How much money do I need to retire?

What you need to know

- No two retirement plans look the same, but make sure you have enough money to achieve your goals

- Using an investment strategy that delivers above-inflation returns could be a good way to ensure your wealth is preserved

- Cashflow forecasting can help you to choose an approach that best meets your vision of a comfortable retirement

- At Rothschild & Co we invest our clients' wealth in high-quality companies that we believe will grow over the long term

What does your dream retirement look like? Some people hope to travel the world, indulging their appetite for adventure. For others, it's about reacquainting themselves with hobbies and passions that have taken a back seat during a busy career. Many people simply wish to spend more quality time with their loved ones.

You may want to do all of these things – and more. After all, you've had a successful career and earned it.

Whatever your aspirations may be, it's likely you'll be asking yourself one key question: do I have enough money to fund the lifestyle I want in retirement?

You’ll also need to be aware of the eroding effect of inflation, which can reduce the real value of your wealth. This is why our investment strategies focus on outpacing inflation over time, rather than a particular index.

The best way to ensure you have an adequate nest egg for the future is through prudent retirement planning and wealth management. To calculate how much money you and your family will need, we analyse your finances and future expenses using cashflow forecasting.

Planning your ideal retirement

There are many life events that may prompt you to think more carefully about your retirement plans. The sale of a business, for example, or your adult children flying the nest and starting families of their own. Perhaps you're thinking of retiring early?

Most people know that the earlier you begin saving for retirement, the better. But life can be unpredictable, which is why it's important to be prepared for a range of scenarios.

Cashflow forecasting can provide you with a better understanding of your financial situation and what you need to do now to achieve your retirement goals.

Considering your current lifestyle and expectations for the future is the first step. When would you like to retire? Are you hoping to fully retire or continue working in some capacity? Do you plan to buy a property or make other large purchases? How much can you afford to gift to your children and still have enough to live comfortably?

Using these and other insights, a cashflow forecast can model multiple 'what if?' retirement scenarios based on the savings, investments and pensions you have in place, as well as sensible assumptions about their long-term performance.

We find that this type of analysis can be eye-opening, giving them a clear illustration of how even small changes to their financial planning today can have tangible outcomes for their income and wealth in retirement.

Cashflow forecasting can provide you with a better understanding of your financial situation and what you need to do now to achieve your retirement goals."

'Can I maintain my current standard of living?'

One client was hoping to retire in the next few years but wasn't sure whether they were on track to save enough money to maintain the lifestyle they wanted.

Their current financial situation was as follows:

- A nest egg of £4.5 million, comprising ISA, pension and general investment portfolios

- £1.3 million in cash

- An annual income of £2 million

- An affluent lifestyle – total living expenses of £300,000 a year

Upon retirement, the client wanted to purchase a new property and expected £150,000 would be needed each year for living expenses.

The client planned on gifting £1 million to each of their two children when they turned 30 (one this year and one in two years’ time).

