Consensus outlook: mid-year update

Consensus underestimated the stickiness of inflation, the magnitude and duration of the tightening cycle as well as the resilience of the US economy. Inflation and the end of the tightening cycle will be key drivers of 2H23 asset performance.

What was expected for 2023 in Dec 2022?

- 2023 outlooks were all about the major central banks’ monetary policy tightening, the path of inflation and the potential benefits from the reopening of the Chinese economy.

- There was no clear consensus on whether the US economy might fall into recession. In Europe, a recession was broadly expected due to elevated energy prices, and higher inflation rates.

- Tighter monetary policy was expected to nonetheless trigger an economic slowdown which would bring inflation down and allow central banks to adopt less restrictive monetary policy. Specifically, consensus expected the Fed to deliver the last rate hike in 1Q23.

- For equity markets, consensus expected a difficult 1H23 in which markets could re-test the lows seen in 2022. Strategists were generally positive on the Chinese equity market which was expected to experience strong tailwinds from the reopening of the economy.

How has the outlook changed?

- The consensus was clearly underestimating the magnitude and duration of the tightening cycle.

- With inflation still considerably above the 2% target, monetary policy and the possibility of recession risk remain dominating themes. Consensus sees an end to the monetary tightening cycle in the US and in Europe in 3Q and 4Q, respectively but no immediate easing thereafter.

- Artificial Intelligence (AI) became the dominating theme for equity markets: the so-called ‘Magnificent Seven* stocks accounted for most of the S&P500’s year-to-date gains.

What does consensus expect now for 2023?

- Economics: On the economic outlook, expectations for a recession range from narrowly avoiding one to experiencing a milder setback. Inflation is likely to remain at elevated levels with core inflation above target, meaning that the Fed and ECB will not start to ease policy this year.

