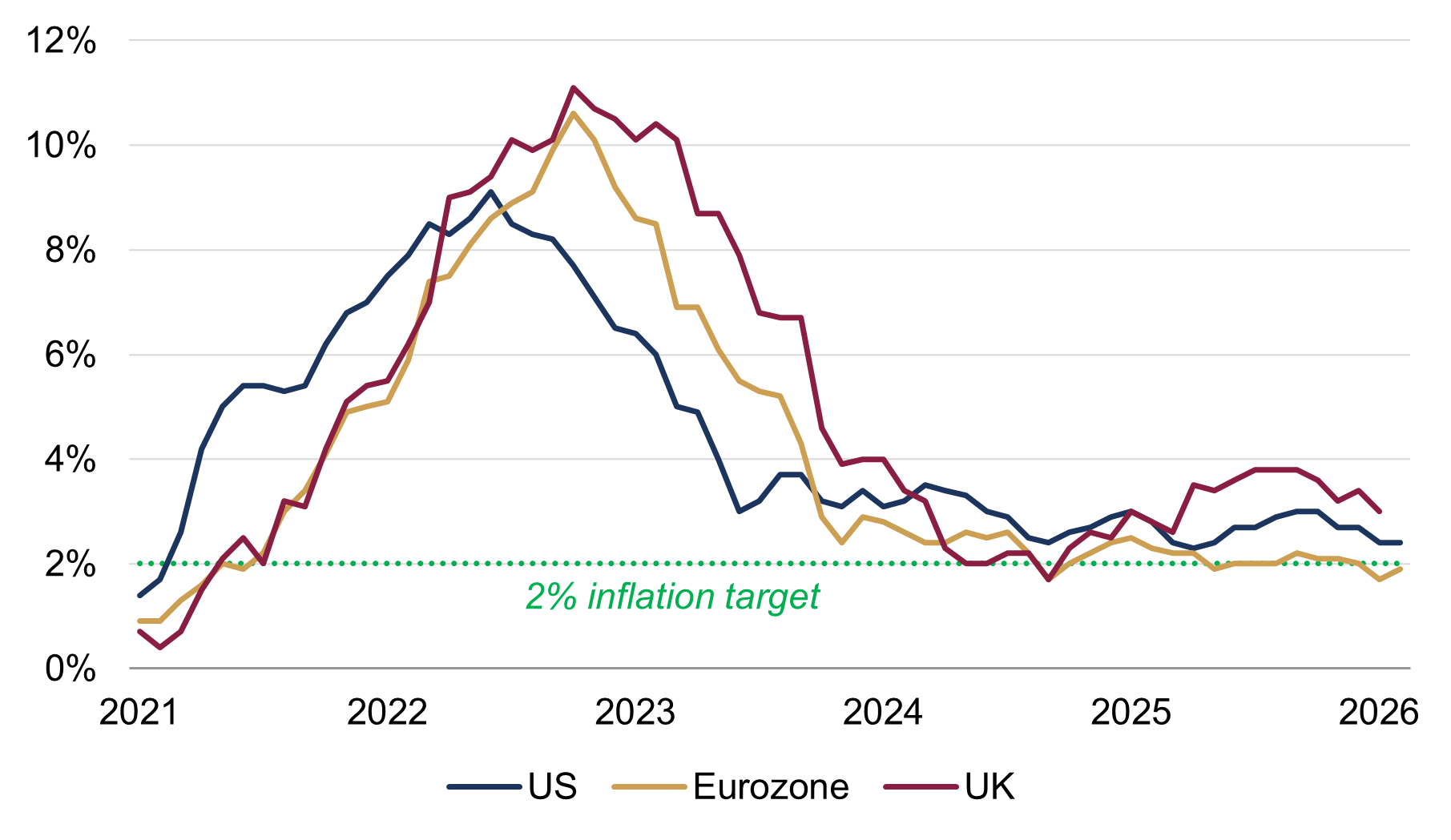

Inflation had been moderating in the US and Europe in recent months, with headline CPI (Consumer Price Index) rates mostly in the lower half of the notional 2-4% range that we have long suggested they may stick in (figure 1).

Figure 1: Headline CPI inflation rates

Year-over-year (%)

Source: Rothschild & Co, Bloomberg

However, energy prices have now surged as a result of the US/Israel-Iran conflict. How might this energy shock alter that inflation picture?

For context, energy usually accounts for a small proportion of western nations’ CPI baskets (~5-10% across the US, UK and eurozone). That said, it can be highly volatile at times, leading to large contributions to headline inflation (in either direction).

