Europe’s fiscal impetus

Excitement over continental Europe’s growth trajectory appears to have faded over the course of this year, as AI-related developments – where the US and EM Asia are frontrunners – have returned to centre stage.

Nonetheless, European growth still seems set to improve. The prospective short-term boost to aggregate demand from fiscal policy which aroused that excitement – notably in Germany – is still pending, and may also provide Europe with an opportunity to deliver some of the supply-side changes which matter most to longer-term growth (see Products Matter blog).

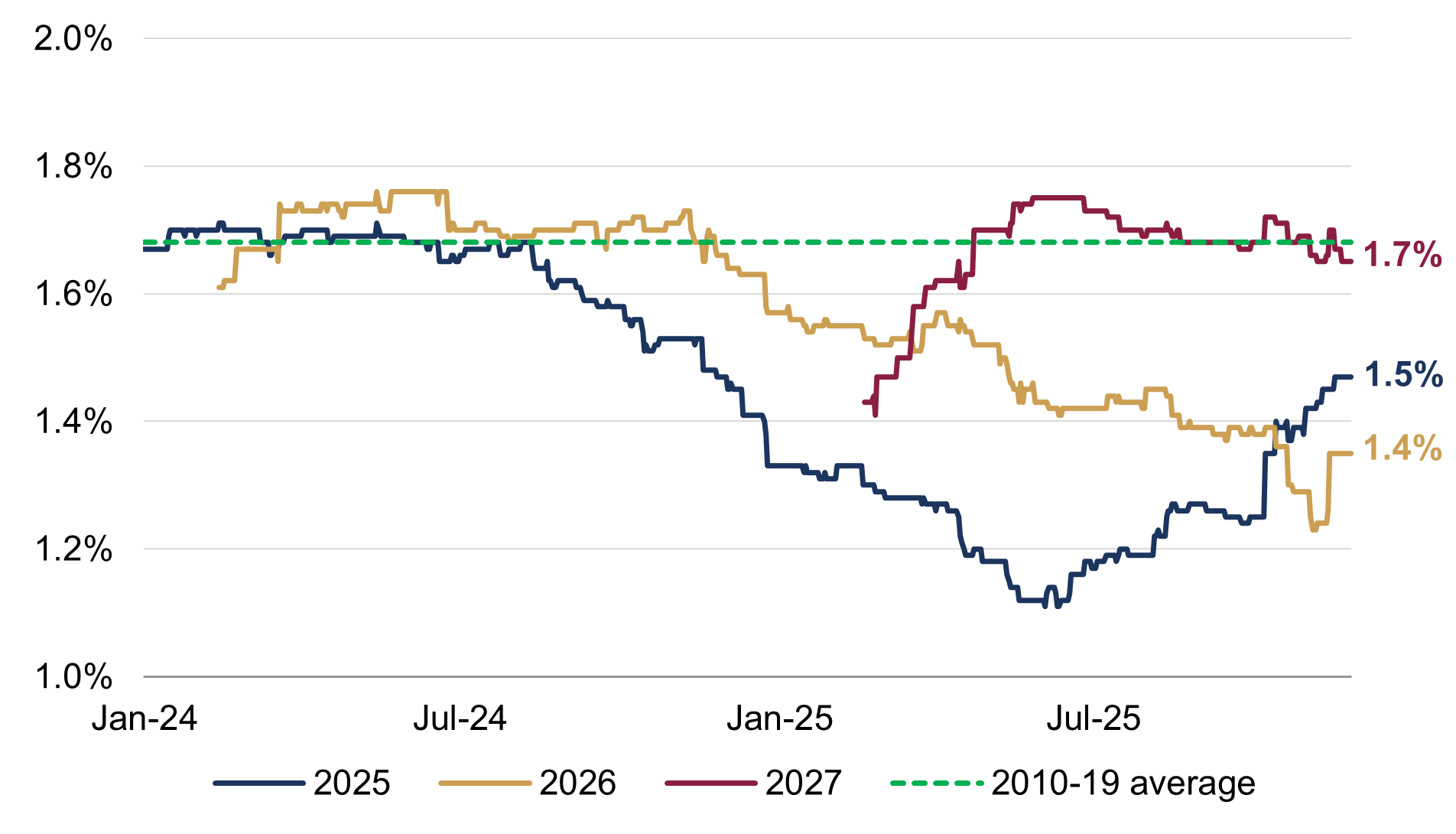

EU GDP growth estimates have not yet changed meaningfully, despite the sizeable stimulus announcements (figure 1). The recent upgrade to this year’s growth estimate seems to have coincided with a reversal in Trump’s tariff policies since ‘Liberation Day’ rather than a positive reappraisal of local developments. Remarkably, economic activity is projected to slow next year: prospects for 2027 seem to have improved, but only to the extent of matching the bloc’s average pre-pandemic growth rate.

Are the prospects of EU growth being underestimated amid the looser spending backdrop?

Figure 1: EU GDP growth estimates

Consensus estimate evolution (calendar year, %)

Source: Rothschild & Co, , Bloomberg. Note: Labels are rounded to one decimal point.

Germany’s spending splurge

Growth in Germany – which accounts for just under a quarter of EU GDP – has remained feeble this year, on track to only just avoid stagnation, following the decline in its product competitiveness. However, the most economically-significant fiscal developments have occurred there this year, and so its growth outturns may soon improve.

The new coalition, led by the CDU’s Friedrich Merz, announced huge spending plans following their election victory in February. A €500 billion infrastructure package was unveiled, which included a €100 billion allocation to Germany’s climate-related fund. The various projects – ranging from transport to digitalisation – were allowed to be financed over a 12-year period, which would amount to just under 1% of additional domestic GDP growth per year. Other exemptions from the restrictive ‘debt brake’ – the requirement for Germany to balance its budget – included additional defence spending (which technically is unlimited) and additional state-level borrowing. At the time of its announcement, some local commentators went as far to say it was the biggest economic development since the fall of the Berlin Wall.

For would-be ‘bond vigilantes’, it’s worth noting that Germany’s net debt is less than 50% of GDP, which is roughly half that of the US, UK or France.