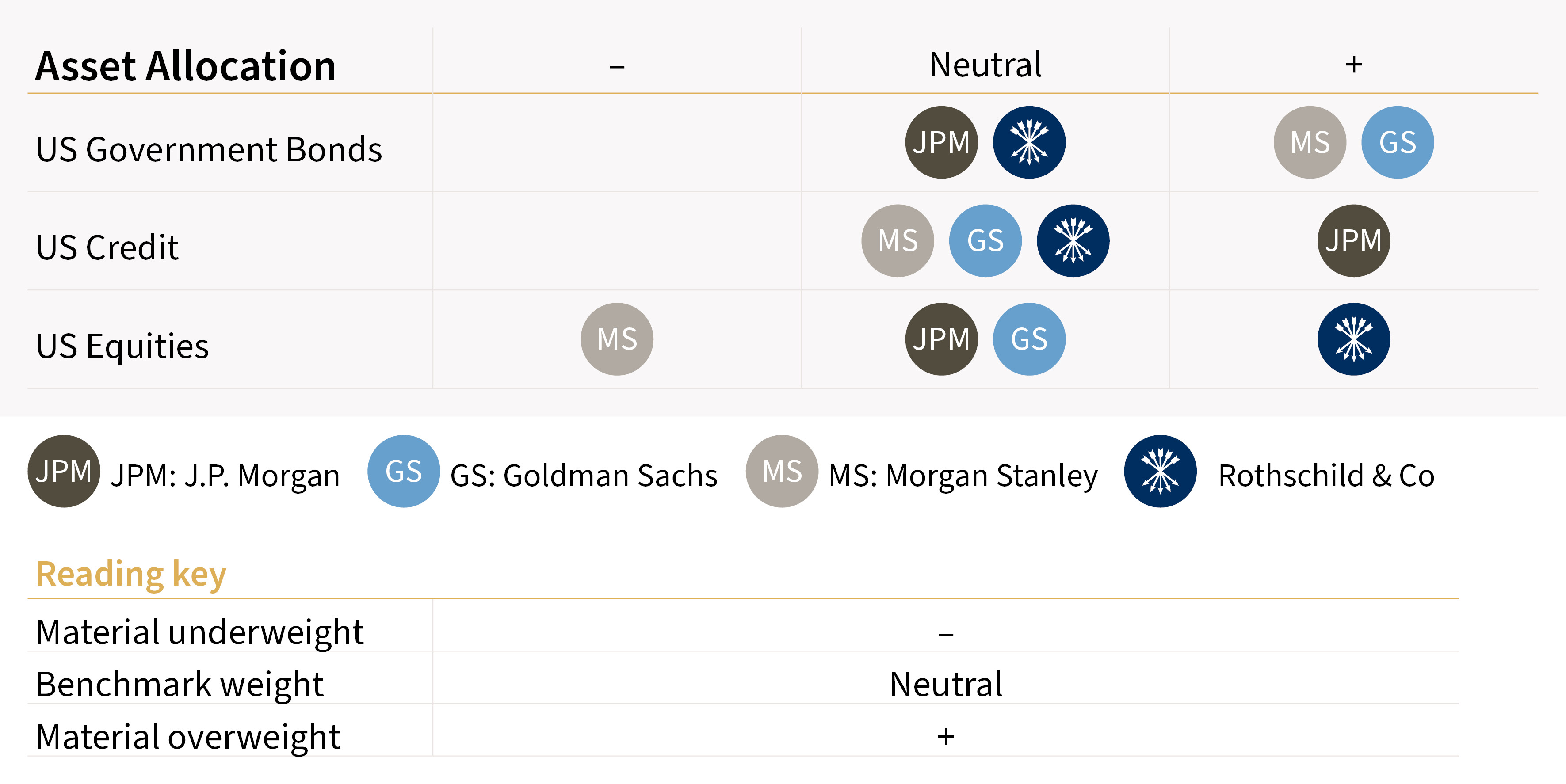

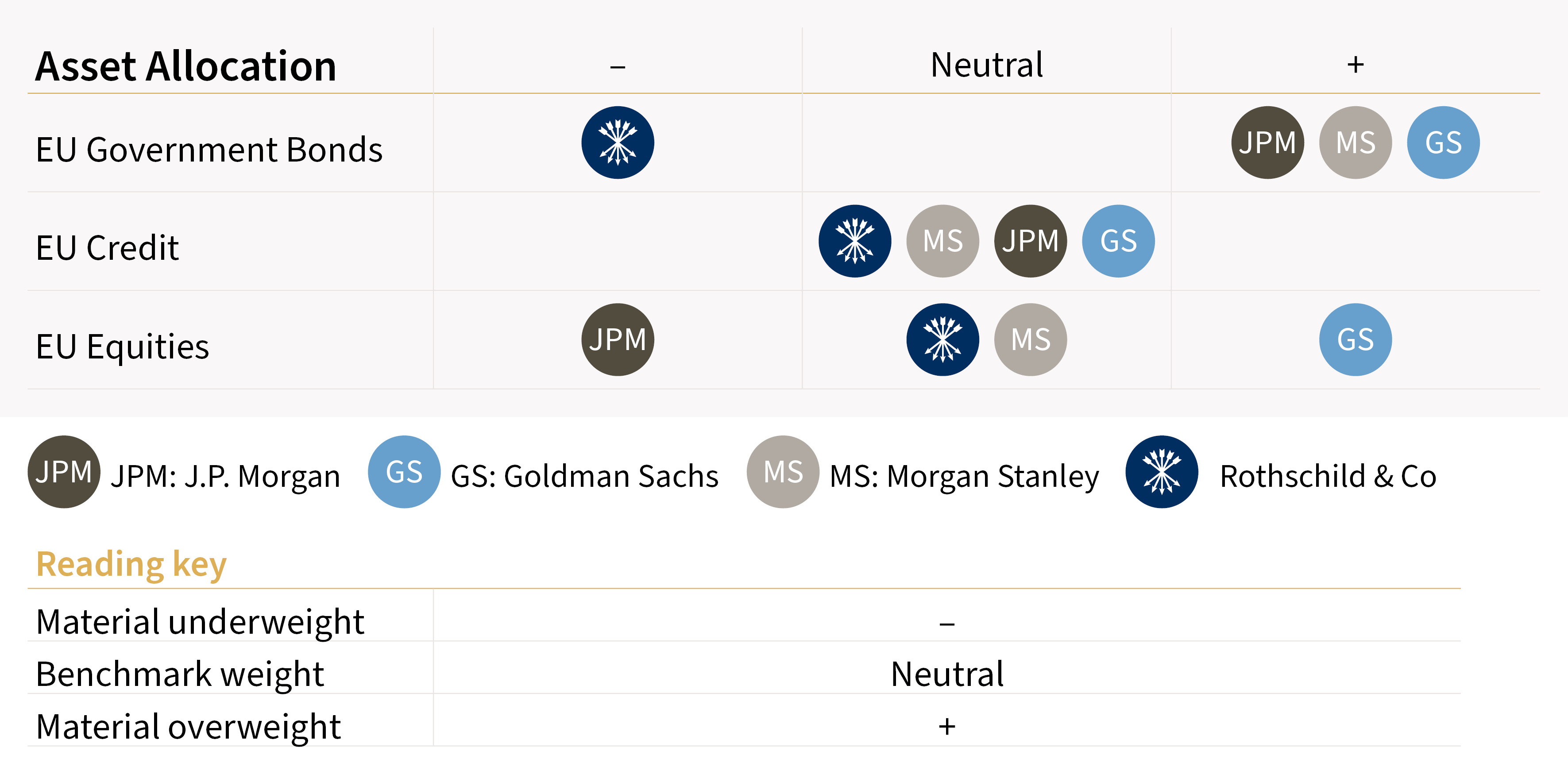

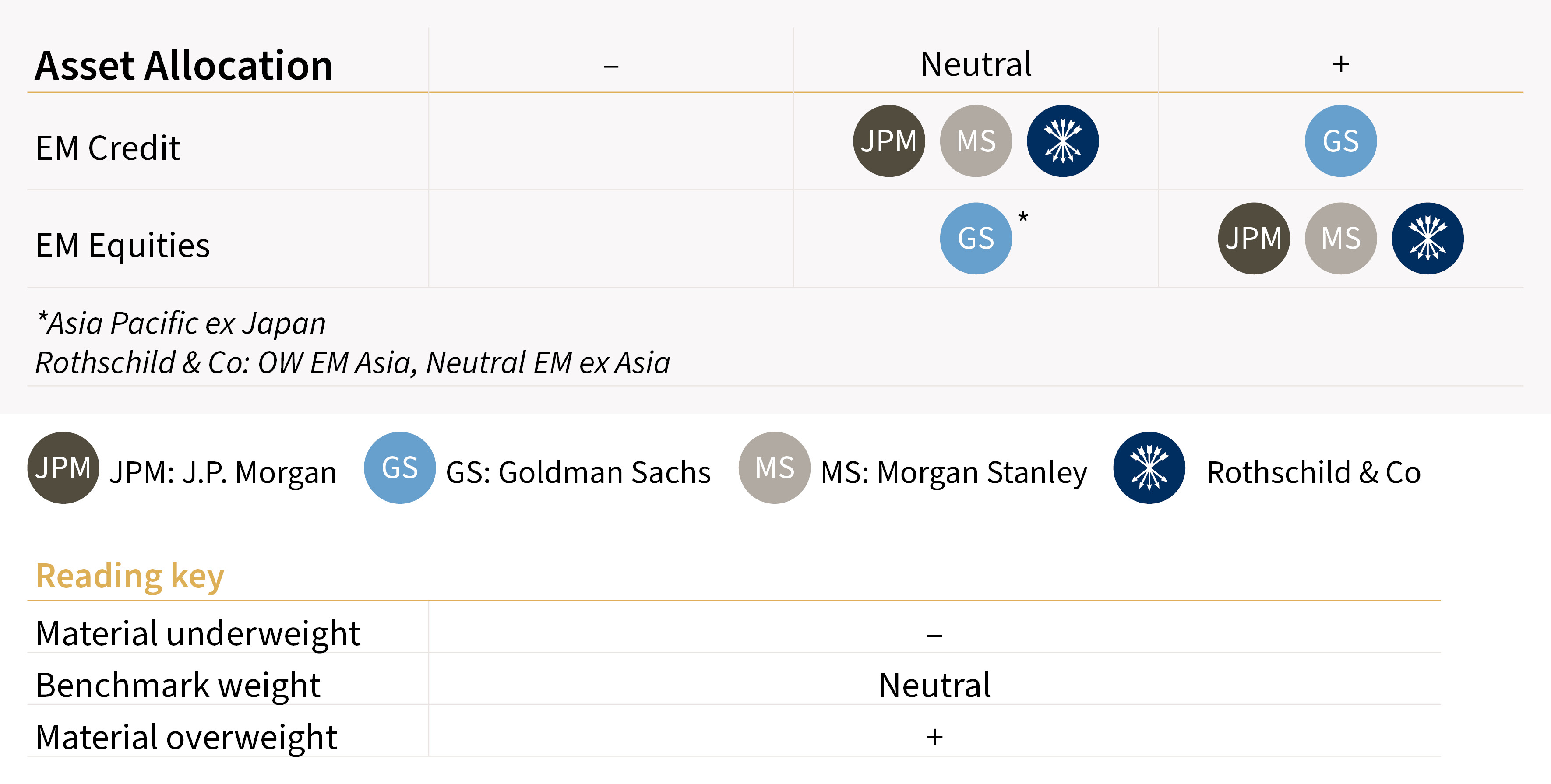

- Equities: Strategists’ views on US and European equities are mixed and range from negative to positive. Overall, there is a clear preference for Europe over the US. The overweight for Japan remains amid attractive valuations, ongoing corporate reforms, economic growth accelerating, and accommodative policy. In Emerging Markets, China is still a consensus overweight following a difficult 1H23.

- Rates: US, European and UK government bonds are considered attractive. 10-year yields are expected to end the year lower as the policy tightening cycle ends and economies slow. In Japan, on the other hand, consensus expects higher 10-year JGB yields following inflation revival and potential end of the Yield Curve Control strategy.

- Credit: Consensus prefers a defensive credit exposure and favours IG over HY credit with a regional preference for Europe over the US.

