2023: it was the best of times, it was the worst of times

If 2022 was the market’s annus horribilis, 2023 has been an altogether better year. Economic resilience has surprised, if not humbled the more pessimistic commentators: growth has continued, and inflation has faded sharply. We are still awaiting the long-anticipated recession. Optimistic investors have been rewarded: global stocks were up over a fifth this past year (in US dollar terms), with most asset classes sharply recovering from their losses in 2022.

Yet the more hopeful economic and market backdrop has been in stark contrast to the tense and unsettling geopolitical developments – whether US political dysfunction, or more grave matters, including Russian hostilities and most recently the grim developments in the Middle East.

2023 reminds us that while misery and misfortune do not have always have a market impact, the business cycle always does. Here we explore a selection of market developments from the year gone by.

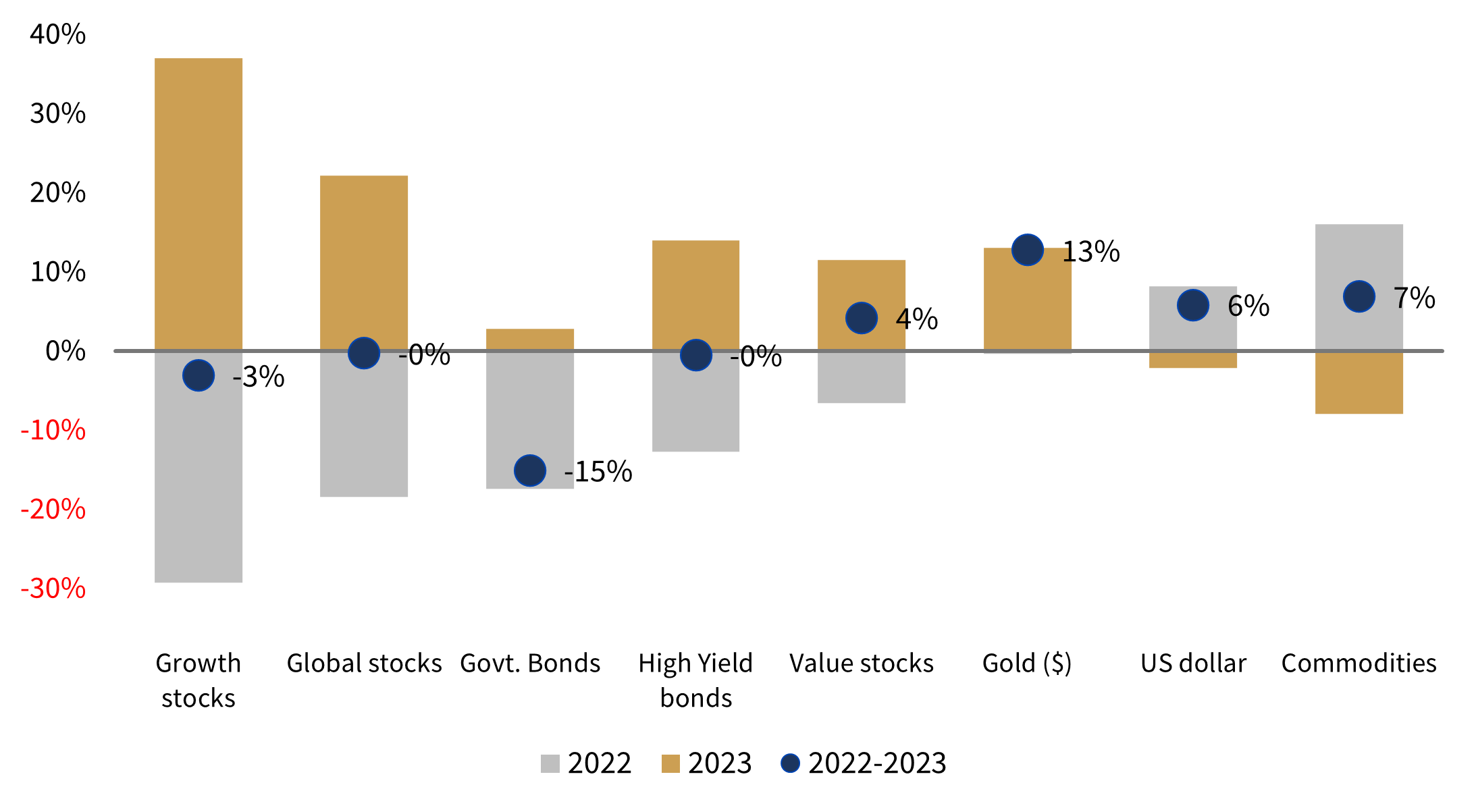

A better year for investors…

2023 returns ranked by 2022 total return

(% change in USD)

Source: Bloomberg, MSC, ICE BofA

Index returns shown on a total return basis in US dollars (unhedged)

2023 has been almost a mirror image of 2022, with most asset classes retracing their losses. As the adage goes, misfortune is virtue's opportunity. Last year wasn’t without its challenges: a short-lived banking crisis, choppy disinflation – threatened by a brief revival in energy prices – and the numerous geopolitical risks. But it was the threat of higher interest rates – the sharpest tightening cycle in four decades – that remained in the driving seat, shaping investor sentiment.

Stock markets marched higher, led by the US (see below), alongside speculative grade corporate bonds. Fixed income investors narrowly avoided a third consecutive year underwater – only made possible by the remarkable year-end rally in government bonds. Commodities retreated in 2023 – mostly driven by the big falls in energy prices – albeit gold bucked the trend. Bitcoin was one of the best performing assets, up 150%, but is still languishing at two thirds of its 2021 all-time high.