In recent months, concerns have emerged around the implementation of these funds: there have been reports of infrastructure funds potentially being misallocated to day-to-day spending, and it’s possible that not all the planned investment actually materialises. Even so, the ex-post numbers will likely be large enough to move the growth dial, which should start to become more visible from next year. The Ministry of Finance’s medium-term fiscal plan projections from a few months ago confirmed the scale of increase, with net new borrowing set to multiply next year (relative to recent years’ levels), and parliament will shortly vote on the 2026 budget. Similar to the wider EU bloc, consensus GDP estimates are suggesting a below-trend pace of GDP growth next year, which might be too pessimistic given the size of the planned spending.

Wider fiscal impulse

There has also been a spending shift across the continent. The main driver of this behaviour may have been Mr. Trump’s demands that Europe should be paying for its own defence, but it also followed on from last year’s Draghi report, which provided several recommendations on how to close the growth – or innovation – gap with the US and China (one of which was reforming the defence industry).

Perhaps unsurprisingly, then, the defence industry seems to have gained fiscal traction. Almost all European NATO members agreed to raise their defence spending targets to 5% of GDP by 2035 earlier this year, and more anecdotally, defence companies have expressed interest in idle auto manufacturing plants across the continent. There are also signs of progress towards military equipment standardisation: Franco-German authorities have reportedly been pressing industry leaders to resolve their issues over the stalled flagship fighter jet project, and more positively, they recently signed an agreement to develop a sovereign early warning system (a US one is currently used).

The announcement of the European Commission’s ReArm Europe Plan / Readiness 2030 in March was arguably the most significant defence-related development (excluding Germany). As its name suggests, the plan aims to build a ‘credible’ EU defence readiness by 2030, through various coordinated initiatives. It has already led to the EU relaxing its fiscal rules – defence spending carve-outs were introduced – and initial demand for its defence loan initiative, Security Action for Europe (SAFE), was strong. Overall, the ReArm plan could unlock around €800 billion in defence spending over a multi-year window – almost 4.5% of EU GDP (although, it may include a few non-EU nations) – with several of its projects set to launch next year.