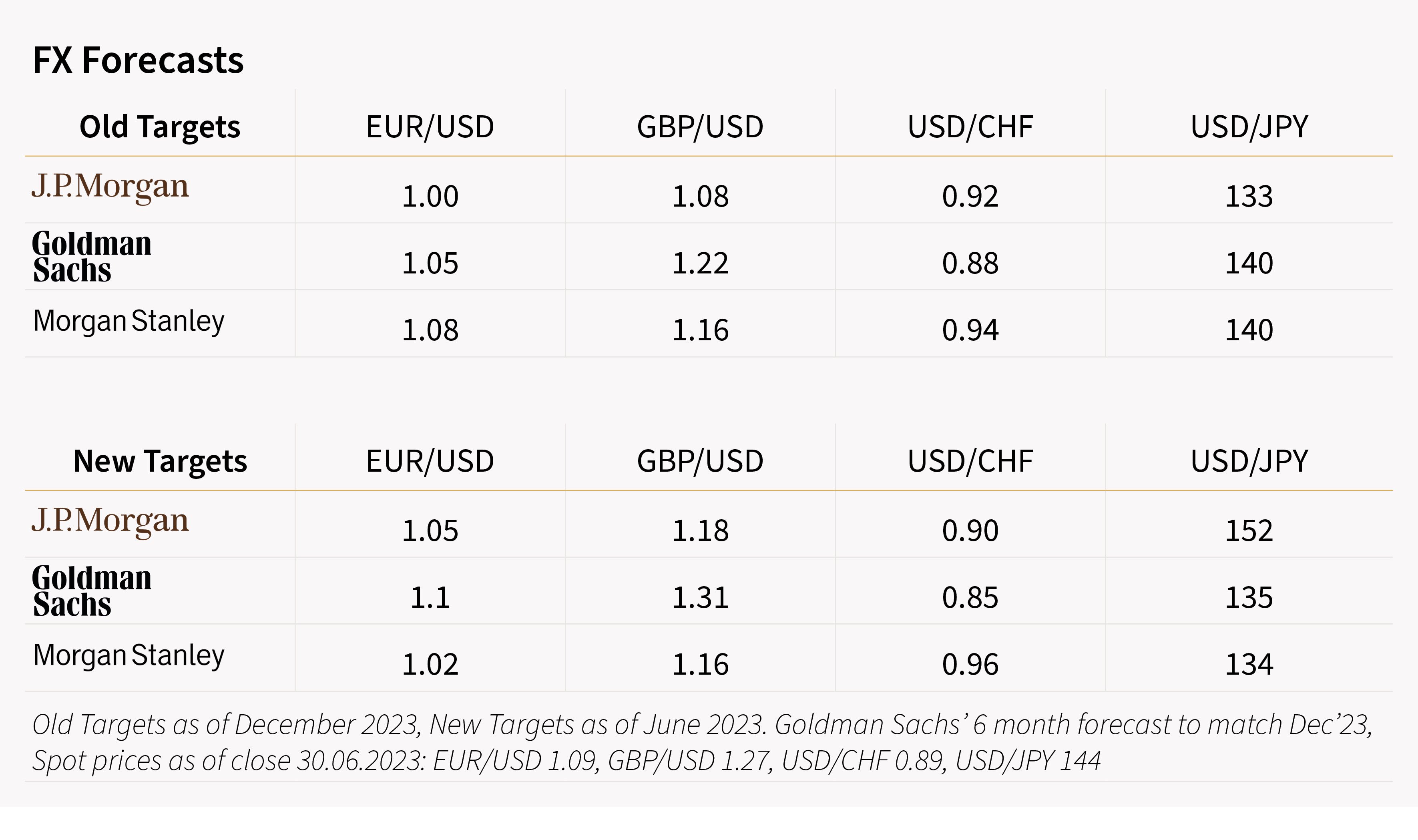

- FX: Consensus believes the USD could strengthen as it uniquely offers both defensive characteristics and positive carry in the G10.

- Commodities: Economic momentum needs to accelerate before opportunities re-emerge in the commodities space.

- Gold: Consensus sees the gold price supported by the ending of central banks’ tightening cycles. This is more likely to crystalize once the Fed starts cutting rates.

