Growth Equity Update

February 2025 – Edition 35

- ‘We are so back baby.’ Matt Turk of Firstmark: Despite DeepSeek, AI continues to dominate VC fundraising and at rapidly growing valuations. It is widely reported that Anthropic is close to a $2bn raise at a $60bn valuation that would be twice that of November 2024; and that SoftBank is close to a $40bn investment in Open AI at a $260bn pre money valuation, implying Open AI has added c$1bn a day to its value since its $6.6bn round at a $157bn valuation in October 2024.

- Infused with AI: AI infuses the start-up scene so far in 2025. We look at the Stargate Project led by OpenAI and Softbank which plans to invest $500bn in building new US AI infrastructure; at President Macron’s announcement that private sector companies have pledged to spend €109bn on AI initiatives in France; and at the General Catalyst led ‘EU AI Champions Initiative’ announced at the Paris AI summit and dedicated to investing €150bn in European AI in the next five years.

- Secondary market appetite strong: The Forge Global private marketplace is seeing the proportion of expressions of interest to buy private market secondaries at the highest level it has been since the end of 2020.

- Markets in 2025 - Inversion of trends: Eventful markets (tariffs, divergence in US European rate cuts, DeepSeek) have seen a turnabout in relative US/European index performance. Ytd to 7th February the European STOXX 600 up 7% and the FTSE100 up 6% lead the S&P 500 up 2.7% with NASDAQ and the Magnificent Seven up just 1%.

- January - another strong month for VC raises: Our Deal Monitor recorded 35 US deals at $100m or more in January for a total of $11.3bn. European VC saw 65 raises of $20m+ for a total of $4.9bn, the biggest month since September 2023.

- ‘What is thinkable is also possible.’ Wittgenstein

Click here to download a PDF version of Growth Equity Update

Growth equity – 2025 marked by AI led exuberance

“We are so back baby” Matt Turck, Firstmark Group

In January’s Growth Equity Update we made a series of predictions about the Venture Capital/Growth Equity markets for 2025. Two of those predictions were that the scale of venture capital investment would grow again in 2024, and that artificial intelligence would be the leading sector with its influence growing and widening.

At the end of January, the revelation that the Chinese open source DeepSeek R1 AI large language model had been developed at very low cost without access to US semiconductors and technology might have been expected to disrupt these predictions. Indeed, in public markets to the 7th of February we have seen an inversion in the recent hierarchy of index performance with the relatively tech-light Euro STOXX600 and FTSE 100 outperforming the tech-heavy NASDAQ and Magnificent Seven in the US.

Despite this, the two-tier market that has emerged in venture capital - AI and everything else - continues. The DeepSeek phenomenon appears to have been embraced, absorbed and the optimism about AI’s power to transform industries and valuations has moved on. Some indicators of the present mood of the private markets:

- The last three months of 2024 saw a substantial pick up in US VC fundraising activity with the Rothschild & Co Deal Monitor recording three successive months of $16bn+ raises. These were led by a flurry of major AI raises. Q4 saw raises from Databricks ($10bn), OpenAI ($6.6bn), xAI ($6bn), Anthropic ($4bn), Perplexity ($500m), Physical Intelligence ($400m), Vultr ($333m), Sandbox AQ ($300m), Liquid AI ($250m), Writer ($200m) and Tessl ($125m).

- In January Anthropic raised a further $1bn of funding from Google and is widely reported to be close to a further $2bn raise to be led by Lightspeed at a valuation of $60bn. This would double the $30bn valuation established in its $4bn raise in November 2024 and more than treble the $18bn valuation at its $750m raise in January 2024.

- Widespread press reports suggest that SoftBank is close to making a $40bn primary investment in Open AI at a $260bn pre money valuation. The intention is that the money would be paid out over the next 12-24 months. That valuation level would imply that -DeepSeek notwithstanding – Open AI has added c$1bn to its valuation each day since its last $6.6bn round in October 2024 at a valuation of $157bn.

- Separately a group of investors led by Elon Musk has submitted a $97.4bn bid for the nonprofit entity that controls Open AI eliciting the response from Open AI’s Dam Altman that the platform ‘is not for sale.’

- The scale of the turnaround in Softbank’s appetite to invest is something to behold. In its Q1 2022/23 figures to end June 2022 it announced a 3.16 trillion yen ($23.4bn) net loss at the group level which followed on from a 2.1 trillion yen loss in the March quarter. At that time SoftBank CEO Masayoshi Son commented ‘For new investments, we have to be more selective.’ In FY 2021 Softbank made $44.3bn of new investments. In FY22 that fell to just $3.1bn (and $2.2bn of that was in Q1). Nevertheless, at its full year press conference SoftBank's CFO Yoshimitsu Goto commented he ‘can't explain clearly how excited’ Son is about the new opportunities presented by AI. In early 2025 Softbank appears about to invest $40bn in Open AI – almost equivalent to its entire investments in 2021. In addition, it is one of the core backers of the Stargate Project, a new company which intends to invest $500bn in the next four years building new AI infrastructure for OpenAI in the United States. Softbank is the core partner with financial responsibility and Masayoshi Son is the chairman.

