Strategy blog: The credit cycle

Received wisdom has it that bond investors are smarter than stock investors. The corollary is that credit analysts are more ruthlessly focused on fundamentals – cash flow, leverage, and the risk of default. Return of capital trumps return on capital.

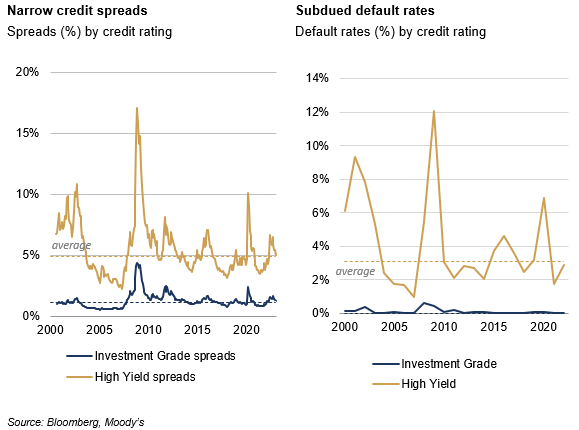

But if bond markets are the best proxy for macroeconomic risks, then credit investors appear remarkably sanguine about the outlook: credit spreads (a measure of corporate stress) have narrowed, and default rates remain low. At the same time, global bond issuance in January kicked off 2023 in record fashion - there is no shortage of demand for new issues.

At the risk of understating recent events, it has been a challenging and unusual cyclical backdrop over the past few years. Businesses are more constrained than governments in managing untenable debt positions – their credit is less good. But so far, the widely predicted collapse of corporate bond prices, and a wave of defaults, have failed to materialise.

Has the reckoning been avoided or merely delayed? The arrival of higher interest rates, lacklustre earnings, and greater competition for capital may present some challenging headwinds to indebted companies.

Deleveraging is underway

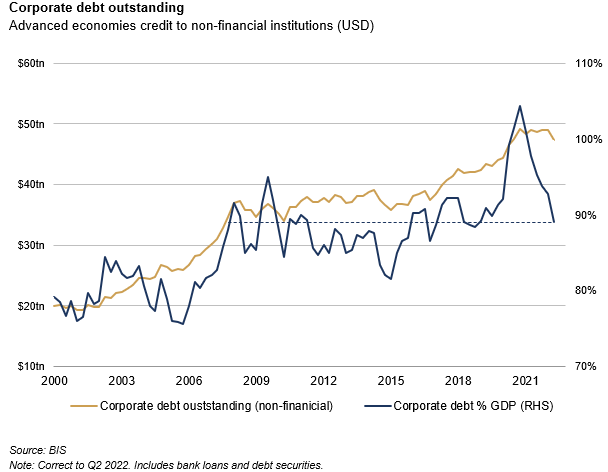

Corporate distress during the pandemic was swiftly quelled by abundant liquidity and direct policy support, which enabled many to companies to borrow unencumbered through the crisis. Yet the big surge in corporate issuance in 2020 was partly reversed by deleveraging, with debt peaking towards the latter half of 2021.

More remarkable though has been the big retreat in corporate debt relative to output. For much of the past two decades, debt issuance has outstripped economic growth, but the arrival of faster nominal growth (partly driven by inflation surging higher) and on ongoing deleveraging has seen a precipitous decline in the relative debt position: currently close to 90% of GDP (down from from 104% at the end of 2020). On this basis, the corporate debt stock is unchanged over the past 15 years.

Robust fundamentals

Total liabilities viewed in isolation tell you little about whether a company is a ‘going concern’ – is it able to repay or service those debts? How is that stock of debt distributed across different ratings and borrowers?