*Magnificant seven = Apple, Microsoft, Amazon, Google, Nvda, Meta & Tesla

More on Street View

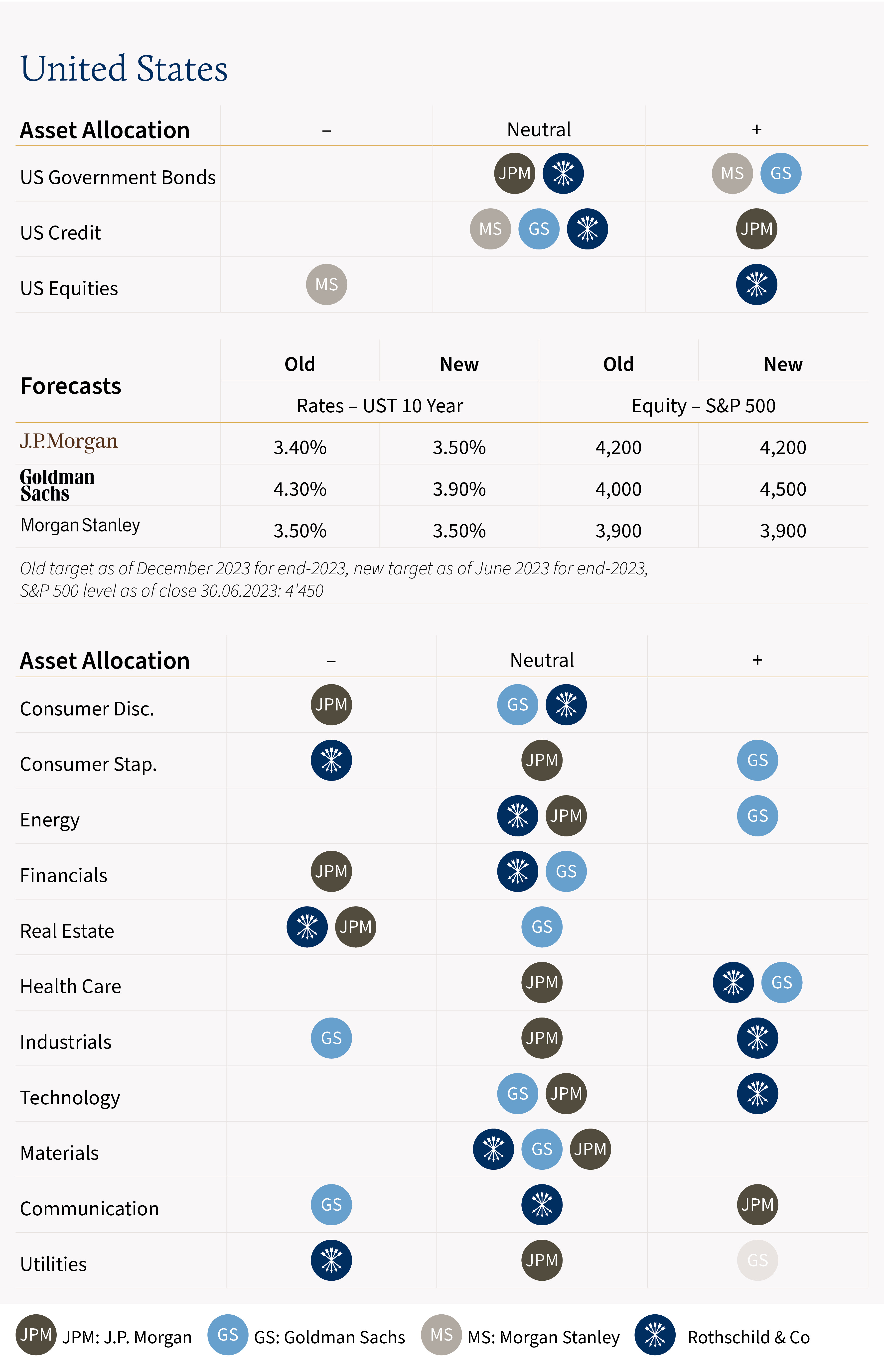

United States

Inflation normalisation and growth resilience will determine how 2H23 will unfold

Macro View

At the end of 2022, there was a wide range of recession forecasts, but most brokers expected the macroeconomic backdrop to deteriorate at some point in 2023, due to weaker consumption and rising unemployment rates. The other view was for inflation to peak in early 2023, and for disinflation to lead the Fed to cut rates in 2H23.

The main surprise was the resilience of the US economy with better-than-expected macro news flow despite regional bank failures in the early spring. While inflation peaked, core inflation remained sticky – resulting in a more hawkish central bank.

2H23 will be about understanding the extent to which tighter monetary policy has impacted the economy, and also how long monetary policymakers will remain committed to higher rates.

There is a growing consensus among analysts that a soft landing may be achievable: if so, a recession could be avoided in 2023. Real growth estimates for year-end have improved (from 0.3% to 1.4%) with growing talk of a possible “goldilocks” scenario.

Rates & Credit

From TINA to TARA*: with bond yields rising, 2023 was expected to attract fixed income flows and most brokers increased their allocation to the asset class throughout the year. Brokers started the year expecting Fed Fund rates to peak between 4.5% and 5.25% with the last hike to occur in 1H23 (before loosening by year-end).

The Fed turned out to be more aggressive than initially expected. Expectations are now for the Fed Fund rates to reach 5.25%-5.50% by year-end, a long plateau and no cuts before 2024. Concensus expect the 10yr yield to end the year at 3.53% versus 3.83% at the end of 1H23 and brokers have recently turned more constructive on duration. In credit, spreads have behaved relatively well in 1H23. Corporate fundamentals are expected to remain robust within both IG and HY markets. Expectations are for IG spreads to remain compressed into year-end (currently at 10yr average). While some brokers expect US default rates to continue to increase in 2H23 and subsequently in 2024, they expect HY spreads to behave well until 1H24 when many companies will start facing some refinancing needs.

Equities

At the end of 2022, brokers projected flat equity returns in the US for 2023. Volatility was expected to remain elevated, and there were some calls suggesting that the lows of 2022 could be re-tested (before regaining some ground closer to year-end).

During 1H23, the S&P 500 instead rallied by 17%. Positive returns were supported by resilient macro data, better-than-expected earnings and an AI-fueled rally. Volatility was contained and equity positioning significantly rose from last fall. However, beneath the surface, equities saw extreme divergences in performance across size, sectors and styles. Mega-cap tech stocks outperformed amid artificial-intelligence enthusiasm.