- In May 2024 chief scientist and co-founder Ilya Sutskever left OpenAI and started his own company, AI research lab Safe Superintelligence. In September 2024 it raised $1bn in a deal led by Andreessen Horowitz and Sequoia, valuing the business at $5bn. Safe Superintelligence is now widely reported to be in discussions to raise funding at a $20bn valuation. The company has a mission statement that it aims to build AI models that surpass human intelligence while remaining aligned with human interests. It is though yet to unveil any technology or products. The business has no revenues.

- Defense technology start-up Anduril is widely reported to be raising $2.5bn at a valuation of $28bn. This would be around double the valuation it commanded in August 2024 when it was valued at $14bn. Anduril does have revenue – around $1bn in 2024. It signed a partnership with OpenAI in December to deploy AI systems for ‘national security missions’.

- The ability of private companies to raise substantial funding at generous valuations is reducing the impetus for them to consider IPO. Companies such as fintech Stripe confidently raise primary and provide liquidity for staff in secondary deals. As its CEO John Collinson has remarked ‘With the IPO, we’re not in a rush. Businesses which are profitable have many, many more options than businesses which are dependent on outside capital.’

What a change in mood from November 2022 when FTX collapsed and March 2023 when Silicon Valley Bank went bankrupt.

As that wry commentator of the VC industry, Matt Turck of Firstmark Group observes, ‘We are so back baby’.

What about investor mood? Here are some perspectives - sourced from Pitchbook, Forbes and elsewhere – on the current mood amongst VC investors and market participants.

The first is from Andreessen Horowitz, is about a year old, addresses AI and its enthusiasm for it, and looks pretty prescient.

"The potential size of this market is hard to grasp — somewhere between all software and all human endeavours"

At Target Global founder and partner Shmuel Chafets comments:

"2025 should be a year of AI adoption at scale. We’ll see AI integrated more deeply into day-to-day business operations and consumer life."

Allocate is a Palo Alto based VC platform. Co-founder Hana Yang comments:

"As we enter a transformative technology supercycle driven by advancements in artificial intelligence, alongside a reset in capital markets and improved operating efficiencies, 2025 is poised to be one of the most dynamic and interesting vintage years for the innovation economy."

There is awareness of the risks of over exuberant valuations for AI assets but limited appetite to call a halt to them in the near term.

Evgenia Plotnikova, a general partner at Dawn Capital comments:

"A buoyant public market and high dry powder in venture means there is likely to be an even greater divide between public and private valuations, with the latter at times defying gravity. While the jury is still out on whether those high valuations are justified and just how much AI can eat into the global knowledge work economy, we are unlikely to see a trough of disillusionment in 2025."

A view echoed by Tobias Bengtsdahl, a partner at VC incubator and accelerator Antler Group:

"Even though the AI bubble is inflating quickly, don’t underestimate how important it is to have actual traction—meaning paying, returning users. Too many founders think they can put AI in their pitch deck and raise a round, but investors are still risk-averse after the downturn and want to see real numbers."

On the broader state of venture capital markets, Jeannette zu Fürstenberg, managing director at General Catalyst comments:

"We are bullish on Europe and expect VC dealmaking to show steady growth in 2025. Europe is at a pivotal moment: Its deep technical talent, rich industrial heritage, and global leadership in applied AI create the perfect conditions for transformative innovation."

General Catalyst has (see Growth Equity Update November 2024) a new concept of a broader partnership with founders which states ‘to achieve outsize impact using applied AI and global resilience to address what we believe are the world’s great challenges, we must also transcend the traditional definition of venture capital.’ It is the leader of the ‘EU AI Champions Initiative’ announced at the recent Paris AI summit in which over 70 organisations with more than $3 trillion in market capitalisation are dedicated to investing €150bn in European AI in the next five years.

Equation Capital is a fund of funds co-founded by former Lakestar partner Mark Schmitz. It invests in up-and-coming VC funds which it believes will shape the European startup ecosystem. He comments:

"We see a lot more fund managers deploying capital at the intersection of science and commercialization. Technology enabled by scientific breakthroughs is now seen as more than just an investment opportunity. It also serves to promote sovereignty of nations and creates competitive advantages for business…[in] 2025 we continue to back ambitious solo GPs and micro-VCs with a strong thematic focus on frontier tech. Areas of particular interest include robotics, next-gen computing, synthetic biology and energy transition."

Charlotte Palmer, Vice President at Integra Global Advisors which serves ultra-high net worth families and charitable institutions observes:

"We see 2025 as one of the most opportune vintages in recent years for venture capital investment. Founders and investors capitalized on the unique conditions following the dot-com bubble and 2008 financial crisis, and today’s environment presents a landscape of innovation and opportunity as well."

Some see AI as changing the nature of the venture capital investment business. Aakar Vachhani, managing partner of Fairview Capital, an independent advisor focused on GP-led secondary solutions comments:

"In 2025, LPs will begin to see how agentic AI will transform the venture capital and startup ecosystem. AI-driven efficiencies are poised to lower barriers for startup formation and accelerate iteration and value creation."