Oil flows and production disrupted

Iran itself has only accounted for 3-5% of global oil production in recent years, but hostilities have affected flows through key chokepoints in the region – notably, the Strait of Hormuz (figure 2). Roughly a fifth of global oil consumption passes through the latter artery daily, and these have now effectively come to a standstill. Re-routing oil to the Red Sea from the exposed Gulf nations may be difficult, partly due to pipeline capacity constraints, but also because Iranian proxies – such as the Houthis – could target vessels attempting to pass through the Bab al-Mandab Strait. The Suez Canal is perhaps the most viable trade route, but oil deliveries to Asia – which is where most such shipments go – would be significantly delayed, needing to be re-directed via the Cape of Good Hope (the southern tip of Africa).

Figure 2: Key shipping routes in the Middle East

Source: Rothschild & Co, Bloomberg Finance L.P., Mapbox, OpenStreetMap

Energy infrastructure and ports in nearby countries have also been directly attacked, including those that are located away from the Hormuz bottleneck, such as in Oman. To make matters worse, oil storage is nearing capacity – partly due to the lack of vessels – causing production to slow. Rebooting output would not be instantaneous – some oilfields may take months to return to ‘normal’. Clearly, an escalation in conflict would result in a major energy shock.

US energy CPI sensitivities

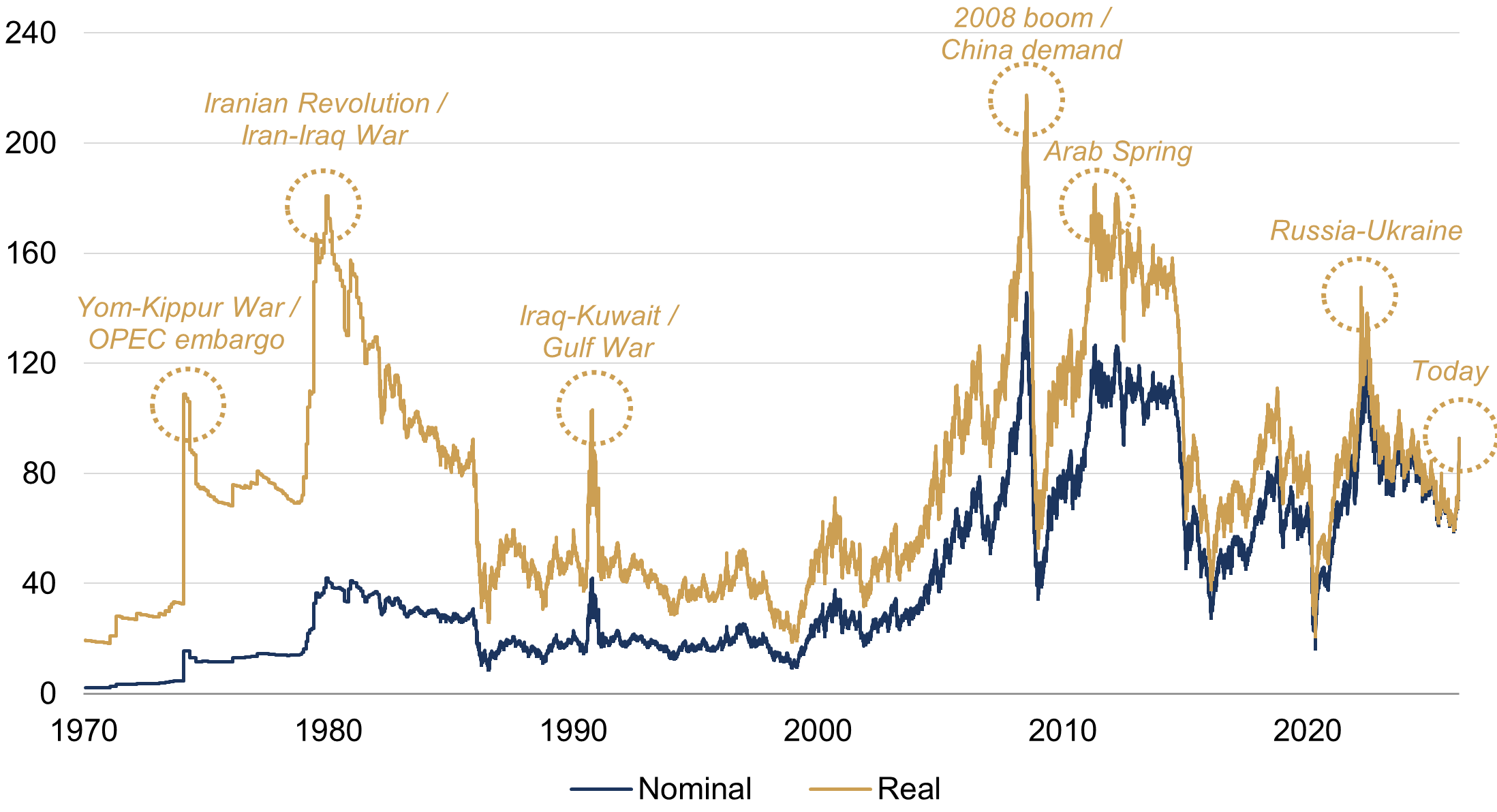

Perhaps unsurprisingly, the front-month Brent crude oil contract has risen by a quarter in dollar terms since the start of the conflict, to roughly $90 per barrel (although, its closing price on Monday was closer to $100). It is now in the upper end of its recent years’ trading range and further moves higher cannot be ruled out: Qatar’s energy minister recently warned that oil could hit $150 per barrel if Gulf production fully shuts down (which would surpass the $128 mark it reached in March 2022, following Russia’s invasion of Ukraine). The latter scenario would be a notable oil price shock – even when adjusted for inflation (figure 3).