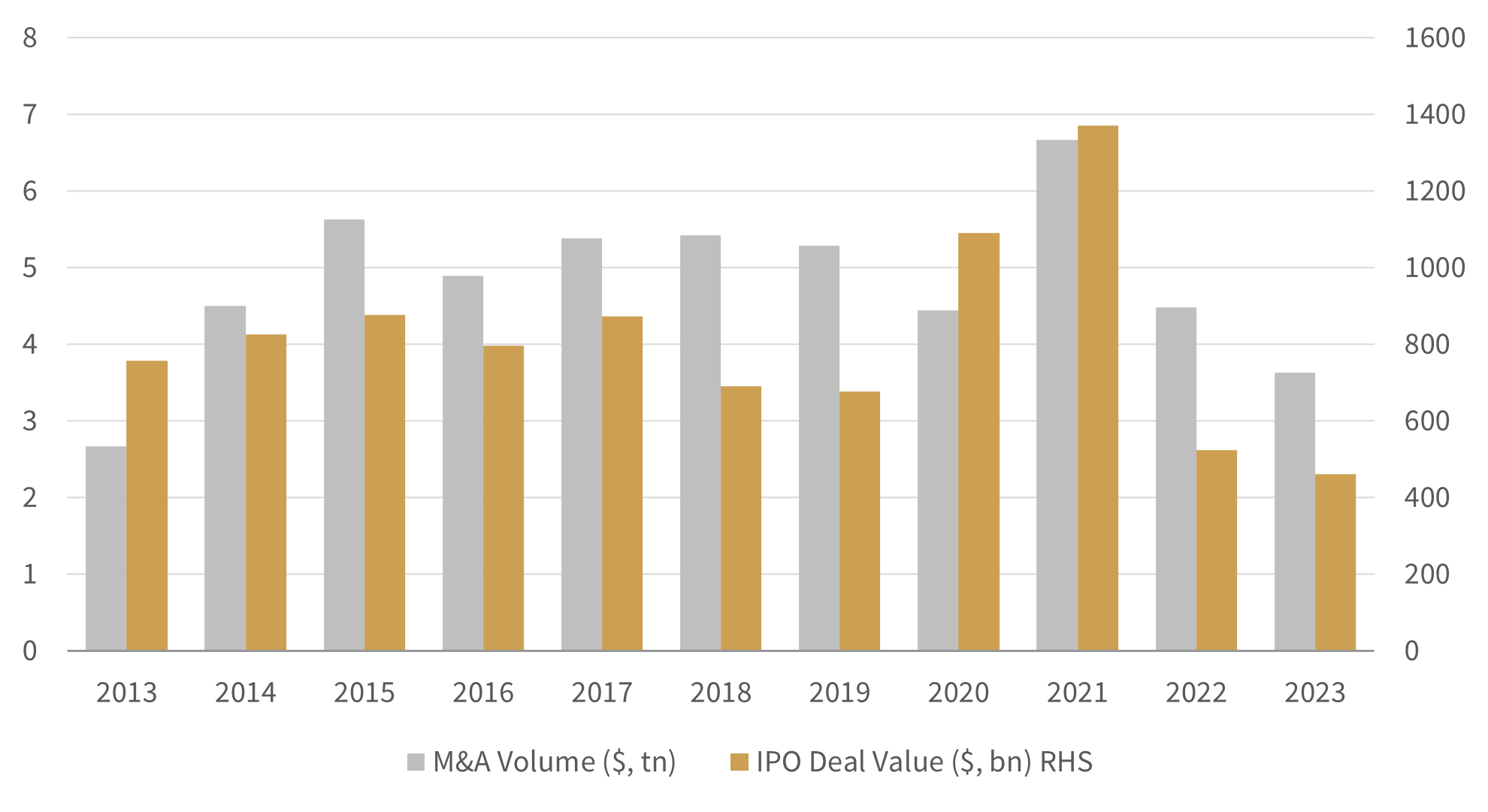

…but another lacklustre year for corporate activity

Corporate transactions: Global M&A volumes and Initial Public Offerings

Source: Bloomberg

In capital markets, the spectre of higher interest rates and uncertain (if unexpectedly resilient) economic backdrop led to a stasis in deal flow and volumes. Listings are on track for their most subdued year since the GFC, and M&A volumes are half the level they were two years ago.

Global corporate bond issuance (not shown) has been equally subdued - issuance of non-financial debt in 2023 looks set to have been the weakest a decade (2022 is also in contention). While some companies appear to have been putting new investments on hold and have not sought to raise new capital, the slowdown in activity partly reflects the fact that many companies took advantage of historically low yields in the preceding years, while extending the maturity of that debt further into the future. Ultimately, 2023 may well reflect a gradual normalisation in activity following a pretty buoyant period.

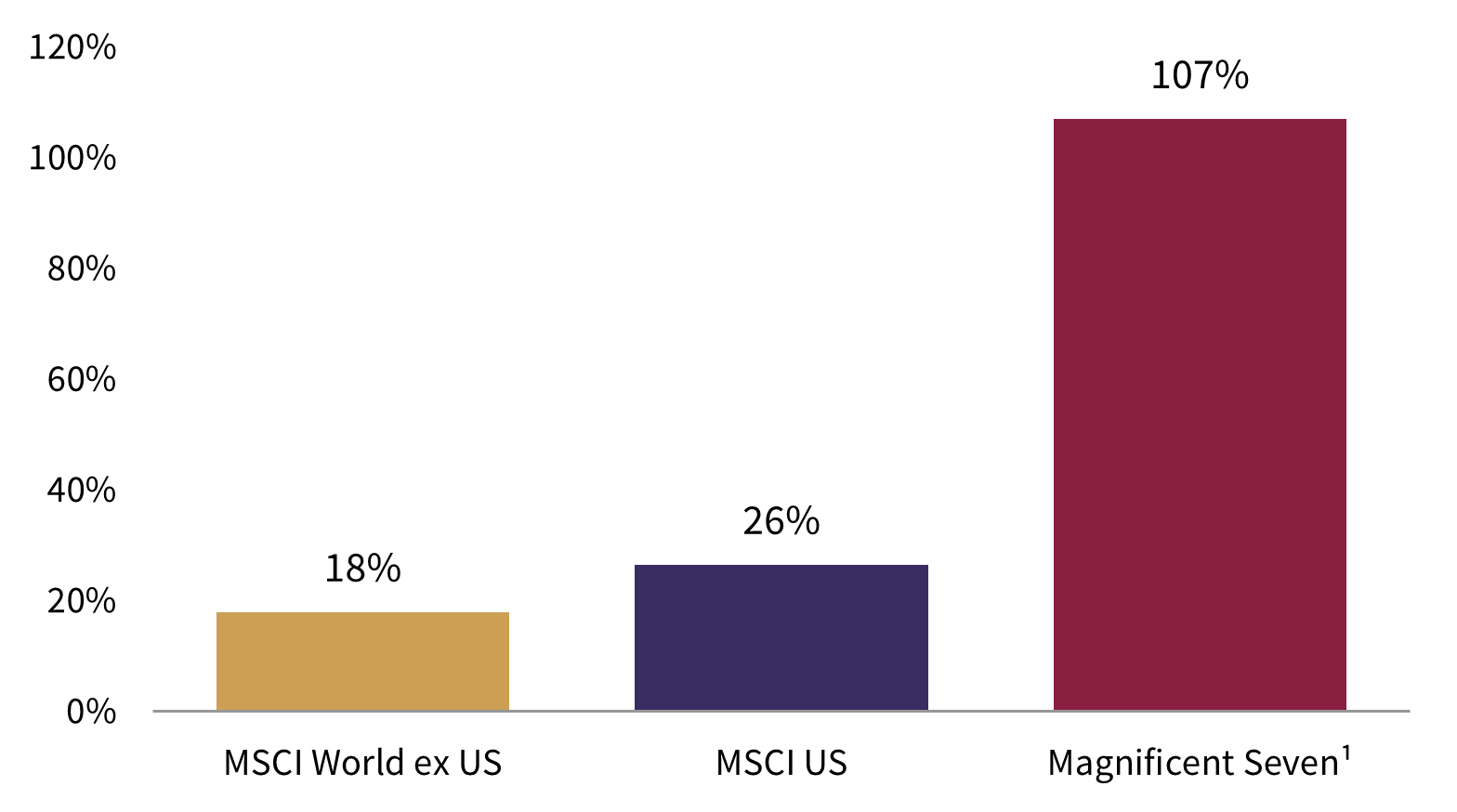

US exceptionalism and the Magnificent Seven

2023 total return

(% change in USD)

Source: Bloomberg, MSCI,

Index returns shown on a total return basis in US dollars (unhedged)

1 Magnificent Seven includes Apple, Microsoft, Amazon, Alphabet, Meta, Tesla and Nvidia

Most of 2023 was characterised by very narrow stock market leadership –- the US and it’s richly valued ‘technology’ juggernauts have been leading the market higher, with investors seduced by the promise of productivity-enhancing Artificial Intelligence. Through to the end of October, the US stock market’s 11% year-to-date return was entirely accounted for by the ‘Magnificent Seven’, while the average S&P 500 stock was down 3%.

However, risk appetite turned more positive in the final two months of the year and participation within the US market (and more widely) broadened. Cyclical sectors and smaller stocks started to outperform and the gulf between the leaders and laggards started to narrow – by year-end the average US stock concluded the year up 14%.

But despite this late year-end rotation, US exceptionalism persists: the US stock market has now outperformed the rest of the world in 10 out of the past 14 years.

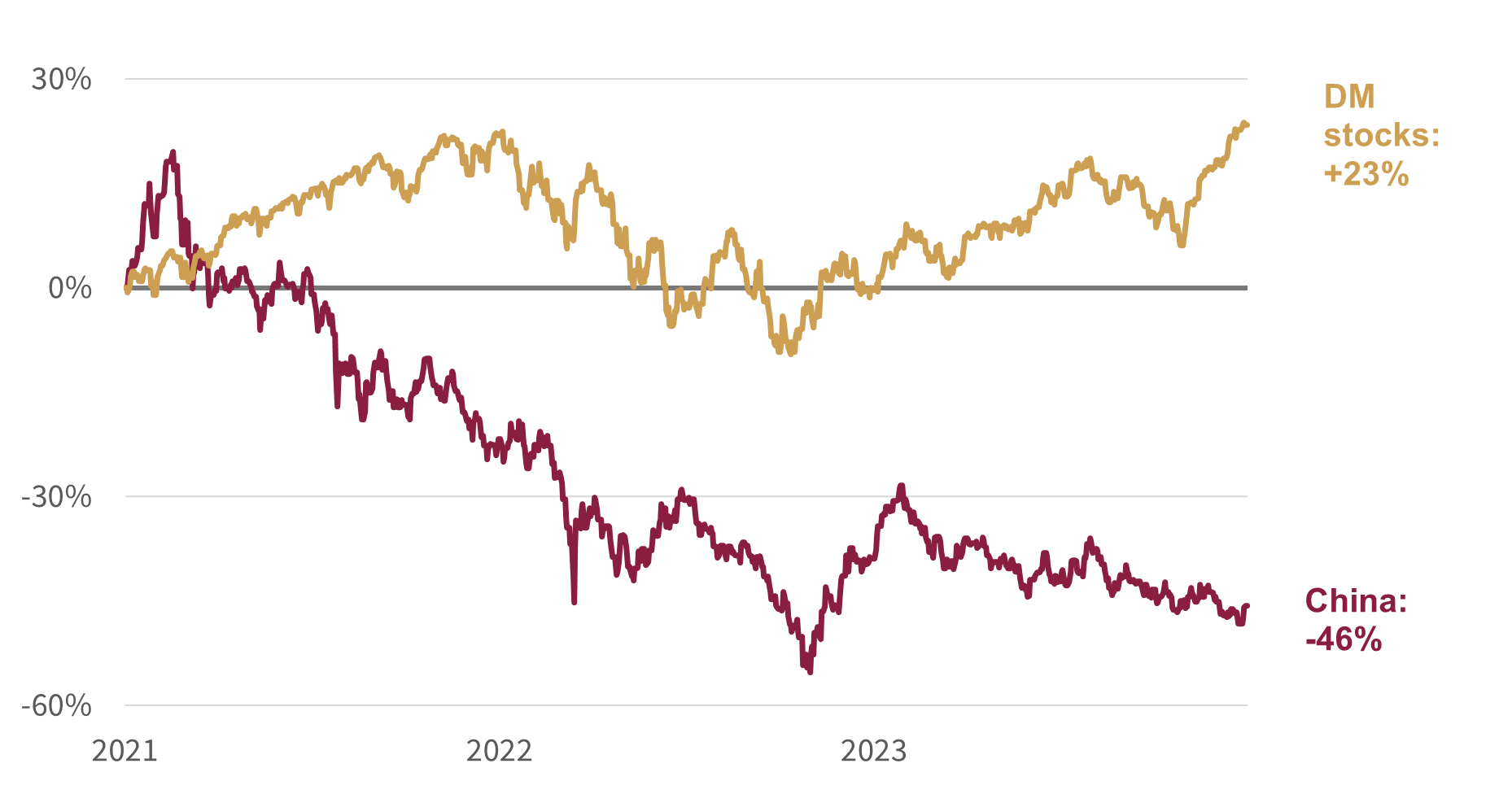

China: from disappointing to downbeat

MSCI World vs MSCI China cumulative total return: Jan 2021 to Dec 2023

(% change in USD)

Source: Bloomberg, MSCI

Index returns shown on a total return basis in US dollars (unhedged)

China is a clear example of how strong economic growth does not always translate to better stock market performance. The MSCI China index fell 11% in 2023 (in US dollar terms) and marks a three-year losing streak. Cumulatively, the index has almost halved since the start of 2021, and currently it represents just 3% of the (investable) MSCI all countries index – relative to the US, which stands at nearly two thirds. Pessimism, it seems, is endemic.

However, China’s economic prospects are encouraging. Despite property sector related woes, growth is on track to hit Beijing’s 5% target in 2023 – and a similar target is pencilled-in for 2024. Its stock market is cheap on most valuation measures – now the long-awaited revival in sentiment needs to follow…

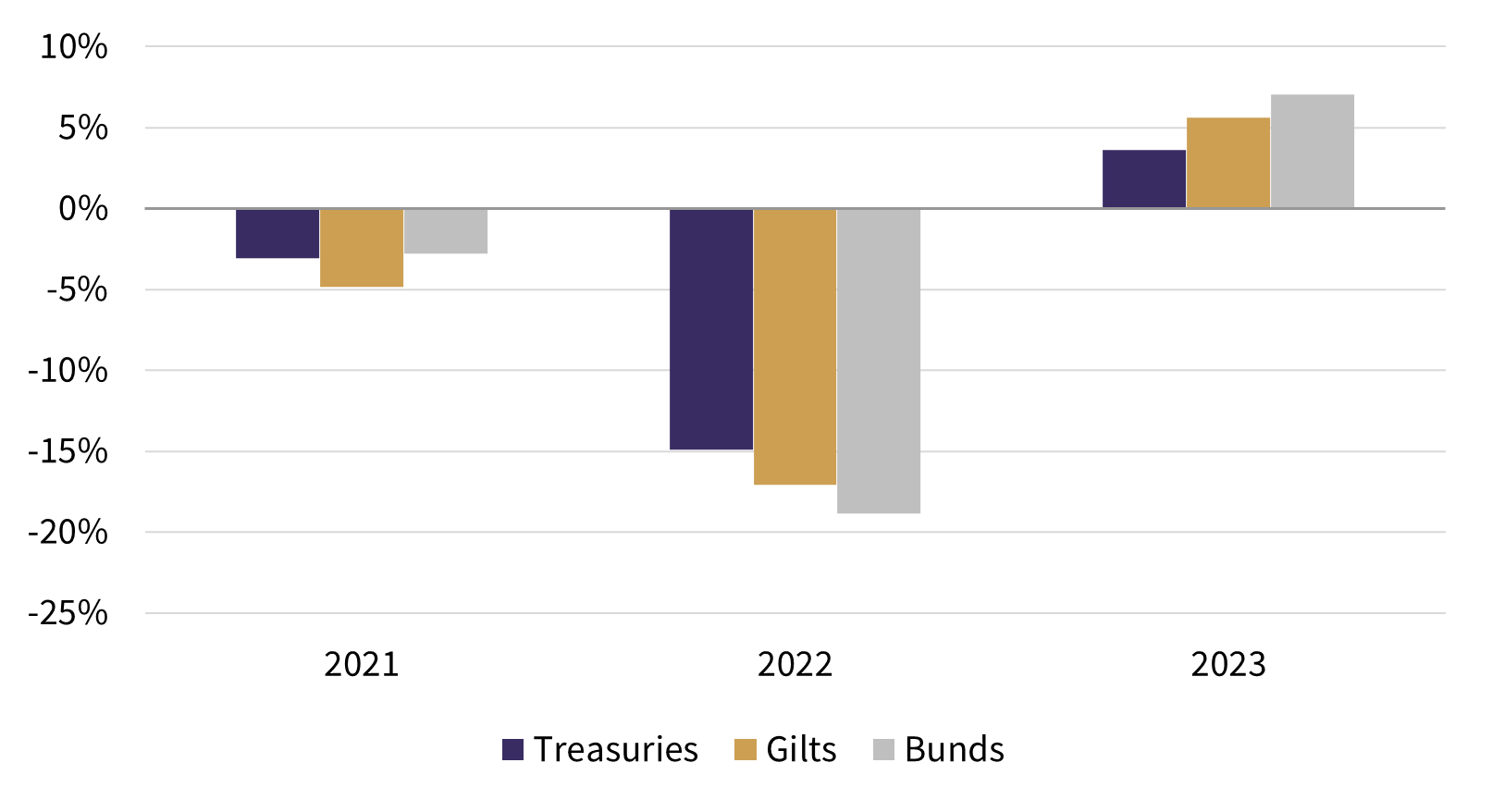

The bond bear market may be finally over

7-10 year government bond total returns: 2021, 2022 and 2023

(% change in local currency)

Source: Bloomberg

Even after the worst year (2022) in a generation for bond investors, it wasn’t until the final months of 2023 that bonds were on course to a deliver a positive return last year. Through to the end of the October, the US 10-year US treasury yield was close to 5% and the 10-year gilt yield close to 4.7%, both having risen over 100bps since the start of the year – driven mostly by the big revival in real yields.

But the bond vigilantes’ actions seem to have been relatively short lived – in the final two months of the year, G7 government bond yields fell sharply, delivering the best two-month return (+9%) since 2008. Ultimately, benchmark 10-year government bond yields ended the year at or below where they started it, with the US treasury at 3.9% (unchanged), the UK gilt at 3.5% (-13bps), and the German bund at 2.0% (-54 bps).

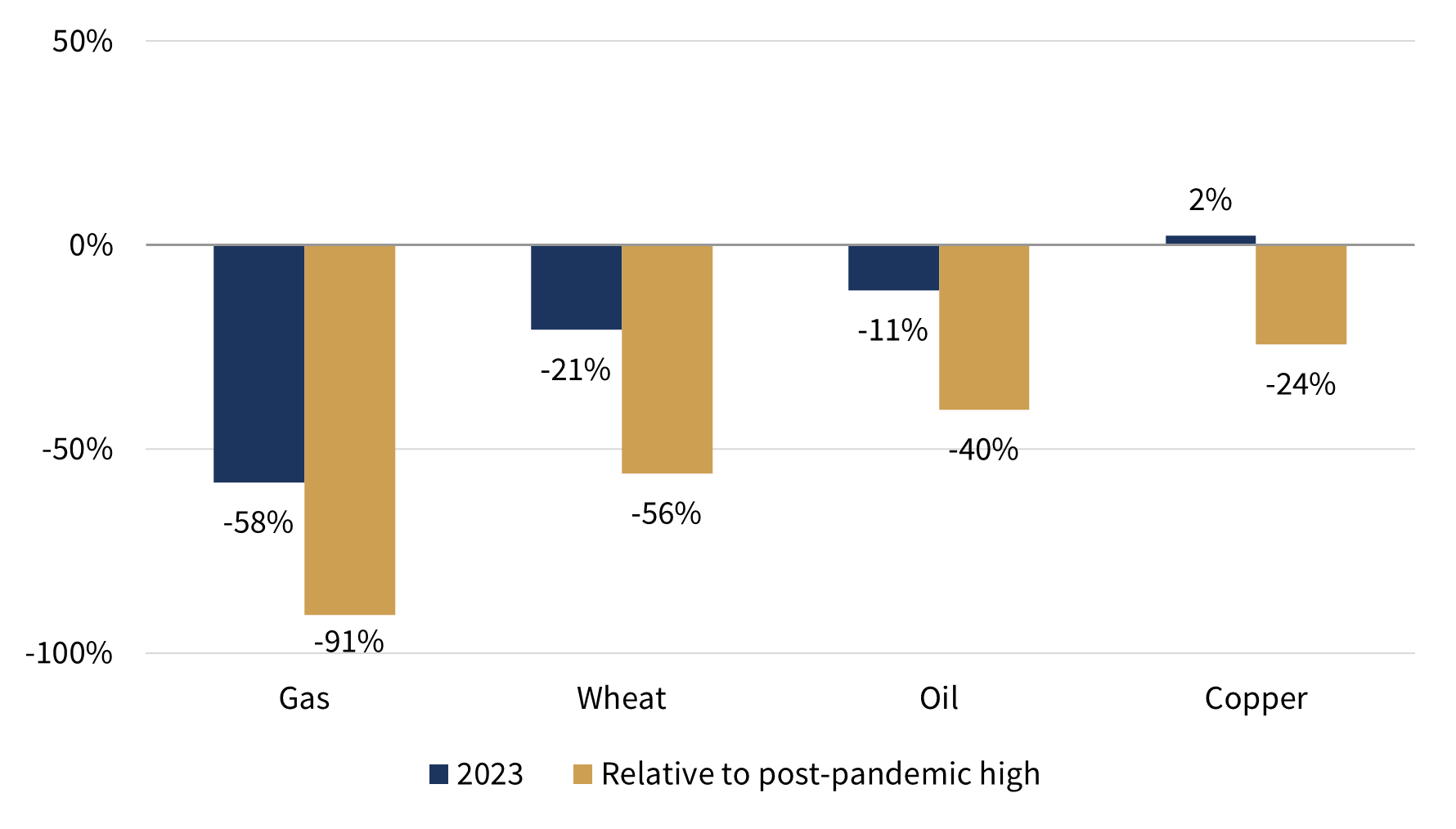

Commodity prices: slowly normalising?

Selected commodities: 2023 and relative to post-pandemic high

(% change in spot prices, in US dollar terms)

Source: Bloomberg

The commodity cycle continued to turn lower in 2023, following a frothy few years for goods’ prices and raw inputs. Most visibly we’ve seen big declines in oil this year, down over a tenth (despite OPEC’s best efforts) and European gas prices which have more than halved. Beyond that agricultural commodities and the industrial metals complex have also fallen.

While the gradual retreat in commodity prices is often viewed as a sign of softening growth, this latest bout of weakness reflects mostly improved supply – rather than a collapse in demand for raw inputs. One obvious (positive) impact is on consumer prices: goods prices (and not just volatile energy or food prices) are falling, and this deflation seems set to continue.

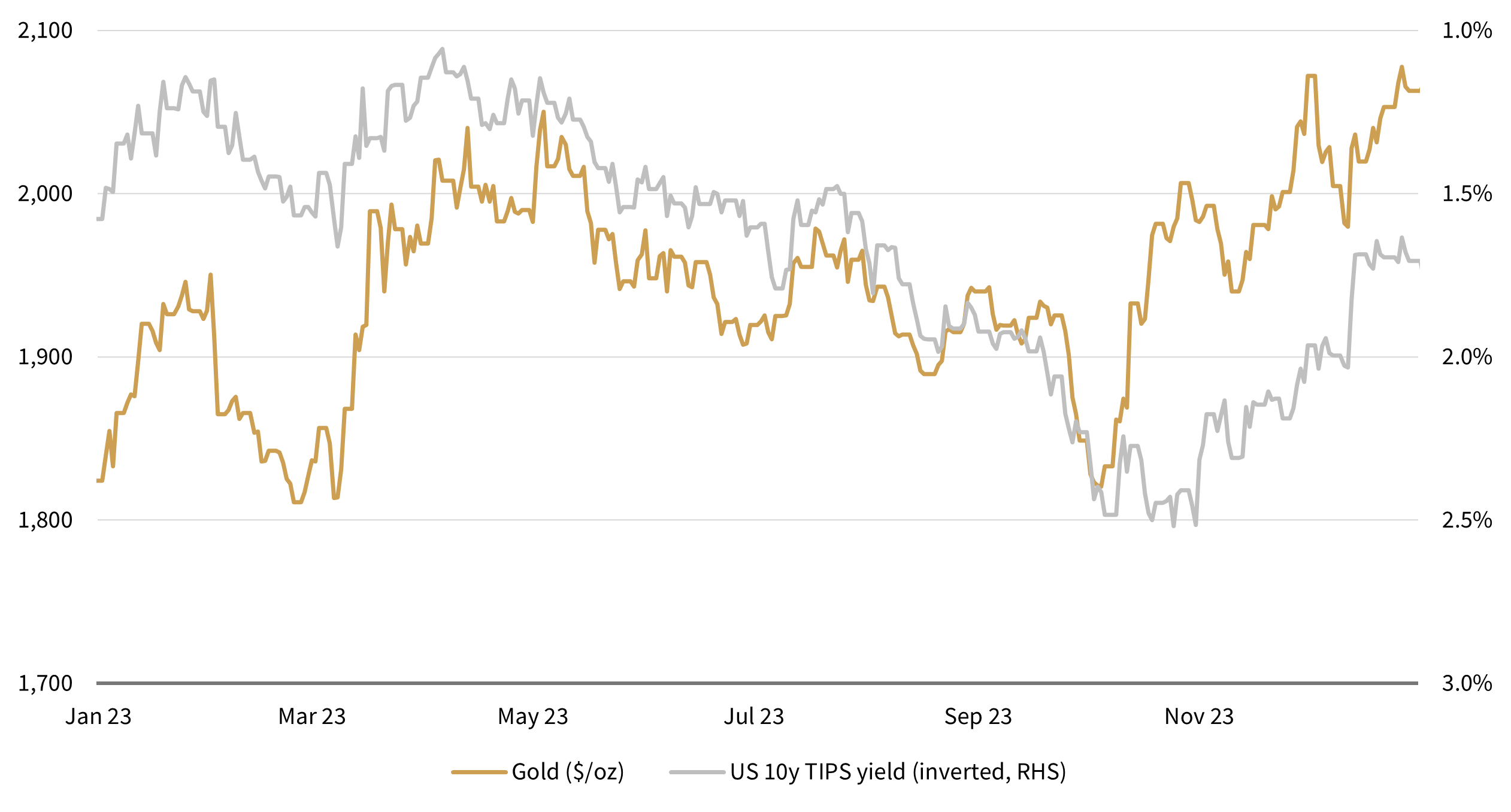

Gold continued to shine

Gold ($/oz) and the US 10-year TIPS real yield (%)

Source: Bloomberg

Gold’s hedging characteristics are variable at the best of times. Strong performance in 2023 (+13% in USD) has coincided with a period when inflation expectations have fallen and stock markets have rallied.

In reality, gold has not marched higher in a linear fashion, but has been whipsawed by the movement in real yields and the dollar. After surging initially in response to banking-related distress in March, between early May and early October gold erased all its earlier gains as the ‘real’ yield on US 10-year TIPS more than doubled to 2.5% – briefly the highest in over 15-years. It wasn’t until the final two months that gold once again regained its lustre, briefly rising to an all-time high of $2,077, although it remains below its inflation-adjusted high in 1980.

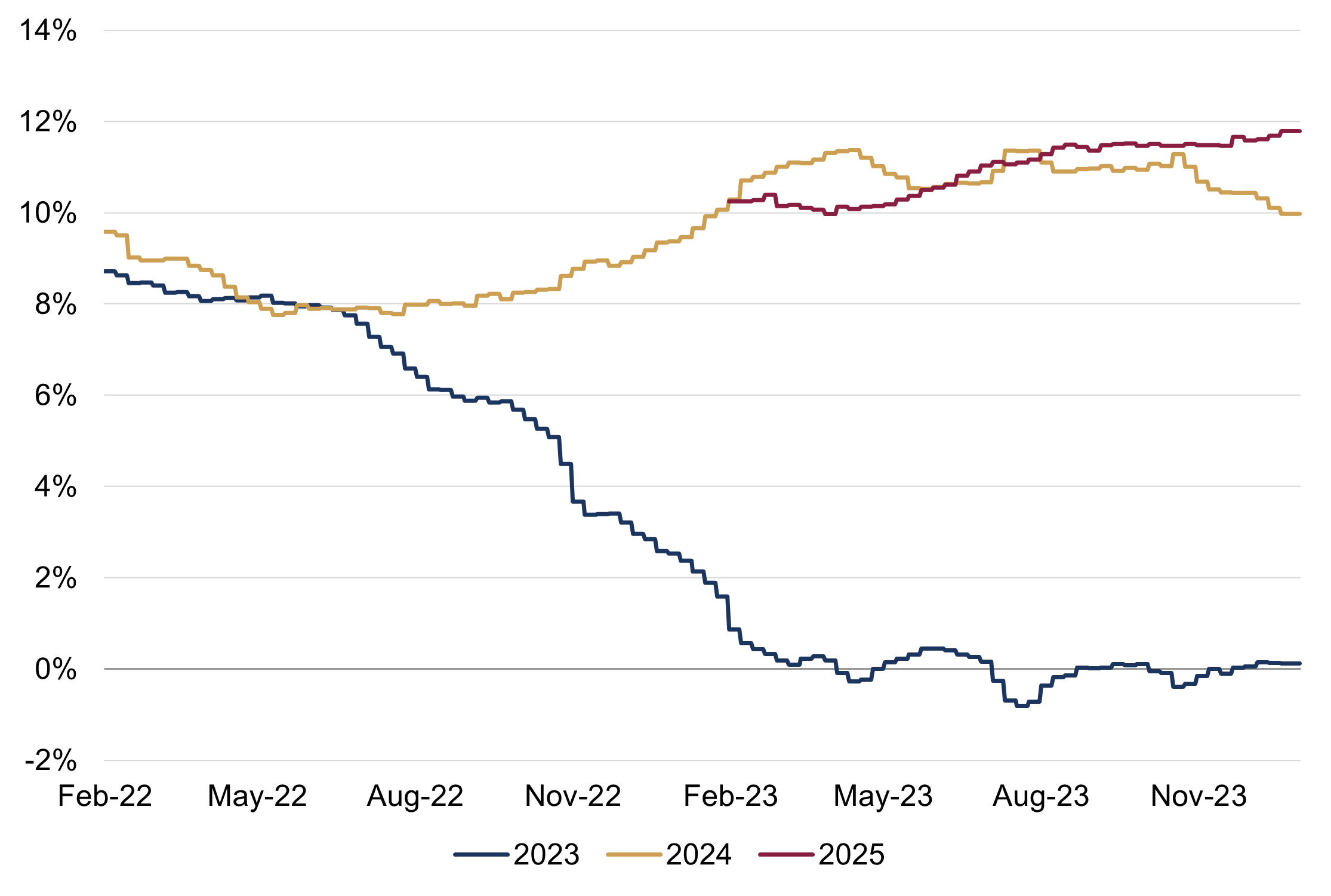

Stable corporate earnings

Evolution of global earnings estimates by calendar year (EPS, %)

Source: Rothschild & Co, I/B/E/S, Datastream

On the face of it, global earnings have barely budged in 2023. But that stagnant picture (pending the fourth quarter outturn) has been distorted and weighed down by the commodity-producing sectors (as it was flattered by the energy sector in 2022). Absent the material and energy sectors’ impact, the story is tracking a few percentage points higher for the full year. Digging deeper, some sectors – including discretionary, communications and industrials – have delivered strong earnings growth rates.