We have noted in successive Growth Equity Updates that the flow of money into VC funds has become more concentrated in the larger firms. Pitchbook data suggests that the top 30 funds raised 75% of all venture capital in the US in 2024. Albert Azout, managing partner at Level Ventures muses on the potential consequence:

"Second-tier Series A/B firms will die out as they cannot compete with multi funds firms like a16z, Accel, Sequoia, etc. We believe that in the future a segment of startups will skip Series A/B rounds and go straight to growth rounds, given their ability to get to scale on limited amounts of capital."

Europe and the US – Fuelling AI investment

EU AI Champions, InvestAI, the Paris AI Action Summit and Stargate

The last month has seen a series of announcements to promote scale AI investment across the US and Europe.

Three notable announcements in Europe were centred around the Paris AI summit at the start of the month.

EU AI Champions Initiative: A group of venture capital firms, corporations and start-ups have joined together in the ‘EU AI Champions Initiative’. Over 70 organisations with more than $3 trillion in market capitalisation are involved. Supporters of the initiative, which is led by General Catalyst include venture backed companies including Helsing, Eleven Labs, Flix, GetyourGuide, Omio, Mistral AI, Personio, Pigment, RobCo and Loft Orbital. Public companies backing the scheme include Airbus, ASML, Siemens, Infineon and Philips. The group is calling for greater investment in AI infrastructure and less regulation. The project sees twenty institutions investing €150bn in European AI over the next five years.

The mission statement of the group is:

"The initiative aims to frame a positive vision for Europe by mobilizing talent and capital, accelerating AI adoption in established industries, and increasing European companies’ competitiveness. Led by General Catalyst our mission is to foster a resilient partnership between incumbents and technology providers to unlock Europe’s full potential in AI. Europe can seize a generational opportunity by leading in applied AI, integrating it into Europe’s industrial base to boost productivity, resilience and economic sovereignty, particularly in key sectors like manufacturing, energy and defence."

The group’s manifesto is here: An-Ambitious-Agenda-for-European-AI

Its ideas for applications across industries include how generative AI could boost Europe’s productivity, featuring examples like Novo Nordisk using AI and Cradle for therapeutic discovery, Loft Orbital and Helsing developing an AI-powered defence intelligence system, and SAP and Mistral AI reinventing enterprise software.

Generative AI could add $575bn to the European economy by 2023

InvestAI -€50bn of incremental EU backing: At the Paris AI summit the President of the EU Commission, Ursula von der Leyen, announced a €50bn EU initiative dubbed InvestAI to supplement the EU AI Champions Initiative including a new European fund of €20bn for AI gigafactories saying ‘This large AI infrastructure is needed to allow open, collaborative development of the most complex AI models and to make Europe an AI continent.’

France - €109bn of AI investments in five years: At the start of February the AI Action Summit was held in Paris bringing together world leaders to discuss the future of AI. The conference was attended by, amongst others, Sam Altman of Open AI, Dario Amodei of Anthropic and Demis Hassabis of Google DeepMind.

Ahead of the summit French President Emmanuel Macron announced that private sector companies have pledged to spend €109bn on artificial intelligence initiatives in France.

Contributors to this total include the MGX fund from the United Arab Emirates which has pledged to invest €30- €50bn for a new campus for data centres. Brookfield, the Canadian alternatives firm, announced €20bn of funding to support the development of AI infrastructure in France. Apollo Global another alternative asset manager, is contributing $5bn for AI energy-related investments.

Two data centre businesses have pledged backing for the scheme. Digital Realty, a real estate investment trust which is focused on data centres, has pledged €6bn to expand its presence in Paris and Marseille while Equinix will invest €630m for new data centres in Paris and Bordeaux.

The AI cloud platform FluidStack has signed an MoU with the French government for an AI supercomputer scheme with an initial investment of €10bn. It expects to be operational by 2026.

France’s state investment bank, and mainstay of its venture capital scene, Bpifrance, has announced a €10bn investment programme as part of the initiative. Bpifrance is already a significant investor in the French AI companies Mistral, H and Poolside. Its new investment will focus on three main areas -foundation models, AI infrastructure companies, and hardware firms developing specialised AI semiconductors.

President Macron described the funding initiative as ‘the equivalent for France of what the US has announced with Stargate'.

The Stargate Project: So, what has the US announced? The Stargate Project, announced in January, is a new company which intends to invest $500bn in the next four years building new AI infrastructure for OpenAI in the United States.

It is a gathering of the technology clans with some powerful financial backing. The initial equity funders in Stargate are SoftBank, OpenAI, Oracle, and MGX, the Abu Dhabi based fund investing in AI initiatives. SoftBank and OpenAI are the lead partners for Stargate, with SoftBank having financial responsibility and OpenAI in charge of operations. Masayoshi Son of SoftBank is the chairman. Arm, Microsoft, NVIDIA, Oracle, and OpenAI are the technology partners.

The new company was announced by President Trump who dubbed it 'the largest AI infrastructure project by far in history' saying it would help keep 'the future of technology' in the US.

The companies announced an immediate $100bn of funding and revealed that its first data centre is already under construction in Abilene, Texas. It is one of an initial ten datacentres each of 0.5m square feet to be built. The revenue model and what products and services are to be offered are yet to be disclosed.