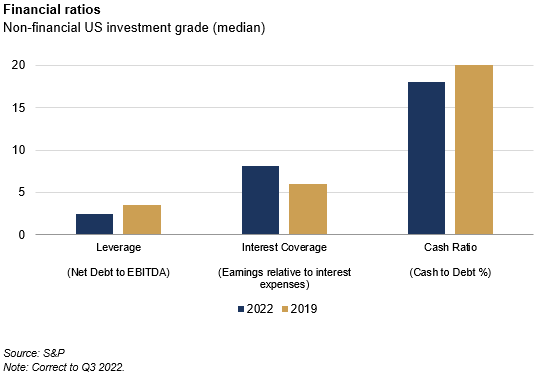

Issuance slowed dramatically in 2022, not only reflecting the more challenging market backdrop and higher interest rates, but the fact that many companies had simply taken advantage of lower yields through 2020 and 2021 - recapitalising their balance sheets and building sizable cash buffers in the process. The result is a more stable and less interest rate sensitive stock of outstanding debt.

Leverage ratios for high quality US borrowers, for example, have fallen relative to pre-crisis levels: the median net debt to EBITDA multiple has fallen to c. 2.5x (Q3 2022). Another important measure assessing financial viability is interest coverage (the inverse of the leverage ratio) - how readily a company can pay the interest on its outstanding debt from its pre-tax earnings – which has risen too. The cash ratio – a liquidity measure which reflects cash available to cover short-term obligations – has fallen slightly, despite initially surging higher during the pandemic.

Equally, the long maturity profile of that debt – close to 9 years for higher quality investment grade names - suggest there is no imminent maturity wall, rather a steady stream of bonds that need to be refinanced in the coming years. Bottom-up analyses indicate that only a quarter of outstanding corporate bonds (across the credit spectrum) will mature before 2025.

While some indebted sectors and companies may well face a reckoning – particularly those at the sharp end of the interest rate cycle – there are tentative signs that we may be turning a corner on credit ratings. For much of 2022, credit rating downgrades (by the major rating agencies) eclipsed upgrades by a substantial margin, but this trend appears to be slowing in 2023.

Inexpensive valuations

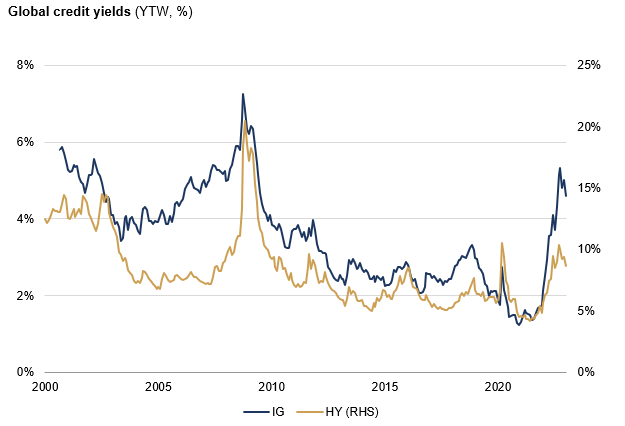

As for investors on the other side of the table, there is no doubt that 2022 was painful. Yields more than doubled last year across both high-quality investment grade bonds and low-quality high yield (‘junk rated’) bonds, which corresponded to double-digit losses (in total return terms) over the course of the year.

But with the big fall in prices, the arrival of higher yields presents a new opportunity. The current yield on high quality (investment grade) corporates is close to 5%, while high yield is offering an 8-9% running yield at present – well in excess of prospective inflation (and arguably comparable to the prospective return on stocks).

Credit spreads are currently close to long term averages and are clearly not discounting a weakening economic backdrop or the risk of further credit downgrades. But there remains a sizeable yield cushion to buffer against possible downgrades or losses through defaults. Indeed, if economic momentum continues, and earnings – which have yet to collapse – start to track higher once again, then those credit spreads could narrow even further.

Of course, whether those bonds investors are always right is a moot point. After all, many investors – like us – invest in both bonds and stocks…

Ready to begin your journey with us?

Past performance is not a guide to future performance and nothing in this blog constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.