Looking ahead, after four consecutive quarters of modestly falling earnings (starting in Q3 2022), the third quarter may well have marked the low point (at least for now). Earnings estimates for 2024 and 2025 have been holding steady in recent months, pointing to low double digit (10-12%) growth ahead.

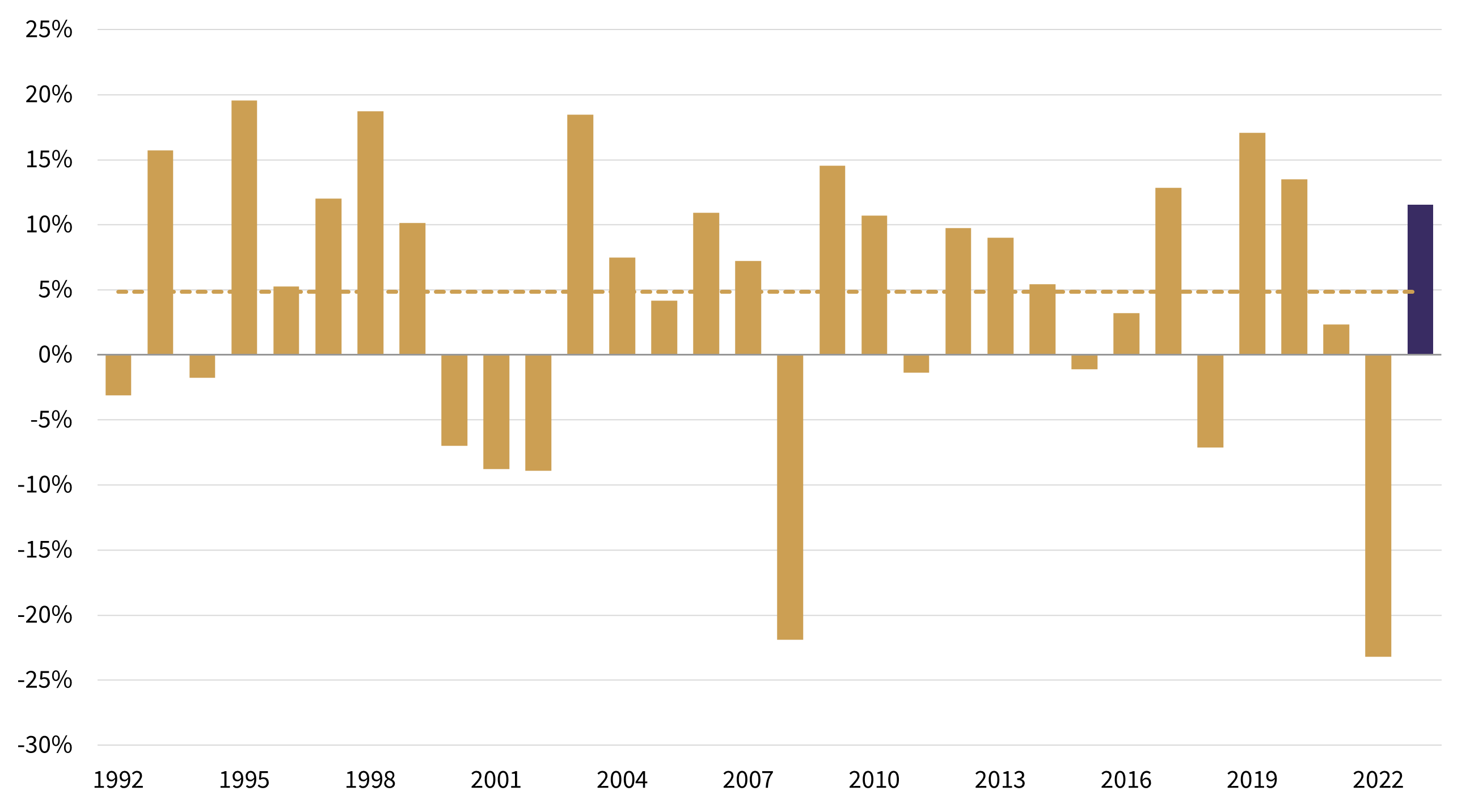

Stocks and bonds: a richer opportunity set?

Calendar year ‘real’ returns for a ‘60:40’ US balanced portfolio: 1992 to 2023

(60% developed market equities and 40% US 10-year treasuries)

Source: Bloomberg, MSCI

Index returns shown on a total return basis in US dollars (unhedged), gross of fees. Inflation based on US CPI

Over the past 30 years a typical ‘60:40’ balanced portfolio (comprising 60% US equities and 40% US treasuries) would have returned 5% above inflation (on average). 2023’s 11.5% (real) return appears to be a return to form following 2022’s difficulties.

Stocks and bonds have lost some valuation headroom in recent months, but looking ahead the risk of monetary overkill has faded – the big central banks seem poised to ease in the coming quarters – and expectations for corporate profitability are stabilising at healthy levels. Plausible long-term returns from the big two asset classes is more evenly balanced and remains ahead of prospective inflation – something that hasn’t been the case for quite some time.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.