The proposed Stargate Project investment is separate from the widely reported potential $40bn funding that Softbank is proposing to invest in OpenAI at a valuation of $300bn. That valuation level would imply that -Deepseek notwithstanding – OpenAI has added more than $1bn to its valuation each day since its last $6.5bn round in October 2024.

Public markets – inversion at the start of 2025

So far in 2025: An eventful start to the year in markets has seen a turnabout in the performance of indices with the US lagging and Europe leading the way. Ytd to the 7th of February the European STOXX 600 is up 6.6% with the UK’s FTSE100 up 5.7%. The S&P 500 is up 2.7% with the NASDAQ lagging at a rise of 1.3%. The Magnificent Seven index is up just 1%.

The key influences year to date have been:

US interest rate expectations. As expected, the Fed left interest rates unchanged at 4.25%-4.5% at its meeting on January 28th. The Fed noted that US inflation remains ‘somewhat elevated’ omitting its previous statement that ‘progress’ was being made towards its target 2% inflation rate. Fed Chair Jay Powell said that the Fed would need to see ‘real progress on inflation or some weakness in the labour market before we consider making adjustments.’

Subsequently the January figures showed the US added 143,000 jobs in January – short of predictions of 170,000 but following an upwards adjustment of the December figure from 256,000 to 307,000 and with a 10bps fall in the unemployment rate to 4%. These numbers appear to bolster the Fed’s view that interest rates do not presently need to fall.

President Trump indicated before the Fed meeting that he felt interest rates should fall ‘a lot’. After the meeting he noted that ‘Holding the rates at this point was the right thing to do.’ His new Treasury Secretary, Scott Bessent, has indicated that Mr Trump’s real focus is that long term rates – notably 10-year US Treasury yields - should come down. Mr Bessent commented on Bloomberg News that as the Trump administration’s policies of ‘energy dominance, deregulation and non-inflationary growth’ make their impact, the 10-year US Treasury yield is ‘going to naturally come down’.

The impact of tariff announcements: Feeding into the debate on the level of short-term rates is the potential impact of tariff actions by the Trump administration. As one commentator has noted - each of the past three weekends have seen President Trump announce a 25% tariff on something or someone – first Colombia, then Mexico and Canada, and then on steel and aluminium imports.

The official line from the Fed is that tariffs have not yet had an impact and are not factored into the current thinking with Mr Powell saying that on policy decisions the Fed will ‘patiently watch and understand and see how it plays out’.

Some of the individual Fed policymakers have noted that, at the very least, the imposition of tariffs may make it difficult to determine what is deriving inflation. So Chicago Fed President Austan Goolsbee in early February identified a series of supply chain threats including ‘large tariffs and the potential for an escalating trade war’ noting that ‘If we see inflation rising or progress stalling in 2025, the Fed will be in the difficult position of trying to figure out if the inflation is coming from overheating or if it’s coming from tariffs.’

Separately Boston Fed President Susan Collins observed that some of the tariff proposals are taking decision makers into uncharted territory. ‘We have limited experience of such large and very broad-based tariffs…. There are many different dimensions, and there are second-round effects as well, which make it particularly hard to really assess what the amounts would be ... We don’t know what the time frame would be that would cause a rise in a price level.’

The markets presently expect rates to be held at the Fed’s March meeting and again in May but there is an expectation, albeit not a certain one, that there will be a further 25bps cut at the June meeting. The Official Fed dot plot looks for 50bps of cuts in 2025.

This excellent analysis from Rothschild &Co strategists Kevin Gardiner and Anthony Abrahamian highlights the potential impacts of some of the Trump administration’s initiatives:

Trumponomics – an overview of the headline policies

Interest rate cuts elsewhere: Faltering confidence in the pace and scale of US interest rate cuts may have impacted the progress of the US indices but the opposite effect is being felt in Europe.

The ECB continues its campaign of rate cuts in response to signs of economic stagnation in the Eurozone. At the end of January, it cut interest rates for the fourth month in a row. The decision to cut rates by 25bps to 2.75% was unanimous and means that Euro rates have now dropped by 125bps from their recent peak of 4% in May 2024. Markets are factoring in another 75bps of rate cuts by the end of 2025 which would take rates down to 2%.

The ECB’s action is in response to disappointing growth statistics which indicated that the Eurozone slid back to zero economic growth in Q4 2024, missing analyst forecasts of a 0.1% expansion and falling back from the 0.4% of Q3. Germany’s GDP fell by 0.2% in Q4. For 2024 as a whole the Eurozone economy grew by 0.7%. Expectations presently look for c1% growth in 2025 versus the IMF’s forecast for US GDP growth of 2.7%.

The UK: A similar picture of lower interest rates in response to low economic growth expectations is seen in the UK. In early February the Bank of England cut interest rates by 25bps to 4.5% having left them steady at 4.75% in its December meeting. Market expectations are for at least another 50 bps of rate cuts by the end of 2025 with a possibility (40%) that the figure might be 75bps – which would take rates down to 3.75%.

At the same time UK inflation is expected by the Bank of England to rise during 2025, hitting 3.7% in Q3 due to higher energy charges, well above the 2% target before falling back again in 2026 to c2.5% with the 2% target being reached in 2027.