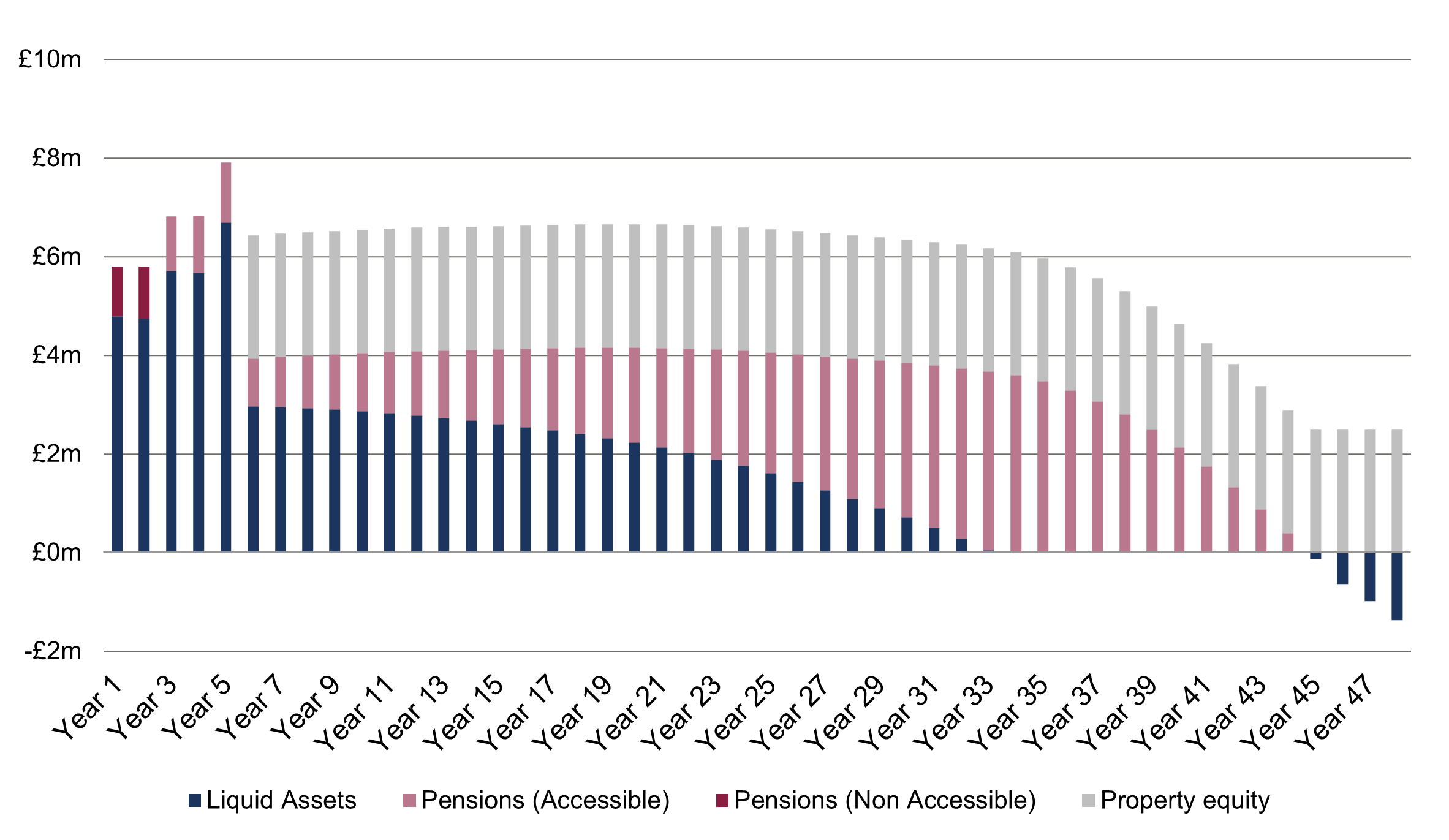

Our cashflow forecasting explored two possible scenarios – retirement in two years and four years.

If the client retired in two years' time, their wealth would total approximately £6 million, including a £2.5 million property and £150,000 a year spending money.

This scenario would allow them to retire sooner, but after 20 years, they would have less than £2.5 million of their original £6 million wealth and they would need to draw from their pension.

If instead they retired in four years, they would be able to set aside approximately £8 million. What's more, their wealth would grow ahead of inflation such that they wouldn’t need to touch their pension (and it could be left to their children), even after buying a £2.5 million property and maintaining the £150,000 a year living expenses. This is based on their investments achieving their return objectives.

The client also had concerns around market volatility, so we modelled a conservative third scenario (shown below) where their investments fell by 20% in the same year they retire and purchase the property:

Despite the considerable market fall, the client would still have sufficient liquid wealth to support their lifestyle for 44 more years, ignoring the property.

Boosting your retirement pot

After seeing a cashflow forecast, people are often surprised to learn that their current savings won't afford them the lifestyle they were expecting in retirement, especially if they are hoping to pass their wealth on to the next generation.

Fortunately, it's never too late to top up your retirement pot.

As our case study above shows, delaying retirement allows you to continue boosting your savings with income, while also benefiting from the power of compounding in your investments.

Even a few extra years can have a significant impact on how long your money will last once you retire. Of course, we recognise that working longer is not always possible or desirable. For example, you may be aiming to retire after receiving an offer to sell your business.

Cashflow forecasting can provide you with a better understanding of your financial situation and what you need to do now to achieve your retirement goals."

A cashflow forecast can help you decide whether the transaction price will be sufficient to cover your needs. If not, you may need to adjust your retirement expectations.

Whether you're working longer, selling a business or boosting your savings in other ways, it's also important to ensure your money isn't being whittled away by inflation in the meantime. Inflation can have a dramatic eroding effect on your wealth, particularly over many years in retirement. At Rothschild & Co, we invest our clients' wealth in high-quality companies and funds that we are confident will grow sustainably ahead of inflation.

By seeking to preserve your wealth first and foremost, and using tools such as cashflow forecasting to guide the conversation, we hope to provide reassurance that your nest egg is in safe hands, both as you approach retirement and throughout your golden years.

If you’d like to learn more about how our investment strategy can help your retirement planning, please get in touch today.

Ready to begin your journey with us?

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more articles

-

The US consumer: mixed signals

Strategy Blog

Should we give US consumer spending the benefit of the doubt? Real wage growth has continued while rising interest rates have not affected all households in a consistent way. In this strategy blog we take a look at the health of the US consumer market.

-

The perils of making predictions

Quarterly Letter

History is littered with examples of people making predictions that later turned out to be inaccurate. How can we become better at forecasting the future? Our Quarterly Letter delves into this topic to investigate some of the perils of making predictions.

-

Rothschild & Co’s UK Wealth Management business names James Morrell as Deputy CEO

Press releases

The newly created Deputy CEO role will provide increased capacity at a senior level to help meet the growing demand for Rothschild & Co’s wealth management services from existing and future clients.

-

Rothschild & Co wins Western Europe's Best Bank for Advisory from Euromoney

Awards

This is the second consecutive year we have been named Western Europe's Best Bank for Advisory, reflecting the breadth of our capabilities across M&A and financing advisory across the region.

-

Is small beautiful again?

Strategy Blog

Large companies have typically offered far more attractive returns than their smaller counterparts, but that has changed recently. What’s behind the reversal? In this strategy blog we examine the reasons behind the switch and whether this trend is likely to continue.

-

A mid-year review with our CIO and Global Investment Strategist

Perspectives podcast

A mid-year review on the main macroeconomic developments and how our strategies have perfomed with our CIO Dr. Carlos Mejia and Global Investment Strategist Kevin Gardiner.