Middle East conflict

Geopolitical risk has surged anew. The possibility of escalation is clear and daunting, but the range of potential outcomes may not be as one-sided as it seems, and investors have long been aware of this specific risk. As we have sadly had reason to note often of late, grim humanitarian and political developments are not always accompanied by financial upheaval. The impact on global oil, shipping, and capital markets has so far been small. More dramatic disruption, though possible, is not inevitable.

Higher oil prices are the most obvious way in which such events might affect capital markets. Brent Crude prices have recently risen by almost a tenth, to $75 per barrel, but remain below their year-to-date high, and are unremarkable when viewed relative to their inflation-adjusted trend. Stock markets have been remarkably stable: the MSCI World index has only edged lower by 1% since Friday in dollar terms. There is no sign of a “flight to safety” in global bond markets, which are also little changed.

The price of oil could yet rise more substantially, particularly if conflict spreads to nearby major oil-producing countries, or if flows in the Strait of Hormuz – a key trade route between the Persian Gulf and the Gulf of Oman, which takes around a fifth of global oil consumption – are halted. Some commentators have suggested that the latter event might almost double the price of oil, for a while at least, in which case the economic implications and likely market reaction would be more severe. However, scenarios also exist in which the price of oil falls, rather than increases further.

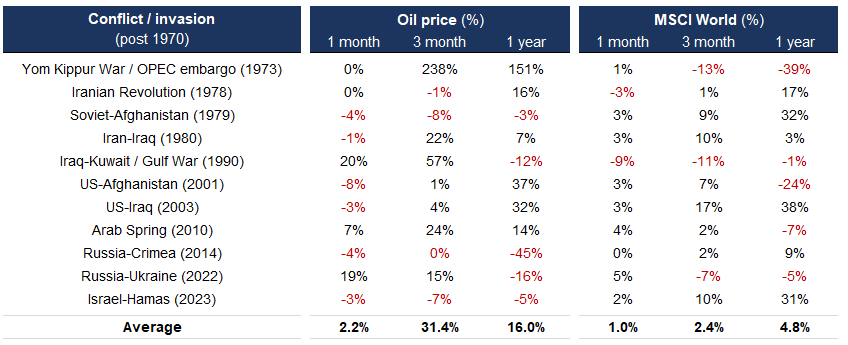

The table below reminds us of several historic instances since 1970 in which troubling developments seemingly left stock markets relatively unmoved or even higher. The various wider economic and market contexts will have differed, of course.

Figure 1 | Selected geopolitical events: oil and stock market movements

(USD, %)

Source: Rothschild & Co, Datastream, MSCI

The Yom Kippur War in late 1973 – and the subsequent oil embargo by the Organization of Arab Petroleum Exporting Countries – had the greatest initial impact on oil, which quickly tripled in nominal terms (at a time when oil was a more important input than it is today). It was also associated with a big stock market fall (though as noted, economic circumstances were different, and the oil price may not have been the only cause of the fall): the MSCI World Index was down by almost 40% a year after the war started. Oil prices also surged, and stock prices fell, in the first few months after Iraq’s invasion of Kuwait.

However, stocks rose in the year after Iraq launched a full-scale invasion of Iran in 1980 – coinciding with US interest rates peaking – and when the US entered Iraq in 2003. More recently, Russia’s invasion of Ukraine was followed by relatively modest and brief moves, while the attack in October 2023 was followed by lower oil costs and higher stock markets.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.