The Bank of England accompanied the rate cut with a halving of its 2025 UK GDP growth forecast, coming down from its November forecast of 1.5% to just 0.75%. It looks for a recovery to 1.5% growth in 2026 and 2027. The overall effect was to boost the FTSE 100 index, largely due to perceived currency benefits of weaker sterling on overseas earners.

Deepseek and the ‘Lagnificent Seven’: The term Magnificent Seven for the group of leading US tech stocks was coined by the Bank of America strategist Michael Hartnett as recently as 2023.

In early 2025 the Chinese business DeepSeek emerged as a potential disruptor of the disruptors. Its R1 large language model is open source (rather than proprietary technology like OpenAI), is free to use ( challenging the subscription based business model of Western LLM companies), it has been developed at a fraction of the cost of US counterpart LLMs (perhaps for as little as c$6m) and has been created with limited access to US technology and semiconductors.

As a result, Mr Hartnett has now coined the term ‘Lagnificent Seven’ to reflect the view that the challenge imposed by DeepSeek, combined with heady starting valuations and headwinds to the US economy, will mean the Magnificent Seven underperforms other US sectors and international stocks in 2025.

It is not as yet a view necessarily widely shared. A Bloomberg Markets Live Pulse survey of 260 investors conducted at the end of January found 88% of the respondents saying that the DeepSeek R1 model will have little or no impact on the US tech majors. 63% said they had no plans to change their exposure to the S&P 500. 59% of respondents cited the actions of the Trump administration as a bigger catalyst than AI for stock performance in 2025.

DeepSeek though has shaken certainties. After its R1 model and its characteristics were publicised over the weekend of 25-26 January, the Magnificent Seven and Nasdaq fell 3% on January 27th (the S&P500 was down 1.5%, the FTSE 100 was flat). NVIDIA shares, arguably the most exposed given that DeepSeek had limited access to its GPUs, led the Magnificent Seven down that day dropping 17%. The Mag 7 index has travelled sideways since but is still marginally up on its start year levels.

The group of stocks has broken into two. Meta (+19% ytd) and Amazon (+4%) have outperformed. The rest are down on the year with Apple -7%, NVIDIA -6%, Tesla -5% and Microsoft and Google down 2%.

Intentions to spend heavily on AI capex remains in place with Meta planning $60-65bn of spend in 2025 up from c$40bn in 2024 including an AI data centre ‘so large it would cover a significant part of Manhattan’ with CEO Mark Zuckerberg saying 2025 ‘will be a defining year for AI’ .

Microsoft will spend $80bn in 2025 on AI and anticipates lower cost means of accessing AI as positive for customer use of its applications. Alphabet agrees with $75bn of planned AI spend in 2025, up over 40% on 2024, and CEO Sundar Pichai saying ‘The cost of actually using [AI] is going to keep coming down, which will make more use cases feasible.’

Amazon has indicated that its capex, most devoted to AI, may top $100bn in 2025. CEO Andy Jassy commented:

"The vast majority of that CapEx spend is on AI for AWS …We think virtually every application that we know of today is going to be reinvented with AI inside of it and with inference being a core building block, just like compute and storage and database."

Nvidia shares rallied on the back of these post DeepSeek reiterations of substantial AI spending.

Apple and Tesla shares are less closely focused on AI developments. The relative weakness of Apple shares is more focused on the potential impact of the 10% tariffs on imports from China announced by the Trump administration given its heavy reliance on Chinese production. Tesla shares - strong performers since the re-election of President Trump - have weakened as the administration suspended federal funding for the buildout of electric vehicle chargers in the US and on the back of weaker Q4 earnings. Nevertheless, assertions by Elon Musk that 'I'm not saying it's an easy path, but I see a path for Tesla being the most valuable company in the world by far' may have limited the fall in the shares.

Reactions to the Magnificent Seven are important in a venture capital/Growth equity context because the group captures many of the themes that are driving the VC sector, notably the heavy investor commitments to AI businesses such as the LLM players (Open AI, xAI, Anthropic, Perplexity, Mistral), data centres (Vantage, Crusoe, Coreweave, XEnergy, Nscale), AI applications (SafeSuperIntelligence, AlphaSense, Glean, Scale AI, Clio, Helsing, H), autonomous vehicles (Wayve, Waymo, Cruise), semiconductors (Tenstorrent, Groq, Rivos, Hailo), and AI for dedicated industries like Biotech (EvolutionaryScale, Xaiira Therapeutics).

Perhaps surprisingly in this context the FTSE Venture Capital Index which measures the performance of the US venture capital industry, with a strong sector weighting towards technology, is up 10% ytd at 22,477, just 6% off its highs of August 2021. It has sustained a long rally since early September 2022.

The continued strength of the index may reflect the possibility that the ‘commoditisation’ of AI represented by the DeepSeek initiative may be favourable to those companies using AI inference models to build applications. It may also reflect the continued determination of VC investors to support the existing leaders in the industry, typified in the last month by reports that Softbank plans to invest a further $40bn in Open AI at a valuation of c$300bn.