For 2H23, views are mixed: there is debate whether the worst of the earning recession is behind us. All brokers seem to agree that in the absence of Fed easing, 2H23 will become more challenging for stocks, due to “higher for longer” interest rates, higher positioning and more expensive valuations following the 1H23 rally. On average, brokers expect the S&P 500 to end the year around current levels. Market volatility is also unusually low, and some brokers expect it to move higher in 2H23.

Style preferences are once again mixed with a small majority of brokers still favouring growth stocks into year-end.

*TINA= ‘there is no alternative’

*TINA= ‘there is no alternative’

*TARA= ‘there are reasonable alternatives’

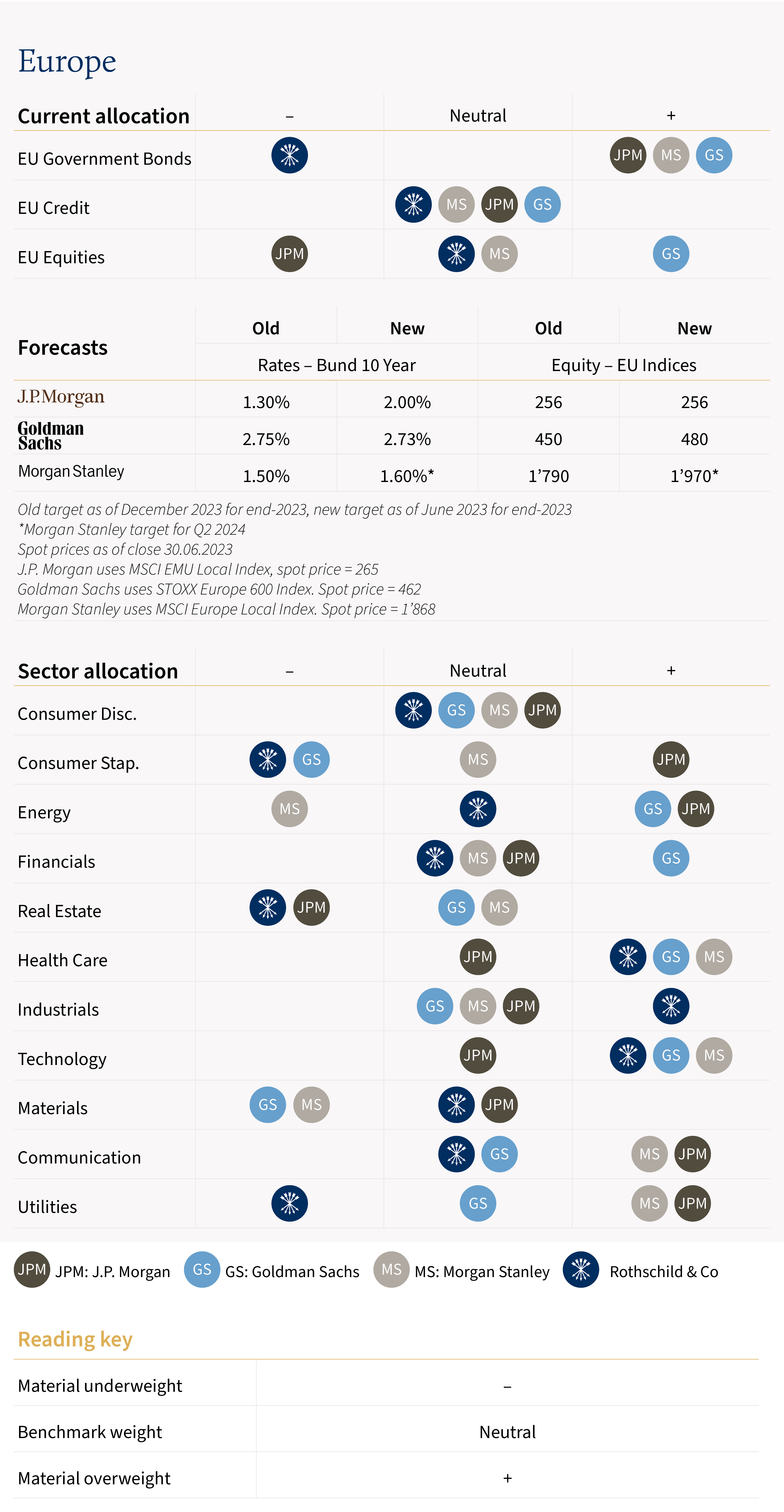

Europe

Strong first half for equities in Europe, focus remains on inflation and ECB’s peak in rates

Macro View

At the end of 2022, brokers pointed to higher inflation rates and energy prices as major risks in Europe. A moderate recession was expected.

Growth in the Eurozone was close to flat in 1H23, and business surveys started to diverge, with stronger services and weaker manufacturing. The labor market remained tight, with the unemployment rate at 6.5%, a record low.

In 1H23, Europe saw relief from last year’s energy price shock, following Russia’s invasion of Ukraine. Gas prices collapsed below pre-invasion levels, but the conflict remains a risk to the region’s stability.