There has nevertheless been economic debate around the impact of defence spending on GDP growth, with claims that it carries a low ‘fiscal multiplier’ (i.e., the increase in overall output would be smaller than the equivalent change in defence expenditure). The supposed rationale is that some of these funds may be allocated to investments with a ‘low shelf life’ (or, those with few ‘positive spillovers’): for example, producing a tank that is then shortly destroyed on the battlefield. Yet, it’s worth remembering that the production of military equipment – however durable – still creates output, a job and a source of income. Spending will also be directed to other areas within defence, such as collaborating on procurement and R&D, which should lead to innovation and ultimately support Europe’s long-term economic growth prospects.

Defence is not the only part of EU spending likely to see significant stimulus. Decarbonisation is an area in which a structural acceleration in spending seems likely. Europe is over reliant on imported gas – 2022 was a potent reminder – and it remains committed to its ‘net zero’ goals. To achieve its more pressing 2030 goal of reducing net greenhouse gas (GHG) emissions by 55% (compared to 1990 levels), the additional green investment needed in the EU is estimated to be roughly €477 billion per year, according to the European Commission (that is over 2.5% of EU GDP). The European Council also recently agreed to target a 90% reduction in net GHG emissions by 2040, before achieving ‘net zero’ by 2050, both of which are likely to require even greater investment.

Finally, rebuilding Ukraine’s infrastructure in future will require European involvement: the World Bank estimated that the direct damage was around €170 billion as of the end of 2024, and the US had requested for Europe to commit $100 billion (~€87 billion) as part of its (initial) 28-point peace plan.

Conclusion: Cautiously optimistic

While there are likely to be (a lot of) bureaucratic hurdles during the journey, European spending seems poised to get a boost, perhaps as soon as 2026. It seems a little unusual, then, that those EU GDP growth estimates have not responded to these fiscal developments, particularly as other cyclical developments seem supportive of growth as well: the European Central Bank deposit rate has halved (and is in fact negative in inflation-adjusted terms); household balance sheets remain healthy; some of the peripheral economies have been performing strongly; US tariff risk has been dissipating; the US dollar decline – which has dampened local exporters’ earnings this year – has tentatively stabilised.

From a stock market standpoint, the MSCI Europe ex UK and Switzerland index has actually matched the US benchmark this year, even in local currency terms, though the former has lost significant momentum (in relative terms) since the first quarter of 2025. Analysts are still expecting EU corporate earnings to grow in double-digit territory over the next couple of years – and while earnings usually grow faster than GDP, this seems more upbeat than what those lacklustre economic projections suggest.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more Wealth Management UK articles

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.

-

Stories from the road

Quarterly Letter

Through deep research and direct engagement with businesses, we seek high-quality companies with strong competitive advantages, disciplined capital allocation and the ability to compound wealth over time.

-

Bringing the right advisers together

Insights

Significant wealth brings complex financial and personal decisions. Rothschild & Co helps coordinate trusted advisers, ensuring aligned, objective guidance, long-term planning and access to specialist expertise through a personalised advisory board.

-

Five stock market talking points in 2026

Strategy Blog

Global equities rose despite geopolitical tensions, as markets looked through near-term risks. AI infrastructure spending drove returns and earnings growth, valuations sent mixed signals, and corporate activity remained subdued but showed signs of recovery.

-

The next UK Prime Minister

Strategy Blog

Following Keir Starmer’s resignation, Andy Burnham has emerged as Labour’s likely successor. Despite political uncertainty, markets remain calm, with economic and geopolitical trends outweighing domestic politics. Significant policy change appears unlikely.

-

SpaceX: Infinity and beyond?

Strategy Blog

Markets are preparing for a wave of megacap IPOs led by SpaceX, amid strong AI-driven optimism. While liquidity should absorb issuance comfortably, questions remain around valuations, passive investing, concentration risk and index influence.