Rothschild & Co strategist Kevin Gardiner thinks the prospect of further significant market gains are becoming less likely in 2025. He summarises the current key drivers of the market in this graphic:

Forge Global – Private Market outlook for 2025

Forge Global’s synopsis is that private markets are being shaped by emerging technologies, surging interest in artificial intelligence and continued valuation adjustments post the private market fall out of 2021.

Forge Global, the leading global private securities marketplace, recently released its market outlook for 2025. Forge is a leading player in secondaries and private markets data. Its synopsis is that private markets are being shaped by emerging technologies, surging interest in artificial intelligence and continued valuation adjustments post the private market fall out of 2021. Forge Report - Q1 2025 Investment Outlook

Its key predicted themes going into 2025 are:

A revival of IPOs: Forge’s December 2024 Private Market Update reveals an expanding IPO pipeline in the second half of 2024, bolstered by a potentially more relaxed regulatory environment. Forge data suggests an increasingly optimistic outlook with the 2025 IPO pipeline showing signs of revitalization with several established unicorns making meaningful moves toward public exits in 2025.

A bigger year for VC fundraising: As we noted in the last Growth Equity Update VC funding, particularly in the US, finished the year very strongly. Forge identifies a ‘hopeful tone’ for fundraising in the coming months citing ‘In early-2025, the fundraising climate in the private market is showing signs of re-acceleration, coupled with divergence. Early-stage funding remains resilient, with investors focusing on sectors like AI, climate tech, and biotech. However, late-stage funding rounds face valuation corrections as public market comparables exert downward pressure.’

More up rounds: The Forge data indicates that up rounds heavily predominated over down rounds in Q4 2024. The chart distributes the outcome of the rounds with reference to the year of the company’s previous raise. Interestingly more than half of the Q4 up rounds were from companies that had already raised in the last two years – the impact of positive momentum and potentially a more realistic starting valuation. By contrast companies that saw down rounds were most likely to have previously raised in 2022. In previous quarters, most down rounds were concentrated among companies that last raised during the 2021 valuation bubble.

US VC rounds – More than 50% of Q4 2024 up rounds had raised within the last two years

Strong secondary market appetite: Not a prediction, but the secondary market appetite for private assets quoted on the Forge system was strong towards the end of the year. The chart shows the balance of indications of interest on the exchange. The proportion of expressions of interest to buy (the darker bar) were at about 75% of the total by the end of the year. This is at the highest level it has been since the end of 2020. As with so much else in the private space. Forge attributes this to the intense interest in AI names as well as to the effect of Space X’s December 2024 tender offer.

Forge Markets- Highest buy side interest since 2020

January – a strong start to the year for US and European VC raises.

2025 has started strongly for the venture capital/Growth Equity market on both sides of the Atlantic. Our Deal Monitor recorded 35 deals at $100m or more in the US in January raising a total of $11.3bn. This was almost three times the amount raised in January 2024 and continued the strong trend at the end of 2024 when each of the October, November and December months saw c$16bn of fundraises.

The largest sectors in January 2025 were metaverse (a single $3bn raise for Infinite Reality), biotech ($2.5bn, led by $1bn for RetroBiosciences) and AI ($1.25bn, led by $1bn for Anthropic).

In Europe our Deal Monitor recorded $4.9bn of raises in Europe in January, up 14% on January 2024 (which was the biggest month of 2024) and 2.5x the level of January 2023. The top sectors were Biotech ($1.1bn), Healthcare ($1.05bn) and ClimateTech ($674m).

The US – $11.3bn of US venture backed raises of $100m+ in January

Notable raises in the US in January included:

Infinite Reality is ‘powering the next generation of commerce, creativity and connection through AI and immersive technologies.’ It offers immersive technologies in digital media and e-commerce to brands and creators to get better audience engagement and ultimately monetisation. The company has made multiple acquisitions in the last year, notably the $450m Landvault purchase in July ( Landvault has built over 1.2m square feet of virtual experiences for brands), the $250m acquisition of the Drone Racing League, the $75 million purchase of Ethereal Engine, the $45m acquisition of UK based XR platform and creative studio Zappar and, post this raise, the purchase of virtual shopping platform Obsess. The $3bn fundraise, which was largely backed by a private investor with a global technology/real estate portfolio, valued the business at $12.25bn.

DeepSeek’s arrival on the AI LLM scene with a high-performance model developed at a miniscule cost compared with those of the US AI leaders sent public investors in AI related businesses, particularly Nvidia and the large data centre companies, scurrying for cover. Nevertheless, private investors continue to offer significant funding to US AI businesses. Anthropic is understood to have taken a further $1bn of funding from Google. This follows its $4bn raise in November 2024 at a valuation of c$30bn which in turn came after its $750m raise in January at a valuation of c$18bn. The company is widely reported to be close to a further $2bn raise to be led by Lightspeed at a reported valuation of $60bn.

Showing that the appetite for the US AI model appears undimmed, widespread press reports suggest that SoftBank is in talks to invest c$40bn in OpenAI. This would mean SoftBank would overtake Microsoft as OpenAI’s largest single investor. OpenAI’s most recent raise was for $6.6bn led by Thrive Capital in October 2024 at a valuation of $157bn.