Inflation has started to turn lower, as energy prices have fallen, and supply chain disruptions have eased. UK inflation dynamics look slightly different, with core inflation yet to turn lower – perhaps due to stronger nominal wage growth. Central banks in Europe are still tightening, although the ECB is now closest to its expected “peak” rate.

One important external factor for Europe is China’s reopening, which has proven to be patchy so far – as warned by some brokers at the end of 2022.

Rates & Credit

At the end of 2022, brokers expected that the ECB could end interest rate increases as early as 1H23.

However, monetary tightening continued in Europe in 1H23. Inflation has cooled but remains elevated, and two further hikes are expected by the ECB to 4%. The end of the BoE’s tightening cycle is likely further away due to stickier inflation figures. Overall, brokers have a bullish medium-term view on duration in Europe. The risk is if we see higher and/or delayed peaks in policy rates than anticipated.

On Credit, according to brokers, fundamentals in Europe remain solid: corporate leverage stands at low levels, cash balances are at near-record levels and interest coverage is healthy on aggregate. Banking sector concerns are more a US story. Spreads would need a clear signal on the macro front to widen meaningfully. Interest expenses should be watched (impact of low growth and higher rates), as well as future refinancing. This is especially relevant for high yield issuers, a segment where brokers expect default rates to rise to 3-4%.

Equities

At the end of 2022, brokers expected low single-digit returns as a moderate recession was forecasted (which could affect margins).

In 1H23, Europe performed better than anticipated. The Euro Stoxx 50 outperformed the S&P 500 up until May. Europe also experienced better breadth. In 1H23, the Euro Stoxx 50 median stock up was +17% compared to +5% for the S&P 500 over the same period.

During 1H23, European equities have experienced a stronger 2023 EPS revisions compared to other regions. Earnings revision ratios, which compare brokers’ upgrades versus downgrades, were positive and remain a slightly better than in the US. Companies in Europe have maintained margins intact so far. With a 12-month forward P/E at 12.7x, most brokers view the European stock market as attractive on an absolute and relative basis. However, some brokers view the monetary tightening lag on the economy as a potential headwind to equity returns.

In Europe, brokers generally favor defensives (e.g. Healthcare) over cyclicals, as well as growth-related sectors (e.g. Technology).

Emerging Markets

After a difficult 1H23, brokers remain optimistic on Chinese growth for 2H23

Macro View

- By the end of last year, the outlook for Emerging Markets (EM) was skewed to the upside supported by China’s expected economic rebound.

- However, while China’s GDP rebounded in 1Q23 – fueled by travel consumption and services activity –growth momentum declined significantly in 2Q23, amid low consumer confidence, a sluggish property market and uncertainty over the export sector. Despite these concerns, brokers generally expect limited stimulus measures in the near-term. Estimates are for China’s growth to stabilize in 2H23 (5.5% growth in 2023, revised lower from 5.70%).

- EM ex China growth is expected to slow below trend following aggressive hiking in Brazil, Chile and CEE. Some brokers view recession risks as a possibility and believe that markets may have underestimated this scenario.

Credit

- While most brokers agree that central banks are close to finishing rate hikes – viewed as a tailwind for the asset class – they believe that respective central banks will wait for further evidence of reduced inflation numbers before considering rate cuts.

- Most brokers remain neutral EM Credit with a slight preference for EM Local Currency bonds over Hard Currency (EUR and USD denominated). Brokers believe the latter should outperform once the EM central bank cutting cycle kicks-off and the broadening of EM disinflation materialize.

- Brokers expect EM Credit to deliver positive returns in 2H23, supported by lower US Treasury yields and higher carry but view limited performance from spread compression. EM IG credit spreads currently trade well below the long-term average and HY close to its long-term average.

Equity

- During 1H23, Emerging Market equities underperformed the MSCI World (+3.5% vs +14%). However, it is worth noting that EM equities experienced significant dispersion in 1H23 with Latam Equities (+19%) outperforming developed market versus China underperforming (-6.5%).

- For 2H23, brokers generally appear more constructive. EM Equities – especially EM Asia – may be supported by better earnings growth, low positioning, rate cuts by EM central banks, cheap valuations and potentially EM growth dynamics looking better than its DM peers. An appreciation in the USD in 2H23 could cap potential upside.

Commodities

Stable outlook for commodities in 2H23 before a potential rebound next year as central banks start easing the monetary policy

Commodity View

- At the end of 2022, there was a broadly optimistic outlook for commodities, especially energy. However, positive supply-related developments in 1H23 were key in alleviating the energy crisis experienced in 2022. Fear of a potential recession amid higher interest rates, and China’s growth disappointment led brokers to downgrade their 2023 estimates in 1H23. OPEC production cuts announcement – combined with a declining US rig count – may offer some stability to oil prices in 2H23. Brokers believe that oil prices may rebound in 2024 once central banks begin to ease policy, so long as a recession is avoided.

- As for gold, expectations were mixed entering 2023. Despite higher real yields, gold has performed well year-to-date. While some brokers expect gold to be supported for the remainder of the year, others believe it will remain range-bound until the Fed cuts rates, perhaps in 2024. Brokers also mention the strength of the US dollar and positive USD carry as other factors that could limit the upside potential for gold.