Figure 3: Brent crude oil

Left axis: nominal USD; Right axis: today’s USD price adjusted for inflation

Source: Rothschild & Co, Bloomberg, LSEG Datastream

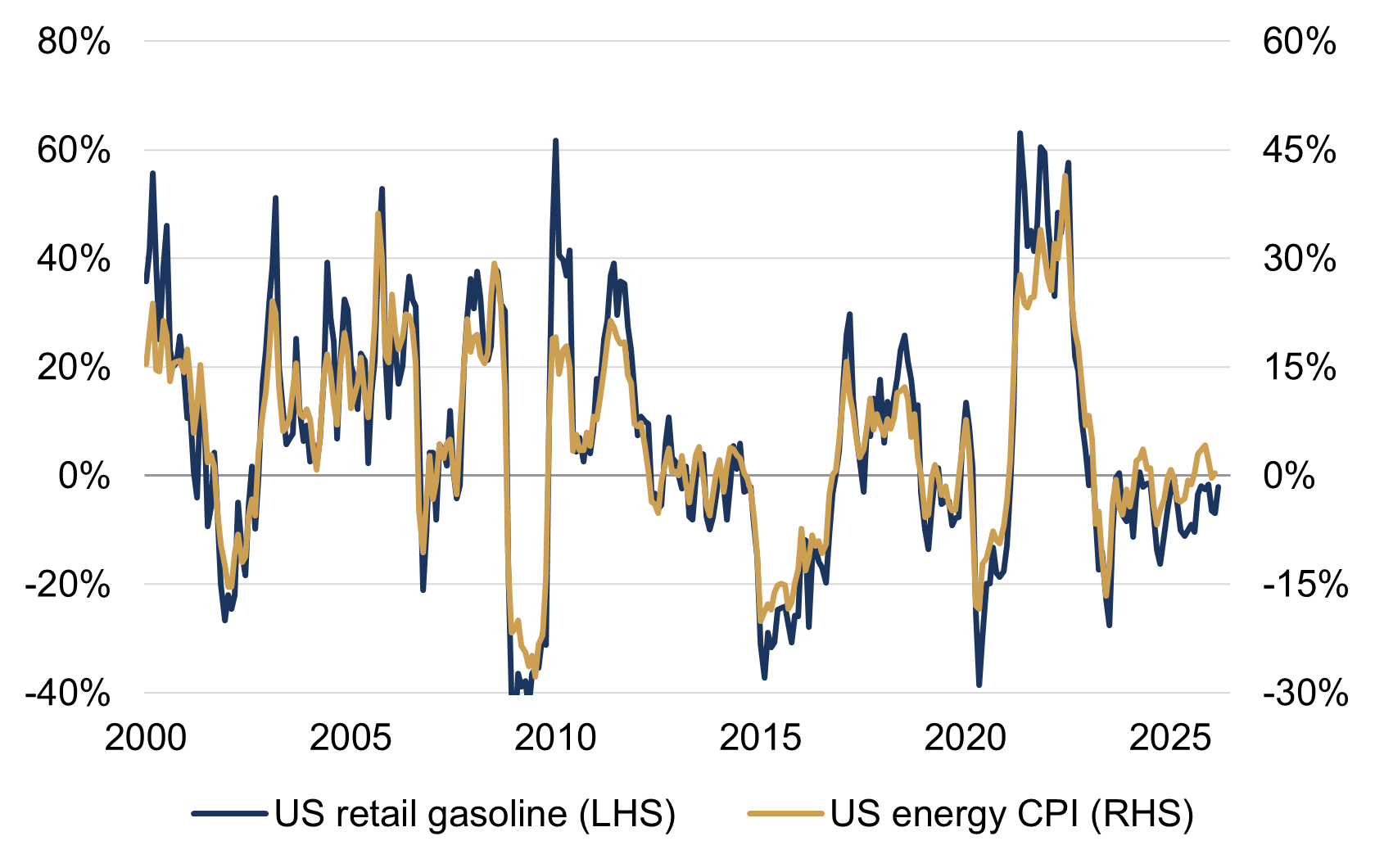

For US consumers, Brent crude may be less relevant than West Texas Intermediate (WTI), but the order of magnitude in price changes to date have been similar, and are quickly reflected in the ‘price at the pump’. Crude oil accounts for roughly half the cost of gasoline – the other costs are a mix of refining, distribution and taxes – which is in turn roughly half of the energy category within the CPI (the link is clear in figure 4). We can therefore roughly estimate the likely looming impact of higher oil prices on US headline inflation.

Figure 4: US gasoline prices and US energy CPI

Year-over-year change (%)

Source: Rothschild & Co, LSEG Datastream, US Energy Information Administration

A back-of-the-envelope calculation suggests that regular gasoline prices may rise by nearly 20% with oil at $100 per barrel (that is, by roughly half the change in the price of crude oil). In the more worrying $150 per barrel scenario, US retail gasoline prices could surge by approximately 50%. The direct weight of gasoline in US energy CPI is almost a half, but the effective weight is likely larger at perhaps three-quarters (if we compare the left-and right-hand axes in figure 4), possibly due to spillovers into other energy CPI categories. The energy component itself is roughly 6% of the total US CPI, meaning the near-term contribution to year-over-year US headline inflation would be under a percentage point in the $100 per barrel scenario, or more than two percentage points in the $150 per barrel scenario.

This is of course an approximation only: we don’t know what will happen to other costs, whether directly oil-related or not.

Another European gas spike?

Meanwhile, the energy price shock could be more damaging for European economies, given that Europe is more reliant on natural gas, and local wholesale gas prices have risen much more sharply than oil benchmarks (note: US natural gas prices have been somewhat stable, perhaps because local gas supply is more elastic than crude oil).

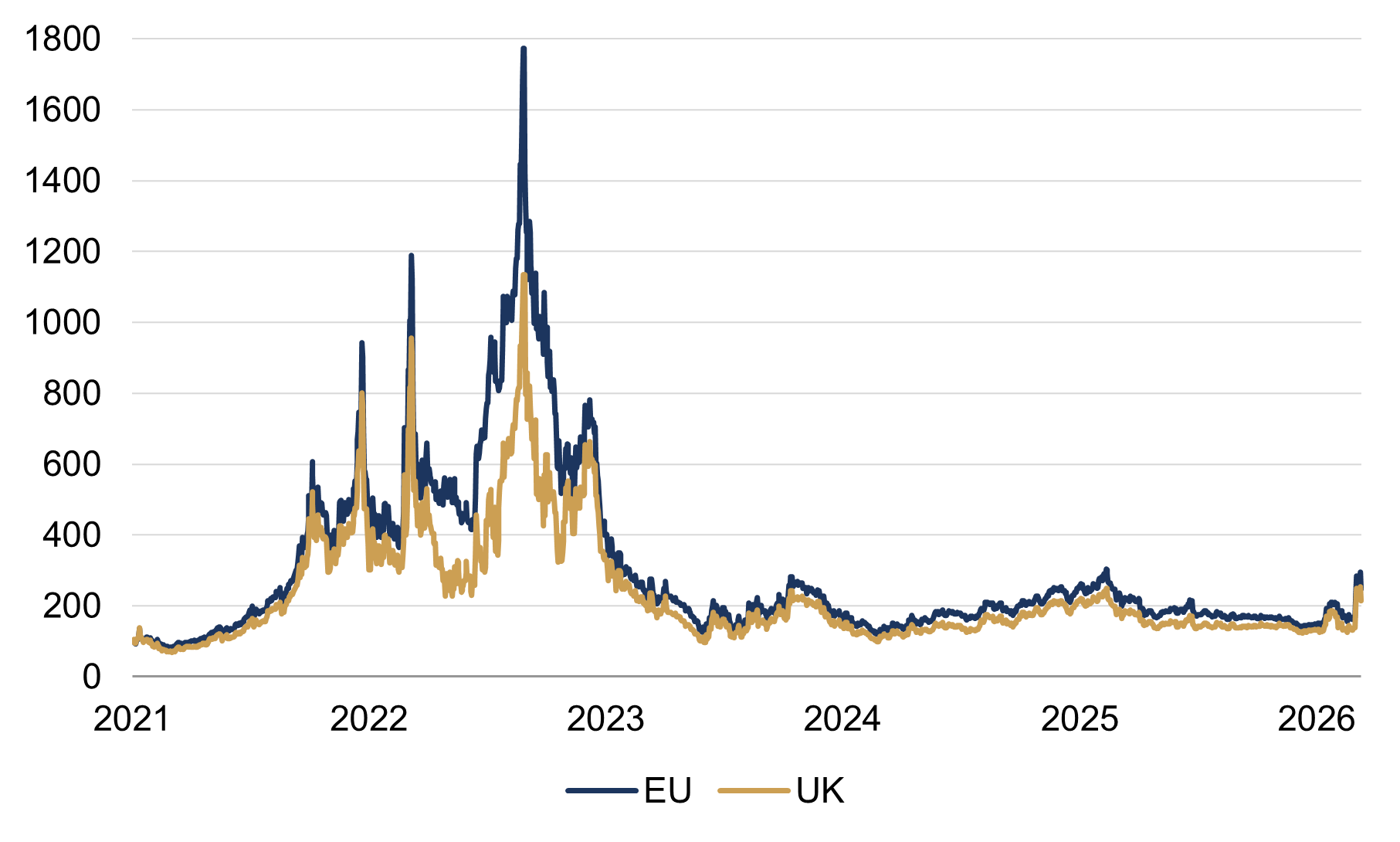

Qatar – which accounts for a fifth of global LNG supply – has halted operations, and other major gas-exporting countries (such as Azerbaijan) could be pulled into the conflict. While most energy outflows from the region are to Asia, the reduction in overall supply – coupled with Europe’s dependency on importing natural gas (and unusually-low inventories) – has caused short-term UK and EU gas contracts to rise by more than 50% in price.

However, the translation from the wholesale gas price to consumer prices (i.e., European energy CPIs) is trickier to quantify, as European gas markets are highly regulated (and thus complex), and local energy mixes (and government policy) vary across each country.

For example, the UK government sets an ‘Energy Price Cap’ each quarter, which as the name suggests, imposes a cap on how much suppliers can charge households for each unit of energy consumed. While the cap tends to reflect the direction of travel of wholesale prices, it will not be the exact amount, given it was implemented by the national regulator to essentially ‘smooth’ household energy bills. Moreover, following the surge in gas prices in 2022, the government introduced an ‘Energy Price Guarantee’ to impose a ceiling on the existing price cap. But levels today are probably not high enough to push the price cap near that old ceiling: wholesale UK and European gas prices remain 80-85% below their August 2022 highs (figure 5).

Figure 5: Wholesale European natural gas prices

Rebased indices (January 2021 = 100, local contracts)

Source: Rothschild & Co, Bloomberg. Note: EU series is the front-month ICE Endex Dutch TTF Natural Gas Futures Contract.

Above-target inflation to persist

It’s possible, then, that the upper bound of our noted 2-4% inflation range is breached in the event of a lasting energy price shock. Higher energy prices may also filter through to production costs, which could push the larger (albeit less volatile) CPI categories higher, such as ‘goods’ and ‘services’. The final CPI category, food, is also likely to rise, given the region’s importance in fertilizer production and exports (urea prices have indeed already surged).

Overall, it is difficult to make confident predictions around the inflationary implications of this conflict – much depends on its duration and severity, which is unknowable – but constructive outcomes, while hard to imagine, are still possible (particularly given the mercurial nature of President Trump).

Of course, we are focusing here on the likely short-term effects. However, if energy costs eventually affect economic activity and employment significantly, resulting in a big setback to growth, or even a recession, the longer-term impact might turn out to be smaller, or even negative. This is why central banks need to think very carefully about responding to such a relative price shock with tighter monetary policy – a topic we will be addressing shortly.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.

-

The next UK Prime Minister

Strategy Blog

Following Keir Starmer’s resignation, Andy Burnham has emerged as Labour’s likely successor. Despite political uncertainty, markets remain calm, with economic and geopolitical trends outweighing domestic politics. Significant policy change appears unlikely.

-

SpaceX: Infinity and beyond?

Strategy Blog

Markets are preparing for a wave of megacap IPOs led by SpaceX, amid strong AI-driven optimism. While liquidity should absorb issuance comfortably, questions remain around valuations, passive investing, concentration risk and index influence.