Helion Energy, a private company backed by OpenAI’s Sam Altman, raised a $425m Series F also supported by Lightspeed and Softbank Vision 2. Helion is a nuclear fusion business and is deemed safer than nuclear fission (it generates electricity by forcing atoms together in a magnetic field rather than splitting them apart). These are long duration businesses requiring success in the laboratory to be translated to success in commercial power plant conditions. Much of the excitement in Helion Energy is linked to the association with OpenAI and the company’s deal with Microsoft which plans to have it supplying commercial scale energy to Microsoft by 2028 – just three years away.

The revival in Biotech raises was noted in our December update ‘One of the features of 2024 has been the resurgence of biotech deals. In 2023 there were 13 deals of $200m or more in US biotech raising $3.2bn. In 2024 there were 17 such deals raising $5.7bn.’

January kept up this strong trend with $2.5bn raised for biotech companies including three raises of more than $200m (Kardigan, $300m for cardiovascular drug development; Aviceda Therapeutics, $208m for ophthalmic for geographic atrophy; Tenvie Therapeutics, $200m for small molecules for neurological diseases). In addition, Retro Biosciences raised a $1bn Series A for its work on anti-ageing, age related diseases and conditions. Again, a notable investor in the round was OpenAI’s Sam Altman.

Europe: In 2024 the VC market in Europe had a strong start to the year with the value of raises up 36% yoy at $17.7bn by the end of H1. The value of raises in H2 then fell by 12% yoy leaving the year as a whole up 7.5% at $34.2bn. January was the single month with the highest fundraising total in 2024 at $4.3bn.

Nevertheless, this level was exceeded in January 2025 with the value of European raises hitting $4.9bn across 65 deals of $20m+. In total there were 15 deals of more than $100m, a greater number than in any month in the last two years. It was the biggest month for European VC fundraising since September 2023 and, prior to that, June 2022.

Notably more than 40% of that total was made up by raises in Biotech ($1.1bn) and Healthcare ($1.05bn) including five of the top ten deals.

The largest of these was the $410m Series A at Verdiva Bio backed by Fortion and General Atlantic. Verdiva has developed a GLP1 peptide for obesity and cardiometabolic disorders. Neko Health, a preventative screening service whose body scans are used to detect cancers, cardiovascular disease and other conditions was co-founded by Spotify founder Daniel Ek. Its $260m Series B was backed by Lightspeed Venture Partners and will allow it to increase the number of scanning centres in London and Stockholm and elsewhere. The company has a 40,000-person waitlist (including me for the last three months) for its £299 scanning service.

Climate Tech remains a prominent sector in Europe. January’s largest deal was for the German battery energy storage systems business, Green Flexibility. Private Equity group Partners made a €400m equity investment as part of a broader €1bn package of funding. Green Flexibility has a project pipeline of over 10 GW. The firm's first projects are already in construction.

We observed in the December Growth Equity Update that 2024 was a strong year for raises in travel and booking management software with five deals raising $1.3bn including $570m from Travelport which competes with Amadeus and Sabre; a $500m Series C in Lighthouse (formerly OTA Insight). A commercial intelligence platform for the hospitality industry; a $110m raise for Visit Group’s supplies collaborative commerce software to ‘experience vendors’ and $110m to Mews for its SaaS based software tools to hotels.

Kinnevik led a $104m Series D raise for TravelPerk, the Spanish business travel platform in January 2024 at a valuation of $1.4bn. Travel Perk offers a comprehensive platform aimed at SMEs allowing them to book, manage and report all their domestic and international travel. TravelPerk has raised again in January 2025 with a $200m Series E round at a valuation of $2.7bn. The round accompanied the acquisition of Yokoy, an AI-led provider of expense, invoice, and card payment processing software. The round was led by Atomico and supported by Noteus Partners, Kinnevik and General Catalyst.

Eight deals in Travel software applications in 2024/5 raising $1.8bn

There was one big AI raise in Europe in January, Synthesia raising $180m at a valuation of $2.1bn, up from $1bn in its previous 2022 raise. The round was led by NEA supported by WiL, Atlassian Ventures, PSP Growth, GV and MMC Ventures. Synthesia uses AI to create realistic avatars turning plain text into lifelike videos. The applications are B2B, being used typically for corporate videos and training and by staff looking to turn PowerPoint presentations into videos. The company has 60,000 customers, most on a subscription basis and the business sells into 60% of the Fortune 100. In the year to December 2023 revenues were £24.7m with an operating loss of £27.9m. The valuation of $2.1bn is c67x 2023 revenues.

Europe - $4.9bn of raises in January 2025- Strongest month since September 2023

Our views on the state of the venture capital markets

The combination of global inflation, rising interest rates, and increased geopolitical risk substantially impacted the venture capital market in 2022 and 2023. 2024 saw some adaptation to the ‘new normal’. The refocusing of venture backed companies to achieve a better balance of growth, profitability and cash flow and the delivery of interest rate cuts have led to increased optimism and enthusiasm for growth equity.

Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment led to a sharp impact on valuations in private markets. The scale of the fall in the FTSE Venture Capital Index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023 and slow recovery in 2024.

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models, the applications of AI and industries (data centres, semiconductors) supporting the development of AI.

- Enthusiasm for AI and related technologies has driven the overall level of the FTSE Venture Capital Index back to within 6% of its highs of August 2021.

- Outside the AI space the VC market is selectively regaining confidence with a revival of interest in fintech, biotech and software being notable. Certain investors remain very active in the space with substantial funds to deploy. There remains substantial dry powder in the VC industry

- The speed of the investment process has slowed since 2021-22. The level of diligence on new deals has stepped up.

- 2023 and 2024 saw more down rounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these.

- It seems likely that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses.

- Valuation priorities have shifted with investors having moved away from an emphasis on revenue growth and revenue multiple emphasis. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and an emphasis on DCF and comparative based multiples.

Read the previous editions:

May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024, January 2025

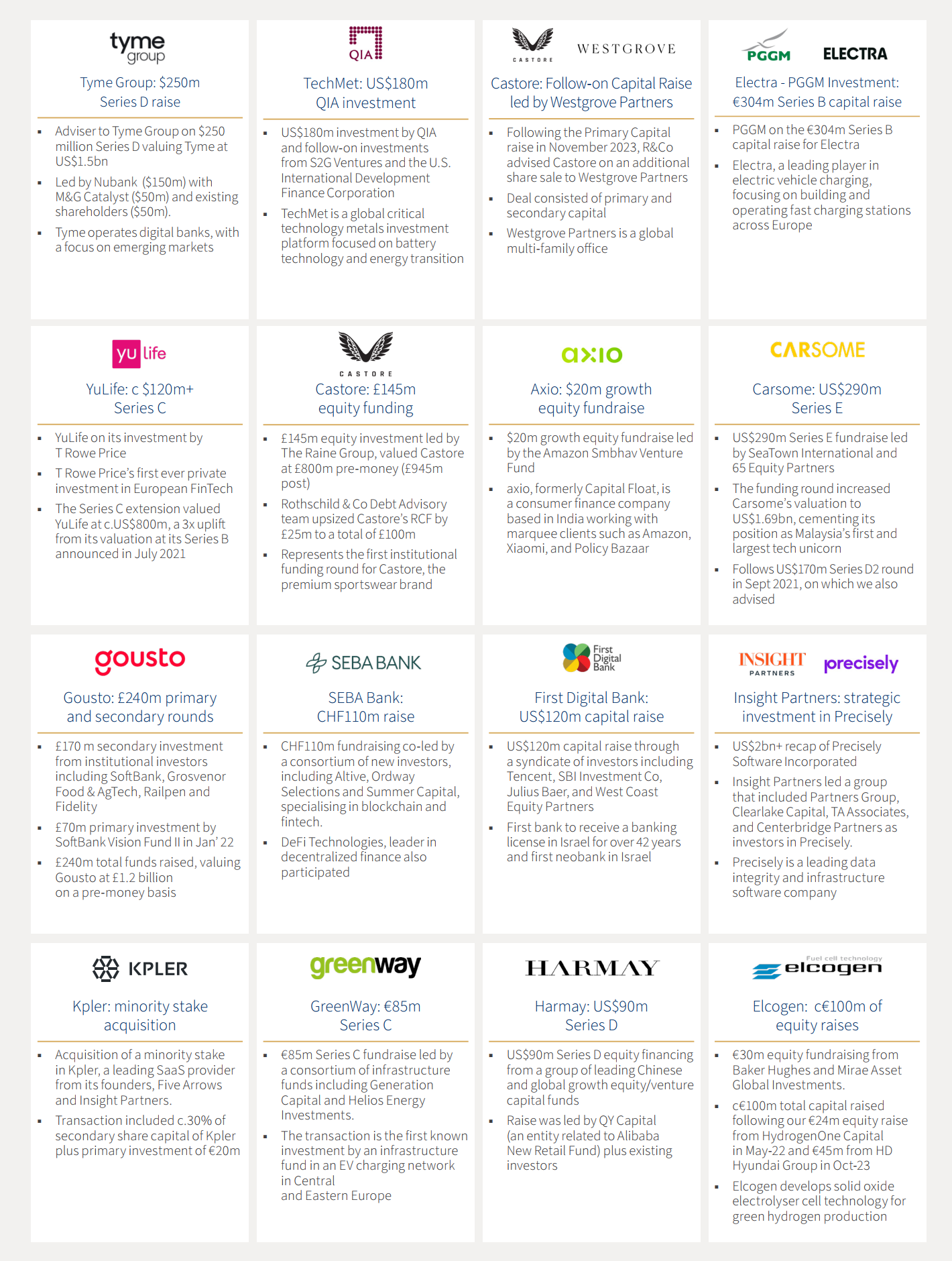

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Chris Hawley

Global Head of Private Capital

chris.hawley@rothschildandco.com

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Advisory

patrick.wellington@rothschildandco.com

+44 20 7280 5088

+44 7542 477 291

Mark Connelly

Head of North American Equity Markets Solutions

mark.connelly@rothschildandco.com

+1 212 403 5500

+1 917 297 5131

Thomas Chung

Head of Private Capital, North America

thomas.chung@rothschildandco.com

+1 212 403 5559

+1 917 594 7208