FX

After a difficult 1H23 for the USD, brokers turned more optimistic on the currency for 2H23

FX View

- Brokers started the year with expectations of a stronger USD in the 1H23 (following the appreciation seen in 2022), and a weak 2H23, assuming a rebound in global growth. Yet a reduction in interest rate differentials and a more resilient global economy were the main headwinds cited by brokers for a weak USD in 1H23. For 2H23, brokers now see recession fears as a potential tailwind for the USD.

- Brokers believe that the EUR could come under pressure in 2H23 in case EU versus US growth differential accentuates. They expect the ECB to follow the Fed decisions, albeit with a lag and therefore do not expect a hawkish ECB stance to drive the EUR higher in 2H23.

- In Switzerland, brokers have upgraded their outlook for CHF due to a stricter focus on inflation versus its European peer.

- The Japanese Yen outlook appears more ambiguous: brokers have a wide range of year-end targets. The new BoJ Governor Ueda has not yet signaled changes to future yield curve control policy despite core inflation rising. JPY strength seems contained for the rest of the year.

Forecasts for end 2023

Disclaimer & more information

Notes and terminology

FED = Federal Reserve

ECB = European Central Bank

OPEC = Organization of the Petroleum Exporting Countries

EM = Emerging Markets

DM = Developed Markets

EPS = Earnings per Share

GFC = Global Financial Crisis

QE = Quantitative Easing

AI = Artificial Intelligence

ESG = Environmental, Social and Governance

CEE = Central Eastern Europe

IG = Investment Grade

HY = High Yield

TINA = There is no alternative

TARA = There are reasonable alternatives

Forecast sources

Global

Goldman Sachs, Global Views: Lower Risks, Higher Rates, as of 6th June 2023

J.P. Morgan, 2023 mid-year outlook – Global Research, as of 22nd June 2023

Morgan Stanley 2023 Global Strategy Mid-Year Outlook – Crunch Time, as of 4th June 2023

United States

Goldman Sachs, US Weekly start – Lifting our S&P 500 target to 4500 as narrow YTD rally broadens beyond mega cap tech , as of 8th June 2023

Jefferies, JefMacro Weekly – It just ain’t that bad; the Powell paradox solved?, as of 25th June 2023

Goldman Sachs, Global Views: Lower Risks, Higher Rates, as of 6th June 2023

J.P. Morgan, 2023 mid-year outlook – Global Research, pages 3-4, 7-9, 15-17, 22-24 as of 22nd June 2023

Morgan Stanley 2023 Global Strategy Mid-Year Outlook – Crunch Time, page 1-3, 14, 26-29, , as of 4th June 2023

Europe

Goldman Sachs, Strategy Espresso: 2H 2023 Outlook: European Equities – Any further returns?

J.P. Morgan, 2023 mid-year outlook – Global Research, page 11-12, 20, 26-27

J.P. Morgan, European Credit Strategy Mid-Year Outlook – The Waiting Game

Morgan Stanley 2023 Global Strategy Mid-Year Outlook – Crunch Time, page 11-19, 26-29

Emerning Market

J.P.Morgan, Global Emerging Markets Research - Emerging Markets Outlook and Strategy, as of 9th June 2023

J.P.Morgan, Global Markets Research - China Equity Strategy, as of 12th June 2023

Goldman Sachs, EM Sovereign Credit Monitor – Squeezing into Summer, as of 6th July 2023

Morgan Stanley, 2023 Midyear Investment Outlook: Soft Landing - Hard Choices, as of June 13th 2023

Foreign exchange

J.P. Morgan, Mid-year outlook: Ten questions (and answers) on FX in 2H23, as of 23rd June 2023

Goldman Sachs, Global FX Trader – Get Real!, page 8, as of 16th May 2023

Morgan Stanley 2023 Global Strategy Mid-Year Outlook – Crunch Time, page 45, as of 4th June 2023

Commodities

J.P. Morgan, 2023 mid-year outlook – Global Research, pages 5, 32-33, as of 22nd June 2023

Goldman Sachs, Oil Analyst: The Energy Crisis and Long-Run Oil Prices, as of 23rd June 2023

Morgan Stanley, Global Strategy Mid-Year Outlook: Crunch Time, pages 35-37, as of 4th June 2023

Note: We select, when available, the closest target to the end of 2023, depending on the counterparty (stated as end of 2023, 4Q2023, 6-month forecast or, alternatively, 2H2023). Forecasts might be changed by counterparties depending on market circumstances

Disclaimer

This document is produced by Rothschild & Co Bank AG, Zollikerstrasse 181, 8034 Zurich, for information and marketing purposes only. It does not constitute a personal recommendation, an advice, an offer or an invitation to buy or sell securities or any other banking or investment product. Nothing in this document constitutes legal, accounting or tax advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Bank AG as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever.

In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice. Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. Neither this document nor any copy thereof may be sent to or taken into the United States or distributed in the United States or to a US person. Rothschild & Co Bank AG is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA.